Central banks are selling gold now for one blunt reason: they need cash, and gold is the most liquid, pain‑free asset they can dump without triggering a credibility crisis.

The news wires report— “liquidity pressures”, “emerging‑market currency volatility”, “increased spending requirements” — but the underlying mechanics are more structural and revealing – they need the cash!

Central banks have swung from record gold accumulation to noticeable selling because the global system has shifted from long‑term hedging to short‑term survival.

The war in the Gulf has tightened liquidity, pushed up government spending, and destabilised emerging‑market currencies, forcing policymakers to turn their most liquid reserve into cash.

Gold is the one asset they can sell quickly without signalling panic, and that is shaping behaviour across dozens of reserve banks.

War, liquidity and the need for dollars

The Hormuz conflict has driven up energy costs, disrupted shipping and forced governments to spend more on defence and subsidies.

Emerging‑market central banks, already under pressure from currency volatility, need hard currency to intervene in FX markets and stabilise their economies. Selling gold provides instant access to dollars without dumping sovereign bonds or burning through already‑thin reserves.

A falling gold price creates a window

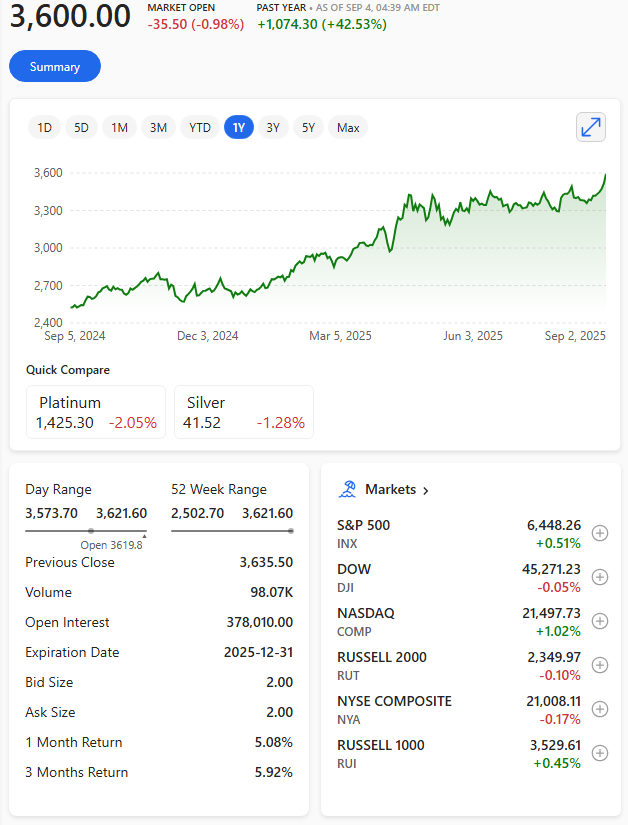

Gold has slipped around 12% from its January 2026 peak, entering a contraction phase despite geopolitical risk. For reserve managers, that is a cue to realise gains from the 2022–25 buying spree while prices remain historically high.

Selling now avoids being forced to sell later at distressed levels if the conflict deepens or fiscal pressures worsen. It will be bought back again at a later time.

The buffer they built is now being used

The record buying of recent years was driven by fears of sanctions, inflation and geopolitical fragmentation.

Those purchases created a cushion that can now be drawn down. The shift to selling does not signal a loss of faith in gold; it reflects the reality that reserves accumulated for stability are now being used to fund stability.

The deeper story is not about gold at all, but about a global system under strain: governments facing rising costs, currencies under pressure, and central banks forced to prioritise liquidity over long‑term positioning.

This is why central banks hold gold.