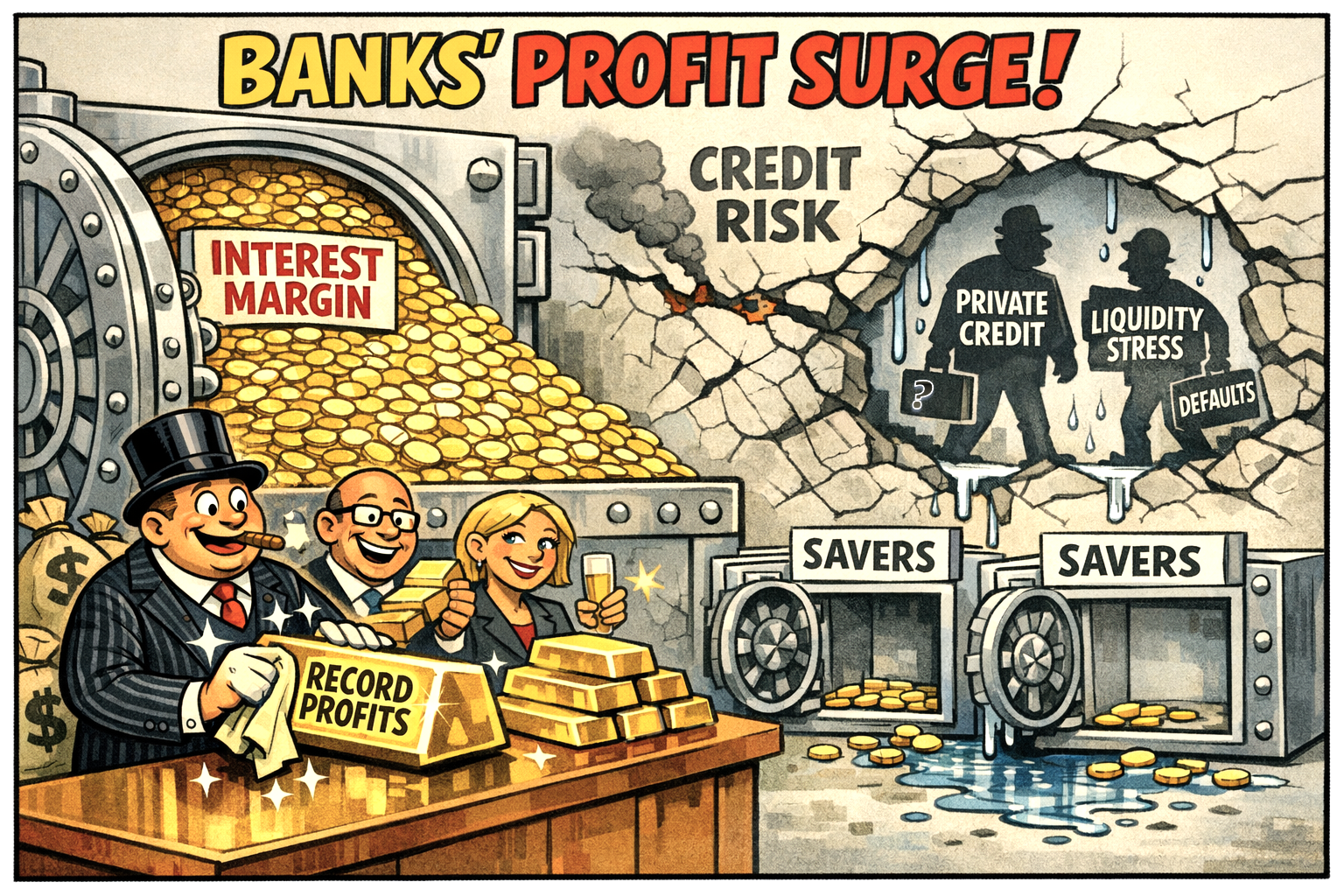

Banks are reporting unusually strong profits because higher interest rates have widened margins, while slow pass‑through to savers, cost‑cutting, and capital optimisation have amplified returns — even as credit risks begin to rise.

Why profits are so high

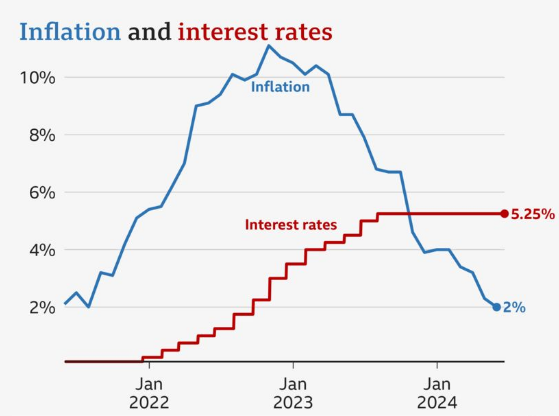

The latest figures show that UK banks are still benefiting from the long tail of the interest‑rate cycle.

Even though the Bank of England has not raised rates since August 2023, the base rate remains at 4.5%, allowing lenders to earn significantly more on mortgages and credit than they pay out on deposits.

This margin expansion has been the single biggest driver of profit growth. Research from recently highlighted from Positive Money shows that the UK’s four largest banks have generated £136.8 billion in pre‑tax profits since rate rises began in December 2021, and are on track to exceed their record £45.9 billion made in 2024 by around 14% in 2025.

A second factor is the government’s interest payments on central bank reserves. Because commercial banks are paid the base rate on their risk‑free deposits at the Bank of England, they stand to receive around £30 billion a year in transfers through to 2030 — effectively a public subsidy that boosts earnings without requiring additional lending.

Banks have also been aggressively returning capital to shareholders. Between 2022 and 2024, the big four spent £42 billion on dividends and £32 billion on share buybacks, reinforcing the perception that profits are being harvested rather than reinvested.

How banks are sustaining these profits

The profitability story is not just about rates. Structural shifts are helping banks defend margins even as the rate cycle turns.

1. Slow deposit repricing High Street banks have been reluctant to raise savings rates in line with market levels. As consumers move deposits to specialist lenders offering better returns, the big banks still retain a large, low‑cost funding base.

KPMG reportedly notes that high street banks’ share of deposits has only slipped from 84% in 2019 to 80% in 2024 — still dominant enough to preserve cheap funding.

2. Capital optimisation through securitisation Banks are increasingly using Significant Risk Transfer (SRT) securitisations to free up capital and improve return on equity. Securitised loan volumes have grown at a 4% CAGR between 2022 and 2025, allowing banks to recycle capital into higher‑yielding assets.

3. Cost discipline and digital transformation With margins expected to compress as rates eventually fall, banks are pushing cost‑cutting, automation, and AI‑driven process redesign.

KPMG reportedly forecasts sector‑wide returns on equity could fall from 18% in 2023 to 10% by 2027 without structural change — making efficiency programmes essential to sustaining profitability.

The emerging risk: impairments

Barclays’ latest results show rising credit impairment charges, including an £823 million provision linked to mortgage‑market stress and fraud‑related losses.

This raises the question of whether the credit cycle is turning. If impairments rise across the sector, the profit boom could fade.

The biggest emerging credit risks sit outside the banking system and that is private credit, leveraged borrowers, and liquidity mismatches that could spill back into banks.

Private credit is now large, interconnected, and showing signs of strain. Rising defaults, deteriorating loan quality, and withdrawal caps at major funds point to mounting stress. Defaults could climb sharply, with Morgan Stanley reportedly warning they may reach 8%, far above historical norms.

A second risk is liquidity pressure. Funds are restricting redemptions as investors rush for the exit, exposing the fragility of semi‑liquid structures.

Finally, contagion risk is growing because banks finance private‑credit funds and pipelines. As analysts note, deeper interconnections mean a downturn could transmit stress back into the regulated system.

Conclusion

Banks are reporting strong profits because the rate environment, public transfers, and capital strategies have created a uniquely favourable backdrop.

But the model is fragile: as impairments rise and rates eventually fall, the sector may be approaching the end of its profit‑supercycle.