The Dow Jones Industrial Average (DJIA) hit a new all-time high, on 13th December 2023. It closed at 36799 surpassing its previous record of 36585points that it had set on 4th January 2022. This was the fourth consecutive record close for the index.

Record high

The Dow’s record high was driven primarily by the Fed holding the interest rate at 5.5% and signalling that it expects to cut interest rates three times in 2024 to stimulate growth and inflation.

Other factors such as strong corporate earnings, optimism about the economic recovery from the COVID-19 pandemic, the emergence of AI and its effect on the economy and for a U.S. ‘soft landing’ all played their part.

Dow a bellwether for the U.S. economy

The Dow is not only a measure of stock market performance, but also a reflection of the overall health and confidence of the U.S. economy. It is often used as a benchmark for investors and analysts to evaluate their portfolios and strategies. The Dow is also closely watched by policymakers and media outlets as a measure of public sentiment and expectations.

Dow hits new all-time high

Dow hits new all-time high

The Dow, in intraday trading, continued to climb to over 37200.

Fed holds U.S. rates at 5.5%, indicates three cuts coming in 2024

The Federal Reserve on Wednesday 13th December 2023 held its key interest rate steady for the third time in a row and set the scene for multiple rate cuts in 2024 and 2025.

With inflation easing and the economy holding up policymakers Federal Open Market Committee policymakers voted unanimously to keep the rate in a range between 5.25%-5.5%.

Possible three Fed rate cuts pencilled in for 2024

Along with the decision to stay on hold, the FOMC pencilled in at least three rate cuts in 2024, assuming quarter percentage point increments. That’s less than market pricing of four, but more aggressive than what officials had previously indicated.

Markets had widely anticipated the status quo decision which could end a cycle that has seen 11 hikes, pushing the interest rate to its highest level in more than 22 years. There was uncertainty, though, about how ambitious the FOMC might be regarding policy easing.

The FOMC’s so called ‘dot plot’ of individual members’ expectations indicate another four cuts in 2025, or a full 1%. Three more reductions in 2026 would take the Fed rate down to between 2%-2.25%, close to the longer-term outlook, though there were considerable difference in the estimates for the final two years.

Dow at new all-time high!

Following the Fed update the Dow Jones Industrial Average jumped more than 400 points, surpassing 37,000 for the first time creating a new Dow all-time high.

Prices across a wide spectrum of goods and services moved slightly higher in November 2023 but were mostly in line with expectations, thus further easing pressure on the Federal Reserve.

The consumer price index, a closely watched inflation gauge, increased 0.1% in November, and was up 3.1% from a year ago, the U.S. Bureau of Labor Statistics reported Tuesday 12th December 2023.

While the monthly rate indicated a pickup from the flat CPI reading in October 2023, the annual rate showed another decline after hitting 3.2% a month earlier.

Gold prices on Monday 27th November 2023 climbed to a more than six-month high as the U.S. dollar weakened.

Investors, it is reported, have placed their bets, suggesting the Federal Reserve is finished with interest rate hikes.

Gold was up around 0.52% at $2,012 per ounce in early afternoon trading (London time). It reached a high of $2,017.82 earlier in the day. Gold futures for December 2023 hit $2,018.90 according to analysts’ data.

The dollar index, a measure of the greenback against major currencies, was 0.13% lower as markets price in a more than 90% chance the Fed will hold rates at its next two meetings.

Analysts at Goldman Sachs reportedly said that the outlook for 2024 is that gold’s ‘shine is returning’.

The potential upside in gold prices will be closely tied to U.S. real rates and dollar moves.

Federal Reserve members, in their most recent meeting, gave little indication of cutting interest rates anytime soon, particularly as inflation remains well above their goal of 2%, according to minutes released Tuesday 21st November 2023.

The detail of the meeting held 31st October – 1st November 2023, showed that Federal Open Market Committee (FOMC) members are still concerned that inflation could be stubborn or move higher, and that more may need to be done.

They indicated that policy would need to stay ‘restrictive’ at the very least, inflation is on a convincing move back to the central bank’s 2% goal.

Observing the data available at CME FedWatch the stock market does not seem to expect the Fed to start cutting rates aggressively anytime soon, this opinion is based on the current pricing data of the fed-funds futures market.

According to the CME FedWatch Tool, the probability of a rate cut in the next FOMC meeting on 13th December 2023 is very low. It is likely interest rates will be left unchanged.

The market seems to expect the Fed will hold the current rate of 5.25% until at least March 2024, but will then gradually lower it to 4.75% by December 2024.

The market seems to be more optimistic about the U.S. economic outlook and the Fed’s ability to control inflation. The mood on rates has been buoyed recently with inflation data coming in better than expected.

It is highly likely that the Fed will have to cut rates more aggressively in 2024 and 2025 to stimulate the economy and avoid a potential prolonged recession.

Fed Chair Jerome Powell reportedly said he and his colleagues remain steadfast in getting policy in line with their 2% inflation target, but ‘we are not confident that we have achieved such a stance’.

He stressed the Fed nevertheless can be cautious as the risks between doing too much and too little have come into closer balance.

Federal Reserve Chairman Jerome Powell reportedly said Thursday 9th November 2023 that he and his fellow policymakers are encouraged by the slowing pace of inflation but are unsure whether they’ve done enough to keep the momentum going.

Inflation battle

Speaking a little more than a week after the central bank voted to hold rates steady, Powell said in remarks aimed at the International Monetary Fund (IMF) gathering in Washington, D.C., that more work could be ahead in the battle against high prices.

The statement comes with inflation still well above the Fed’s long-standing goal but also considerably below its peak levels in the first half of 2022. After 11 U.S. rate hikes, we have witnessed the most aggressive policy tightening since the early 1980s, the FOMC have increased rates from pretty much zero to a range of 5.25%-5.5%.

Those increases have coincided with the Fed’s preferred inflation gauge, the core personal consumption expenditures price index, to fall to an annual rate of 3.7%, from 5.3% in February 2022. The more widely followed consumer price index peaked above 9% in June of last year.

Progress

Powell referenced the progress the economy has made. Gross domestic product (GDP) accelerated at a ‘quite strong’ 4.9% annualised pace Q3 2023, though Powell also said the expectation is for growth to ‘moderate in coming quarters’. He described the economy as ‘just remarkable’ in 2023 in the face of a broad expectation that a recession was inevitable.

Nothing like a massive ‘self-pat’ on the back for a job well-done? Remember the Fed’s initial analysis? IT was for inflation to be ‘transitory’. They didn’t get that right either.

Futures pricing, according to the CME Group, suggested there’s less than a 10% chance that the FOMC will approve a final rate hike at its Dec. 12-13, 2023, meeting, even though committee members in September pencilled in an additional 0.25% rise before the end of 2023.

Impression drawing of Fed Chair. The Fed is ‘not confident’ according to Jerome Powell.

Traders anticipate the Fed will start cutting rates next year, probably around June 2024.

Central banks, 18 months ago got it fundamentally wrong and they got it wrong on many other occasions too.

So why take any notice?

The Fed and other central banks insisted that inflation would be ‘transitory’ – it wasn’t. It reached 7%. That’s 5% above the target of 2%.

Along with the misdiagnosis on prices, Fed officials, according to projections released in March 2022, collectively saw the key interest rate rising to just 2.8% by the end of 2023. It is now 5.25%.

The Great Depression (1929–1939) was an economic bomb that affected countries across the world. It was a period of severe economic depression after a major fall in stock prices in the United States. It began around September 1929 and led to the Wall Street stock market crash on 24th October 1929 (Black Thursday). See Wikipedia article here.

It was the longest, deepest, and most widespread depression of the 20th century.

The Great Depression of 1929

The Great Inflation

The Fed pursued an overly expansionary monetary policy in the 1960s and 1970s, which fueled high inflation and eroded the value of the dollar. The Fed also underestimated the impact of oil shocks and other supply shocks on inflation and was slow to tighten monetary policy to restore price stability. The Fed eventually raised interest rates sharply in the late 1970s and early 1980s, which triggered a severe recession. And in1991 inflation surged to 8.5%.

The Great Recession

The Fed likely contributed to the build-up of financial imbalances and excessive risk-taking in the 2000s, (Dotcom bubble) – by keeping interest rates too low for too long and by failing to adequately supervise and regulate the financial system.

The Fed likely contributed to the build-up of financial imbalances and excessive risk-taking in the 2000s

The Fed also reacted too slowly to the emerging signs of distress in the housing market and the financial sector and was unprepared for the global financial crisis that erupted in 2008. Remember, ‘sub-prime’ lending. We can see signs of similar stress in the U.S. car loan market now.

The Fed and other central banks including the Bank of England initially underestimated the severity and duration of the pandemic and its impact on the economy. The Fed also overestimated the transitory nature of inflation, which surged to a 30-year high in 2021 due to supply chain disruptions, pent-up demand, fiscal stimulus, and base effects. The Fed maintained an ultra-accommodative monetary policy stance for too long, despite mounting evidence of overheating and inflationary pressures.

The Fed finally raised interest rates by 0.75% in December 2022, but faced criticism for being behind the curve and for communicating poorly with the markets.

Transitory inflation

The Fed said inflation would be transitory in 2021 and 2022. The Fed used this term to describe the higher-than-normal prices that emerged during the Covid-19 economic crisis, which were expected to be temporary and not part of a long-term trend. The Fed attributed the inflation surge to factors such as supply chain bottlenecks, pent-up demand, fiscal stimulus, and base effects.

The Fed also said that it would let inflation run above its 2% target for some time, to achieve an average inflation rate of 2% over time. However, as inflation remained high and persistent in 2021 and 2022, the Fed faced criticism for being behind the curve and for communicating poorly with the markets. The Fed eventually raised interest rates.

And now, much of the same. The Fed is again ‘tinkering’ with policy to manage ‘transitory’ inflation and will most probably engineer a recession as a result.

The U.S. Treasury yields are the interest rates that the U.S. government pays to borrow money for different periods of time.

The 10-year Treasury yield is one of the most important indicators of the state of the economy and the expectations of inflation and growth. On 23rd October 2023, the 10-year Treasury yield rose above 5% for the first time since 2007, as investors increasingly accepted that interest rates will stay higher for longer and that the U.S. government will further increase its borrowing to cover its deficits.

Significant

This is a significant milestone, as it reflects the market’s view that the Federal Reserve will maintain elevated interest rates to control inflation and that the U.S. economy will remain resilient despite the challenges posed by the Covid-19 pandemic, geopolitical tensions and environmental issues.

The higher yield also means that the government will have to pay more to service its debt, which could affect its fiscal policy and spending priorities. The higher yield also affects other borrowing costs, such as mortgages, student loans, and corporate bonds, which could have implications for consumers and businesses.

10 Year Yield

The 10-year Treasury yield is influenced by many factors, such as supply and demand, inflation expectations, economic growth, monetary policy, and global events. The yield has been rising steadily since it hit a record low of 0.5% in March 2020, when the pandemic triggered a flight to safety and a massive stimulus from the Fed. Since then, the yield has been driven by the recovery of the economy, the surge in inflation, the reversal of the Fed’s bond-buying program, and the increase in the government’s borrowing needs.

Yield curve

The ten-year yield is closely watched by investors, analysts and policymakers as it provides a benchmark for valuing other assets and assessing the outlook for the economy. The yield is also used to calculate the yield curve, which is the difference between short-term and long-term Treasury yields.

The shape of the yield curve can indicate the market’s expectations of future interest rates and economic activity.

Artwork impression of computer screen: U.S. ten-year treasury yield breaches 5% for the first time since 2007

A steep yield curve means that long-term yields are much higher than short-term yields, which suggests that investors expect higher inflation and growth in the future. A flat or inverted yield curve means that long-term yields are lower than or equal to short-term yields, which implies that investors expect lower inflation and growth or even a recession.

The current yield curve is steepening, as long-term yields are rising faster than short-term yields. This indicates that investors are anticipating higher inflation and growth in the long run, but also that they are concerned about the sustainability of the government’s fiscal position and the impact of higher interest rates on the economy.

Indicators

The 10-year Treasury yield is an important indicator of the state of the economy and the expectations of inflation and growth. It has reached a level that has not been seen since before the global financial crisis of 2008-2009. This reflects the market’s view that interest rates will stay higher for longer and that the government will increase its borrowing to cover its deficits. The higher yield also affects other borrowing costs and asset prices, which could have implications for consumers and businesses.

The yield is influenced by many factors and is closely watched by investors, policymakers, and analysts. A 5% yield is a worry for the market, inflation, interest rates, geo-political risks and recession are the others, that’s enough!

The interest the government pays on national debt has reached a 20-year high as the rate on 30-year bonds touches 5.05%.

A rise in the cost of borrowing comes at a difficult time for the chancellor, Jeremy Hunt, as he prepares for the autumn statement on 22nd November 2023. The chancellor has already made clear that tax cuts will not be announced in the autumn statement.

National debt £2,590,000,000,000

The total amount the UK government owes is called the national debt and it is currently about £2.59 trillion – £2,590,000,000,000.

The government borrows money by selling financial products called bonds. A bond is a promise to pay money in the future. Most require the borrower to make regular interest payments over the bond’s lifetime.

UK government bonds – known as ‘gilts’ – are normally considered very safe, with little risk the money will not be repaid. Gilts are mainly bought by financial institutions in the UK and abroad, such as pension funds, investment funds, banks and insurance companies.

QE

The Bank of England (BoE) has also bought hundreds of billions of pounds’ worth of government bonds in the past to support the economy, through a process called quantitative easing or QE.

A higher rate of interest on government debt will mean the chancellor will have to set aside more cash, to the tune of £23 billion to meet interest payments to the owners of bonds. This in-turn means the UK government may choose to spend less money on public services like healthcare and schools at a time when workers in key industries are demanding pay rises to match the cost of living.

Double debt

The current level of debt is more than double what was seen from the 1980s through to the financial crisis of 2008. The combination of the financial crash in 2007/8 and the Covid pandemic pushed the UK’s debt up from those historic lows to where it stands now. However, in relation to the size of the economy, today’s debt is still low compared with much of the last century.

UK debt £2,590,000,000,000

The U.S, German and Italian borrowing costs also hit their highest levels for more than a decade as markets adjusted to the prospect of a long period of high interest rates and the need for governments around the world to borrow.

It follows an indication from global central banks, including the United States Federal Reserve and the Bank of England (BoE), that interest rates will stay ‘higher for longer’ to continue their jobs of bringing down inflation.

£111billion on debt interest in a year

During the last financial year, the government spent £111 billion on debt interest – more than it spent on education. Some economists fear the government is borrowing too much, at too great a cost. Others argue extra borrowing helps the economy grow faster – generating more tax revenue in the long run.

The Office for Budget Responsibility (OBR), has warned that public debt could soar as the population ages and tax income falls. In an ageing population, the proportion of people of working age drops, meaning the government takes less in tax while paying out more in pensions, welfare and healthcare services.

The latest U.S. jobs report for September 2023 was released on Friday, October 6, 2023.

The U.S. economy added 336,000 jobs last month, much more than expected, despite the Federal Reserve’s struggle to cool the world’s largest economy.

The unemployment rate was 3.8%, in line with August 2023. The data lifted hopes that the central bank will manage to guide the U.S. economy to a ‘soft landing’, where a recession is avoided. Bear in mind the Fed were late in dealing with the initial rise in inflation – so this battle has become harder and prolonged.

The job gains were the largest monthly rise since January 2023, and almost twice what economists had anticipated. Government and healthcare added the most jobs. The labour market still appears solid.

However, not all indicators were positive. The ADP’s national employment report showed that private-sector employers added only 89,000 jobs in September, far fewer than expected. Some factors outside the Fed’s control, such as the autoworker strike and the threat of a government shutdown, could yet damage the U.S. economy.

The labour force participation rate also remained low at 63.2%, indicating that many workers have yet to return to the labour market since the Covid19 pandemic of 2020.

The stock market has been experiencing some volatility and uncertainty in September and October 2023, as investors fret about inflation, interest rates, and the possibility of a U.S. recession.

Main facts affecting the current stock market

The month of October has produced some severe stock market crashes over the past century, such as the Bank Panic of 1907, the Wall Street Crash of 1929, and Black Monday 1987.

October has also marked the start of several major long-term stock market rallies, such as Black Monday itself and the 2002 nadir of the Nasdaq-100 after the bursting of the dot-com bubble.

The S&P 500 dropped 4.5% in September 2023 and finished the third quarter in the red.

The U.S. Treasury yield curve has been inverted for months – which is a historically strong recession indicator.

The Fed maintained interest rates at the current target range of between 5.25% and 5.5% in September 2023, but signalled that it may need to raise rates again to combat inflation.

The consumer price index gained 3.7% year-over-year in August 2023, down from peak inflation levels of 9.1% in June 2022 but still well above the Fed’s 2% long-term target.

The bond market is currently pricing in an 81.7% chance the Fed will choose not to raise rates again on 1st November 2023.

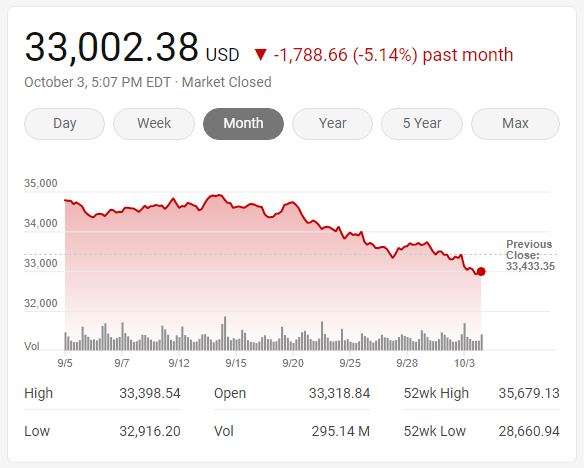

The Dow Jones Industrial Average was down at 33002, Tuesday 3rd October 2023.

Stocks fell as investors pulled money from equities and moved it to the hot bond market.

International markets also faced significant turmoil, sending mini shockwaves through global financial centres, which reverberated in equities.

The dollar rose to the highest since December and is heading towards the twelfth positive week in a row.

Uncertainty

Uncertainty in the U.S. political system is having a major affect too. Especially with the ousting of the speaker and the real fear of a government shutdown looming large.

The U.S. Treasury yields are the interest rates that the U.S. government pays to borrow money. The 10-year and 30-year Treasury yields are the most widely followed indicators of the long-term health of the U.S. economy and the expectations of inflation and growth.

10 year yield at 4.80%

According to the latest data, the 10-year Treasury yield surged to 4.80% on Tuesday, 3rd October 2023, which is the highest level since 12th October 2007.

30 year yield at 4.79

The 30-year Treasury yield rose to 4.79% on Monday, 2nd October 2023, which is the highest since 6th April 2010.

The main reasons for the rise in the Treasury yields

The strong U.S. economic data that showed that the labour market remains hot and the manufacturing sector rebounded in September 2023.

The Federal Reserve’s ‘higher for longer’ mantra signalled that the central bank would keep raising rates until inflation is under control.

The reduced demand for safe-haven assets as the U.S. government averted a shutdown over the weekend by passing a short-term stopgap funding measure.

Uncertainty at the heart of the U.S. political system.

The implications of higher Treasury yields

The higher borrowing costs could weigh on the economic growth and consumer spending in the future.

Higher inflation expectations could erode the purchasing power of the fixed-income investors and increase the risk of a bond market sell-off.

The higher interest rate differential could attract more foreign capital inflows into the U.S. dollar and strengthen its value against other currencies.

The Federal Reserve held interest rates steady in a decision released Wednesday 20th September 2023, while also indicating it still expects one more hike before the end of the year and fewer cuts than previously indicated next year.

That final increase, if realised, would be it for now according to data released at the end of the Fed two-day meeting. If the Fed goes ahead with the move, it would be the twelfth rate hike since policy tightening began in March 2022.

No change priced in

Markets had fully priced in no move at this meeting, which kept the fed funds rate targeted in a range between 5.25%-5.5%, the highest in some 22 years. The rate fixes what banks charge each other for overnight lending but also affects many other forms of consumer debt too.

While the no-hike was expected, there was plenty of uncertainty over where the rate-setting Federal Open Market Committee (FOMC), would go from here.

Judging from reports released Wednesday 20th September 2023, the bias appears towards more restrictive policy and a higher-for-longer approach to interest rates.

At 4.33%, the 10-year Treasury yield in the U.S. is at its highest in 16 years. That represents a risk-free, long-duration asset with relatively high returns and this is challenging the stock market.

Why should traders invest in stocks that may not return as much, or just slightly more and take unecessary risks, when there is an asset class that guarantees around 4% return or slighlty more?

Cash is king?

Cash is now yielding 5% in the U.S., short term bonds are yielding 5% plus, so equities for the first time in a long time, have actually got some competition.

Typically stocks if they do well, are likely to return more than a risk-free asset, precisely because it isn’t certain stocks will rise. That’s called the equity risk premium, a return that’s supposed to compensate stock investors for the chance that they might lose money. But, as the premium is below 1% now. Historically, it’s been between 2% and 4% – meaning stocks are looking much less attractive than Treasuries.

Harder job for the Fed?

Another potential issue that could crop up with high Treasury yields is that it could make the Federal Reserve’s job tougher. During the recent Jackson Hole gathering, the Fed head has indicated that more interest rate hikes are still high possibility.

But don’t panic just yet… this is likely a pullback phase of a bull market analysts suggest. That is, it’s still too early to be bearish on stocks.

Yardeni Research president Ed Yardeni is reported to have said that the market is ‘going to hang in there’ and ‘a year-end rally will bring the S&P 500 back to something like 4,600‘.

That implied an increase of almost 5% in stocks – while not certain – would give Treasuries a run for their money again.

The FEDNOW payment system is a new instant payment infrastructure developed by the Federal Reserve that allows financial institutions of every size across the U.S. to provide safe and efficient instant payment services.

Live system

It went live on July 20, 2023 and enables individuals and businesses to send and receive money in near real-time, 24/7/365, through their depository institution accounts.

The service is a flexible, neutral platform that supports a broad variety of instant payments and offers optional features such as fraud prevention tools, request for payment capability, and tools to support payment inquiries.

FedNow is the first new payment rail in the United States since the introduction of the Automated Clearing House (ACH) in the early 1970s.

Digital Dollar?

Is this a possibly a pre-emptive strike to get ahead of international digital currency deployment and set the scene to adopt a digital payment structure of a new ‘crypto coin system’ for the future – the digital dollar?