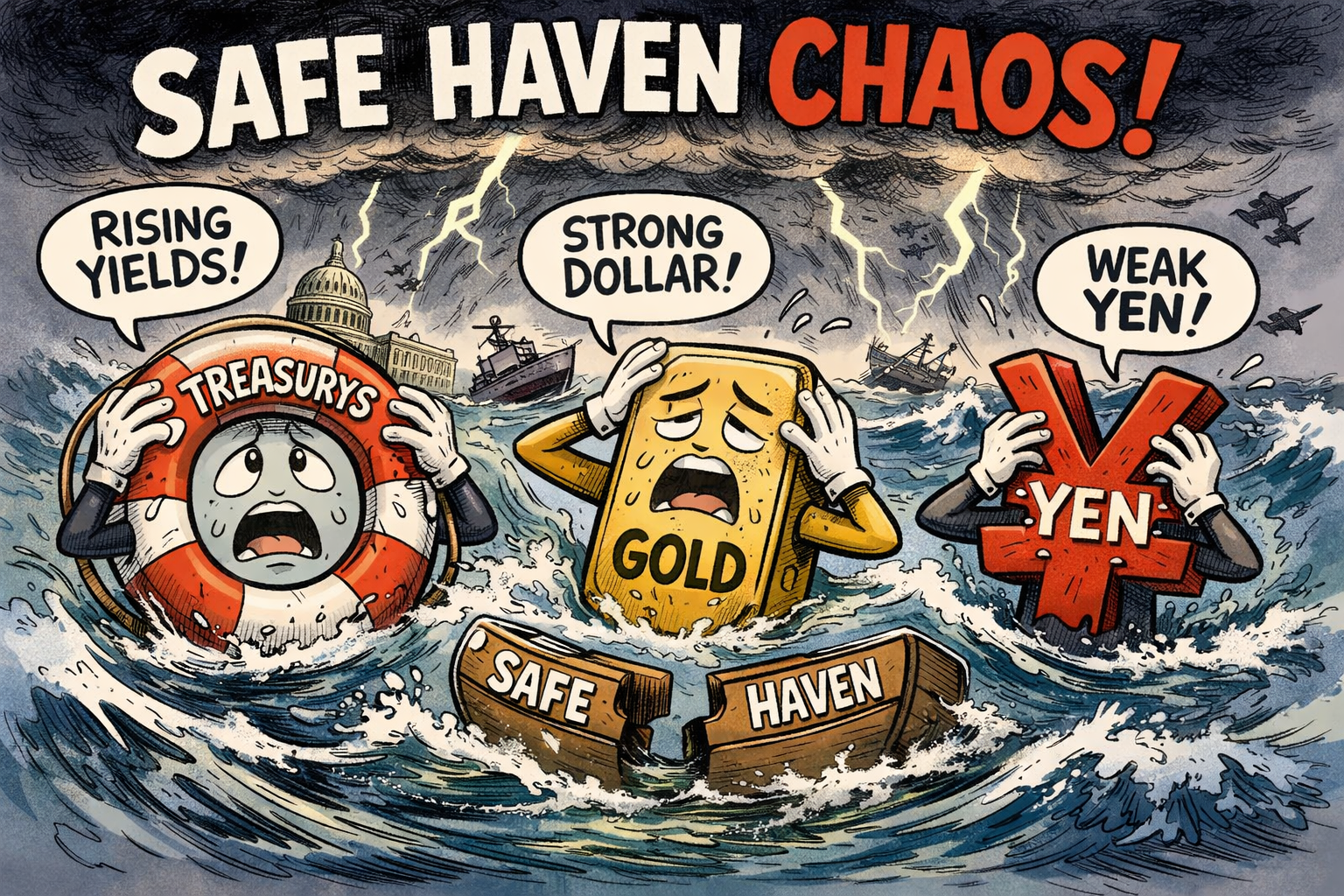

Safe havens are still called safe havens, but their behaviour in 2026 shows they’re no longer the automatic bolt‑holes investors once relied on.

The old crisis playbook — buy Treasurys, buy yen, buy gold — has been scrambled by a very different macro environment, where inflation, fiscal strain and policy divergence overpower fear.

Treasuries?

U.S. Treasuries, historically the world’s default refuge, have been moving the “wrong” way. Instead of yields falling during geopolitical shocks, they’ve risen — a direct consequence of higher real yields and persistent inflation expectations.

When oil doubled after the Iran conflict closed the Strait of Hormuz, markets didn’t panic into bonds; they repriced inflation.

Add the United States’ swollen deficit, and Treasuries suddenly look less like a sanctuary and more like an asset with its own vulnerabilities.

Gold?

Gold, the ancient crisis hedge, has also lost its shine. Despite war and volatility, prices have sagged from their January 2026 peak.

A stronger dollar and elevated real yields have dominated its behaviour, while last year’s retail-driven surge left the market more exposed to “fast money” unwinding than to traditional safe-haven flows.

Structurally, gold still works — but tactically, it’s been unreliable.

Yen?

The yen, once the quintessential risk-off currency, has arguably suffered the biggest reputational hit. Even with the Bank of Japan hiking rates to 30‑year highs and intervening heavily, the currency has slid to multi‑decade lows.

Japan’s towering debt load and stark policy divergence from other major central banks have made yield differentials overpower fear.

Fundamentals

Safe havens haven’t disappeared — they’ve fragmented. Instead of rising together when markets wobble, each now responds to its own fundamentals.

In a world where investors chase AI equities even during war, resilience requires a broader mix of assets, not blind faith in yesterday’s refuges.