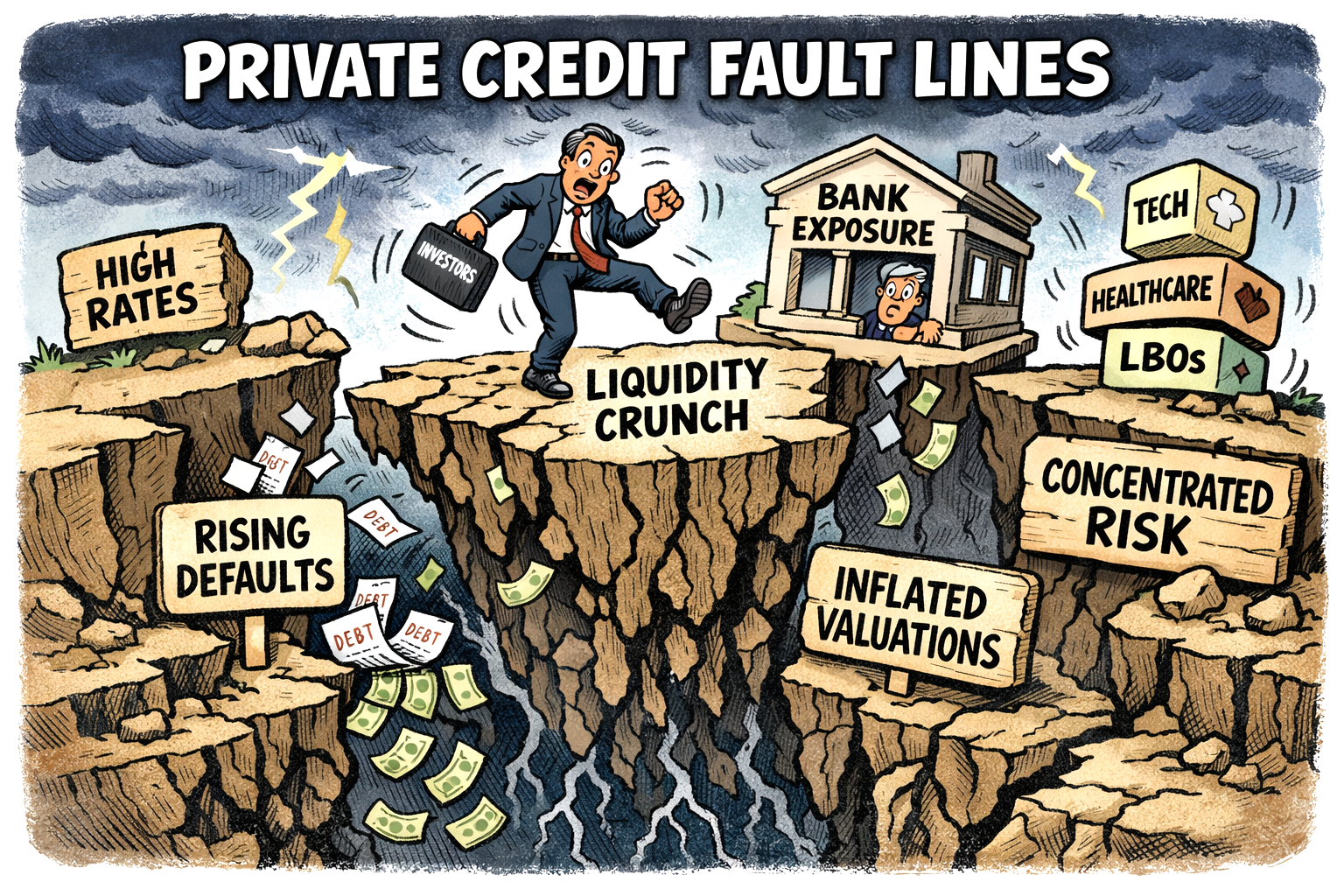

Private credit has become the fault line running beneath the banking system. And it’s now large enough to matter, opaque enough to worry investors, and now visible enough that banks can’t wave it away.

Complicated picture

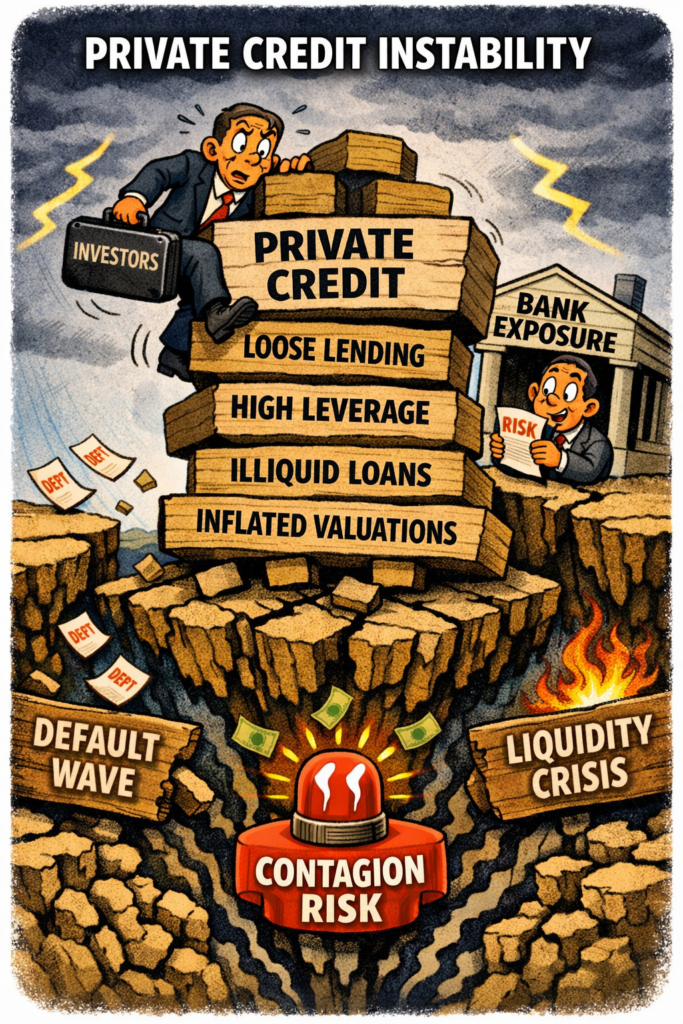

European lenders spent this earnings season insisting their exposures are “well diversified” or “immaterial”, yet the numbers tell a more complicated story.

Barclays alone reportedly disclosed £15 billion of private‑credit exposure, part of a much larger £66 billion book tied to non‑bank financial intermediaries.

Its hit from the collapse of Market Financial Solutions — a specialist lender undone by alleged fraud — was small in accounting terms, but symbolically important. One cockroach rarely travels alone.

Structural

The deeper issue is structural. Private credit has ballooned into a parallel lending system, lightly regulated and increasingly interconnected with banks through financing lines, securitisations, and business‑development companies.

When these semi‑liquid vehicles face redemption pressure — as several have this year — the stress ricochets back into the banking system. UBS and Deutsche Bank both reportedly emphasised their underwriting standards, but neither disputed that liquidity strains are real.

What unnerves investors is not a wave of defaults — yet — but opacity. Bank of America’s latest survey shows investment‑grade investors are uneasy because they simply cannot see where the risks sit.

Software lending in the U.S., chemicals in Europe, and China‑driven price pressure all add sector‑specific fragility. High‑yield specialists, closer to the coalface, are oddly calmer; they know where the bodies usually fall.

Contained?

The banking system’s official line is that everything is contained. But containment depends on liquidity holding, valuations staying stable, and no further MFS‑style surprises emerging.

Private credit has grown faster than transparency, and faster than the regulatory perimeter. That mismatch — not any single default — is what now shadows the banks.

The issue

The central concern with private credit is simple: it has grown faster than the safeguards designed to contain it.

What was once a niche corner of finance is now a multi‑trillion‑pound shadow banking system whose risks are only partially visible to regulators, banks, or investors. That opacity is now becoming a problem.

Expansion

Private‑credit funds have expanded aggressively by offering speed, flexibility, and looser covenants than traditional banks. In a low‑rate world, that model looked benign. In a high‑rate world, it looks fragile.

Many borrowers were underwritten on assumptions that no longer hold: stable cashflows, cheap refinancing, and buoyant valuations. As rates stay elevated, those assumptions are breaking down.

Defaults

Defaults are rising, and recovery values are uncertain because loans are bespoke, illiquid, and rarely traded.

Liquidity

Liquidity is the second fault line. Private‑credit vehicles promise semi‑liquid access to investors while holding assets that cannot be sold quickly without taking a loss.

When redemptions pick up, funds resort to withdrawal gates, side pockets, or emergency financing lines from banks.

That is where the contagion risk emerges. Banks insist their exposures are modest, but they provide leverage, subscription lines, and warehousing facilities to the very funds now under pressure.

A liquidity squeeze in private credit can therefore boomerang back into the regulated system.

Valuation

Valuation risk is the third issue. Because loans are marked to model rather than market, losses can be slow to surface.

That delays recognition, masks stress, and encourages complacency. When reality finally intrudes — through a default, a refinancing failure, or a forced sale — the adjustment can be abrupt.

The final concern is concentration. Private credit is heavily exposed to software, healthcare, and sponsor‑backed roll‑ups. If one of these sectors turns, the losses will not be isolated.

Private credit is not about to collapse as such. But it is large, opaque, and increasingly interconnected — and that combination is rarely harmless.