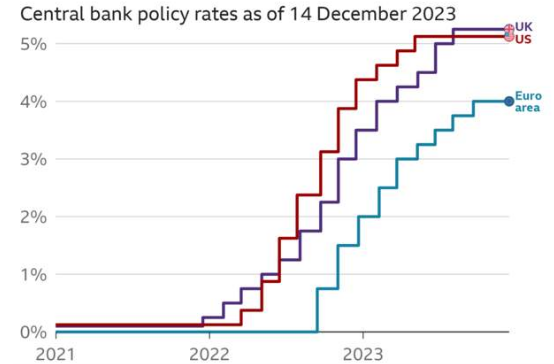

UK interest rates have been held at 5.25%. This is the third time in a row the Bank of England has opted to hold rates the same.

The decision, which was widely expected by financial markets, means borrowing costs will remain at their highest level for 15 years.

the Bank of England’s Monetary Policy Committee (MPC) voted 6-3 to keep rates at a 15-year high.

There was reportedly no discussion of cutting interest rates, and it’s still concerned that price rises might be stickier in the UK economy than in the U.S. or Eurozone.

The U.S. yesterday, 13th December 2023 indicated that 2024 could see three interest rate cuts. No such indication was forthcoming from the UK.

The Dow Jones Industrial Average (DJIA) hit a new all-time high, on 13th December 2023. It closed at 36799 surpassing its previous record of 36585points that it had set on 4th January 2022. This was the fourth consecutive record close for the index.

Record high

The Dow’s record high was driven primarily by the Fed holding the interest rate at 5.5% and signalling that it expects to cut interest rates three times in 2024 to stimulate growth and inflation.

Other factors such as strong corporate earnings, optimism about the economic recovery from the COVID-19 pandemic, the emergence of AI and its effect on the economy and for a U.S. ‘soft landing’ all played their part.

Dow a bellwether for the U.S. economy

The Dow is not only a measure of stock market performance, but also a reflection of the overall health and confidence of the U.S. economy. It is often used as a benchmark for investors and analysts to evaluate their portfolios and strategies. The Dow is also closely watched by policymakers and media outlets as a measure of public sentiment and expectations.

Dow hits new all-time high

Dow hits new all-time high

The Dow, in intraday trading, continued to climb to over 37200.

Fed holds U.S. rates at 5.5%, indicates three cuts coming in 2024

The Federal Reserve on Wednesday 13th December 2023 held its key interest rate steady for the third time in a row and set the scene for multiple rate cuts in 2024 and 2025.

With inflation easing and the economy holding up policymakers Federal Open Market Committee policymakers voted unanimously to keep the rate in a range between 5.25%-5.5%.

Possible three Fed rate cuts pencilled in for 2024

Along with the decision to stay on hold, the FOMC pencilled in at least three rate cuts in 2024, assuming quarter percentage point increments. That’s less than market pricing of four, but more aggressive than what officials had previously indicated.

Markets had widely anticipated the status quo decision which could end a cycle that has seen 11 hikes, pushing the interest rate to its highest level in more than 22 years. There was uncertainty, though, about how ambitious the FOMC might be regarding policy easing.

The FOMC’s so called ‘dot plot’ of individual members’ expectations indicate another four cuts in 2025, or a full 1%. Three more reductions in 2026 would take the Fed rate down to between 2%-2.25%, close to the longer-term outlook, though there were considerable difference in the estimates for the final two years.

Dow at new all-time high!

Following the Fed update the Dow Jones Industrial Average jumped more than 400 points, surpassing 37,000 for the first time creating a new Dow all-time high.

In a significant development that has raised concerns among investors and policymakers worldwide, China’s debt outlook has been downgraded as the country grapples with a slowing economy. This move reflects growing apprehensions about the sustainability of China’s economic growth and its ability to manage its burgeoning debt.

Moody’s issued the warning as it cut its outlook on the government’s debt to negative, from stable. China said it was disappointed by the move, calling the economy resilient. China also reported to have said it is unnecessary for Moody’s to worry about China’s economic growth prospects and fiscal sustainability.

Rapid Expansion

For years, China’s rapid economic expansion has been the engine of global growth, but recent trends indicate a deceleration. The once double-digit growth rates have now tapered, with projections suggesting a further slowdown in the coming years.

China exports

This deceleration is attributed to various factors, including trade tensions, demographic shifts, and a maturing economy.

Downgrade

The downgrade, announced by a prominent credit rating agency recently, underscores the risks associated with China’s increasing debt levels. The country’s total debt, which includes government, household, and corporate debt, has climbed to around 85%* of its GDP. This debt accumulation is partly due to the government’s efforts to stimulate the economy through infrastructure spending and lending to state-owned enterprises.

Property Sector

The property sector, a significant pillar of China’s economy, has also shown signs of strain. High-profile defaults and a cooling housing market have added to the concerns, prompting fears of a ripple effect across the economy. The government’s crackdown on excessive borrowing and speculative investments has further tightened liquidity, impacting developers and homeowners alike.

The burden of debt sits heavy in China’s property sector.

Response

In response to the downgrade, China’s finance ministry has expressed confidence in the country’s economic resilience. Officials argue that the fundamentals of the Chinese economy remain strong, with continued efforts towards high-quality development and structural reforms. They assert that the concerns raised by the credit agencies are overstated and that China’s fiscal position remains robust.

Warning signal

Nevertheless, the downgrade should serve as a warning signal. It highlights the need for careful fiscal management and policy adjustments to navigate the challenges ahead. As the global economy faces uncertainty, the world will be closely watching how China addresses its debt dilemma and maintains its trajectory of growth.

This situation presents a complex puzzle for China’s leadership, balancing the goals of economic stability and sustainable development. The outcome will have far-reaching implications, not just for China but for the entire global economy.

The world awaits to see how China will write the next chapter in its remarkable economic story. If this goes wrong – it will go wrong in a big way.

Update Friday 8th December 2023

China’s top decision-making body of the ruling Communist Party on Friday said that the country’s fiscal policy ‘must be moderately strengthened’ to stimulate economic recovery, according to state-run news outlet.

85%* debt to GDP ratio

China’s debt-to-GDP ratio was recorded at around 77% of the country’s Gross Domestic Product in 2022. This ratio is an important indicator of a country’s economic health, reflecting its ability to pay back its debts. This ratio has been on the rise in recent years, indicating an increase in national debt relative to the GDP. For instance, the ratio was around 23% in 2000 and grew to 34% in 2012, with a significant jump to the current level.

China’s projected debt to GDP ration

Forecasts suggest that China’s debt-to-GDP ratio could reach 104% by 2028

It’s important to note that such figures can vary and should be interpreted within the context of each country’s economic structure and policies.

The economy fell by 0.3% October, after growth of 0.2% in September 2023.

UK GDP is 0.0%

The UK economy shrank more than expected in October 2023, as higher interest rates hit consumers. The bad weather didn’t help either.

Household spending has been dented by rate rises as the Bank of England tries to tackle inflation. It is due to make its next rate decision on Thursday 14th December 2023. Retail and tourism were hit by severe weather hit the UK in October 2023.

Analysts had predicted that the economy would fall by just 0.1% but services, manufacturing and construction sectors all contracted more than expected.

The UK economy has been stagnating and the Prime Minister has promised to speed up economic growth. But no significant recovery is expected until January 2025.

Chancellor’s spin

Commenting on the latest figures, Chancellor Jeremy Hunt said it was ‘inevitable economic growth would be subdued, whilst interest rates are doing their job to bring down inflation.’

The figures underline the ongoing impact of the cost-of-living crisis and the tools employed by our ‘decision’ makers on our behalf.

Prices across a wide spectrum of goods and services moved slightly higher in November 2023 but were mostly in line with expectations, thus further easing pressure on the Federal Reserve.

The consumer price index, a closely watched inflation gauge, increased 0.1% in November, and was up 3.1% from a year ago, the U.S. Bureau of Labor Statistics reported Tuesday 12th December 2023.

While the monthly rate indicated a pickup from the flat CPI reading in October 2023, the annual rate showed another decline after hitting 3.2% a month earlier.

The two most significant events for gold demand in 2023 were the collapse of Silicon Valley Bank and the Hamas attack on Israel, the World Gold Council(WGC) said, estimating that geopolitics added between 3% and 6% to gold’s performance over the year.

The WGC estimated that central bank demand added 10% or more to gold’s performance in 2023 and said even if 2024 does not reach the same heights, above-trend buying should still offer an extra boost to gold prices.

The precious metal broke through $2,100 per ounce on Monday 4th December 2023 in intra-day trading, before moderating slightly. Spot gold prices were hovering at around $2,030 per ounce Friday 8th December 2023.

Gold price year to date chart

What is the World Gold Council

The World Gold Council (WGC) is a market development organization for the gold industry. It works across all parts of the industry, from gold mining to investment, with the aim of stimulating and sustaining demand for gold. The council sets standards, strengthens markets, and shapes the global conversation about gold. It was established to promote the use of and demand for gold through marketing, research, and lobbying.

The council includes 33 members, many of which are gold mining companies.

The latest U.S. job data indicates that job growth accelerated in November 2023, with seasonally adjusted non-farm payrolls increasing by 199,000.

The unemployment rate has dropped to 3.7%, even as more workers entered the labour market. This points to underlying strength in the labour market and is a positive sign for the U.S. economy.

U.S. job creation chart January 2022 – November 2023

U.S. job creation chart January 2022 – November 2023

Stocks had risen as investors awaited these latest employment figures, which are closely watched as an indicator of potential moves by the central bank on interest rates.

Mixed reaction

Markets showed a mixed reaction to the report, with stock market futures modestly negative while Treasury yields surged. Job creation showed little signs of slowing as payrolls grew even faster than expected and the unemployment rate fell despite signs of a weakening economy.

Good news for the U.S. economy but Treasury yields are on the up again.

U.S. citizens have accumulated a record-breaking $1 trillion in credit card debt.

The Federal Reserve’s interest rate hikes through 2023 have caused average interest rates for credit cards to spike to more than 22%. Rates on retail credit cards are even higher, nearing 29% on average.

Despite rising costs and higher borrowing rates, a record number of consumers shopped over the Thanksgiving holiday weekend. The National Retail Federation found that more than 200 million consumers went shopping that weekend, more than the 196.7 million shoppers who turned out in 2022.

Retailers Macy’s and other larger retailers have issued warnings about a slowdown in repayments on their credit cards, highlighting a potential risk to retail revenue this holiday season.

The resilience of the American consumer will continue to be tested by the still-rising costs of groceries, fuel, energy and housing.

Interesting fact

The U.S. credit card debt is approximately equal to the size of Apple’s market cap of $1 trillion.

A report published Tuesday by the Kick Big Polluters Out coalition found that at least 2,456 fossil fuel lobbyists registered to attend the two-week long summit. That’s more than almost every other country delegation, except for Brazil (3,081) and COP28 host the United Arab Emirates (4,409), the report said.

Supporters say the number of fossil fuel lobbyists attending the talks is ‘beyond justification’ and demonstrates that polluting industries are seeking to advance a fossil fuel agenda.

Others however say that Big Oil’s participation at COP28 should be welcomed.

Unabated

There’s also a debate about whether an agreement should centre on abated fossil fuels, which are trapped and stocked with carbon capture and storage technologies. Unabatedfossil fuels are largely understood to be produced and used without substantial reductions in the amount of emitted greenhouse gases.

Delegates at the beginning of COP28 sealed a landmark deal to help the world’s most vulnerable countries pay for the impacts of climate disasters. To me, that suggests it is okay to carry on with business as usual because the industry can throw money at the poorer people suffering at the brunt end of climate effects.

Announcements at COP28 have sought to help decarbonize the energy sector, with nearly 120 governments pledging to triple renewable energy capacity by 2030, recent news reports show.

Whichever way we care to spin this, we are nowhere near ready to switch to renewables.

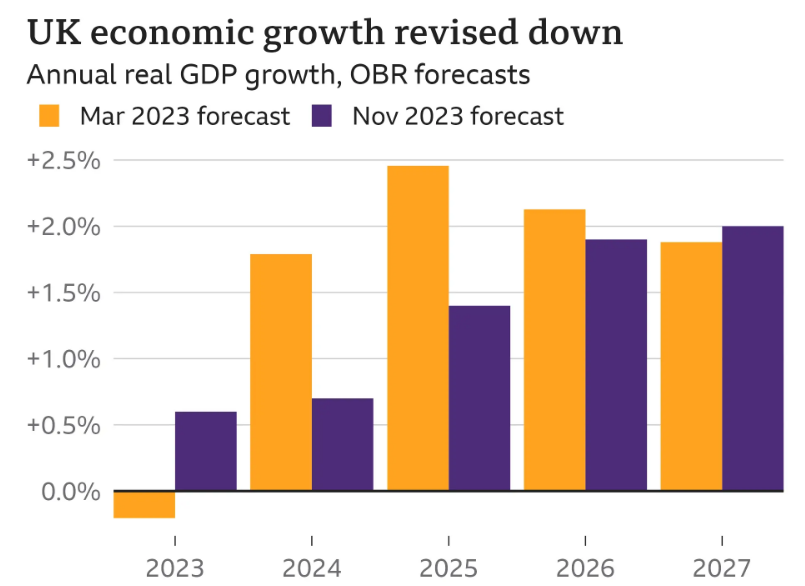

The UK economy will grow much more slowly than expected in the next two years as inflation takes longer to fall, the Office for Budget Responsibility (OBR) says.

Are we locked in a never-ending austerity cycle?

Living standards are also not expected to return to pre-pandemic levels until 2027-28, the Office for Budget Responsibility (OBR) said. It comes as the chancellor announced tax cuts and a rise in benefits in his 2023 Autumn Statement.

The OBR publishes two sets of economic forecasts a year, which are used to independently predict or guess what may happen to government finances. These are based on its best guess calculations about and are subject to ‘change’.

It’s just a forecast – so should we take any notice?

According to the OBR, the UK will grow by 0.6% in 2023 – much better than previous predications last autumn, when it calculated the economy would fall into recession and shrink.

However, it slashed its growth outlook to 0.7% in 2024 and 1.4% in 2025 – down from a previous forecast of 1.8% and 2.5%.

The OBR warned that inflation – currently 4.6% – will only fall to 2.8% by the end of 2024, before reaching the Bank of England’s 2% target in 2025. Previously it forecast inflation would easily beat the target next year.

OBR & ONS data set

These gloomy predictions put the Government on a collision course with the Bank of England and Britain’s budget watchdog as they clash over whether or not the UK economy is on the up.

Annual inflation in the euro zone sank to 2.4% in November 2023 from 2.9% in October 2023, data showed Thursday 30th November 2023.

Core inflation was also below expectations at 3.6%.

The European Central Bank has stressed that it is too early to declare victory in the 20-member euro zone bloc, as they monitor potential pressures from wage increases and energy markets.

Headline inflation has now fallen significantly from the peak levels of 10.6% in October 2022.

China’s factory activity contracted for a second month in a row in November 2023.

Non-manufacturing activity hit yet another new low this year, signalling that the world’s second-largest economy was still not out of the woods and may require more policy support.

The official manufacturing purchasing managers’ index unexpectedly dropped slightly lower to 49.4 in November 2023 from 49.5 in October 2023, according to data from the National Bureau of Statistics released Thursday 30th November 2023.

The U.S. economy grew even stronger than previously calculated in the third quarter, the result of better than expected business investment and stronger government spending, the Bureau of Economic Analysis reported Wednesday 29th November 2023.

Gross domestic product (GDP), a measure of all goods and services produced during the three-month period, climbed to 5.2% annualised pace, the department’s second estimate showed. The increase superseded the initial 4.9% figure and was better than the 5% forecast from economists.

Upward revision

Primarily, the upward revision came from increases in non-residential fixed investment, which includes structures equipment and intellectual property. The category showed an increase of 1.3%, which still presented a sharp downward shift from previous quarters. Government spending also helped boost the Q3 estimate, rising 5.5% for the July-through-September 2023 period.

However, consumer spending registered a downward revision, now rising just 3.6%, compared to 4% in the initial estimate.

Inflation

There was some mixed news on the inflation front. The personal consumption expenditures price index, a gauge the Federal Reserve follows closely, increased 2.8% for the period, a 0.1% downward revision.

Corporate profits increased 4.3% during the period, up sharply from the 0.8% gain in the second quarter.

Spending plans outlined in the chancellor’s Autumn Statement represent ‘a very big fiscal risk’, according to the UK’s OBR.

Mr Richard Hughes, chair of the Office for Budget Responsibility (OBR), told MPs on the Treasury Select Committee that spending plans carried a level of ‘uncertainty’. He suggested that much of the promised spending is funded by projected savings rather than income already received.

Last week, the OBR slashed its forecast for UK economic growth.

In March, the OBR said it expected GDP – a measure of the size and health of a country’s economy – to grow by 1.8% in 2024 and 2.5% in 2025.

Predications cut

Those predictions have now been cut, with a new forecast suggesting the UK economy will grow by 0.7% in 2024 and 1.4% in 2025.

‘It is very difficult to assess the credibility of the government’s spending plans, because after March 2025 the government doesn’t have any spending plans,’ Mr Hughes said, as he and other members of the OBR faced questions on the Autumn Statement.

Tax by stealth

Even though the chancellor announced a cut to NI rates, he opted to leave NI and income tax thresholds untouched, meaning they remain frozen until 2028. By doing this, more workers will fall into the higher tax bracket thus creating larger than expected tax revenue for the treasury. And, as workers secure pay rises, they may end up paying more tax if they are dragged into that higher tax band.

Some 2.2 million more workers now pay the basic rate income tax of 20% compared with three years ago, according to official figures, while 1.6 million more people have found themselves in the 40% tax bracket in the same period.

Just a thought, wasn’t the former UK prime minister ousted because of unfunded projections or was that unfunded tax cuts?

The governor of the Bank of England, Andrew Bailey has raised concerns over economic growth as he warned again that interest rates will not be cut in the ‘foreseeable future’.

The bank boss said he was concerned over the UK economy’s potential to grow. It comes after the government’s forecaster cut its growth outlook for the UK, due to high inflation, interest rates, energy and food price increases which were exacerbated by the Covid pandemic and Russia’s invasion of Ukraine.

Inflation, which is the rate consumer prices rise at, has dropped sharply in recent months, falling to 4.6% in the year to October largely as a result of lower energy prices.

However, it is still more than double the Bank of England’s 2% target and Mr Bailey warned lowering inflation further would be ‘hard work’.

Interest rates are currently at 5.25%, a 15-year high, which has pushed up borrowing and mortgage costs.

The first transatlantic flight using 100% sustainable aviation fuel (SAF) is scheduled to take off on Tuesday, 28th November 2023.

UK Government funded project

The flight is operated by Virgin Atlantic and will fly from London’s Heathrow to New York’s JFK airport. The flight is part of a UK government-funded project to demonstrate the feasibility and benefits of using SAF as an alternative to conventional jet fuel. SAF can reduce carbon emissions by over 70% compared to fossil jet fuel.

The flight will also use biochar credits to offset any remaining emissions and achieve net zero.

Biochar is the lightweight black residue, made of carbon and ashes, remaining after the pyrolysis of biomass, and is a form of charcoal.

Support

The flight is supported by a consortium of companies, including Boeing, Rolls-Royce, BP, Imperial College London, University of Sheffield, Rocky Mountain Institute, and ICF. The transatlantic flight has received a permit to fly from the UK Civil Aviation Authority, after undergoing technical assessments and ground testing.

The flight will use a Boeing 787 Dreamliner powered by Rolls-Royce Trent 1000 engines. The SAF used will be made primarily from waste oils and fats, such as used cooking oil.

The flight is not the first transatlantic flight to use SAF, but it is the first to use 100% SAF. In 2019, Gulfstream flew a G600 aircraft from Georgia to the UK using a 30/70 blend of SAF and jet fuel.

The Virgin Atlantic flight will be the first to use pure SAF on a commercial airliner.

Update 29th November 2023 – History made

The first transatlantic flight by a large passenger aeroplane, fueled by ‘greener fuel’ was a success.Operated by Virgin Atlantic, it flew from London’s Heathrow to New York’s JFK airport.

Gold prices on Monday 27th November 2023 climbed to a more than six-month high as the U.S. dollar weakened.

Investors, it is reported, have placed their bets, suggesting the Federal Reserve is finished with interest rate hikes.

Gold was up around 0.52% at $2,012 per ounce in early afternoon trading (London time). It reached a high of $2,017.82 earlier in the day. Gold futures for December 2023 hit $2,018.90 according to analysts’ data.

The dollar index, a measure of the greenback against major currencies, was 0.13% lower as markets price in a more than 90% chance the Fed will hold rates at its next two meetings.

Analysts at Goldman Sachs reportedly said that the outlook for 2024 is that gold’s ‘shine is returning’.

The potential upside in gold prices will be closely tied to U.S. real rates and dollar moves.

The UK energy price cap is expected to rise by 5% in January 2024, which means that a typical household who pays by Direct Debit will face an annual bill of £1,931, up from £1,834 in the previous quarter.

This increase comes at a “difficult period” for struggling households, as many are already facing higher costs of living due to the pandemic, Brexit, and inflation.

Designed to protect customers

The energy price cap is designed to protect customers from unfair price hikes and ensure that they pay a fair price for their energy. However, it does not limit the total bill, which depends on how much energy is actually used.

Therefore, customers are advised to shop around for better deals and switch to cheaper tariffs if possible. This, however, is easier said than done.

It is also recommended that struggling customers contact suppliers if they have difficulty paying their bills and seek help from schemes, grants, and benefits.

The UK energy price cap is a limit on the maximum amount that energy suppliers can charge customers on standard or default tariffs for each unit of gas and electricity they use. It is set by Ofgem, the energy regulator, every three months based on the underlying costs of energy and inflation.

Some of the main takeaways from the chancellor’s autumn statement November 2023

National Insurance rate cut from 12% to 10% from 6 January, affecting 27 million people.

The 75% business rates discount for retail, hospitality and leisure firms in England extended for another year.

Class 2 National Insurance – paid by self-employed people earning more than £12,570 – abolished from April.

Class 4 National Insurance for self-employed – paid on profits between £12,570 and £50,270 – cut from 9% to 8% from April.

Full tax break permitting companies to deduct spending on new machinery and equipment from profits – now made permanent.

Funding of £4.5bn to attract investment to strategic manufacturing sectors, including aerospace, green energy, aerospace, life sciences and zero-emission vehicles.

Some £500m over the next two years to fund artificial intelligence (AI) innovation centres.

New premium planning services for England, with faster decision times for major business applications and fee refunds when these are not met.

Defence spending to remain at 2% of national income – a Nato commitment.

Overseas aid spending kept at 0.5% of national income, below the official 0.7% target.

Reaffirms previous commitments made last autumn to provide £14.1bn for the NHS and adult social care in England, as well as an extra £2bn for schools, in both 2023‑24 and 2024-25.

Fuel duty remains 52.95p per litre for petrol and diesel, after the chancellor announced a 5p per litre cut for 12 months in March 2023

State pension payments to increase by 8.5% from April, in line with average earnings.

Claimants in England and Wales deemed able to work who refuse to seek employment to lose access to their benefits and extras like free prescriptions.

UK autumn statement – art illustration of office worker preparing data

Further £1.3bn to help people who have been unemployed for over a year.

National Living Wage – to increase from £10.42 to £11.44 an hour from April.

Funding of £1.3bn over the next five years to help people with health conditions find jobs.

OBR Stats

Independent Office for Budget Responsibility (OBR) expects the economy to grow by 0.6% this year and 0.7% next year, rising to 1.4% in 2025; then 1.9% in 2026; 2% in 2027 and 1.7% in 2028.

Living standards not expected to return to pre-pandemic levels until 2027-28.

Underlying debt forecast to be 91.6% of GDP next year; 92.7% in 2024-25; 93.2% in 2026-27; before declining to 92.8% in 2028-29.(One to watch)

OBR forecasts that inflation – the rate prices are rising – will fall to 2.8% by the end of 2024, before reaching the Bank of England’s 2% target rate in 2025.(One to watch)

The OBR says higher inflation means real value of departmental budgets will be £19bn lower by 2027/28 compared with March 2023 forecasts.

Borrowing forecast to fall from 4.5% of GDP in 2023-24; to 3% in 2024-25; 2.7% in 2025-26; 2.3% in 2026-27; 1.6% in 2027-28 and 1.1% in 2028-29.(One to watch)

Federal Reserve members, in their most recent meeting, gave little indication of cutting interest rates anytime soon, particularly as inflation remains well above their goal of 2%, according to minutes released Tuesday 21st November 2023.

The detail of the meeting held 31st October – 1st November 2023, showed that Federal Open Market Committee (FOMC) members are still concerned that inflation could be stubborn or move higher, and that more may need to be done.

They indicated that policy would need to stay ‘restrictive’ at the very least, inflation is on a convincing move back to the central bank’s 2% goal.

It was reported Friday 17th November 2023 by the city-state’s central bank that Singapore will be piloting the live issuance and use of wholesale central bank digital currencies in 2024.

During the pilot, the Monetary Authority of Singapore, (MAS) will partner with local banks to pilot the use of wholesale CBDCs to facilitate domestic payments.

What is a CBDC?

A CBDC is a digital form of a country’s fiat currency, issued and regulated by the central bank or monetary authority of that country. CBDCs are different from cryptocurrencies, which are decentralized and not backed by any government.

Singapore is one of the countries that has been actively exploring the potential of CBDCs, both for wholesale and retail purposes. Wholesale CBDCs are meant for interbank transactions and cross-border payments, while retail CBDCs are meant for general public use and everyday payments.

CBDC MAS timeline

In November 2021, the Monetary Authority of Singapore (MAS) launched Project Orchid, a retail CBDC project that aims to build the infrastructure and test the use cases for a digital Singapore dollar. The project will explore the concept of purpose-bound digital Singapore dollars, which allow senders to specify how and where the money will be used.

In August 2021, MAS announced Project Dunbar, a wholesale CBDC project that involves the collaboration of the Reserve Bank of Australia, Bank Negara Malaysia, and South African Reserve Bank. The project will develop prototypes of shared platforms for cross-border transactions using multiple CBDC’s.

In June 2021, MAS published a monograph on the economic considerations of a retail CBDC in the Singapore context. The monograph concluded that there is no urgent case for a retail CBDC in Singapore, but MAS wants to be prepared in case the situation changes in the future.

In April 2021, MAS extended the regulatory sandbox for Project Ubin, a wholesale CBDC project that started in 2016. Project Ubin has successfully demonstrated the feasibility of using blockchain technology for clearing and settlement of payments and securities.

Singapore to pilot use of wholesale central bank digital currencies in 2024

In March 2021, MAS joined the Multiple CBDC (m-CBDC) Bridge initiative, a wholesale CBDC project that involves the Bank of Thailand, the Hong Kong Monetary Authority, and the Bank for International Settlements. The project will explore the use of distributed ledger technology to enable real-time cross-border transactions using multiple CBDC’s.

Process

Banks will issue tokenized bank liabilities in the form of claims in balance sheets. Retail customers can then use the tokenized bank liabilities in transactions with merchants, who will then credit these bank liabilities with their respective banks. Tokenization refers to the process of issuing a digital form of an asset on a blockchain.

The CBDC will then be automatically transferred to the merchant as a form of payment during the transaction.

Many central banks are testing and exploring their own digital currencies, includung the UK and U.S.

European Central Bank President Christine Lagarde on Friday 17th November 2023 reportedly said that Europe is now at a critical juncture, with deglobalization, demographics and decarbonization looming on the horizon.

Fragmentation

‘There are increasing signs that the global economy is fragmenting into competing blocs’, she said at the European Banking Congress, according to a transcript.

Focusing on Europe, she said that a continuous decline in the population of working age looks set to start as early as 2025, alongside climate disasters that are increasing every year.

Her answer to these shocks was that massive investment would be needed in a short space of time, requiring what she called a ‘generational effort‘.

Barriers

‘As new trade barriers appear, we will need to reassess supply chains and invest in new ones that are safer, more efficient and closer to home‘, Lagarde reportedly said.

‘As our societies age, we will need to deploy new technologies so that we can produce greater output with fewer workers. Digitalization will help. And as our climate warms, we will need to advance the green transition without any further delays‘.

Shoppers bought less food and fuel in October 2023 as they were hit by rising living costs and poor weather, according to ONS data.

The volume of products sold last month fell by 0.3% to the lowest level since February 2021 when large parts of the UK were in Covid lockdowns. Retail sales had been expected to grow in October 2023.

Demand for other goods was also lower, the ONS reported.

The CNBC/NRF Retail Monitor, which tracks card transactions, also reported a drop in consumer spending in October 2023, with retail sales, excluding autos and petrol/diesel, falling by 0.08%, and core retail, which also removes restaurants, declining by 0.03%.

The report suggested that the consumer took a spending break ahead of the holiday season, amid rising inflation, supply chain disruptions, and labour shortages.

Observing the data available at CME FedWatch the stock market does not seem to expect the Fed to start cutting rates aggressively anytime soon, this opinion is based on the current pricing data of the fed-funds futures market.

According to the CME FedWatch Tool, the probability of a rate cut in the next FOMC meeting on 13th December 2023 is very low. It is likely interest rates will be left unchanged.

The market seems to expect the Fed will hold the current rate of 5.25% until at least March 2024, but will then gradually lower it to 4.75% by December 2024.

The market seems to be more optimistic about the U.S. economic outlook and the Fed’s ability to control inflation. The mood on rates has been buoyed recently with inflation data coming in better than expected.

It is highly likely that the Fed will have to cut rates more aggressively in 2024 and 2025 to stimulate the economy and avoid a potential prolonged recession.