Over the last weekend of June 2024, China released its official PMI figures, with the manufacturing PMI remaining at 49.5, the same as in May 2024, indicating a second consecutive month of contraction.

On Monday 1st July 2024, Japan adjusted its first-quarter GDP figures, showing a contraction of 2.9% year-on-year, a revision from the previously reported 1.8%.

Asia markets started the second half 2024 mixed as investors assessed June business activity data from China as well as Japan’s GDP revision.

On Friday 28th June 2024, the Japanese yen dropped to its lowest point in 38 years, surpassing the 161 threshold against the dollar reached for the first time since December 1986.

The yen has faced challenges, slipping beyond the 160 mark again.

Since the Bank of Japan concluded its negative interest rate policy and reportedly abandoned its yield curve control policy in March 2024, the yen has been on a consistent decline.

After this policy change, the yen breached the 150 level against the U.S. dollar and hit 160 in late April 2024, which prompted intervention by the country’s finance ministry.

UK economy purring but not roaring like a lion… yet!

The UK economy expanded more than initially thought in the first quarter of 2024, signalling a recovery from recession, according to updated official data.

The Office for National Statistics (ONS) reported that from January to March 2024, the economy experienced a growth of 0.7%, revised from the preliminary estimate of 0.6% released last month.

The ‘Sahm Rule’ serves as a heuristic indicator employed by the Federal Reserve to ascertain the onset of a recession in the economy.

The Sahm Rule is a real-time evaluation tool based on monthly unemployment data from the Bureau of Labor Statistics (BLS). Named after economist Claudia Sahm, it forecasts the onset of a recession when the three-month moving average of the national unemployment rate (U3) increases by 0.50% or more compared to its lowest point in the preceding 12 months.

This simple yet effective indicator helps policymakers monitor economic cycles and respond accordingly

Time to cut according to the ‘Sahm Rule’

Sahm has reportedly stated that the Fed is taking a significant risk by not implementing gradual rate cuts now. Last week, Federal Reserve officials significantly reduced their forecasts for rate cuts this year, shifting from three anticipated reductions noted in the March 2024 meeting to just one.

According to the creator of a well-established rule for predicting recessions, the Federal Reserve is risking an economic contraction by not lowering interest rates immediately.

In May 2024, China’s retail sales exceeded forecasts, increasing by 3.7% from the previous year and surpassing the anticipated 3% rise.

Conversely, industrial output experienced a 5.6% growth on an annual basis, falling short of the projected 6% increment. Meanwhile, fixed asset investment saw a 4% increase from the previous May, narrowly missing the predicted 4.2% growth.

In April 2024, the U.K.’s economic growth came to a standstill, figures released on Wednesday 12th June 2024 indicated, putting a pause on the subdued recovery from the previous year’s recession just weeks before the UK election.

Analysts had anticipated growth a levelling off following a 0.4% expansion in March 2024.

Over a longer period however, the outlook was slightly more positive, with a 0.7% increase in gross domestic product (GDP) in the three months leading up to April 2024.

The construction sector saw a 1.4% decrease, marking its third consecutive decline, and production output fell by 0.9%. However, the U.K.’s dominant service sector witnessed growth, with a 0.2% increase.

The UK had managed modest growth each month in the first quarter of the 2024 as the country emerged from a mild short technical recession.

Bad economic news appears to have had an interesting impact on the stock market recently.

Traditionally, negative economic data might be anticipated to result in falling stock prices; however, recent trends have diverged from this norm.

News trend

In the past two months, negative economic news has had a paradoxically positive effect on equities. Investors have responded well to poor economic indicators, partly due to the belief that these could lead the Federal Reserve to begin reducing interest rates.

Dollar and the stock market

In recent times, the S&P 500, a large-cap equity index, and the U.S. dollar have exhibited a nearly perfect correlation. As the dollar has seen a gradual decline, the stock market has conversely experienced a rise. Typically, investors flock to the security of cash, and consequently the dollar, in times of uncertainty, yet they also channel investments into stocks upon the arrival of favourable news.

Economic data

Despite the upbeat trend in the stock market, real economic data has frequently fallen short of Wall Street’s predictions. The Citi Economic Surprise Index, a gauge that compares data to expectations, has been on a downward trajectory. This suggests that expectations have been surpassing the actual economic conditions, signalling that the economic situation may not be as favorable as previously thought.

Dilemma for the Fed

The Federal Reserve methodically reviews economic indicators to influence their interest rate decisions. Typically, unfavorable economic reports might prompt the Fed to reduce rates, unless there’s an uptick in inflation. Escalating inflation generally nudges the Fed towards a tighter monetary policy.

Monthly data roll-out

Data concerning the U.S. labour market presented to the Fed and markets may create that ‘pivotal’ moment – it often does – markets move of Fed comments and ‘awaited’ news. Reports detailing job openings, private sector job creation, and the Bureau of Labour Statistics’ nonfarm payrolls will shed light on the economy’s condition.

If job growth remains within the ‘Goldilocks range’ (neither too strong nor too weak), it may preserve the fragile equilibrium where unfavourable economic news has paradoxically favoured stock prices, while preventing excessive gloom.

Conclusion

To summarize, although adverse economic news has lately been advantageous for stock markets, monitoring this precarious balance is crucial. Excessive pessimism could be a harbinger of impending difficulties, despite its current benefits.

Note about Citigroup Economic Surprise Index

The Citigroup Economic Surprise Index is the sum of the difference between the actual value of various economic data and their consensus forecast. If the index is greater than zero, it means that the overall economic performance is generally better than expected, and the S&P 500 has a high probability of strengthening, and vice versa.

Economists expected a smaller retail sales fall of 0.4%.

Sales volumes declined across multiple sectors, with clothing retailers, sports equipment, games and toys stores, and furniture outlets experiencing a downturn as adverse weather conditions led to a decrease in customer visits, according to the ONS.

March’s figure was revised from flat to a 0.2% decline.

Sales increased by 0.7% over the three months leading up to April, compared to the preceding three months, despite a sluggish December and holiday season. However, there was a 0.8% decline when compared with the same period last year.

Will the Bank of England (BoE) drop interest rates in June now that inflation is down to 2.3% – close to the target of 2%?

The April inflation came in higher than anticipated, falling to 2.3%, as reported by the Office for National Statistics on Wednesday 22nd May 2024.

Traders have now reduced their expectations of a June interest rate cut by the Bank of England (BoE). Markets reacted negatively in early trading.

The headline inflation rate decreased from 3.2% in March, marking the first instance since July 2021 that inflation has fallen below 3%, nearing the Bank of England’s target of 2%.

Contrary to the predictions of economists surveyed by Reuters, who expected a more significant drop to 2.1%, services inflation – a critical indicator monitored by the BOE due to its significance in the UK economy and as a gauge of domestically generated price increases – only fell marginally to 5.9% from 6%, missing the anticipated 5.5% from the BOE.

Core inflation, which excludes energy, food, alcohol, and tobacco, decreased to 3.9% in April from 4.2% in March.

The substantial decline in the headline rate was largely anticipated due to the year-on-year decrease in energy prices. However, investors shifted their attention to core and services inflation following indications from BOE policymakers of a potential interest rate cut later in the summer, contingent on new data.

After the data release, the market-makers probability of a June rate cut plummeted to 15% from 50% and the chance of an August cut also fell to 40% from 70%.

Lingering concerns over underlying inflationary pressures mean a June rate cut is unlikely. However, these figures may convince more rate setters to vote to ease policy, providing a signal that a summer rate cut is still a possibility.

The U.K. economy has recovered from its ‘technical’ recession, with the gross domestic product (GDP) increasing by 0.6% in the first quarter, surpassing expectations.

Official figures released on Friday revealed this growth, which exceeded the 0.4% predicted by economists surveyed by Reuters for the previous quarter.

In the latter half of 2023, the U.K. experienced a mild recession due to ongoing inflationary pressures impacting economic performance.

Technically there is no official definition of a recession – however, two straight quarters of negative growth is widely accepted as a technical recession.

The production sector in the U.K. saw an expansion of 0.8% from January to March, whereas the construction sector experienced a decline of 0.9%. The economy witnessed a growth of 0.4% in March on a monthly basis, succeeding a 0.2% increase in February.

According to the Office for National Statistics, the services sector, which is vital to the U.K. economy, grew for the first time since the first quarter of 2023. This growth of 0.7% was primarily propelled by the transport services industry, marking its most significant quarterly growth since 2020.

Much Ado About Nothing

‘Much Ado About Nothing’ is a comedy by William Shakespeare, written around 1598 – 1599. The play is included in the First Folio, published in 1623, and is set in the Italian city of Messina.

The International Monetary Fund calculates that Russia’s economy will expand more rapidly than all advanced economies this year.

According to the latest World Economic Outlook released by the IMF, Russia’s economy is projected to expand by 3.2% in 2024.

This growth outpaces the anticipated growth rates for the U.S. at 2.7%, the U.K. at 0.5%, Germany at 0.2%, and France at 0.7%.

G7 growth percentages

Russia at 3.2%

U.S. at 2.7%

France at 0.7%

U.K. at 0.5%

Germany at 0.2%

The forecast may be galling for Western countries that have endeavoured to economically isolate, restrict and punish Russia for its invasion of Ukraine in 2022.

Russia has demonstrated that Western sanctions on its industries have made it more self-sufficient and that private consumption and domestic investment remain resilient.

Oil exports

Oil and commodity exports to nations such as India and China, (two of the largest countries in the world by population) – as well as alleged sanction evasion and high oil prices, have allowed Russia to maintain strong oil export incomes streams.

UK and Europe growth

Outside of Russia, the IMF has revised its forecasts for Europe and the UK, projecting a growth of 0.5% for this year. This positions the UK as the second-lowest performer within the G7 group of advanced economies, trailing behind Germany.

The G7 also includes France, Italy, Japan, Canada and the U.S.

However, UK growth is expected to improve to 1.5% in 2025, placing the UK in the top three best G7 performers, according to the IMF.

The IMF also reported said that interest rates in the UK will remain higher than other advanced nations, close to 4% until 2029.

Inflation in the U.K. eased to 3.2% from 3.4% in March, the Office for National Statistics said on Wednesday 17th April 2024.

But a higher-than-expected reading creates more concern as investors push back bets on the timing of the first Bank of England (BoE) rate cut.

Economists expected 3.1% as inflation has been falling gradually since it peaked at 11.1% in late 2022.

Food prices provided the biggest downward drag on the headline rate, the ONS said, while motor fuels pushed it higher.

The core inflation rate, excluding energy, food, alcohol, and tobacco, was reported at 4.2%, slightly above the forecasted 4.1%. Services inflation, closely monitored by U.K. monetary policymakers, decreased from 6.1% to 6%, still surpassing the expectations of economists and the Bank of England (BoE).

The March core inflation figure, remaining above 4%, is expected to fuel speculation that inflation is more persistent than recent projections indicated, potentially delaying the anticipated timing of initial interest rate reductions.

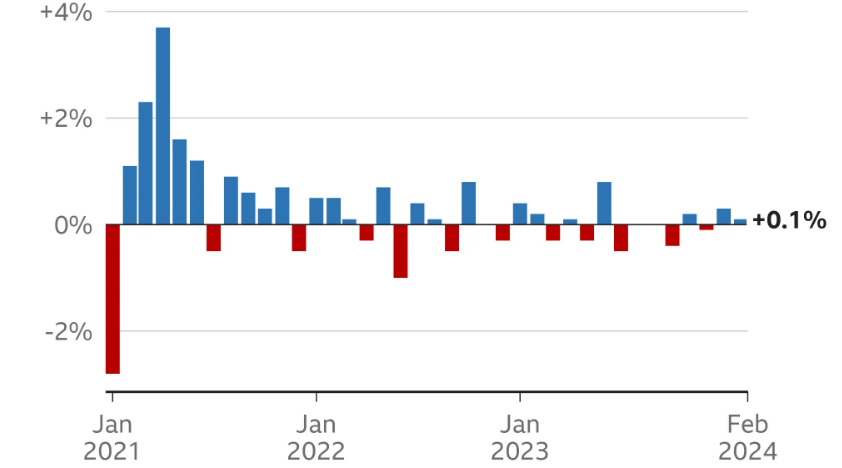

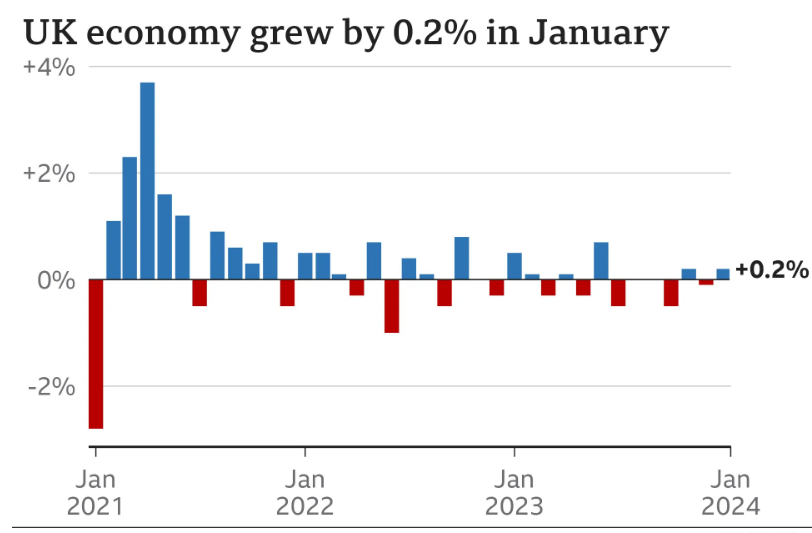

One tenth of 1% is very little but we can at least hope the UK is on it’s on way out of recession

Let’s blame the weather

The economy grew by 0.1%, figures show, boosted by production and manufacturing in areas such as the car sector. The Office for National Statistics (ONS) said that construction was dampened by wet weather.

The official ONS statistics also revised its previous estimate for January 2024 from 0.2% growth up to 0.3%.

Hunt is happy with 0.1% growth…?

Chancellor Jeremy Hunt reportedly suggested that the new figures were a “welcome sign that the economy is turning a corner”. “We can build on this progress if we stick to our plan,” he added.

That’s good then Jeremy – well done you, nice plan!

The Office for National Statistics (ONS) has released updated UK GDP figures, confirming that the UK entered a technical recession in the last six months of the previous year.

The new data shows the economy contracted by 0.1% in the three months from June to August 2023, with a further decline of 0.3% in the subsequent financial quarter from September to December 2023. The overall economy grew by 0.1% throughout 2023.

However, early signs suggest that the UK began to recover in January 2024, with initial data indicating some growth, and surveys suggesting this trend may have gained momentum into February and March 2024.

More than a fifth of working-age adults in the UK are currently not actively seeking employment, according to recent figures.

The economic inactivity rate during the period from November 2023 to January2024 stood at 21.8%, a slight increase compared to the previous year. This means that approximately 9.2 million people aged between 16 and 64 are neither employed nor actively searching for jobs. The total figure has risen by over 700,000 since before the onset of the coronavirus pandemic.

Several factors contribute to this problem

Long-Term Illness: Approximately one-third of the working-age population not participating in the labour force cite long-term illness as the primary reason for their inactivity. Health-related issues have kept a significant portion of the population away from work.

The pandemic: of 2020 caused work flight. 700,000 extra out of the workplace since the coronavirus pandemic Covid 19 hit the UK in 2020.

Students and Education: Students pursuing education are often classified as economically inactive. Their focus on studies and lack of job-seeking activity contribute to this category.

Care Responsibilities: Individuals who care for family members or manage household responsibilities fall into this bracket. Caring duties can be time-consuming and prevent active job hunting.

People with Disabilities: Those with disabilities may face barriers in accessing employment opportunities. Accommodations and inclusive policies are essential to address this issue.

Early Retirement: Some adults choose early retirement, and once retired, they rarely express a desire to return to work. This group contributes significantly to the inactive population.

Discouraged Workers: Individuals who have given up on job searches due to discouragement or lack of suitable opportunities are also part of this category.

Gender Gap: Historically, more women have been classified as economically inactive compared to men. However, this gap has narrowed over the years as more women have entered the workforce.

Age Trends: Recent data indicates that while the number of economically inactive individuals due to illness has decreased, there has been an increase among those aged 16 to 34. Mental health issues are believed to be a contributing factor in this age group.

Persistently high level

The persistently high level of economic inactivity poses challenges for the UK economy. As the country emerges from the pandemic, addressing workforce shortages becomes crucial. Measures such as reducing National Insurance Contributions and extending free childcare services aim to encourage people to seek employment or increase their working hours.

More effort is needed to further incentivise workforce participation, if not, the UK economy will suffer for many more years than would otherwise be necessary.

According to the revised official data, the Japan’s gross domestic product (GDP) grew by 0.4% in the fourth quarter of 2023 compared to the same period in the previous year.

According to this revision, the economy avoided a technical recession, which is usually defined as two successive quarters of negative growth.

On Monday 11th March 2024, Japan’s Cabinet Office released figures that indicated a 0.3% decline in private consumption for the quarter. Private consumption accounts for about 60% of the economy.

Nevertheless, the updated figures fell short of expectations, as some economists had predicted a higher revision in Q4.

In his Capitol Hill testimony on 6th March 2024, Federal Reserve Chairman Jerome Powell reiterated that was not yet time to begin cutting interest rates.

To fight inflation, which reached a rate of 9% in the summer of 2022, the central bank has significantly increased interest rates in recent times. However, prices are still stubborn, especially for things like housing and groceries.

Due to the robust economic performance in early 2024, the expected reduction in interest rates has been postponed. Instead of taking place this month, the rate cuts are now more probable in May or June 2024.

Powell reportedly said: ‘The Committee does not expect that it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.’

He reiterated the pledge to lower inflation to the 2% target and keep long-term inflation expectations stable.

UPDATE

On Thursday 7th March 2024 Powell also said: the Fed is ‘not far’ from the point of cutting interest rates

The U.S. national debt has been growing more quickly in recent months, increasing about $1 trillion nearly every 100 days.

U.S. debt permanently crossed over $34 trillion on 4th January 2024 according to data from the U.S. Department of the Treasury.

It reached $33 trillion on 15th September 2023, and $32 trillion on 15th June 2023. Before that, the $1 trillion move higher from $31 trillion took about eight months.

The U.S. national debt is the total amount of money that the federal government owes to its creditors. That can include, individuals, other countries and corporation. It is composed of two main components: federal debt held by the public and federal governmental debt.

The national debt has grown over time due to various factors, such as recessions, defense spending, and tax cuts. The debt-to-GDP ratio gives insight into whether the US has the ability to cover all of its debt. It also shows how it affects economic growth.

U.S. national debt pile is growing

U.S. national debt is piling up

The national debt increased by 13.3% under President Biden. Up from $27.77 trillion as of 1st March 2020 to $31.46 trillion as of 1st March 2023. The debt also grew by $1.5 trillion, or 5.6%, between the end of 2020 and the end of 2021.

The gross domestic product (GDP) measures the annual economic output of the entire country. The national debt exceeds this amount, which is very high.

As of the end of February 2024, the U.S. debt is almost $34.4 billion. This is the money that the federal government has to borrow to pay for its operating expenses.

The World Bank found that if the debt-to-GDP ratio exceeded 77% for an extended period, it slowed economic growth.

Euro zone inflation eased to 2.6% in February figures showed on Friday 1st March 2024, but both the headline and core figures were higher than expected.

Core inflation

Core inflation, removing the volatile elements of energy, food, alcohol and tobacco was 3.1% above the 2.9% rate expected.

The February figures will be a headache for EU policymakers, as core inflation is still holding above 3% even as the headline rate moves toward the ECB’s 2% target.

India is ‘easily’ the fastest growing economy in the world according to the IMF, as the country’s Q3 GDP growth soared past analysts’ estimates.

The world’s fastest growing major economy expanded 8.4% in the last three months of 2023.

8.4% GDP growth in Q3

At 8.4%, India’s economy expanded at its fastest pace in six quarters, data showed late Thursday, on strong private consumption and upbeat manufacturing and construction activity. Reuters estimates had pegged growth in the October to December period at 6.6%.

Prime Minister Narendra Modi posted on the social media platform X, that it shows ‘the strength of Indian economy and its potential.’

India economy due to jump ahead of Japan and Germany

India is forecast to leap ahead of Japan and Germany as the world’s third biggest economy in the next few years.

The better-than-expected growth was led by a strong performance by the country’s manufacturers, with the sector expanding by 11.6% in the period.

Private consumption, which makes up almost two-thirds of the country’s gross domestic product (GDP), also rose by 3.5%.

That’s the fear spreading through Wall Street as another inflation reading on Friday 16th February 2024 came in hotter-than-expected.

The producer price index rose 0.3% in January 2024. The largest increase since August 2024 and higher than the 0.1% forecast. Excluding food and energy, core PPI jumped 0.5%, again well above consensus.

Stubborn

It is yet another sign of stubborn price pressures across the broader U.S. economy. And it came just days after an unexpectedly hot CPI reading, which gave markets a nasty jolt.

Both data have stoked investor worries on whether inflation is firmly under control. The latest developments also reinforce the Fed’s caution that it will need to see more evidence of disinflation before committing to lower rates.

Mohamed El-Erian, Allianz chief economic advisor, posted on X that like the CPI data, the PPI report was a further indication that the last mile of the inflation battle is more complex than many had assumed (and still assume).

Some economists even argue the jump in Friday’s data will likely push January’s personal consumption expenditures price index, the Fed’s preferred inflation gauge.

The PPI data means we can finalise our core PCE forecast for January, at 0.32%. That would be the biggest increase since September. But the three months since then all saw much smaller gains.

But investors will have to wait until later this month for PCE data when it’s released on 29th February 2024.

The UK’s inflation rate remained at 4% in January 2024, despite the first monthly fall in food prices in two years, ONS figures show.

January U.K. inflation held steady at 4% year-on-year benefitting from easing prices for furniture and household goods, food and non-alcoholic beverages.

According to the latest figures from the Office for National Statistics (ONS), prices for food and non-alcoholic beverages fell on a monthly basis by 0.4%, marking the first decrease since September 2021.

The core CPI figure excluding volatile food, energy, alcohol and tobacco prices annual reading was 5.1%, below the 5.2% estimate – but only a micro 0.1% difference.

The latest inflation data is a reflection of what is happening in the labour market: a tight labour supply is sustaining high wage growth and thus underlying inflationary pressure.

After a decade-long bull run throughout the 1980’s, the Nikkei 225 index reached an all-time high of 38,915 on December 29, 1989, the last trading day of the year.

Few could have imagined, on New Year’s Eve of 1989, that the index would be lower 34 years later. As the New Year arrived, the bubble burst.

And now, Japan’s stock markets are on a tear and closing in on that elusive 38195 high of 1989 – but there’s a catch – the Zombies are coming.

Zombie companies

Zombie firms are businesses that are unprofitable and struggling to keep afloat. They don’t have excess capital to invest and grow the business, or to pay down the loan capital.

Concerns about zombie firms are coming into focus as the Bank of Japan is tipped to raise interest rates in 2024 for the first time since 2007.

It comes as the Nikkei 225 rises to its highest point in almost 34 years

Japan’s stock markets have been on a meteoric run since the start of 2023, repeatedly breaching 33-year highs and outperforming the rest of Asia.

However, there are rising concerns that so called ‘zombie’ firms, which are unprofitable and struggling to keep afloat, could cut short that rally. The Bank of Japan is widely expected to raise interest rates this year, and that could easily tip many of these firms into bankruptcy, which could have a broader impact on the economy and stock market,

Nikkei 225 1-year chart 9th February 2024

Nikkei 225 1-year chart 9th February 2024

Bankrupt businesses

Zombie firms are nothing new in Japan. They first emerged after the stock ‘bubble’ and subsequent crash of the 1990s, when banks continued to support companies that would have otherwise gone bankrupt.

The pandemic of 2020 accelerated the problem of zombie businesses, with the number of zombie firms in Japan reportedly jumping by around 33% between 2021 and 2022.

At the end of 2023, Japan reportedly had around 250,000 companies that are technically zombie businesses

Some experts argue that zombie firms are a drag on Japan’s productivity, innovation, and growth, as they occupy resources and crowd out more efficient firms. The debate on how to deal with zombie firms is ongoing and may have implications for Japan’s economic recovery and future prospects.

Others suggest that zombie firms may have a positive effect, such as preserving employment, social stability, and industrial diversity.

Surely, there is no room for inefficiently run businesses making little or no profit in any economy.

Job creation in the U.S. surged in January 2024, as the economy continued to defy predictions of a slowdown

The U.S. economy added 353,000 jobs and average hourly pay jumped, while the unemployment rate held steady at 3.7%, the Labour Department said.

The report extended more job gains that has surprised economists, who have expected a jump in interest rates since 2022 to slow the economy. It hasn’t. No recession or slowdown in the economy so far.

Early rate cut less likely according to these figures

Average hourly earnings increased 0.6%. Year-on-year basis, wages jumped 4.5%, above the 4.1% forecast.

Non-farm payrolls expanded by 353,000 for the month, well above the 185,000 estimate. The unemployment rate held at 3.7%.

Job growth was widespread in January 2024. Professional and business services 74,000. Other sectors included health care 70,000 and retail trade 45,000.

Analysts now say the job market gain and strength make an early interest rate cut less likely.

The U.S. employment data delivered quite a shock, easily beating expectations, with earnings much higher than expected. Stock markets gained and are at elevated levels for the Dow, Nasdaq and the S&P 500. Record highs have been set – are the highs?

Market analysts said these numbers show the U.S. economy is strong and will change the mindsets of those expecting an early interest rate cut.

Expectations of a recession are off the table too, for now.