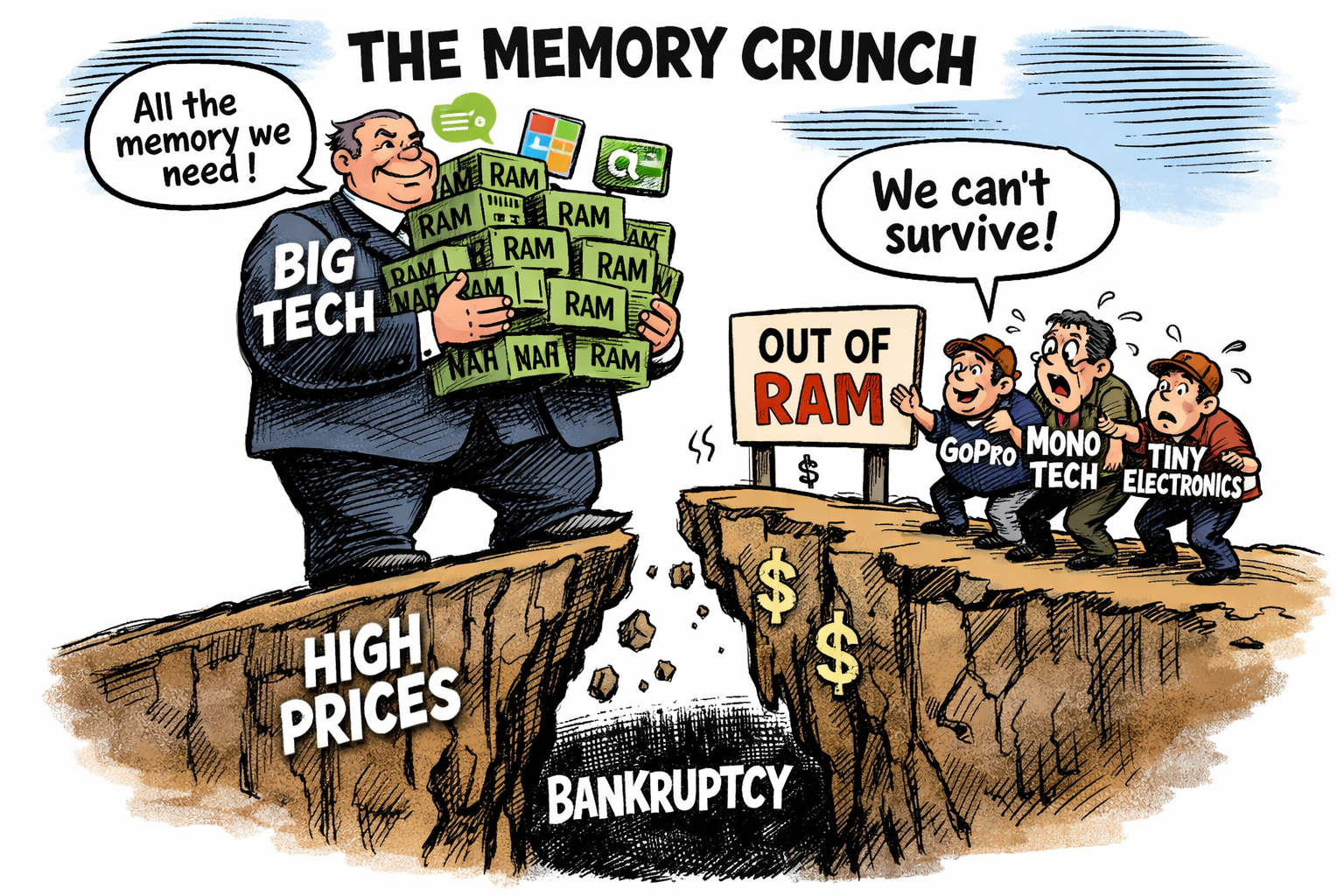

A global shortage of DRAM is rippling through the technology sector, exposing a stark divide between the giants of consumer electronics and the smaller firms that rely on stable component pricing to survive.

What was once a cheap, predictable commodity has become the industry’s most volatile input, with prices rising several hundred per cent in under a year.

Feeding AI

The cause is simple: artificial intelligence systems now consume extraordinary volumes of high‑performance memory, and suppliers are prioritising the biggest buyers.

For companies like Apple, Microsoft and Samsung, the surge in memory costs is disruptive but manageable. These firms have the scale, cash reserves and supply‑chain leverage to secure allocation and pass higher costs on to consumers.

Apple has already raised prices across several product lines, while Microsoft has increased the price of its Xbox Series S and warned that memory costs may double again by 2027. Their margins will tighten, but their market positions remain secure.

Smaller manufacturers face a far harsher reality. Start‑ups, niche hardware makers and mid‑tier consumer electronics brands are being pushed to the back of the queue, forced to pay inflated prices or accept long delays. Some may simply be unable to ship products at all

Pressure.

Companies such as GoPro have already warned investors of existential pressure, and others in the audio, camera and budget‑device sectors are quietly preparing for cancelled launches or reduced specifications.

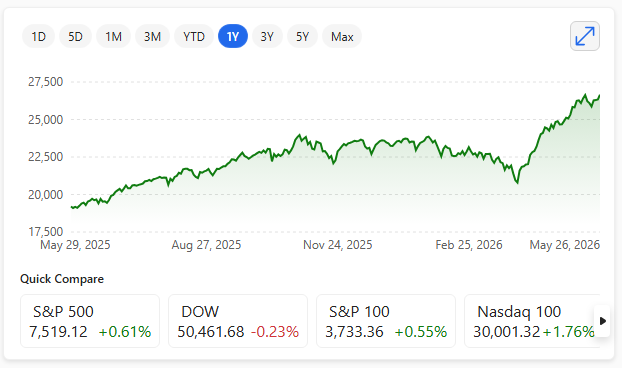

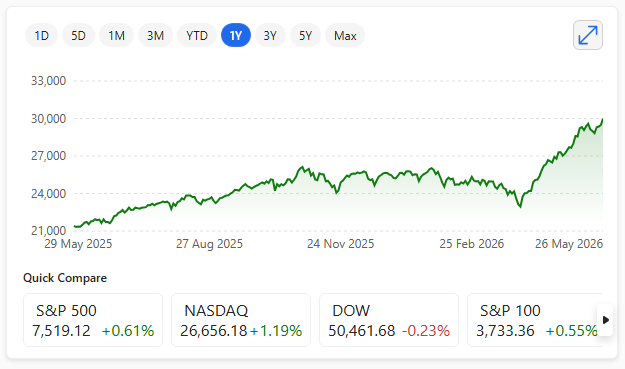

The stock market has responded unevenly. Memory suppliers like Micron and SK Hynix have seen extraordinary rallies, with margins soaring and investors betting on prolonged demand.

Meanwhile, smaller hardware firms are experiencing sharp declines as profitability evaporates.

Longer term, the memory crunch may accelerate consolidation. If supply remains tight, the industry could tilt even further towards a handful of dominant players, with innovation increasingly concentrated among those able to afford the rising cost of participation.