United Kingdom – Latest Data This Week to June 19th 2026

Labour market:

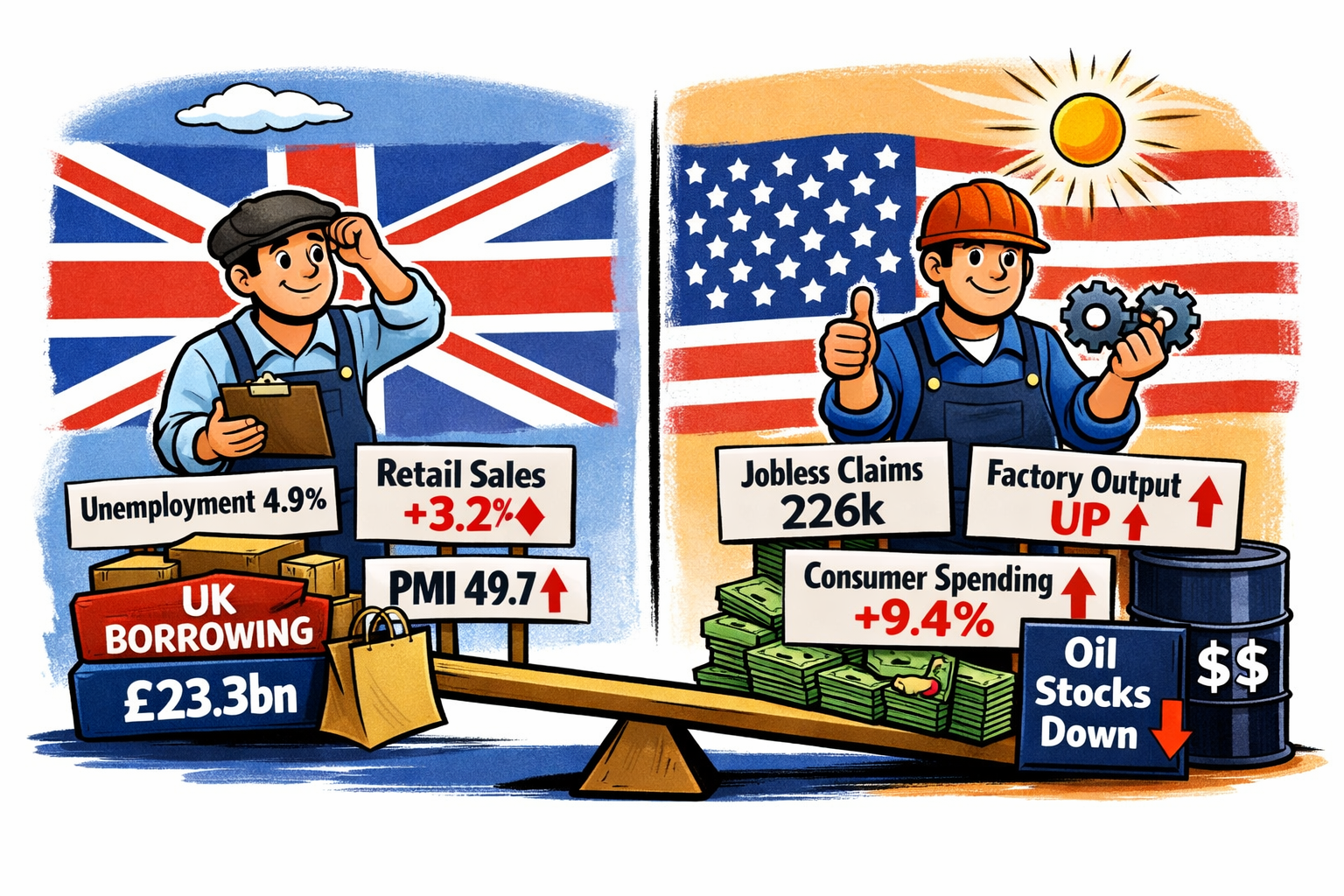

- The UK unemployment rate for April 2026 held at 4.9%, slightly below the previous 5% reading. Average earnings including bonuses grew 4.4%, while earnings excluding bonuses rose 3.4%. Employment increased by 100,000 in April, although HMRC payrolls for May showed only a marginal +2,000 change.

Retail sales:

- Retail sales rebounded strongly in May 2026, rising 1.2% month‑on‑month and 3.2% year‑on‑year, reversing April’s declines. Retail sales excluding fuel also rose 1.2% MoM and 4.6% YoY.

Public finances:

- Public sector net borrowing (excluding banks) came in at £23.3bn in May, slightly worse than April’s revised figure.

Business activity:

- Flash PMIs for June show mixed momentum:

- Manufacturing PMI: 53.9 (expansion)

- Services PMI: 49.3 (contraction)

- Composite PMI: 49.7 (borderline contraction) These readings suggest the UK economy is losing some pace heading into summer.

United States – Latest Data This Week to 19th June 2026

Labour market:

- Initial jobless claims for the week ending 13th June 2026 fell slightly to 226,000, broadly in line with expectations. Continuing claims rose to 1.81 million, indicating some softening in labour market conditions.

Manufacturing & business surveys:

- The Philadelphia Fed Manufacturing Index jumped to 10.3 in June from –0.4, signalling a notable improvement in factory activity.

- The S&P Global flash PMIs for June show:

- Manufacturing: 55.1 (solid expansion)

- Services: 50.7 (modest expansion)

- Composite: 51.5 (steady growth) These point to a resilient US private‑sector backdrop.

Housing & consumer indicators:

- Mortgage rates eased slightly, with the 30‑year rate dipping to 6.47%.

- Redbook retail sales rose 9.4% YoY, suggesting firm consumer spending.

Capital flows & energy:

- Net long‑term TIC flows for April registered $103.1bn, indicating strong foreign demand for US assets.

- API data showed a sharp –8.33 million barrel draw in crude oil stocks, hinting at tighter near‑term supply.

Overall Pictures for UK and U.S.

- UK: A mixed week — labour market steady but softening at the margins; retail sales surprisingly strong; PMIs signalling a mild loss of momentum; public borrowing still elevated.

- US: Data broadly stronger — manufacturing rebounded, services steady, jobless claims stable, and consumer spending indicators show firm.