A stunning breakthrough in China’s microchip industry has rattled global technology markets, wiping billions from company valuations and raising fresh questions over who will dominate the next phase of the artificial intelligence revolution.

Western control

For years, Western export controls were expected to slow China’s progress in developing cutting-edge semiconductors – the tiny but powerful processors that sit at the heart of AI systems.

Instead, Chinese engineers appear to have made significant strides, challenging the assumption that the country would remain years behind its international rivals.

Sharp stock sell-off

The news has sparked a sharp sell-off across technology stocks as investors digested the implications.

Shares in some of the world’s biggest chipmakers and AI-related companies fell as markets reassessed future earnings and the prospect of fiercer global competition.

While AI remains one of the fastest-growing industries on the planet, the emergence of another serious contender has unsettled a sector that has enjoyed remarkable investor confidence.

Strategic asset

Semiconductors have become one of the world’s most valuable strategic assets. They power everything from advanced chatbots and autonomous vehicles to medical research and military systems.

Any nation capable of producing high-performance chips gains not only an economic advantage but also increased technological independence.

Race

Industry experts believe China’s latest achievement could intensify the global race for semiconductor supremacy.

Governments are already investing heavily in domestic chip manufacturing, while technology firms are pouring billions into research to stay ahead of rapidly evolving competition.

Although the market reaction has been dramatic, many analysts see the current volatility as a short-term adjustment rather than a sign that the AI boom is fading.

Breakthrough

Instead, China’s breakthrough may ultimately accelerate innovation, forcing companies around the world to develop faster, smarter and more efficient technologies in what is becoming one of the defining industrial contests of the 21st century.

Or is there a more affordable alternative for AI development compared to the trillions the U.S. has invested?

Is it a security issue or a cost concern over U.S. AI products?

A growing number of U.S. companies are quietly adopting Chinese‑developed artificial intelligence systems, drawn by their rapidly improving performance and significantly lower operating costs.

Investigation

That trend has now triggered a formal investigation on Capitol Hill, where lawmakers warn that the influx of China‑built models could expose American firms to geopolitical, security and ideological risks.

Two House Committees — Homeland Security and the Select Committee on China — have launched a joint probe into how and why Chinese AI models are seeping into U.S. corporate use.

Censorship?

Their concern is not simply economic competition. Officials argue that some China‑origin systems are designed with embedded censorship, narrative‑shaping tendencies and security uncertainties that could compromise American data or influence corporate decision‑making.

A State Department spokesperson described the issue as “serious concerns” about models that may reflect the ideology and interests of the Chinese Communist Party.

Narrowing gap

The investigation comes as Chinese developers close the performance gap with leading U.S. models. Open‑weight systems such as Kimi and DeepSeek have demonstrated capabilities comparable to American rivals in areas like cybersecurity analysis — but at a fraction of the cost.

That price advantage has attracted interest from start‑ups and tech leaders seeking to reduce expenses, even as some government departments have already banned the use of Chinese AI.

U.S. restrictions?

Lawmakers are now weighing potential responses, including procurement restrictions for companies working with federal agencies and broader guidance on the risks associated with foreign model weights freely available online.

Analysts caution, however, that outright bans may be impractical and could unintentionally harm U.S. start‑ups relying on open‑source tools.

The central question for Washington is whether America can offer competitive, affordable alternatives — or whether Chinese AI will become the default foundation of global digital infrastructure.

U.S. was there first and have the advantage, but their AI models and data centre rollout is expensive and needs to be paid for.

Artificial intelligence is often described as “smart”, but that word hides more than it reveals. What we call AI today—whether it’s ChatGPT, Claude, Copilot or any other model—is undeniably clever.

It can generate text, analyse patterns, summarise documents, write code and imitate expertise with startling fluency. But cleverness is not the same as intelligence, and certainly not the same as human intelligence.

Machines

The systems we use now are brilliant pattern machines. They excel at recognising structure, predicting the next likely word, and recombining information in ways that feel insightful.

Yet they do not understand in the human sense. They do not form intentions, build mental models of the world, or experience consequences. Their “knowledge” is statistical, not grounded in physical reality.

This is where the gap becomes obvious. Human intelligence is embodied. We learn by touching, moving, failing, navigating space, and interacting with other minds.

Child intelligence

A child understands gravity not because someone explained it, but because they dropped a toy and watched it fall. AI, by contrast, has no such lived experience. It has no body, no sensory grounding, and no direct engagement with the physical world.

Robotics is the frontier that exposes this difference most clearly. Getting a robot to pick up a cup reliably is far harder than generating a convincing essay about picking up a cup. Real-world intelligence requires perception, adaptation, and resilience.

It demands the ability to cope with uncertainty, noise, and unexpected events. Current AI systems struggle here because they lack the flexible, general-purpose reasoning that humans deploy effortlessly.

Extension of human intelligence

Still, something important has changed. AI is becoming a powerful cognitive tool—an amplifier of human capability. It can scan millions of documents, detect patterns invisible to us, and automate tasks that once consumed hours.

In that sense, AI is not replacing human intelligence; it is extending it. The real transformation will come when these systems are integrated more deeply into physical agents—robots, autonomous machines, and adaptive systems that can act in the world rather than merely describe it.

Capable but not intelligent

Right now, AI is clever, fast, and increasingly useful. But intelligence, in the full human sense, remains a broader, richer, more embodied phenomenon.

The next decade will determine whether machines can move beyond cleverness and begin to acquire something closer to genuine understanding.

As Chinese AI models gain ground, the centre of gravity in the global AI market is shifting — and U.S. firms, investors, and regulators are being forced to confront uncomfortable questions about cost, capability, and competitive advantage.

Chinese systems such as GLM‑5.2, DeepSeek, and Qwen have moved from curiosities to credible alternatives. GLM‑5.2, developed by Zhipu AI, is an open‑weight large language model designed for agentic tasks, reasoning, and enterprise automation.

Traction

It has gained traction because it delivers performance close to top‑tier U.S. proprietary models at a fraction of the cost.

Benchmarks show it landing within a percentage point of Anthropic’s Opus on certain agentic tests, while being dramatically cheaper to run.

For companies under pressure to scale AI workloads without exploding cloud bills, that price‑performance ratio is irresistible.

The consequences for U.S. AI are already visible. First, token‑price inflation from OpenAI and Anthropic has created a widening gap between cost and perceived return.

Capable and cheaper

Many firms report that frontier‑model pricing is “overdone” relative to the incremental gains in capability. When a model that costs 70–90% less can handle 80–95% of tasks, CFOs start asking hard questions.

This is not a collapse in demand for U.S. AI, but a likely recalibration: frontier models are becoming premium tools reserved for the most complex workloads, while cheaper Chinese models absorb the bulk of routine inference.

Apple’s sharp share-price drop recently (June 2026) wasn’t the result of a single misstep, but a sudden collision between global supply‑chain pressure and investor expectations.

The company’s stock slid roughly 6% in one session – its steepest fall in more than a year – after Apple pushed through sweeping price increases across Macs, iPads, HomePods, Apple TV and even Vision Pro.

For a company that normally adjusts pricing with surgical caution, the breadth and scale of these rises jolted the market.

Unprecedented price surge

The trigger sits outside Cupertino. Memory‑chip prices have surged at a pace industry veterans describe as unprecedented, driven by AI data‑centre expansion that is consuming vast quantities of DRAM and NAND.

Apple’s suppliers have passed on extraordinary cost increases, and Apple, unusually, has chosen not to absorb them.

Some Mac configurations rose by hundreds of pounds; certain high‑end models jumped by more than a thousand. Investors interpreted this as a sign that Apple’s margins – already under scrutiny given its premium valuation – are being squeezed harder than expected.

Concerning

The concern is not simply higher prices, but what they imply. If Apple is forced to raise hardware prices now, analysts fear the same pressure could extend to the iPhone later this year.

That would test the limits of consumer tolerance at a time when upgrade cycles are already lengthening. The market’s reaction reflects a deeper anxiety: Apple’s pricing power is formidable, but not infinite.

A modest rebound followed the initial sell‑off, suggesting the drop may have been an overreaction. But prices for Apple products have increased whatever the markets tell us.

Even so, the episode underscores how sensitive Apple’s valuation is to any hint of margin compression in its hardware business.

A global shortage of DRAM is rippling through the technology sector, exposing a stark divide between the giants of consumer electronics and the smaller firms that rely on stable component pricing to survive.

What was once a cheap, predictable commodity has become the industry’s most volatile input, with prices rising several hundred per cent in under a year.

Feeding AI

The cause is simple: artificial intelligence systems now consume extraordinary volumes of high‑performance memory, and suppliers are prioritising the biggest buyers.

For companies like Apple, Microsoft and Samsung, the surge in memory costs is disruptive but manageable. These firms have the scale, cash reserves and supply‑chain leverage to secure allocation and pass higher costs on to consumers.

Apple has already raised prices across several product lines, while Microsoft has increased the price of its Xbox Series S and warned that memory costs may double again by 2027. Their margins will tighten, but their market positions remain secure.

Smaller manufacturers face a far harsher reality. Start‑ups, niche hardware makers and mid‑tier consumer electronics brands are being pushed to the back of the queue, forced to pay inflated prices or accept long delays. Some may simply be unable to ship products at all

Pressure.

Companies such as GoPro have already warned investors of existential pressure, and others in the audio, camera and budget‑device sectors are quietly preparing for cancelled launches or reduced specifications.

The stock market has responded unevenly. Memory suppliers like Micron and SK Hynix have seen extraordinary rallies, with margins soaring and investors betting on prolonged demand.

Meanwhile, smaller hardware firms are experiencing sharp declines as profitability evaporates.

Longer term, the memory crunch may accelerate consolidation. If supply remains tight, the industry could tilt even further towards a handful of dominant players, with innovation increasingly concentrated among those able to afford the rising cost of participation.

IBM’s latest research breakthrough – a sub‑1nm chip architecture built like a “block of flats” – marks one of the most ambitious attempts yet to stretch Moore’s Law beyond its natural limits.

The company claims its new NanoStack design can pack almost 100 billion transistors onto a fingernail‑sized chip, a density that would have been unthinkable even a decade ago.

In early tests, the prototype delivered 50% higher performance and 70% better energy efficiency than IBM’s own 2nm technology, signalling a potential generational leap in computing power.

Moore’s Law at 50 years

For more than half a century, Moore’s Law – the observation that transistor counts double roughly every two years – has shaped the trajectory of the semiconductor industry.

But as transistors approach atomic scales, the physics has become unforgiving. Leakage, heat, and quantum effects increasingly threaten the neat exponential curve that once defined progress.

The industry’s response has been to move vertically: instead of squeezing more transistors across a flat surface, designers are now building upwards.

Verical stacking

IBM’s NanoStack takes this vertical shift to an extreme. Rather than simply elongating transistor structures, the company has begun stacking entire sheets of transistors on top of one another, creating a skyscraper‑like arrangement.

Professor Alan Woodward of the University of Surrey reportedly likens the shift to replacing a city of houses with a 100‑storey tower block – a vivid contrast to the 30–50‑storey equivalents being pursued by rivals such as Samsung and Intel.

The approach is bold, but it comes with engineering hazards. Heat rises through the stack, threatening performance and reliability. Layers that are too thin risk transistors failing to switch off cleanly, undermining the chip’s logic.

Obstacles

These are not trivial obstacles, and IBM acknowledges that commercial production remains several years away.

Yet the company argues that the architectural shift is essential if computing is to keep pace with the demands of AI, cloud workloads, and energy‑constrained data centres.

If NanoStack proves manufacturable at scale, it could represent the most significant extension of Moore’s Law since the industry moved from planar to FinFET designs.

The broader question is whether this vertical strategy can deliver multiple generations of improvement, or whether it is the final flourish before the industry must abandon transistor‑count metrics altogether.

For now, IBM has injected fresh momentum into a field long assumed to be running out of road – and reminded the industry that Moore’s Law may bend, but it is not yet broken.

Moore’s Law states

Moore’s Law is the principle that the number of transistors on a microchip doubles roughly every two years, leading to continual increases in computing power and efficiency.

Qualcomm’s latest pitch is blunt: the age of standalone apps is fading, and AI agents are about to take their place.

It’s a bold claim, but it reflects a wider shift sweeping through the tech industry as on‑device AI becomes powerful enough to handle tasks that once required entire software ecosystems.

Delegating Intent

Qualcomm argues that future smartphones will rely less on tapping icons and more on delegating intent. Instead of opening an app to book travel, edit photos, or manage finances, users will instruct an AI agent that understands context, preferences, and history.

The agent will then orchestrate the work across services in the background. In Qualcomm’s view, this makes the traditional app model feel increasingly rigid and outdated.

The company’s latest Snapdragon platforms are designed around this idea: fast local processing, persistent personal models, and low‑latency agentic behaviour that doesn’t rely solely on the cloud.

It’s a strategic move to keep mobile hardware relevant as AI shifts the centre of gravity away from apps and towards continuous, conversational computing.

Sceptics will note that apps won’t vanish overnight. But the direction of travel is clear. If Qualcomm is right, the next major platform shift won’t be about bigger screens or faster chips.

It will be about replacing the app grid with an intelligent layer that simply gets things done.

SoftBank’s sharp 10% slide on Wednesday became the defining symbol of a broader rout across Asia’s technology markets, as the region absorbed the full force of Wall Street’s overnight tech sell‑off.

The reversal ended a brief rebound in chipmakers and reignited concerns that valuations across the artificial‑intelligence complex have run too hot for too long.

The immediate pressure on SoftBank stemmed from reports that its attempt to raise at least $6 billion through a margin loan backed by its OpenAI stake had stalled.

That setback landed at a moment when sentiment toward high‑growth tech names was becoming more fragile, amplifying the downside.

Investors rotated out of risk, hitting Japan’s semiconductor ecosystem: Advantest and Renesas both fell more than 3%, while South Korea’s SK Hynix plunged over 8% and Samsung Electronics dropped 7.45%.

Taiwan’s TSMC and Hon Hai were also dragged lower.

A deeper structural worry is now taking hold. Massive AI‑related fundraising — including upcoming listings for SpaceX, Anthropic and OpenAI — appears to be siphoning capital away from publicly traded tech stocks.

Some investors see this as the early stage of a rotation; others fear it signals overheating. For Japan, one unexpected beneficiary could be defence contractors, with strategists suggesting a shift toward “heavies” as retail traders search for stability.

In essence, Son is reframing SoftBank’s entire identity around AI, portraying it not as a sector but as the next economic infrastructure — a claim that, if realised, would make the dot‑com era look modest by comparison.

SoftBank becomes Japan’s most valuable company as of May 2026.

Scale of transformation: Son argues that artificial intelligence will reshape every industry, dwarfing the internet’s impact in the early 2000s.

SoftBank’s strategy: He reportedly plans to channel the group’s investment focus almost entirely toward AI ventures, positioning SoftBank as a global accelerator for AI‑driven companies.

Vision Fund revival: After years of losses, Masayoshi Son sees AI as the catalyst to reignite the Vision Fund’s profitability, citing rapid advances in generative and autonomous systems.

Economic outlook: He predicts exponential productivity gains and new business models emerging from AI integration, describing it as a “moment of singularity” for technology and finance.

Investor sentiment: Some analysts remain cautious, recalling SoftBank’s volatile history with tech valuations, but acknowledge that Son’s influence could again shape global investment trends.

AI is more than the next dot-com era – it’s the new tech revolution in creation.

Nvidia’s long‑anticipated push into the PC market has finally materialised — and it marks the company’s most aggressive attempt yet to extend its dominance beyond the data centre.

At Computex in Taipei, Jensen Huang unveiled the N1X, an Arm‑based CPU fused with a Blackwell‑class GPU into a new RTX Spark superchip, set to appear this autumn in premium Windows laptops from Microsoft, Dell, HP, ASUS, Lenovo and MSI .

The move is strategically significant. For decades, the PC’s central processor has been the guarded territory of Intel and AMD, with Apple’s M‑series proving the only major Arm‑based disruption.

Nvidia is now entering that arena with a design built explicitly for the age of agentic AI — machines that run multiple AI processes simultaneously, shifting huge volumes of data between GPU and CPU.

Nvidia has argued for months that CPUs have become the bottleneck in modern AI workflows, and the N1X is its answer: a custom Arm design, co‑developed with Microsoft and manufactured on TSMC’s 3‑nanometre process, paired with 128GB of unified memory for high‑bandwidth compute.

Huang framed the launch as a generational reset: “the first completely re‑engineered, reinvented line of PCs in 40 years.” It’s hyperbole with intent.

Nvidia wants to define the AI PC in the same way it defined the AI data centre — not as an incremental upgrade, but as a new category.

More than 30 laptops and 10 desktops are reportedly planned over time, with early models aimed at creators, AI developers and high‑end gamers seeking thin, light machines with workstation‑level capability.

The competitive implications are profound. Arm‑based computing is accelerating across the industry, and Nvidia’s arrival puts direct pressure on Intel and AMD just as both are scrambling to articulate their own AI‑centric roadmaps.

If RTX Spark delivers the performance uplift Nvidia promises, the centre of gravity in the PC market could shift rapidly — from x86 incumbents to a company that has already rewritten the rules of modern computing once.

The expected public listings of SpaceX, OpenAI and Anthropic represent the most consequential cluster of IPOs in two decades.

Each company sits at the centre of a structural shift—space infrastructure, frontier AI models and safety‑driven AI systems—and each is likely to command a valuation in the high hundreds of billions, if not beyond.

Their arrival on public markets will not be a routine liquidity event. It will be a reordering of index composition, capital flows and investor psychology.

At the mechanical level, the impact on the S&P 500 and Nasdaq will be immediate. Index providers now operate fast‑entry rules that allow very large IPOs to join major benchmarks within days rather than months.

This compresses the adjustment period and forces passive funds to sell existing constituents to make room for the newcomers.

The selling pressure will fall disproportionately on the current megacap cohort—Microsoft, Apple, Alphabet, Amazon, Meta, Nvidia and Tesla—because these names dominate index weightings and therefore become the primary source of liquidity for rebalancing.

The indices themselves may not fall sharply, but the internal rotation will be violent.

The Nasdaq will feel the shock most acutely. Its concentration in technology means the inclusion of three new giants will trigger a scramble for weight, with ETFs forced to buy limited‑float shares at whatever price the market sets.

The S&P 500, broader and more liquid, will absorb the change more smoothly, but even there the effect will be visible: a temporary dip in existing leaders, a spike in volatility and a rapid reshaping of the top‑ten constituents.

The S&P 500 and Nasdaq will almost certainly experience a temporary liquidity shock, a forced rotation out of existing megacaps, and then—once the dust settles—a re‑concentration around the new AI/space giants.

The scale of SpaceX, OpenAI and Anthropic means the indices will not be able to absorb them quietly.

What will likely happen when SpaceX, OpenAI and Anthropic list their IPOs?

1. A mechanical sell‑off in today’s biggest tech names

Index funds must sell existing holdings to make room for the new entrants.

Goldman Sachs notes passive funds will need to rebalance as soon as these mega‑caps are added.

JPMorgan estimates that at a $2T valuation, up to $95bn of the eight largest tech stocks may need to be sold to rebalance portfolios.

Nasdaq’s new “fast entry” rules allow these companies to join the Nasdaq 100 within 15 days of listing. S&P Dow Jones is considering similar fast‑track inclusion for mega‑caps. The Motley Fool

This compresses what used to be a 12‑month absorption period into weeks.

3. Liquidity drain is real—but limited in absolute terms

Deutsche Bank estimates that even the largest IPOs would still represent just over 0.1% of S&P 500 market cap. So the market‑wide liquidity drain is modest, but the rotation effect is violent because it concentrates selling in a handful of megacaps.

4.ETF flows will be chaotic

Strategas warns that ETFs tracking trillions will compete for a tiny float, making inclusion “frantic.” SpaceX is reportedly floating only ~5% of shares initially. That means forced buying at any price, followed by forced selling elsewhere.

5. After lockups expire (180 days), the second wave hits

SpaceX’s prospectus notes that selling pressure increases as lockups roll off in phases over 180 days. Expect a two‑stage impact:

Stage 1: violent index rebalancing

Stage 2: insider‑driven supply shock

So what happens to the S&P 500?

Short-term (0–3 months after IPOs):

Mild index-level dip as megacaps are sold to fund inclusion.

Volatility spike around rebalance windows.

Narrow leadership becomes even narrower temporarily.

This is consistent with historical mega‑IPO patterns (e.g., Tesla’s inclusion forced tens of billions in one-day flows).

Medium-term (3–12 months):

The S&P 500 becomes more top‑heavy, not less.

SpaceX, OpenAI, Anthropic quickly become meaningful index weights due to their trillion‑dollar valuations.

If AI earnings continue to dominate, the index likely recovers and re‑concentrates around the new entrants.

HSBC reportedly notes that stronger tech valuations—especially from high‑valuation IPOs—could push the S&P 500 above 8,000 if earnings broaden.

What about the Nasdaq?

The Nasdaq 100 is hit harder because:

It is more tech‑concentrated.

Fast‑entry rules force inclusion within 15 days.

Expect:

Sharper rotation, especially out of semiconductor and hyperscaler names.

Higher volatility as QQQ must buy the new entrants aggressively.

A structural reshaping: SpaceX, OpenAI and Anthropic could become low‑ to mid‑single‑digit weights almost immediately.

The contrarian view (Michael Burry)

Burry argues the IPOs won’t break the bull market, because IPOs float only a “small little bit” of shares, limiting true supply impact. He believes narrative > mechanics.

There’s truth in that: the story of AI and space‑compute may ultimately lift the indices after the initial turbulence.

My Opinion

Short-term: Expect a sell‑off in existing megacaps, a volatility spike, and mechanical downward pressure on both S&P 500 and Nasdaq.

Medium-term: Once the forced rotation is complete, the indices likely resume their upward trend, now with three new trillion‑dollar engines powering them.

Long-term: This is the biggest index‑composition shock since the dot‑com era. The S&P 500 and Nasdaq will become even more dominated by AI‑infrastructure and space‑compute giants.

In other words: the indices wobble, then re‑concentrate, then march higher—unless AI demand itself cracks.

If that happens then we’ll most likely witness a crash!

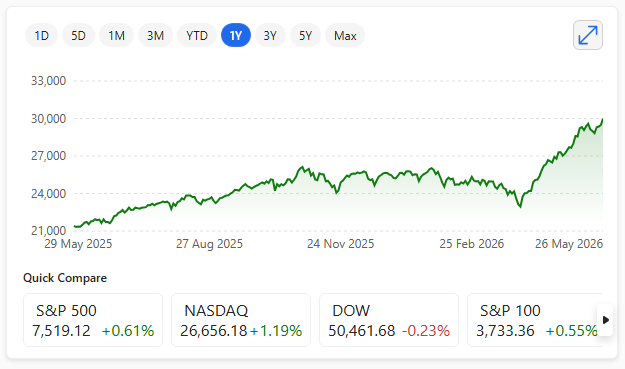

The S&P 500 and Nasdaq Composite surged to new all‑time highs yesterday, extending a rally that shows little sign of fatigue as investors continue to pile into megacap technology and AI‑linked names.

The move higher came despite a patchy run of U.S. macro data, underscoring how dominant earnings strength and sector‑specific momentum have become in driving equity sentiment.

S&P 500:7,519.12, up 45.65 points (+0.61%) — a record closing high.

S&P 500 26th May 2026

The S&P 500’s climb was supported by broad participation across technology, communication services and consumer discretionary, with investors rewarding companies delivering consistent revenue and margin expansion.

Market breadth has improved modestly in recent weeks, helping reinforce confidence that the rally is not solely dependent on a handful of giants.

Nasdaq Composite:26,656.18, up 312.21 points (+1.19%) — also a record closing high, with an intraday peak of 26,725.29.

Nasdaq Composite 26th May 2026

Nasdaq‑100 (NDX): 30,001.32 – Up: +519.68 points (+1.76%) Intraday high:30,044.49 – a new record high.

Nasdaq 100 26th May 2026

The Nasdaq once again outperformed, propelled by heavy demand for semiconductor, cloud and AI infrastructure stocks.

Upbeat guidance from several major tech firms earlier this month has strengthened the view that the sector’s earnings cycle still has room to run.

While valuations remain elevated and leave the market exposed to any negative surprise, investors have so far shown little inclination to rotate away from the winners.

Yesterday’s triple records highlight the market’s conviction that the AI‑driven profit cycle remains intact.

If the Magnificent Seven were to fall short of the AI and tech transformation investors have priced in, the S&P 500 would face one of the most severe valuation resets in its modern history.

With the group now representing roughly one‑third of the entire index, any collective disappointment would ripple far beyond technology and into every sector tied to index‑tracking capital.

Their valuations are not merely high; they are explicitly built on the assumption of future dominance in AI infrastructure, cloud, automation, consumer platforms and next‑generation hardware.

If that future fails to materialise — or even arrives more slowly than expected — the index’s structure becomes a liability. A small number of companies would be responsible for a large portion of the downside.

Scenario 1: One or two companies stumble

If a single member — say Apple or Tesla — fails to deliver, the impact is sharp but contained. The S&P 500 would likely see a 3–5% drawdown, driven by index‑weight mechanics rather than systemic panic.

Investors have already priced in uneven performance within the group, and the remaining leaders would absorb some of the shock.

The more dangerous case is if one of the AI‑infrastructure engines — Microsoft, Nvidia or Alphabet — disappoints. These companies sit at the centre of the capex cycle.

A miss on AI demand, margins or utilisation would trigger a broader reassessment of the entire AI investment thesis.

Scenario 2: Several of the Seven disappoint simultaneously

A coordinated earnings miss or guidance reset across multiple names would force a valuation compression across the entire index. Because passive flows mechanically overweight the winners, a reversal would unwind years of momentum.

A realistic outcome:

S&P 500 correction of 10–15%

Volatility spike as systematic strategies de‑risk

Rotation into defensives and energy, sectors less dependent on AI narratives

Credit spreads widen, reflecting lower confidence in tech‑driven earnings growth

This is the point where the market stops treating AI as inevitability and starts treating it as a risk.

Scenario 3: The AI thesis breaks entirely

If all seven fail to deliver the productivity, revenue and margin expansion implied by their valuations, the S&P 500 would undergo a structural reset.

The index could fall 20% or more, not because of recessionary conditions but because the market would need to rebuild a new leadership structure from scratch.

The last time leadership collapsed this dramatically was the dot‑com unwind — but today’s concentration is far higher, and passive ownership is far larger. but AI has far more upfront utility, doesn’t it?

The core truth

The S&P 500’s fate is now inseparable from the Magnificent Seven. If they deliver, the index continues to levitate. If they falter, the entire market must reprice what growth, innovation and leadership look like in the post‑AI era.

When the Magnificent Seven Slip: Who Rises Next?

If the AI tide recedes, the market’s leadership will not vanish — it will rotate. The beneficiaries will be the sectors that have quietly compounded earnings while the spotlight stayed fixed on Silicon Valley.

1. Energy and Utilities With AI‑driven data centres consuming vast power, any slowdown in tech expansion would ease pressure on grids and shift investor focus back to traditional producers. Dividend yields and defensive cash flow would regain appeal as growth multiples compress.

2. Industrials and Infrastructure A retreat from speculative tech would redirect capital toward physical productivity — logistics, construction, and manufacturing modernisation. Firms tied to electrification, rail, and defence could see valuation upgrades as investors seek real‑world output rather than digital promise.

3. Healthcare and Pharmaceuticals The sector’s secular growth and pricing power make it a natural refuge when tech falters. Biotech innovation continues independently of AI cycles, and ageing demographics ensure steady demand.

4. Financials Banks and insurers benefit from higher rates and wider spreads when tech valuations deflate. A correction in mega‑caps could even restore balance to passive indices, giving financials a larger share of inflows.

5. Consumer Staples In a post‑AI correction, investors rediscover the comfort of predictable earnings. Food, beverages, and household goods regain their defensive premium as volatility rises.

The narrative shift: The market would move from promise to proof — from speculative AI multiples to tangible earnings. The S&P 500 would not collapse; it would evolve. Leadership would pass from code to concrete, from algorithms to assets.

1. The S&P 500 is structurally dependent on seven companies

The Magnificent Seven now make up ~35% of the entire index’s market cap.

This is the highest concentration in modern history, making the S&P 500 behave more like a mega‑cap tech fund than a diversified benchmark.

2. Their valuations are priced for an AI‑driven future

Current multiples assume sustained exponential AI demand, cloud capex growth, and productivity gains.

Any slowdown in AI adoption, monetisation, or enterprise rollout would force a valuation reset across the leaders.

3. A single-company stumble is absorbable — but still painful

If one member (e.g., Apple or Tesla) disappoints, the index likely sees a 3–5% pullback.

The remaining leaders can offset the drag, but the psychological impact is non‑trivial.

4. A slowdown in the AI infrastructure core is the real risk

Microsoft, Nvidia and Alphabet sit at the centre of the global AI capex cycle.

If cloud AI demand proves slower or less profitable than expected, the S&P 500 could face a 10–15% correction as earnings expectations compress.

5. A broad failure of the AI thesis triggers a structural reset

If AI productivity gains don’t materialise, or margins erode under cost/regulatory pressure, the index could fall 20%+.

This would resemble a leadership collapse, not a normal recession — similar to the dot‑com unwind but with far more concentration and passive capital tied to the winners.

6. Passive flows amplify both upside and downside

With so much capital in index funds, any derating of the top names mechanically drags the entire index lower.

The S&P 500’s fate is now mathematically tethered to the Magnificent Seven.

7. The uncomfortable conclusion

The S&P 500’s trajectory is inseparable from the success or failure of the AI narrative.

If the Magnificent Seven deliver, the index continues to defy gravity.

If they falter, the market must rebuild a new leadership structure from scratch.

The S&P 500 is fundamentally in the danger zone – be careful!

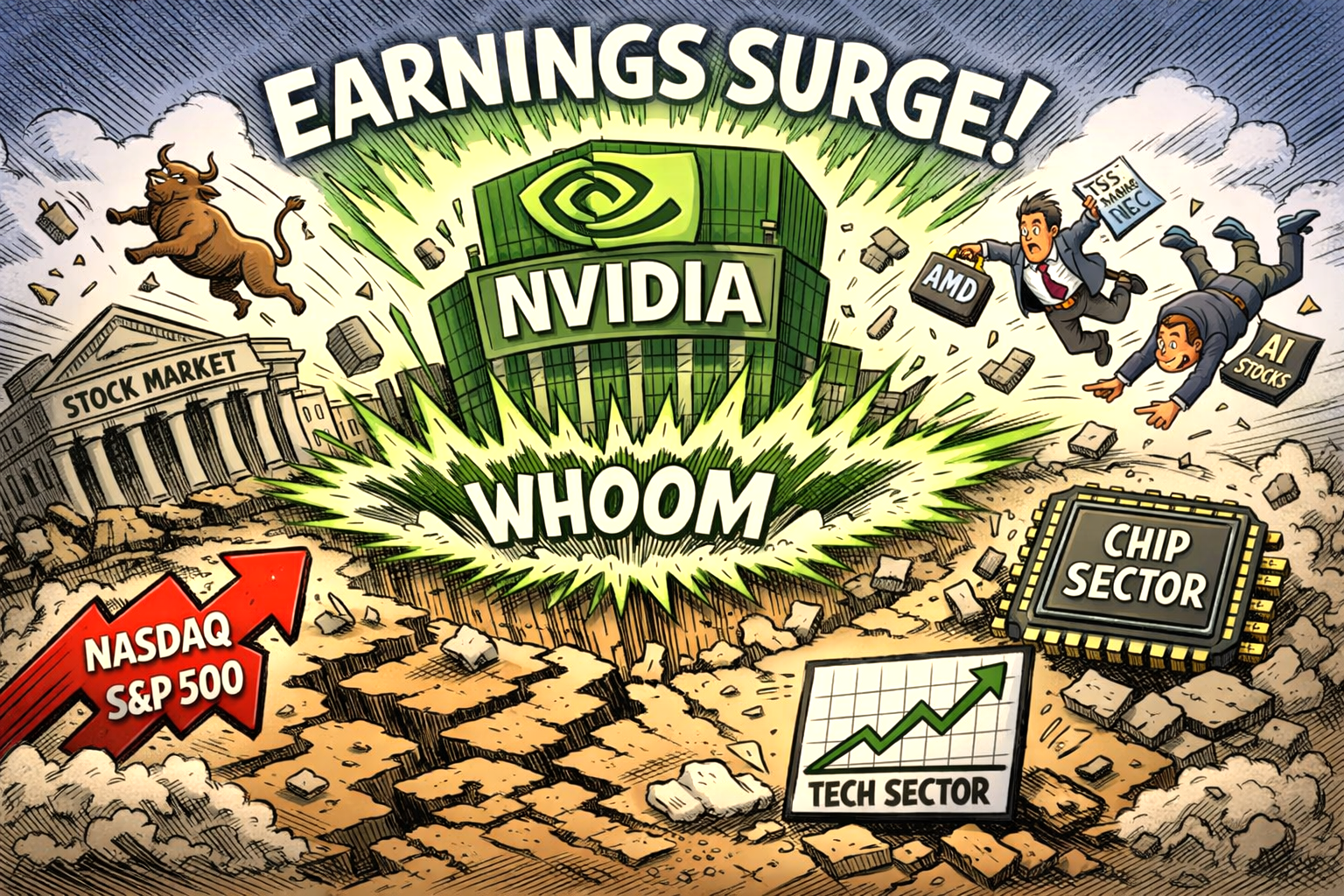

Nvidia’s latest figures have once again reshaped the mood of global markets, reinforcing its position as the defining force of the AI investment cycle.

The company reported another quarter of exceptional revenue growth, driven by unrelenting demand for its data‑centre GPUs and the rapid rollout of next‑generation Blackwell systems.

Elevated expectations

Sales and profits both exceeded already‑elevated expectations, underscoring how deeply Nvidia’s hardware is now embedded in cloud infrastructure, sovereign AI projects, and enterprise adoption.

The immediate market reaction was sharp. Nvidia’s shares jumped at the open, extending a rally that has already made it the world’s most valuable listed company.

The surge briefly pushed its valuation further into uncharted territory, with traders describing the stock as both “unstoppable” and “structurally bid” due to long‑term AI spending commitments from hyperscalers.

Options activity spiked as investors positioned for continued volatility, while short sellers once again retreated.

Broad impact

The broader market felt the impact too. The S&P 500 and Nasdaq both moved higher, lifted by the gravitational pull of Nvidia’s results and renewed confidence in the AI supply chain.

Semiconductor peers such as AMD, Broadcom, and TSMC saw sympathetic gains, while AI‑exposed software names rallied on expectations of stronger infrastructure investment.

Yet the enthusiasm comes with a familiar caveat. Nvidia’s dominance now exerts an outsized influence on index performance, and any future stumble—whether from supply constraints, competitive pressure, or a slowdown in AI capex—would reverberate across global markets.

For now, though, the company remains the engine powering the bull case for technology and all AI follows.

The latest earnings from the U.S. tech hyperscalers underline how aggressively AI investment is reshaping their financial profiles.

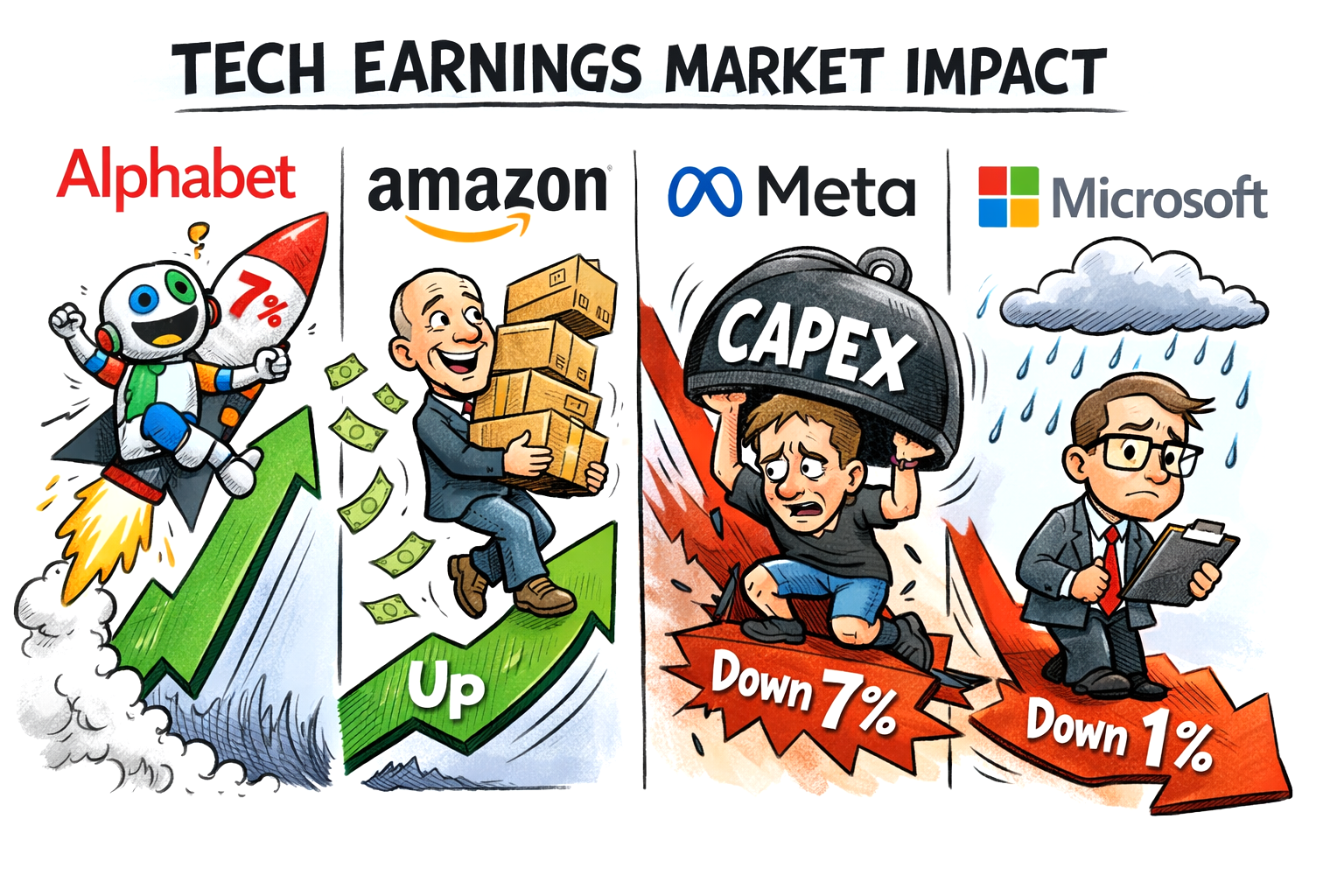

Amazon delivered a strong first quarter, with revenue up 17% to $181.5bn, driven by a sharp 28% surge in AWS sales and continued momentum in advertising. Net income jumped to $30.3bn, boosted by gains from its Anthropic investment, though free cash flow tightened as Amazon accelerated AI‑related capital expenditure.

Alphabet reported a robust start to 2026, with first‑quarter revenue rising 15% to over $113bn and operating income up 16%, supported by broad‑based strength across Search, YouTube and Google Cloud. AI infrastructure demand remains a major driver, with Google Cloud revenue climbing 48% in the latest comparable quarter.

Meta posted one of the strongest sets of results, with revenue up 33% to $56.3bn and net income soaring 61% to $26.8bn, helped by a significant tax benefit. Ad impressions and pricing both increased, while capital expenditure remained heavy as Meta scales its Superintelligence Labs.

Microsoft continued its consistent outperformance, with quarterly revenue up 18% to $82.9bn and net income rising 23%. Its AI business surpassed a $37bn annual run rate, and Intelligent Cloud revenue grew 30%, underscoring Microsoft’s leadership in enterprise AI adoption.

Alphabet and Amazon lifted markets sharply, while Meta fell and Microsoft dipped.

Alphabet’s strong cloud‑driven beat triggered a 7% after‑hours jump. Amazon also rose, gaining around 1–3% as investors welcomed AWS acceleration despite heavy AI spending.

Meta slumped 7% after hours on surging capex concerns.

Microsoft slipped about 1%, reflecting cautious sentiment despite solid cloud growth.

The S&P 500 has never been so dependent on so few companies. The Magnificent Seven — Microsoft, Apple, Nvidia, Alphabet, Amazon, Meta and Tesla — now account for roughly one‑third of the entire index’s value – that’s 33% of the whole S&P 500 vlauation.

Their dominance is not simply a reflection of current earnings power; it is a collective bet on an AI‑centred future that investors assume will transform productivity, reshape industries and justify valuations that stretch far beyond historical norms.

If one, several, or all of these companies fail to deliver the AI revolution that markets have priced in, the consequences for the S&P 500 would be immediate, structural and potentially severe.

Mild

The mildest scenario is a stumble by one or two members. If Apple’s device strategy falters, or Tesla’s autonomy narrative weakens further for instance, the index absorbs the shock.

A 3–5% pullback is plausible, driven by mechanical index weighting rather than systemic fear. Investors already expect uneven performance within the group, and the remaining leaders could offset the disappointment.

Major

The more destabilising scenario is a collective slowdown among the AI infrastructure leaders – Microsoft, Nvidia and Alphabet. These firms sit at the centre of the global capex cycle.

If cloud AI demand proves slower, less profitable or more niche than expected, the market would be forced to reassess the entire economic promise of generative AI.

In this case, the S&P 500 could see a 10–15% correction as valuations compress, volatility spikes and passive flows unwind years of momentum.

Dramatic

The most dramatic outcome is a broad failure of the AI ‘sector’ itself. If the promised productivity gains do not materialise, if enterprise adoption stalls, or if regulatory and cost pressures erode margins, the S&P 500 would face a structural reset.

With a third of the index priced for exponential growth, a collective disappointment could trigger a decline of 20% or more.

This would not resemble a cyclical recession; it would be a leadership collapse similar to the dot‑com unwind, but with far greater concentration and far more passive capital tied to the winners.

The uncomfortable truth is that the S&P 500’s trajectory is now inseparable from the Magnificent Seven. If they deliver, the index continues to defy gravity. If they falter, the market must rebuild a new narrative — and a new set of leaders — from the ground up.

If the Magnificent Seven Lose Their Grip, Who Rises Next?

For years, the S&P 500 has been defined by the gravitational pull of the Magnificent Seven. Their dominance has shaped index performance, investor psychology and the entire narrative arc of global markets.

If these companies lose momentum — whether through slower AI adoption, regulatory pressure, margin compression or simple over‑expectation — leadership will not disappear.

It will rotate. And the beneficiaries are already hiding in plain sight.

Alternative investment to AI

The first and most obvious winners would be Energy and Utilities. As AI enthusiasm cools, investors tend to rediscover the appeal of tangible cash flow. Energy companies, with their dividends and pricing power, become natural refuges.

Utilities, often dismissed as dull, regain relevance as defensive anchors in a more volatile market. If AI‑driven data‑centre demand slows, the sector’s cost pressures ease, improving margins.

Next in line are Industrials and Infrastructure. A retreat from speculative tech would likely redirect capital towards physical productivity — logistics, construction, defence, electrification and manufacturing modernisation.

These sectors have been quietly compounding earnings while Silicon Valley has monopolised attention. If the market shifts from promise to proof, industrials become the new growth story.

Healthcare and Pharmaceuticals would also rise. Their earnings cycles are largely independent of AI hype, driven instead by demographics, innovation and regulatory frameworks. When tech stumbles, healthcare’s stability becomes a premium rather than an afterthought.

Biotech, in particular, benefits from capital rotation when investors seek uncorrelated growth.

Financials stand to gain as well. A correction in mega‑cap tech would rebalance passive flows, giving banks and insurers a larger share of index‑tracking capital. Higher rates and wider spreads already support the sector; a shift away from tech simply amplifies the effect.

Finally, Consumer Staples would reassert themselves. In a market recalibrating after an AI disappointment, investors gravitate towards predictable earnings. Food, beverages and household goods regain their defensive premium as volatility rises.

The broader truth is simple: if the Magnificent Seven falter, the S&P 500 does not collapse — it redistributes. Leadership moves from code to concrete, from speculative multiples to operational reality. The market has always found new champions. It will again.

OpenAI’s reported failure to meet internal revenue and user‑growth targets has sent a sharp tremor through global tech markets, exposing just how dependent the wider AI sector has become on a single company’s momentum.

The Wall Street Journal report — which OpenAI has reportedly dismissed as “ridiculous” — suggested the firm is expanding more slowly than its own projections, raising questions about whether its vast compute‑spend commitments can be sustained. That alone was enough to trigger a sell‑off.

Slide

The steepest declines were concentrated among companies most financially tethered to OpenAI’s infrastructure demands. Oracle, which has a colossal $300 billion, five‑year cloud capacity agreement with the firm, fell more than 4%.

After the news story was released chipmakers followed OpenAI: Broadcom dropped over 4%, AMD slid more than 3%, Nvidia dipped around 1.5%, and CoreWeave — the highly leveraged neocloud provider — sank nearly 6%.

Even Qualcomm, which had recently enjoyed a lift from reports of collaboration with OpenAI on smartphone chips, slipped before recovering.

This is the first moment in the current AI cycle where a wobble at OpenAI has produced a synchronised pullback across the entire supply chain.

Investors are now confronting a question they have largely ignored: what if the sector’s flagship growth curve is not perfectly exponential? But my guess is, like all events at the moment, the market will likely overlook it.

Fragile

The reaction also exposes the fragility of AI‑linked valuations. Markets have priced the boom as if demand is both infinite and linear.

Any hint of deceleration — even one disputed by the company — forces a reassessment of the capital intensity underpinning the industry.

With Anthropic and Google’s Gemini gaining enterprise traction, OpenAI’s dominance is no longer assumed.

Still, several fund managers argue the broader AI investment cycle remains intact. The sell‑off looks less like a turning point and more like a reminder: when one company becomes the gravitational centre of an entire narrative, even a rumour can bend the orbit.

A quiet but decisive shift is under way in the global AI race: some of the most accomplished researchers at Meta, Google, OpenAI and other frontier labs are walking out of the biggest companies in the sector to build their own.

Trend

The trend has accelerated sharply over the past year, with new ventures raising extraordinary sums within months of being founded, as investors bet that smaller teams can move faster than the giants they left behind.

The motivations are remarkably consistent. Researchers say that the commercial pressure inside the largest AI labs has narrowed the scope of what they are allowed to explore.

Rush

With Big Tech locked into a high‑stakes contest to release ever‑larger models on tight schedules, entire areas of research — from new architectures to interpretability and agentic systems — are being deprioritised.

That creates an opening for smaller firms that can pursue ideas too experimental or too slow‑burn for corporate roadmaps.

Investors

Investors have responded with enthusiasm. Former Google DeepMind scientist David Silver secured a record $1.1 billion seed round for his new company, Ineffable Intelligence, while other ex‑DeepMind and ex‑Meta researchers are raising similar sums for ventures focused on reinforcement learning, continuous‑learning systems and autonomous labs.

In total, AI startups founded since early 2025 have already attracted nearly $19 billion in funding this year, putting them on track to surpass last year’s total.

Independence

Founders argue that independence gives them both speed and neutrality. Chip‑design startup Ricursive Intelligence, for example, says customers are more willing to trust a standalone company than a Big Tech competitor with its own hardware ambitions.

Many of these startups are also rebuilding their old teams, hiring colleagues from the very companies they left.

The result is a new competitive dynamic: Big Tech still dominates the AI landscape, but the frontier of innovation is increasingly being pushed by smaller, highly focused labs that believe they can out‑pace the giants – and with lower investment too.

DeepSeek’s newly released V4 model marks a significant step forward in open‑source AI, combining long‑context capability with major architectural upgrades.

DeepSeek V4 arrives as a preview release, offering two variants — V4‑Pro and V4‑Flash — both designed to push the boundaries of efficiency and reasoning performance.

The headline feature is the one‑million‑token context window, enabling the model to process and retain far larger bodies of information than previous generations.

Positioning

This positions V4 as a strong contender in tasks requiring extended reasoning, research support, and complex agentic workflows.

The V4 series introduces a refined Hybrid Attention Architecture, combining compressed sparse and heavily compressed attention mechanisms to dramatically reduce computational overhead.

DeepSeek claims this approach cuts inference FLOPs and KV‑cache requirements to a fraction of those seen in earlier models, making long‑context operation more practical and cost‑effective.

V4‑Pro, the flagship model, includes a maximum reasoning‑effort mode, which the company says significantly advances open‑source reasoning performance and narrows the gap with leading closed‑source systems.

Meanwhile, V4‑Flash offers a more economical, faster alternative while retaining strong capability across everyday tasks.

Accelerating AI ambition

The release underscores China’s accelerating AI ambitions. DeepSeek’s earlier R1 model shook global markets with its low‑cost, high‑performance profile, and V4 continues that trajectory — now optimised for domestic chips and supported by growing local hardware ecosystems.

With open‑source availability and aggressive efficiency gains, DeepSeek V4 strengthens the company’s position as one of the most closely watched challengers in the global AI race.

And it’s far cheaper than its peers and not so power hungry either.

TSMC’s 58% surge in first‑quarter profit is the clearest sign yet that the AI boom is no longer a cyclical uplift but a structural shift reshaping the entire semiconductor industry.

The Taiwanese chipmaker delivered record earnings, comfortably beating analyst expectations, as demand for advanced processors continued to outstrip supply.

Net income reportedly reached NT$572.48 billion, marking a fourth consecutive quarter of record profits, while revenue climbed to NT$1.134 trillion, driven overwhelmingly by high‑performance computing and AI‑related orders.

What stands out is the composition of that growth. Roughly three‑quarters of TSMC’s wafer revenue reportedly came from advanced nodes, with 3‑nanometre chips alone accounting for a quarter of shipments.

Nvidia

Nvidia has now overtaken Apple as TSMC’s largest customer, underscoring how AI accelerators have become the industry’s most valuable real estate.

TSMC’s executives described AI demand as “extremely robust”, with customers signalling multi‑year achievements rather than the usual stop‑start ordering cycle.

The company also moved to reassure investors over supply‑chain risks linked to the Middle East conflict, saying it has diversified sources for critical gases such as helium and hydrogen.

With capacity running hot and capital spending set to hit the top end of guidance, TSMC is positioning itself as the indispensable chipmaker in the AI era.

ASML’s decision to raise its 2026 guidance underlines a simple reality: demand for advanced AI chips is not easing, and the world’s most important semiconductor equipment maker remains at the centre of that surge.

The company signalled stronger-than-expected orders for its extreme ultraviolet (EUV) and next‑generation high‑NA systems, driven by chipmakers racing to expand capacity for AI accelerators, data‑centre processors and cutting‑edge logic nodes.

Bottleneck

The upgrade matters because ASML sits at the bottleneck of global chip production. Only a handful of firms can even buy its most advanced machines, and those firms – chiefly TSMC, Intel and Samsung – are all scaling up AI‑focused manufacturing.

Their capital expenditure plans have held firm despite broader economic uncertainty, suggesting that AI infrastructure is becoming a non‑discretionary investment rather than a cyclical one.

Two forces are driving the momentum. First, hyperscalers continue to pour billions into AI clusters, creating sustained demand for the most advanced lithography tools.

Long-term lock in

Second, geopolitical pressure to secure domestic chip capacity is pushing governments and manufacturers to lock in long‑term equipment orders.

ASML’s raised outlook reinforces the sense that the semiconductor cycle is diverging: consumer electronics remain patchy, but AI‑related manufacturing is entering a multi‑year expansion.

The key question now is whether supply can keep pace with the ambition of its customers.

Meta has unveiled Muse Spark, its first major artificial intelligence model since the company overhauled its AI strategy in response to the underwhelming reception of its previous Llama 4 models.

Developed by the newly formed Meta Superintelligence Labs under the leadership of Alexandr Wang, Muse Spark represents a deliberate shift towards smaller, faster, and more capable systems designed to compete directly with Google, OpenAI, and Anthropic.

Foundation

Muse Spark is positioned as the foundation of a new family of models internally known as Avocado. Meta reportedly describes it as “small and fast by design”, yet able to reason through complex questions in science, maths, and health — a notable claim given the company’s recent struggles to keep pace with rivals.

Early evaluations suggest the model performs competitively in language and visual understanding, though it still trails in coding and abstract reasoning.

Crucially, Muse Spark is deeply integrated into Meta’s ecosystem. It already powers the Meta AI app and website and will soon replace Llama across WhatsApp, Instagram, Facebook, Messenger, and Meta’s smart glasses.

Integrated

This rollout signals Meta’s intention to embed AI more tightly into everyday user interactions, from search and recommendations to multimodal tasks such as analysing photos or comparing products.

The company is also experimenting with new revenue streams by offering a private API preview to select partners — a departure from its previous open‑source approach.

Whether this shift will alienate developers who embraced the openness of Llama remains to be seen.

Meta frames Muse Spark as an early step toward “personal superintelligence”, an assistant that can understand the world alongside the user rather than waiting for typed instructions.

It’s an ambitious vision — and one that will be tested as the model expands globally and faces scrutiny over privacy, safety, and real‑world performance.

Oracle is swinging hard at its own workforce as the company races to reposition itself as an AI‑infrastructure contender.

Thousands of roles are being eliminated, a drastic move that reflects the sheer financial pressure of trying to keep up with hyperscale rivals in the most capital‑intensive tech shift in decades.

The company’s share price has slumped 25% this year, with investors increasingly uneasy about soaring data‑centre spending and the heavy debt required to fund it.

Oracle has already raised $50 billion to bankroll new GPU‑ready facilities, but unlike Amazon or Microsoft, it lacks the cushion of vast cloud scale.

The result: a balance sheet under strain and a leadership team forced into tough decisions.

Future

Oracle’s remaining performance obligations have ballooned to more than half a trillion dollars, fuelled by major AI partnerships including a huge deal with OpenAI.

But those future revenues don’t solve today’s cash‑flow squeeze. Analysts estimate that cutting 20,000 to 30,000 jobs could free up as much as $10 billion — enough to keep the AI build‑out moving without further rattling the markets.

Oracle is betting that a leaner organisation now will buy it the runway to compete later. The question is whether the cuts arrive in time to match the speed of the AI race.

When artificial intelligence first ignited investor enthusiasm, it lifted almost every major technology stock.

The narrative was simple: AI would transform industries, boost productivity and unlock vast new revenue streams.

Yet as the cycle matures, markets are becoming more selective. In recent weeks, shares of IBM have drifted lower, illustrating how the ‘AI effect’ can cut both ways.

At first glance, IBM should be a prime beneficiary. The company has spent years repositioning itself around hybrid cloud infrastructure, data analytics and enterprise AI solutions.

Its Watson platform has been refreshed with generative AI tools designed to automate customer service, streamline software development and enhance business decision-making. Management has repeatedly emphasised AI as a core growth engine.

Market Expectations

However, the market’s expectations have shifted. Investors are increasingly rewarding companies that sit at the very heart of AI infrastructure — those supplying advanced semiconductors, high-performance computing capacity and hyperscale cloud services.

These businesses are reporting visible surges in AI-related demand, often accompanied by sharp revenue acceleration and expanding margins.

By contrast, IBM’s AI exposure is embedded within broader consulting and software operations, making its growth trajectory appear steadier rather than explosive.

This distinction matters in a momentum-driven environment. When earnings updates fail to deliver dramatic upside surprises, shares can quickly lose favour.

Less AI Effect

IBM’s results have shown progress in software and recurring revenue, but they have not reflected the kind of dramatic AI-driven uplift seen elsewhere in the sector. For some investors, that raises questions about competitive positioning and pricing power.

There is also a perception issue. Despite its reinvention efforts, IBM still carries the legacy image of a mature technology conglomerate rather than a cutting-edge AI disruptor.

In a market captivated by bold innovation stories, narrative can influence valuation just as much as fundamentals.

If capital flows concentrate in a handful of high-growth AI names, diversified players may struggle to keep pace in share price performance.

AI Tension

Yet the sell-off may also highlight a deeper tension within the AI theme. Enterprise adoption of AI tools tends to be gradual, cautious and closely tied to measurable productivity gains.

IBM’s strategy is built around long-term integration rather than short-term hype. While that approach may lack immediate fireworks, it could prove more durable as corporate clients prioritise reliability, governance and cost control.

For now, though, the AI effect is amplifying investor discrimination. In a market eager for rapid transformation, IBM’s more measured path has translated into weaker share performance — a reminder that not all AI exposure is valued equally.

Further discussion

IBM has found itself on the wrong side of the artificial intelligence boom, with its shares tumbling more than 13% after Anthropic unveiled a new capability that directly targets one of the company’s most enduring revenue pillars: COBOL modernisation.

The sell‑off reflects a broader market anxiety that AI is beginning to erode long‑protected niches in enterprise technology, and IBM has become the latest high‑profile casualty.

For decades, IBM has been synonymous with mainframe computing and the maintenance of vast COBOL‑based systems that underpin global finance, government services, airlines, and retail transactions.

These systems are notoriously complex, expensive to update, and dependent on a shrinking pool of specialist developers.

Premium Brand

That scarcity has long worked in IBM’s favour, allowing it to charge a premium for modernisation and support.

Anthropic’s announcement threatens to upend that equation. Its Claude Code tool, the company claims, can automate the most time‑consuming and costly parts of understanding and restructuring legacy COBOL environments.

Tasks that once required teams of analysts months to complete—mapping dependencies, documenting workflows, identifying risks—can now be accelerated dramatically through AI‑driven analysis.

The implication is clear: modernising legacy systems may no longer require the same level of human expertise, nor the same level of spending.

Investors reacted swiftly. IBM’s share price fell to $223.35, extending a year‑to‑date decline of more than 24% – recovering later to $229.39

IBM one-year chart as of 24th February 2026

The drop reflects not only concerns about lost revenue, but also the fear that IBM’s competitive moat—built on decades of institutional reliance on COBOL—may be eroding faster than expected.

The timing has amplified market jitters. Only days earlier, cybersecurity stocks were hit by another Anthropic announcement: Claude Code Security, a feature designed to scan codebases for vulnerabilities.

AI Mood Logic

The rapid expansion of AI into specialised technical domains has created a ‘sell first, ask questions later’ mood across the market, with investors increasingly wary of companies whose business models depend on labour‑intensive or legacy‑bound processes.

For IBM, the challenge now is to demonstrate that it can harness AI rather than be displaced by it.

The company has invested heavily in its own AI initiatives, but the latest market reaction suggests investors are unconvinced that these efforts will offset the threat to its traditional strongholds.

The AI revolution is reshaping the technology landscape at speed. IBM’s sharp decline is a reminder that even the industry’s oldest giants are not insulated from disruption—and that the next wave of AI competition may hit the most established players hardest.

But remember, this is IBM we are talking about.

Explainer

What is COBOL?

COBOL is an old but remarkably durable programming language created in the late 1950s to run business, finance, and government systems, and it’s still powering much of the world’s banking and administrative infrastructure today.

It was designed to read almost like plain English, making it easier for non‑technical managers to understand, and its stability means many core systems have never been replaced.

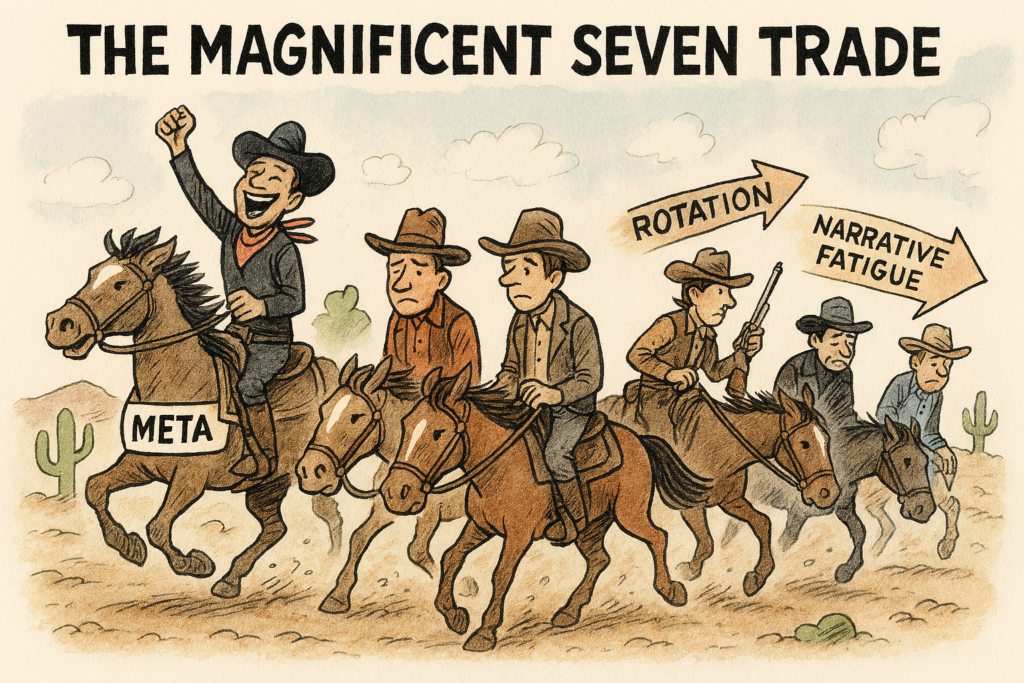

For much of the past three years, the so‑called Magnificent Seven – Apple, Microsoft, Alphabet, Amazon, Meta, Tesla and Nvidia – have powered US equities to repeated record highs.

Their sheer scale, earnings strength and centrality to the AI boom turned them into a market narrative as much as an investment theme.

But as 2026 unfolds, the question is no longer whether they can keep leading the market higher, but whether the idea of treating them as a single trade still makes sense.

The short answer is closer to: the trade isn’t dead, but the era of effortless, broad‑based mega‑cap dominance is fading.

Mag 7 fatigue

The first sign of fatigue is the breakdown in cohesion. Last year, only a minority of the seven outperformed the wider S&P 500, a sharp contrast to the near‑uniform surges of 2023 and early 2024.

Nvidia and Alphabet continue to benefit from the structural demand for AI infrastructure and cloud‑driven productivity gains. Others, however, appear to be wrestling with slower growth, regulatory pressure or strategic resets.

Apple faces a maturing hardware cycle, Tesla is contending with intensifying global competition, and Meta’s spending plans continue to divide investors.

Mag 7 trade – which company is missing?

Divergence

This divergence matters. For years, investors could simply buy the group and let the rising tide of AI enthusiasm and index concentration do the work.

That simplicity has evaporated. Stock‑picking is back, and the market is finally distinguishing between companies with accelerating earnings power and those relying on past momentum.

At the same time, market breadth is improving. Capital is rotating into industrials and defensive sectors as investors seek exposure to areas that have lagged the mega‑cap rally. However, AI is affecting software stocks, law and financial sectors.

Healthy future

This broadening is healthy: it reduces concentration risk and signals that the U.S. economy is no longer dependent on a handful of tech giants to sustain equity performance.

Yet it would be premature to declare the Magnificent Seven irrelevant. Their combined earnings growth is still expected to outpace the rest of the index, and their role in AI, cloud computing and digital infrastructure remains foundational.

Change

What has changed is the nature of the trade. These are no longer seven interchangeable vehicles for tech exposure; they are seven distinct stories with diverging trajectories.

The Magnificent Seven haven’t left the stage. They have likely stopped performing in unison – and for investors, that marks the beginning of a more nuanced, more selective chapter.