The recent rebound in technology shares, led by Google’s surge in artificial intelligence optimism, offered a welcome lift to investors weary of recent market sluggishness.

Yet beneath the headlines lies a more troubling dynamic: the increasing reliance on a handful of mega‑capitalisation firms to sustain broader equity gains.

Breadth

Markets thrive on breadth. A healthy rally is one in which gains are distributed across sectors, signalling confidence in the wider economy. When only one or two companies shoulder the weight of investor sentiment, the picture becomes distorted.

Google’s AI announcements may well justify enthusiasm, but the fact that its performance alone can swing indices highlights a fragility in the current market structure.

This concentration risk is not new. In recent years, the so‑called ‘Magnificent Seven‘ technology giants have dominated returns, masking weakness in smaller firms and traditional industries.

While investors cheer the headline numbers, the underlying reality is that many sectors remain subdued. Manufacturing, retail, and even parts of the financial industry are not sharing equally in the rally.

Over Dependence

Over‑dependence on highflyers creates two problems. First, it exposes markets to sudden shocks: if sentiment turns against one of these giants, indices can tumble disproportionately.

Second, it discourages capital from flowing into diverse opportunities, stifling innovation outside the tech elite.

For long‑term stability, investors and policymakers alike should be wary of celebrating narrow gains. A resilient market requires participation from a broad base of companies, not just the fortunes of a few.

Google’s success in AI is impressive, but true economic strength will only be evident when growth spreads beyond the marquee names.

Until then, the market remains vulnerable, propped up by giants whose shoulders, however broad, cannot carry the entire economy indefinitely.

Google has introduced Gemini 3, its most advanced AI model to date, delivering stronger reasoning across text, images, audio, and video.

Announced on 18th November 2025, it shipped simultaneously across Search, the Gemini app, AI Studio, Vertex AI, and developer tools, reflecting a tightly coordinated release and broad immediate availability.

Google emphasises reduced prompt‑dependence and improved accuracy, with early benchmarks and analyst reactions highlighting competitive gains versus recent frontier models.

The rollout arrives roughly eight months after Gemini 2.5, underscoring the rapid rise of Google’s AI development.

Alongside the model, Google unveiled Antigravity, an agent‑first coding environment that enables task‑level planning and execution within familiar IDE workflows.

Antigravity integrates Gemini 3 Pro and supports agentic development across end‑to‑end software tasks, with early coverage generation strong productivity features and immediate developer interest.

Nano Banana Pro

Google’s image stack also advanced with Nano Banana Pro (Gemini 3 Pro Image), reportedly improving text rendering, edit consistency, and high‑resolution output up to 4K.

The launch coincided with a notable Alphabet share price lift, signalling market confidence in Google’s AI strategy.

Google’s Gemini 3 sent Alphabet’s share price sharply higher, closing at $318.47, up 6.3% from the previous day.

The surge reflected investor enthusiasm for the model’s multimodal capabilities and enterprise integration, with analysts noting it as a decisive achievement in the AI race.

AI effect

The rally spilled over into other AI‑linked stocks: Nvidia rose 2.1% to $182.55 on strong GPU demand, while IBM gained 2.2% to $304.12 after highlighting quantum computing progress.

In contrast, Microsoft edged up only 0.4% to $474.00, as analysts flagged concerns about capital intensity in its AI investments.

Overall, the Gemini 3 announcement revived momentum across the AI market sector, with Alphabet leading the charge and peers benefiting from renewed confidence in AI’s commercial potential.

The Arctic is rapidly becoming the new frontier in the global scramble for critical minerals, with nations vying for influence and resources that could shape the future of energy and technology.

The Arctic, long viewed as a remote and inhospitable region, is now at the centre of a geopolitical and economic contest.

As the world accelerates its transition away from fossil fuels, these resources are increasingly seen as strategic assets.

Countries including the United States, Canada, Russia, and Greenland are intensifying exploration and investment. Greenland, in particular, has emerged as a focal point, with experts noting its abundance of rare earths and uranium.

Canada’s northern territories are also being positioned as key suppliers, with government-backed initiatives to strengthen supply chains and reduce reliance on Chinese dominance in the sector.

Control

The race is not solely about economics. Control of Arctic resources carries profound geopolitical weight. As melting ice opens new shipping routes and makes extraction more feasible, competition is sharpening.

Russia has already expanded its Arctic infrastructure, while Western nations are seeking partnerships and technological innovations to ensure sustainable development.

The Oxford Institute for Energy Studies has highlighted that the Arctic could become a significant contributor to the global energy transition, though environmental risks remain a pressing concern.

Fragile

Critics warn that the pursuit of minerals in such fragile ecosystems could have devastating consequences. Mining operations threaten biodiversity, indigenous communities, and the delicate balance of Arctic environments.

Balancing economic opportunity with ecological responsibility will be one of the defining challenges of this new ‘cold gold rush’.

Ultimately, the Arctic’s mineral wealth represents both promise and peril. If managed responsibly, it could underpin the technologies needed to combat climate change and secure energy independence.

If exploited recklessly, it risks becoming another chapter in humanity’s history of resource-driven conflict and environmental degradation.

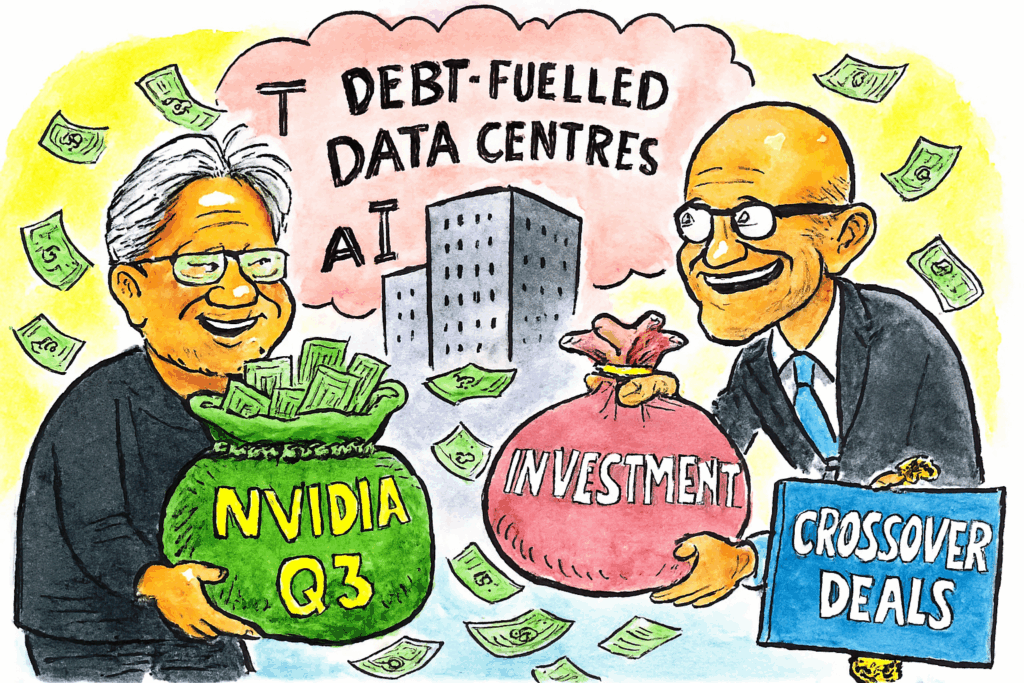

Nvidia’s Q3 results show strength, but the real risk of an AI bubble may lie in the debt-fuelled data centre boom and the circular crossover deals between tech giants.

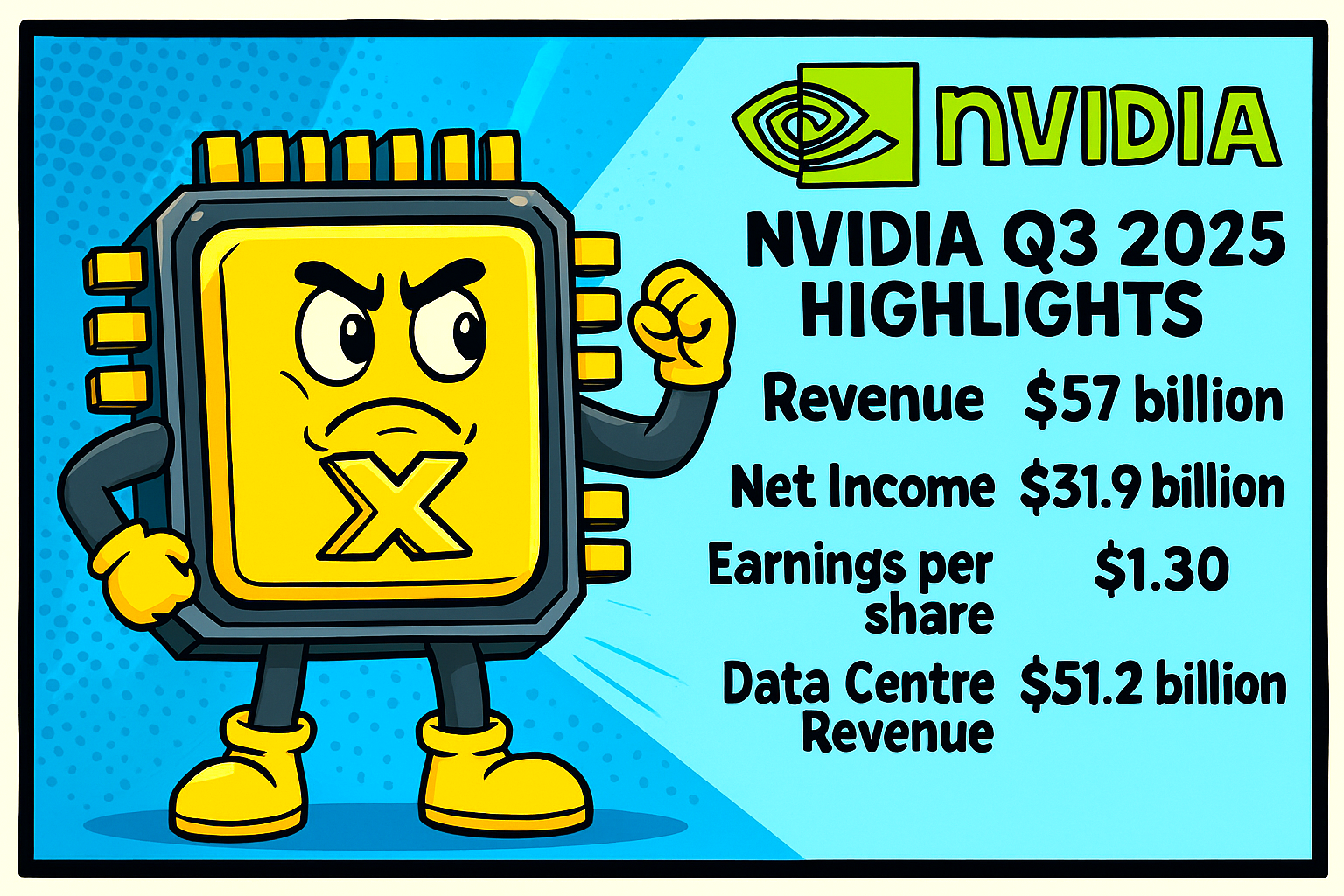

Nvidia’s latest quarterly earnings were nothing short of spectacular. Revenue surged to $57 billion, up 62% year-on-year, with net income climbing to nearly $32 billion. The company’s data centre division alone contributed $51.2 billion, underscoring how central AI infrastructure has become to its growth.

These figures have reassured investors that Nvidia itself is not the weak link in the AI story. Yet, the question remains: if not Nvidia, where might the bubble be forming?

Data centre roll-out

The answer may lie in the debt-driven expansion of AI data centres. Building hyperscale facilities requires enormous capital outlays, not only for GPUs but also for power, cooling, and connectivity.

Many operators are financing this expansion through debt, betting that demand for AI services will continue to accelerate. While Nvidia’s chips are sold out and cloud providers are racing to secure supply, the sustainability of this debt-fuelled growth is less certain.

If AI adoption slows or monetisation lags, these projects could become overextended, leaving balance sheets strained.

Crossover deals

Another area of concern is the crossover deals between major technology companies. Nvidia’s Q3 was buoyed by agreements with Intel, OpenAI, Google Cloud, Microsoft, Meta, Oracle, and xAI.

These arrangements exemplify a circular investment pattern: companies simultaneously act as customers, suppliers, and investors in each other’s AI ventures.

While such deals create momentum and headline growth, they risk masking the true underlying demand.

If much of the revenue is generated by companies trading capacity and investment back and forth, the market could be inflating itself rather than reflecting genuine end-user adoption.

Bubble or not to bubble?

This dynamic is reminiscent of past bubbles, where infrastructure spending raced ahead of proven returns. The dot-com era saw fibre optic networks built faster than internet businesses could monetise them.

Today, AI data centres may be expanding faster than practical applications can justify. Nvidia’s results prove that demand for compute is real and immediate, but the broader ecosystem may be vulnerable if debt levels rise and crossover deals obscure the true picture of profitability.

In short, Nvidia’s strength does not eliminate bubble risk—it merely shifts the spotlight elsewhere. Investors and policymakers should scrutinise the sustainability of AI infrastructure financing and the circular nature of tech partnerships.

The AI revolution is undoubtedly transformative, but its foundations must rest on genuine demand rather than speculative debt and self-reinforcing deals.

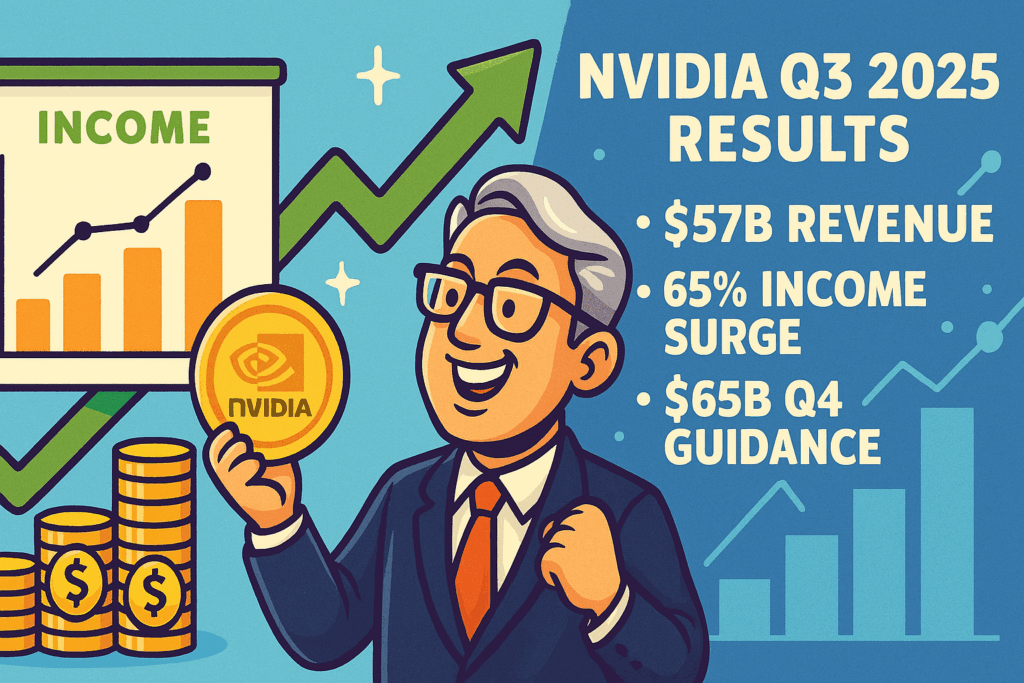

Nvidia has once again (unsurprisingly) defied expectations, reporting record-breaking third-quarter results that underscore its dominance in the artificial intelligence chip market.

Net income surged to $31.9 billion, a remarkable 65% rise compared with last year. Earnings per share came in at $1.30, comfortably ahead of analyst forecasts of $1.26.

The company’s data centre division was the star performer, generating $51.2 billion in revenue, up 25% from the previous quarter and 66% year-on-year.

This reflects the insatiable demand for Nvidia’s Blackwell AI chips, which CEO Jensen Huang reportedly described it as ‘off the charts‘ with cloud GPUs effectively sold out.

Market Impact and Outlook

Shares of Nvidia rose sharply following the announcement, adding to a 39% gain in 2025 so far. Analysts had anticipated strong results, but the scale of growth exceeded even bullish expectations.

Options markets had priced in a potential 7% swing in Nvidia’s stock after earnings, highlighting investor sensitivity to its performance.

Looking ahead, Nvidia has issued guidance of $65 billion in revenue for the fourth quarter, signalling continued momentum.

Huang reportedly emphasised that AI demand is compounding across both training and inference, creating what he called a ‘virtuous cycle’ for the industry.

Strategic Significance

Nvidia’s results reinforce its position at the centre of the global AI boom. Its chips power everything from large language models to robotics, and the company is benefiting from widespread adoption across industries.

With margins above 73%, Nvidia is not only growing rapidly but also maintaining enviable profitability.

The figures highlight how Nvidia has become more than a semiconductor company—it is now a cornerstone of the digital economy.

As AI applications proliferate, Nvidia’s ability to scale production and meet demand will be critical in shaping the next phase of technological transformation.

In short: Nvidia’s Q3 results show explosive growth, record revenues, and a confident outlook, cementing its role as the leading force in AI hardware.

Nvidia CEO reportedly remarked…

‘There’s been a lot of talk about an AI bubble‘, Nvidia CEO Jensen Huang reportedly told investors. ‘From our vantage point, we see something very different’.

As to what that means exactly is up to you to decipher. Regardless of what the AI industry has to offer in the future, from an investor’s point of view, Nvidia’s earnings are clearly something to celebrate.

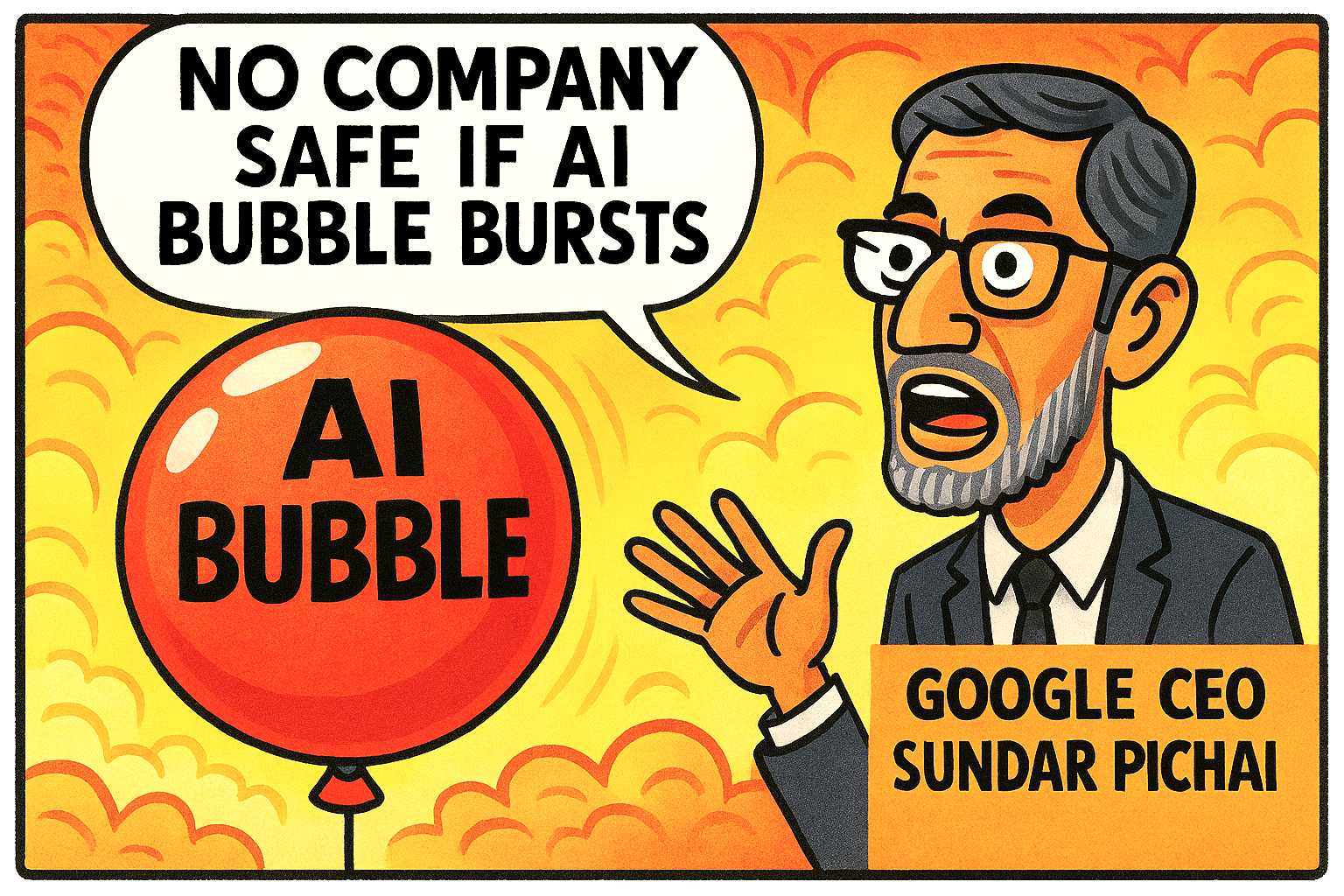

Google CEO Sundar Pichai has warned that no company, including his own, will be immune if the current AI bubble bursts.

He described the boom as both extraordinary and irrational, urging caution amid soaring valuations and investment hype

In a recent interview, Google’s chief executive Sundar Pichai offered a sobering perspective on the rapid expansion of artificial intelligence.

Profound Tech Creation

While he reportedly reaffirmed his belief that AI is ‘the most profound technology humanity has developed‘, he acknowledged growing concerns that the sector may be overheating.

According to Pichai, the surge in investment and valuations has created an atmosphere of exuberance that risks tipping into irrationality.

Pichai stressed that if the so-called AI bubble were to collapse, no company would escape unscathed. Even Google, one of the world’s most powerful technology firms, would feel the impact.

Remember Dot-Com?

He likened the current moment to past speculative cycles, such as the dot-com boom, where innovation was genuine, but market expectations outpaced reality.

Despite these warnings, Pichai emphasised that the long-term potential of AI remains intact.

He argued that professions across the board—from teaching to medicine—will continue to exist, but success will depend on how well individuals adapt to using AI tools.

In his view, the technology will reshape industries, but the hype surrounding short-term gains could distort investment flows and create instability.

His comments arrive at a time when Silicon Valley is grappling with questions about sustainability. Tech stocks have surged on AI optimism, yet analysts caution that inflated valuations may not reflect the true pace of adoption.

Pichai’s intervention serves as both a reality check and a reminder: AI is transformative, but it is not immune to market corrections.

For investors and innovators alike, the message is clear—embrace AI’s promise but prepare for turbulence if the bubble bursts.

Bitcoin has officially entered a bear market, having fallen more than 25% from its October peak of $126,000.

This downturn is rippling across the wider crypto sector, dragging Ethereum, Solana, and other altcoins into steep declines as investor sentiment turns risk-off.

Bitcoin’s recent plunge below $95,000 marks a decisive shift into bear market territory. After reaching an all-time high of $126,000 in early October, the cryptocurrency has shed over a quarter of its value in just six weeks.

Analysts point to a combination of factors: fading hopes of Federal Reserve rate cuts, heavy outflows from Bitcoin ETFs, and broader weakness in technology. The sell-off has erased all of Bitcoin’s 2025 gains, leaving traders cautious and fearful.

This downturn is not isolated. Ethereum has dropped more than 30% from its highs, while Solana and Cardano have suffered double-digit losses.

The total crypto market capitalisation has fallen by approximately $1 trillion since October, underscoring how tightly correlated altcoins remain to Bitcoin’s trajectory.

When the flagship asset falters, liquidity drains across the sector, amplifying volatility.

Investor psychology has shifted dramatically. The ‘buy the dip’ mentality that defined earlier rallies is giving way to defensive strategies, with many now selling into strength rather than accumulating.

Long-term holders have reportedly offloaded hundreds of thousands of BTC in recent weeks, intensifying downward momentum. Meanwhile, ETF outflows — exceeding $1.6 billion in just three days — highlight waning institutional confidence.

For the broader crypto ecosystem, Bitcoin’s bear market signals a period of consolidation and caution. Altcoins, often more volatile, are likely to experience sharper swings.

Yet history suggests that such downturns can reset valuations, paving the way for healthier growth once macroeconomic conditions stabilise.

For now, however, the market remains firmly in risk-off mode, with Bitcoin leading the retreat.

The crypto sector faces nearing a $1 trillion wipeout, with investor sentiment shifting from optimism to fear.

For some time now, talk of an ‘AI bubble‘ has largely come from investors and financial analysts. Now, strikingly, some of the loudest warnings are coming from inside the industry itself.

At the Web Summit in Lisbon, senior executives from companies such as DeepL and Picsart reportedly admitted they were uneasy about the soaring valuations attached to artificial intelligence ventures. Sam Altman of OpenAI has also sounded warnings of AI overvaluation.

DeepL’s chief executive Jarek Kutylowski reportedly described current market conditions as ‘pretty exaggerated’ and suggested that signs of a bubble are already visible.

Picsart’s Hovhannes Avoyan reportedly echoed the sentiment, criticising the way start‑ups are being valued despite having little or no revenue. He reportedly coined the phrase ‘vibe revenue’ to describe firms being backed on hype rather than substance.

These remarks highlight a paradox. On one hand, demand for AI services remains strong, with enterprises expected to increase adoption in 2026.

On the other, the financial side of the sector looks overheated. Investors such as Michael Burry have accused major cloud providers of overstating profits, while banks including Goldman Sachs and Morgan Stanley have warned of potential corrections.

The tension reflects a broader question: can the industry sustain its rapid expansion without a painful reset?

Venture capital forecasts suggest trillions will be poured into AI data centres over the next five years, yet some insiders argue that the scale of spending is unnecessary.

Even optimists concede that businesses are struggling to integrate AI effectively, meaning the promised returns may take longer to materialise.

For now, the AI sector stands at a crossroads. The technology’s transformative potential is undeniable, but the financial exuberance surrounding it may prove unsustainable.

If the warnings from within the industry are correct, the next chapter of the AI story could be less about innovation and more about value correction.

Private equity is increasingly burdened by ‘zombie companies‘ – firms that neither grow nor collapse, but linger in portfolios, draining resources and blocking exits.

In recent years, private equity has faced a troubling phenomenon: the rise of the zombie company.

These are businesses that generate just enough cash to service their debt but fail to deliver meaningful growth or attract buyers, even at discounted valuations.

They remain trapped on balance sheets long after the intended investment horizon, creating a drag on both investors and the wider economy.

The roots of this problem lie in shifting market conditions. Rising interest rates have made debt-heavy buyouts harder to sustain, while a slowdown in dealmaking has reduced opportunities for profitable exits.

Offloading?

In the past, firms could rely on buoyant markets to offload underperforming assets, but today’s cautious buyers are unwilling to take on companies with weak fundamentals.

As noted by a financial educationalist, Oliver GOTTSCHALG – ‘the machine is stuck’ – private equity firms cannot recycle capital efficiently.

For investors, the implications are stark. Capital is locked in funds that cannot distribute returns, potentially undermining confidence in the asset class.

Some firms have resorted to continuation vehicles or fee-generating strategies to keep operations afloat, but these are stopgaps rather than solutions.

The longer companies remain in this half-alive state, the more they consume scarce managerial attention and financial resources.

The persistence of zombie companies also raises broader concerns. They tie up capital that could otherwise support innovation and growth, while their stagnation risks eroding trust in private equity’s promise of dynamic value creation.

Unless market conditions improve or restructuring strategies succeed, the industry may face a decade defined not by bold exits, but by portfolios haunted by the undead.

In short, zombie companies symbolise private equity’s struggle to adapt, neither thriving nor dying but stubbornly refusing to leave

Zombie companies in private equity trap capital, reducing liquidity and investor confidence, which indirectly pressures public markets—especially high‑valuation sectors like AI.

When private equity funds are clogged with underperforming assets, institutional investors face tighter cash flows and may rebalance away from riskier equities.

This creates capital shortages and amplifies volatility in growth stocks. AI firms, already under scrutiny for sky‑high valuations, are particularly vulnerable: investors pull back when liquidity is constrained, leading to sharper corrections.

Recent sell‑offs saw AI stocks lose over $820 billion in value as confidence faltered, reflecting how private equity stagnation can ripple into tech markets.

The Office for National Statistics confirmed that GDP expanded by a mere 0.1% between July and September 2025, down from 0.3% in the previous quarter and below economists’ low expectations of 0.2%.

This ‘painstakingly low and feeble growth’ reflects weak consumer demand, faltering production, and persistent inflationary pressures.

For Chancellor Rachel Reeves, who will deliver her Budget on 26th November 2025, the numbers present a difficult backdrop. With unemployment edging higher and household finances under strain, calls for fiscal support are intensifying.

Yet speculation continues that Reeves will likely opt for tax rises to shore up public finances, a move that risks dampening already fragile growth.

The Bank of England may provide some relief if it cuts interest rates at its final meeting of the year, but monetary easing alone cannot offset structural weaknesses.

Business investment remains subdued, and September’s 2% drop in manufacturing output highlights the challenges facing industry. The JLR debacle didn’t help.

The Budget will therefore be a balancing act: stimulating growth without undermining fiscal credibility.

Today’s figures underline the urgency of that task.

Note:

Rachel Reeves’ 2024 Autumn Budget aimed to lay the groundwork for long-term growth, but it was not widely seen as a ‘growth budget’.

Many business leaders and analysts criticised it for dampening entrepreneurial momentum.

Reeves framed her first Budget as a reset for economic stability, following Labour’s July 2024 election win.

And here we are one year on from 2024 budget with virtually ZERO growth.

In a move that has stunned financial analysts, corporate governance experts, and the broader public alike, Tesla Inc. has approved a record-breaking $1 trillion (£761 billion) compensation package for its CEO, Elon Musk.

In a landmark decision, Tesla shareholders have approved a staggering $1 trillion (£761 billion) compensation package for CEO Elon Musk, marking the largest executive pay deal in corporate history.

The vote, held at Tesla’s annual meeting in Austin, Texas, reportedly saw over 75% of investors back the plan, reaffirming their confidence in Musk’s leadership and long-term vision.

Share deal

The deal is entirely performance-based, with Musk eligible to receive up to 423 million Tesla shares if the company meets a series of ambitious milestones.

These include producing 20 million vehicles annually, deploying one million robotaxis and humanoid robots, and reaching a market valuation of $8.5 trillion.

Reportedly there is no salary or cash bonus—Musk’s payout depends solely on Tesla’s success.

Supporters argue the package aligns Musk’s incentives with shareholder interests, encouraging innovation and growth.

Critics, however, warn of governance risks and the unprecedented concentration of wealth and power.

Musk, already the world’s richest person, could become the first trillionaire if Tesla achieves its targets.

The vote signals Tesla’s intent to evolve beyond electric vehicles into a broader tech powerhouse, betting on AI, robotics, and autonomy—with Musk at the helm.

Artificial Intelligence: The Hype, The Hangover, and What Comes Next…

For the past two years, artificial intelligence has dominated headlines, boardrooms, and investor portfolios.

From generative models that write poetry to chips that promise to revolutionise data processing, AI has been hailed as the engine of a new industrial age. But as 2025 unfolds, the sheen is beginning to dull.

Beneath the surface of record-breaking valuations and breathless media coverage, a more sobering narrative is taking shape: the AI boom may be running out of steam.

Slowing down

Recent market activity paints a cautionary tale. Despite strong earnings from AI stalwarts like Palantir and AMD, stock prices have faltered a little.

Palantir plunged nearly 8% after a blowout quarter, and even Nvidia—long considered the crown jewel of AI hardware—has seen pullbacks.

Analysts warn that Wall Street’s tunnel vision on AI is creating distortions, with capital flooding into a narrow set of companies while broader market fundamentals weaken.

One major concern is overcapacity in data centres. Billions have been poured into infrastructure to support AI workloads, but growth in consumer-facing applications—particularly chatbots and virtual assistants—appears to be plateauing.

Businesses are also grappling with the reality that integrating AI into operations is far more complex than anticipated. From regulatory hurdles to ethical dilemmas, the promise of seamless automation is proving elusive.

Bubble?

The spectre of an ‘AI bubble‘ looms large. Comparisons to the dot-com crash are no longer whispered—they’re openly debated by investors and tech executives alike.

While AI is undoubtedly transformative, the pace of investment may be outstripping the technology’s current utility. As OpenAI’s CEO Sam Altman noted, ‘When bubbles happen, smart people get overexcited about a kernel of truth’.

That kernel remains potent. AI will continue to reshape industries, but the narrative is shifting from euphoric disruption to measured integration. The mania is not over—but it’s maturing.

Investors, developers, and policymakers must now navigate a more nuanced landscape, where realism replaces hype, and long-term value trumps short-term spectacle.

In short, the AI revolution isn’t collapsing—it’s sobering up. And that may be the best thing for its future.

October 2025 saw a notable upswing in global equity markets, with artificial intelligence (AI) emerging as a key driver of investor enthusiasm.

In the United States, major indices closed the month firmly in the green, buoyed by strong third-quarter earnings and renewed confidence in AI’s transformative potential.

Tech giants such as Nvidia, Amazon, and Palantir posted robust results, reinforcing the narrative that AI is not just hype—it’s reshaping business fundamentals.

Nvidia’s leadership in AI chips and Amazon’s expanding AI-driven logistics were particularly well received, while Palantir’s government contracts underscored AI’s strategic reach.

The Federal Reserve’s decision to cut interest rates by 0.25% added further momentum, making growth stocks more attractive and amplifying the rally in AI-heavy portfolios.

Analysts noted that investor sentiment was bolstered by easing trade tensions and a cooling inflation outlook, but it was AI’s ‘secular tailwind of extreme innovation’ that truly captured market imagination.

While some caution that valuations may be running hot, the October 2025 rally suggests that AI is now central to market dynamics. A pullback is likely soon.

As 2025 draws to a close, investors are watching closely to see whether the optimism translates into durable gains—or signals the start of an AI bubble.

Google’s nuclear pivot aligns with green energy goals—but contrasts sharply with Alaska’s oil expansion, which raises environmental concerns

Google’s move to restart the Duane Arnold nuclear plant in Iowa is part of a broader strategy to power its AI infrastructure with carbon-free energy.

Nuclear fission, while controversial, is considered a low-emissions source and offers round-the-clock reliability—something solar and wind can’t always guarantee.

By locking in a 25-year agreement with NextEra Energy, Google aims to meet its AI demands while staying on track for net-zero emissions by 2030.

Why Nuclear Fits the Green Energy Puzzle

Zero carbon emissions during operation make nuclear a strong contender for clean energy.

High energy density means a small footprint compared to solar or wind farms.

24/7 reliability is crucial for powering AI data centres, which can’t afford downtime.

Google’s plan reportedly includes exploring modular reactors and integrating nuclear into its broader clean energy mix.

However, nuclear isn’t without its critics.

Concerns include

Radioactive waste management and long-term storage.

High upfront costs and long construction timelines.

Public resistance due to safety fears and historical accidents.

Alaska’s Oil Recovery: A Different Direction

In stark contrast, the Trump administration has announced plans to open 82% of Alaska’s National Petroleum Reserve for oil and gas drilling.

This includes parts of the Arctic National Wildlife Refuge, home to polar bears, migratory birds, and Indigenous communities.

The move is framed as a push for energy independence and economic growth, but it’s drawing criticism for its environmental impact:

Habitat disruption for Arctic wildlife and fragile ecosystems.

Reversal of previous protections, sparking legal and activist backlash.

The Bigger Picture

Google’s nuclear strategy represents a tech-led green energy evolution, while Alaska’s oil expansion reflects a traditional fossil fuel revival.

The juxtaposition highlights a growing divide in U.S. energy policy: one path leans into innovation and sustainability, the other doubles down on extraction and short-term gains.

Nuclear power produces virtually no carbon emissions during operation, making it one of the cleanest sources of large-scale, continuous energy—though waste disposal and safety remain key challenges.

But…

Nuclear power is clean in terms of carbon emissions, but its waste remains a long-term challenge—requiring secure containment for thousands of years.

While nuclear energy produces virtually no greenhouse gases during operation, it generates radioactive waste that must be carefully managed.

Here’s how the waste issue fits into the broader energy conversation

What Is Nuclear Waste?

High-level waste: Spent fuel from reactors, highly radioactive and thermally hot. Requires cooling and shielding.

Intermediate and low-level waste: Contaminated materials like tools, clothing, and reactor components. Less dangerous but still regulated.

How Is It Managed?

Short-term: Stored on-site in cooling pools or dry casks.

Long-term: Plans for deep geological repositories—sealed underground vaults designed to isolate waste for 10,000+ years.

UK example: The Low Level Waste Repository in Cumbria is being capped with engineered barriers to prevent environmental leakage.

France: Reprocesses spent fuel to reduce volume and reuse materials, though still produces waste.

Japan: Actively searching for a permanent disposal site, with local politics shaping progress.

Innovations and Controversies

New reactor designs aim to produce less waste or use existing waste as fuel.

Deep Fission’s concept: Building reactors in mile-deep shafts that could be sealed permanently.

Public concern: Waste disposal remains a top reason for nuclear opposition, especially in regions like Taiwan

What about greenhouse gasses emitted building a plant and the operation?

Nuclear power emits very low greenhouse gases during operation, but construction and fuel processing do produce emissions—though still far less than fossil fuels over the plant’s lifetime.Dealing with the waste is the real issue.

Here’s a breakdown of the full lifecycle emissions:

Lifecycle Emissions of Nuclear Power

According to the World Nuclear Association and IEA

Construction phase: Building a nuclear plant involves concrete, steel, and heavy machinery—materials and processes that emit CO₂. This upfront carbon cost is significant but amortised over decades of clean operation.

Fuel cycle: Mining, enriching, and transporting uranium also produce emissions, though modern methods are improving efficiency. Operation phase: Once running, nuclear plants emit virtually no greenhouse gases. They don’t burn fuel, so there’s no CO₂ from combustion. Decommissioning: Dismantling old plants and managing waste adds a small carbon footprint, but it’s minor compared to fossil fuel alternatives.

How Nuclear Compares to Other Energy Sources

Energy Source

Lifecycle CO₂ Emissions (g/kWh)

Coal

820

Natural Gas

490

Solar PV

48

Wind

12

Nuclear

12

Sources: World Nuclear Association

Nuclear’s carbon profile is front-loaded: it costs carbon to build, but pays back in decades of clean power. Compared to fossil fuels, it’s a dramatic improvement.

And unlike solar or wind, it’s not weather-dependent—making it ideal for powering AI data centres that demand constant uptime.

Still, critics argue that the slow build time and high capital cost make nuclear less agile than renewables. Others point out that waste management and public trust remain unresolved.

In a bold move that signals the escalating energy demands of artificial intelligence, Google has announced plans to invest heavily in nuclear power to fuel its data centres.

As AI models grow more complex and compute-intensive, the tech giant is turning to atomic energy as a stable, carbon-free solution to meet its insatiable appetite for electricity.

The shift comes amid mounting scrutiny over the environmental impact of AI. Training large language models and running real-time inference across billions of queries requires vast amounts of energy—often sourced from fossil fuels.

Google’s pivot to nuclear is both a strategic and symbolic gesture: a commitment to sustainability, but also a recognition that the AI era demands a fundamentally different energy paradigm.

SMR’s

At the heart of this initiative is Google’s partnership with advanced nuclear startups exploring small modular reactors (SMRs) and next-generation fission technologies.

Unlike traditional nuclear plants, SMRs are designed to be safer, more scalable, and quicker to deploy—making them ideal for powering decentralised data infrastructure.

Google’s goal is to integrate these reactors directly into its cloud and AI campuses, creating a closed-loop ecosystem where clean energy powers the very machines shaping the future.

Critics, however, warn of the risks. Nuclear waste, regulatory hurdles, and public perception remain significant barriers.

Some environmentalists argue that the urgency of the climate crisis demands faster, more proven solutions like solar and wind. Yet others see nuclear as a necessary complement—especially as AI accelerates demand beyond what renewables alone can supply.

This isn’t Google’s first foray into atomic ambition. In 2022, it backed nuclear fusion research through its DeepMind subsidiary, applying AI to optimise plasma control.

Now, with fission in focus, the company appears determined to lead not just in AI innovation, but in the infrastructure that sustains it.

The implications are profound. If successful, Google’s nuclear strategy could set a precedent for the entire tech industry, reshaping how data is powered in the 21st century.

It also raises deeper questions: Can the tools of the future be truly sustainable? And what does it mean when the intelligence we build begins to reshape the energy systems that built us?

One thing is clear—AI isn’t just changing how we think. It’s changing what we power, and how we power it.

We’re already seeing multiple classic bubble indicators: extreme valuations (Buffett Indicator, Shiller CAPE), record retail participation, AI-driven hype, and surging margin debt—all pointing to elevated risk.

Key Bubble Indicators Already Present

📈 Buffett Indicator (Market Cap to GDP) This ratio is at historically high levels, suggesting stocks are significantly overvalued relative to the economy. Warren Buffett himself has warned investors may be “playing with fire”.

📊 Shiller CAPE Ratio Another respected valuation metric, the cyclically adjusted price-to-earnings ratio, is also elevated—indicating unsustainable earnings multiples and potential for correction.

🧠 AI-driven speculation The rally is heavily concentrated in AI and tech stocks, with some analysts calling it a “toxic calm” before a crash. Search volume for ‘AI bubble‘ is at record highs, and billionaire Paul Tudor Jones has issued warnings.

📉 Retail investor frenzy A record 62% of Americans now own stocks, with $51 trillion at stake. This surge in retail participation is reminiscent of past bubbles, where optimism outpaces caution.

📌 New market highs The Nasdaq, S&P 500, and Dow have hit dozens of new highs in recent months. While bullish on the surface, this pace of gains often precedes sharp reversals.

💸 Margin debt and risk appetite Risk-taking is accelerating, with margin debt climbing and speculative behavior increasing. Analysts note this as a historically bad sign when paired with euphoric sentiment.

What’s Not Yet Peaking (But Worth Watching)

IPO and SPAC volume: While not at 2021 levels, any surge here could signal speculative excess.

Corporate earnings vs. valuations: Some firms still show strong earnings, but the disconnect is widening.

Narrative dominance: AI optimism is strong, but hasn’t fully eclipsed fundamentals—yet.

Cathie Wood, CEO of ARK Invest, has once again stirred debate in financial circles by cautioning that the artificial intelligence (AI) sector may be growing top-heavy.

While she remains bullish on the long-term potential of AI technologies, Wood has signalled concern over the concentration of capital in a handful of dominant players—particularly those driving the S&P 500’s recent surge.

Speaking during a recent investor forum in Saudi Arabia, Wood dismissed fears of an outright AI bubble but acknowledged the risk of valuation corrections as interest rates climb and market exuberance outpaces fundamentals.

Her remarks come as ARK Invest continues to rebalance its portfolio, trimming exposure to overvalued tech giants while increasing stakes in emerging AI innovators such as Baidu and Robinhood.

Wood’s flagship ARK Innovation ETF (ARKK) has rebounded sharply in 2025, up over 87% year-on-year, largely fuelled by AI-related holdings.

Yet she reportedly remains wary of the ‘Mag 7’ effect—where a small cluster of mega-cap stocks like Nvidia, Microsoft, and Alphabet dominate investor attention and index weightings.

Strategy

This concentration, she argues, distorts broader market signals and risks sidelining promising mid-cap disruptors.

In response, ARK has shed positions in AMD and Shopify while doubling down on Baidu, a move that reflects Wood’s belief in underappreciated AI plays beyond Silicon Valley.

Her strategy underscores a broader thesis: that the next wave of AI growth will come from decentralised platforms, edge computing, and global innovators—not just the usual suspects.

While critics remain divided on her timing and tactics, Wood’s portfolio adjustments suggest a nuanced approach—one that embraces AI’s transformative power while resisting the gravitational pull of overhyped valuations.

For investors watching the sector’s evolution, her message is clear: beware the weight of giants.

Microsoft Azure experienced a widespread outage on 29th October, beginning around 16:00 UTC, which affected thousands of users and businesses globally.

The disruption stemmed from issues with Azure Front Door, Microsoft’s content delivery network, and cascaded into failures across Microsoft 365, Xbox, Minecraft, and numerous third-party services reliant on Azure infrastructure.

Major retailers such as Costco and Starbucks, as well as airlines including Alaska and Hawaiian, reported system failures that hindered customer access and internal operations.

Users struggled with authentication, hosting, and server connectivity, with DownDetector logging a surge in complaints from 15:45 GMT onwards.

Microsoft acknowledged the problem on its Azure status page, attributing the outage to a suspected configuration change.

Full service restoration was achieved by about 23:20 UTC, though the timing coincided awkwardly with Microsoft’s Q1 FY26 earnings report, where Azure was reportedly highlighted as its fastest-growing segment.

The incident underscores the critical dependence on cloud infrastructure and raises questions about resilience and contingency planning.

As businesses increasingly migrate to cloud platforms, the ripple effects of such outages become more pronounced, impacting not just productivity, but public trust in digital reliability.

In October 2025, Nvidia’s stock surged past $207 per share, lifting its market capitalisation to $5.06 trillion. Once a niche graphics chip maker, Nvidia now powers the backbone of artificial intelligence worldwide.

CEO Jensen Huang confirmed over $500 billion in chip orders and plans for seven U.S. supercomputers.

This milestone, reached just three months after crossing $4 trillion, places Nvidia ahead of Microsoft and Apple, cementing its dominance in the AI era and redefining the future of computing.

Nvidia one-year chart as of October 2025

Nvidia one-year chart as of October 2025 passes $5 trillion Market Cap

Amazon has reportedly announced its largest corporate restructuring to date, with plans to lay off up to30,000 white-collar employees.

This represents nearly 10% of its global office workforce—as it accelerates its transition toward artificial intelligence and automation-led operations.

The move, confirmed on 28th October 2025, marks a dramatic shift in the tech giant’s internal priorities.

CEO Andy Jassy has framed the layoffs as part of a broader effort to streamline management. The company appears to want to eliminate bureaucratic inefficiencies and reallocate resources toward AI infrastructure.

‘We will need fewer people doing some of the jobs that are being done today, and more people doing other types of jobs’, Jassy is reported as saying.

Affected departments span human resources, logistics, customer service, and Amazon Web Services (AWS). Many roles are deemed redundant due to AI integration.

Heavy investment

The company has been investing heavily in machine learning systems. These are capable of handling tasks ranging from inventory forecasting to customer support. This approach has prompted the reevaluation of traditional staffing models.

While Amazon employs over 1.5 million people globally, the layoffs target its 350,000 corporate staff, signalling a significant recalibration of its white-collar operations.

It was reported that the job cuts were delivered via email, underscoring the impersonal nature of the transition.

The timing of the announcement—just ahead of the holiday season—has raised eyebrows across the industry.

Analysts suggest Amazon is betting on AI to offset seasonal labour demands and long-term cost pressures. However, this risks reputational fallout and internal morale issues.

Structural challenges

Critics argue that the scale of the layoffs reflects deeper structural challenges, including overhiring during the pandemic and a growing reliance on technology to solve human-centred problems.

Others see it as a bellwether for the wider tech sector, where AI is increasingly viewed as both a productivity boon and a disruptive force.

As Amazon reshapes its workforce for an AI-driven future, questions remain about the social and ethical implications of such rapid automation.

For now, the company appears resolute: leaner, faster, and more algorithmically efficient—even if it means leaving tens of thousands behind in the process.

But, AI is also creating job opportunities in other areas.

China’s industrial sector roared back to life in September, posting a 21.6% year-on-year increase in profits— reportedly the sharpest monthly gain in approximately two years.

The rebound offers a glimmer of optimism for the world’s second-largest economy, which has been grappling with sluggish domestic demand and a challenging global trade environment.

According to data released by China’s National Bureau of Statistics, the profit growth was broad-based, reportedly with 30 out of 41 major industrial sectors returning gains.

Key areas

Key contributors included the equipment manufacturing and automotive industries, both of which benefited from policy support and a modest uptick in consumer sentiment.

Analysts reportedly suggest the surge reflects a combination of easing input costs, improved factory output, and a low base effect from the previous year.

However, they caution that the momentum may not be sustainable without deeper structural reforms and stronger domestic consumption.

The September figures follow a 17.2% rise in August, indicating a tentative recovery trend after months of contraction earlier in the year.

Up but down

Still, cumulative profits for the first nine months of 2025 reportedly remain down 9% compared to the same period last year, underscoring the uneven nature of the recovery.

Beijing has recently stepped up efforts to stabilise the economy, including targeted fiscal stimulus and measures to support private enterprise.

Whether these gains can be sustained into the final quarter remains to be seen, but for now, September’s data offers a rare bright spot in an otherwise subdued industrial landscape.

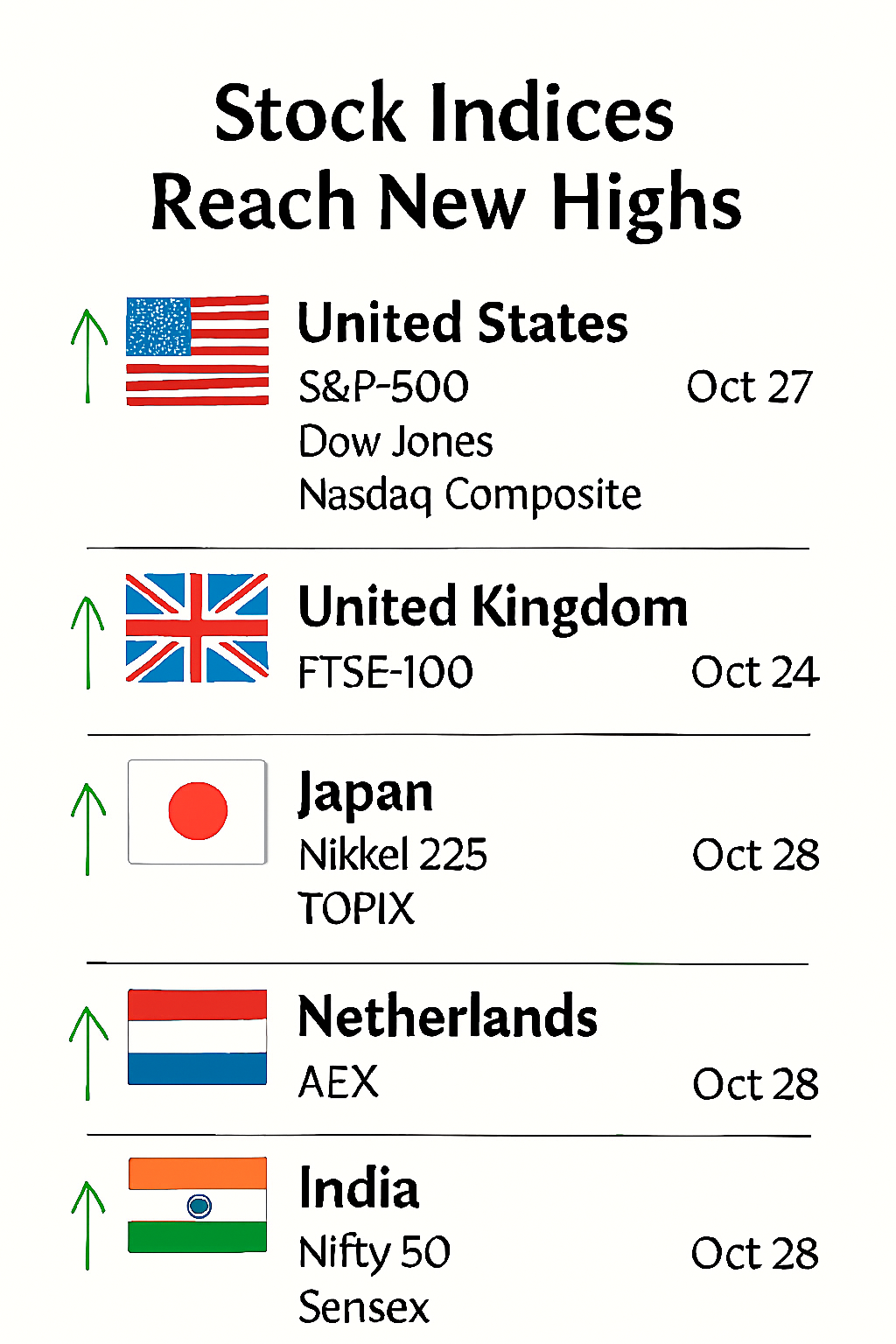

Scaling the Summit:Markets Hit Record Highs Amid Global Uncertainty led by the Nasdaq and S&P 500 reflecting the AI race

Global stock hit new highs October 2025

🌍 Country

📈 Index Name

🗓️ Date

🔝 Closing Value

🇺🇸 United States

S&P 500

Oct 27

6,875.16

🇺🇸 United States

Dow Jones

Oct 27

47,544.59

🇺🇸 United States

Nasdaq Composite

Oct 27

23,637.46

🇬🇧 United Kingdom

FTSE 100

Oct 24

9,662.00

🇳🇱 Netherlands

AEX Index

Oct 28

966.82

🇮🇳 India

Nifty 50

Oct 28

25,966

🇮🇳 India

Sensex

Oct 28

84,778.84

🇯🇵 Japan

Nikkei 225

Oct 28

50,342.25

🇯🇵 Japan

TOPIX

Oct 28

3,285.87

These rallies were largely fueled by optimism over a potential U.S.–China trade deal, cooler inflation data, and expectations of interest rate cuts from the Fed.

The Binance founder had served a four-month sentence after pleading guilty to violating U.S. anti-money laundering laws—a conviction that formed part of a $4.3 billion settlement with the Department of Justice.

CZ’s release marks a dramatic turning point in the U.S. government’s approach to cryptocurrency regulation. Once emblematic of the Biden administration’s crackdown on crypto platforms, CZ now reportedly finds himself at the centre of a political pivot.

Trump’s pardon, announced in October 2025, has been met with both celebration and condemnation. Critics, including Senator Thom Tillis, argue the move undermines efforts to regulate illicit finance, while supporters hail it as a step toward restoring innovation in the digital asset space.

Now based in Abu Dhabi, CZ has vowed to ‘help make America the Capital of Crypto‘. His post-release activities suggest a shift from direct exchange management to broader influence.

Such as, investing in educational initiatives like Giggle Academy, backing blockchain startups, and lobbying for friendlier crypto legislation.

Despite the pardon, expectations remain high. CZ is under intense scrutiny—not just from regulators, but from the crypto community itself.

Many expect him to champion transparency, rebuild Binance’s reputation, and avoid the shadowy practices that led to its U.S. ban in 2019. His future influence may hinge on whether he can balance ambition with accountability.

For now, CZ’s return is symbolic: a signal that the crypto world is once again in flux, with its most controversial figure back in play.

Japan’s benchmark Nikkei 225 index surged past the 50,000 mark for the first time in history, marking a symbolic milestone for Asia’s second-largest economy.

The rally reflects a potent mix of domestic resilience, global investor appetite, and strategic policy shifts that have redefined Japan’s market narrative.

The breakthrough comes amid renewed optimism surrounding U.S.-China trade negotiations, with President Trump signalling progress ahead of a key meeting with Japan’s Sanae Takaichi.

Investors are betting on a thaw in geopolitical tensions, which could unlock export growth for Japan’s tech-heavy industrial base.

Driving the rally are heavyweight stocks in semiconductors, robotics, and AI infrastructure—sectors buoyed by global demand and Japan’s push to become a regional data hub.

Nikkei 225 Index at new history high above 50,000

Companies like Tokyo Electron and SoftBank have seen double-digit gains, fuelled by bullish earnings and strategic pivots toward AI and automation.

Domestically, the Bank of Japan’s continued accommodative stance has kept borrowing costs low, while corporate governance reforms have attracted foreign capital.

The weaker yen has also boosted exporters, making Japanese goods more competitive abroad.

Symbolically, the 50,000 threshold represents more than just market exuberance—it’s a vote of confidence in Japan’s ability to adapt, innovate, and lead in a shifting global landscape.

While risks remain—from demographic headwinds to geopolitical flashpoints—the Nikkei’s ascent signals a new era of investor engagement with Japan’s evolving economic story.

It was just one week ago on Monday 20th October 2025, Amazon Web Services (AWS) experienced a major outage that rippled across the digital world, disrupting operations for millions of users and businesses.

The incident, which originated in AWS’s US-East-1 region, was reportedly traced to DNS resolution failures affecting DynamoDB—one of AWS’s core database services.

This technical fault triggered cascading issues across EC2, network load balancers, and other critical infrastructure, leaving many services offline for hours.

The impact was immediate and widespread. Major consumer platforms such as Snapchat, Reddit, Disney+, Canva, and Ring doorbells went dark.

Financial services including Venmo and Robinhood faltered, while airline customers at United and Delta struggled to access bookings. Even British government portals like Gov.uk and HMRC were affected, underscoring the global reach of AWS’s infrastructure.

World leader

AWS is the world’s leading cloud provider, commanding roughly one-third of the global market—well ahead of Microsoft Azure and Google Cloud.

Millions of companies, from startups to multinational corporations, rely on AWS for everything from data storage and virtual servers to machine learning and content delivery.

Its services underpin critical operations in healthcare, education, retail, logistics, and media. When AWS stumbles, the internet itself feels the tremor.

20 Prominent Companies Affected by the AWS Outage (20th Oct 2025)

Sector

Company Name

Impact Summary

E-commerce

Amazon

Internal systems and Seller Central offline

Social Media

Snapchat

App outages and delays

Streaming

Disney+

Service interruptions

News

Reddit

Partial outages, scaling issues

Design Tools

Canva

High error rates, reduced functionality

Smart Home

Ring

Device connectivity issues

Finance

Venmo

Transaction delays

Finance

Robinhood

Trading disruptions

Airlines

United Airlines

Booking and check-in issues

Airlines

Delta Airlines

Reservation access problems

Telecom

T-Mobile

Indirect service disruptions

Government

Gov.uk

Portal access issues

Government

HMRC

Service delays

Banking

Lloyds Bank

Online banking affected

Productivity

Zoom

Meeting access issues

Productivity

Slack

Messaging delays

Education

Canvas

Assignment submissions disrupted

Crypto

Coinbase

User access failures

Gaming

Roblox

Server outages

Gaming

Fortnite

Gameplay interruptions

This outage wasn’t the result of a cyberattack, but rather a technical fault in one of Amazon’s main data centres. Yet the consequences were no less severe.

Amazon’s own operations were disrupted, with warehouse workers unable to access internal systems and third-party sellers locked out of Seller Central.

Canva reported ‘significantly increased error rates’. while Coinbase and Roblox cited cloud-related failures.

The incident serves as a stark reminder of the risks inherent in centralised cloud infrastructure. As digital life becomes increasingly dependent on a handful of providers, the potential for systemic disruption grows.

A single point of failure can cascade across industries, affecting everything from classroom assignments to emergency services.

AWS has since restored normal operations and promised a detailed post-event summary. But for many, the outage has reignited questions about resilience, redundancy, and the wisdom of placing so much trust in a single cloud giant.

In the age of digital interdependence, even a brief lapse can feel like a global blackout.