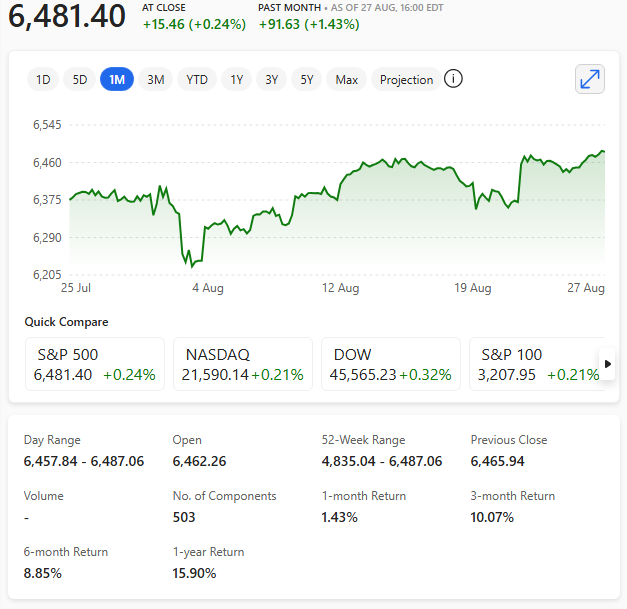

The S&P 500 closed at a fresh all-time high of 6,481.40, on 27th August 2025, marking a milestone driven largely by investor enthusiasm around artificial intelligence and anticipation of Nvidia’s earnings report.

This marks the index’s highest closing level ever, surpassing its previous record from 14th August 2025.

Here’s what powered the rally

🧠 AI Momentum: Nvidia, which now commands over 8% of the S&P 500’s weighting, has become a bellwether for AI-driven growth. Despite closing slightly down ahead of its earnings release, expectations for ‘humongous revenue gains’ kept investor sentiment buoyant.

💻 Tech Surge: Software stocks led the charge, with MongoDB soaring 38% after raising its profit forecast.

🏦 Fed Rate Cut Hopes: Comments from New York Fed President John Williams reportedly hinted at a possible rate cut in September, helping ease bond yields and boost equities.

🔋 Sector Strength: Energy stocks rose 1.15%, leading gains across 8 of the 11 S&P sectors.

S&P 500 at all-time record 27th August 2025

Even with Nvidia’s post-bell dip, the broader market seems to be pricing in sustained AI growth and a more dovish Fed stance.

Nvidia forecasts decelerating growth after a two-year AI Boom. A cautious forecast from the world’s most valuable company raises worries that the current rate of investment in AI systems might not be sustainable.

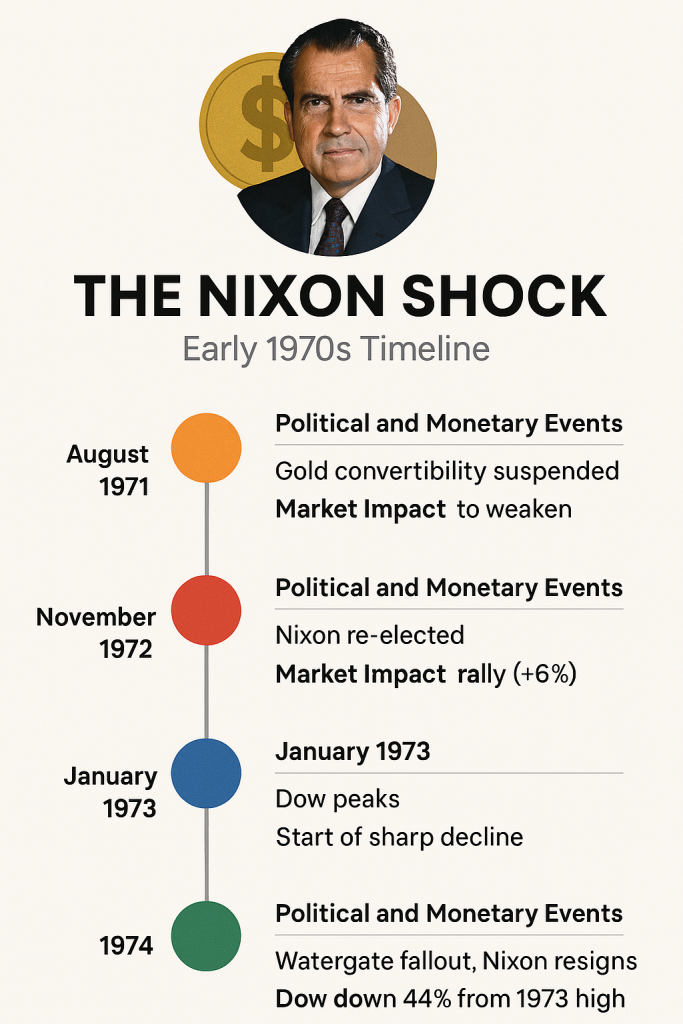

In the early 1970s, President Richard Nixon’s pursuit of re-election collided with the Federal Reserve’s independence, triggering a cascade of economic consequences that reshaped global finance.

The episode remains a cautionary tale about the dangers of politicising monetary policy.

At the heart of the drama was Nixon’s pressure on Fed Chair at the time, Arthur Burns to stimulate the economy ahead of the 1972 election. Oval Office tapes later revealed Nixon’s direct appeals for rate cuts and looser credit conditions—despite rising inflation.

Burns, reluctant but ultimately compliant, oversaw a period of aggressive monetary expansion. Interest rates were held artificially low, and the money supply surged.

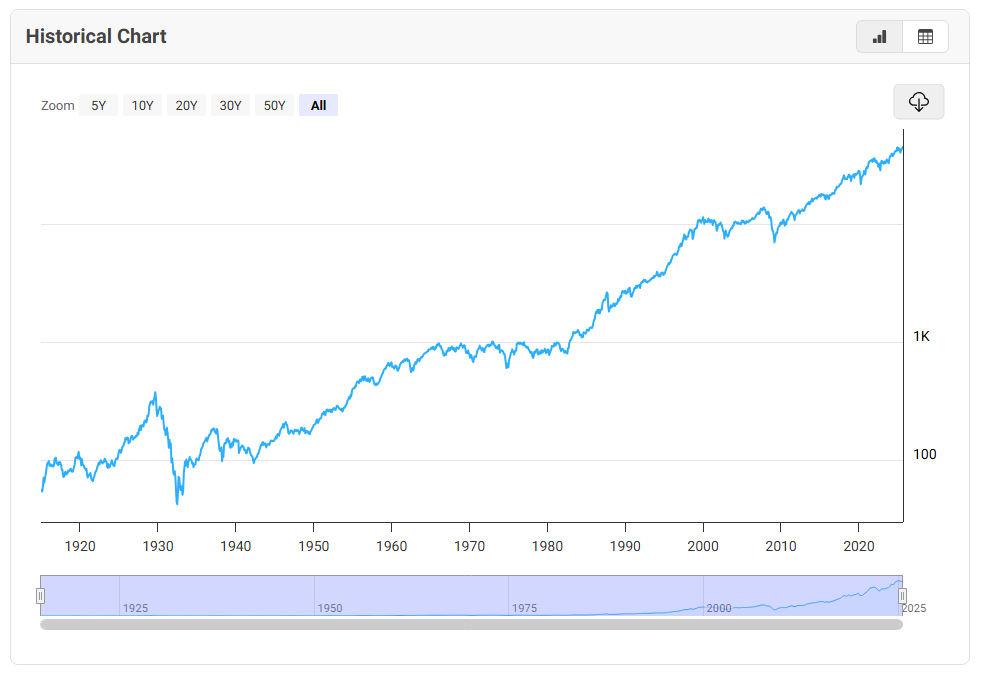

Dow historical chart – lowest 43 points to around 45,400

The short-term result was a booming economy and a landslide victory for Nixon. But the longer-term consequences were severe. Inflation, already simmering, began to boil. By 1973, consumer prices were rising at an annual rate of over 6%, and the dollar was under siege in global markets.

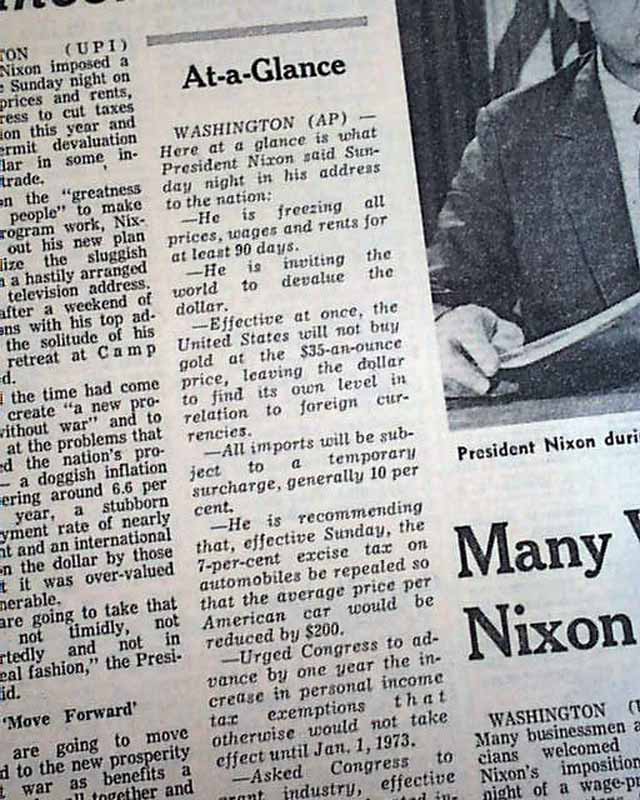

Then came the real shock: in August 1971, Nixon unilaterally suspended the dollar’s convertibility into gold, effectively ending the Bretton Woods system.

This move—intended to halt speculative attacks and preserve U.S. gold reserves—unleashed a new era of floating exchange rates and fiat currency. The dollar depreciated sharply, and global markets entered a period of volatility.

By 1974, the consequences were fully visible. The Dow Jones Industrial Average had fallen nearly 45% from its 1973 peak.

Politics vs the Federal Reserve – lesson learned?

Bond yields soared as investors demanded compensation for inflation risk. The U.S. economy entered a deep recession, compounded by the oil embargo and geopolitical tensions.

The Nixon-Burns episode is now widely viewed as a breach of central bank independence. It demonstrated how short-term political gains can lead to long-term economic instability.

The Fed’s credibility was damaged, and it took nearly a decade—culminating in Paul Volcker’s brutal rate hikes of the early 1980s—to restore price stability.

Today, as debates over Fed autonomy resurface, the lessons of the 1970s remain urgent. Markets thrive on trust, transparency, and institutional integrity. When those are compromised, even the most powerful economies can falter.

THE NIXON SHOCK — Early 1970’s Timeline

🔶 August 1971Event: Gold convertibility suspended Market Impact: Dollar begins to weaken Context: Nixon ends Bretton Woods, launching the fiat currency era

🔴 November 1972Event: Nixon re-elected Market Impact: Stocks rally briefly (+6%) Context: Fed policy remains loose under political pressure

🔵 January 1973Event: Dow peaks Market Impact: Start of sharp decline Context: Inflation accelerates, investor confidence erodes

🟢 1974Event: Watergate fallout, Nixon resigns Market Impact: Dow down 44% from 1973 high Context: Recession deepens, Fed credibility damaged.

Current dollar dive, stocks boom and bust (the Dow fell 19% in a year and then by 44% in 1975 from its January 1973 peak). U.S. 10-year Treasury yields surged (peaking at nearly 7.60% -close to twice today’s yield).

In hindsight, Nixon won the election—but lost the economy. And the Fed, caught in the crossfire, paid the price in credibility. It’s a reminder that monetary policy is no place for political theatre.

Is history repeating itself? Is Trump’s involvement different, or another catastrophe waiting to happen?

A string of recent failings has exposed deep-rooted issues in the agency’s data collection, processing, and publication methods—raising alarm among economists, policymakers, and watchdogs alike.

The most visible setback came in August 2025, when the ONS abruptly delayed its monthly retail sales figures, citing the need for ‘further quality assurance’. This two-week postponement, while seemingly minor, is symptomatic of broader dysfunction.

Retail data is a key indicator of consumer confidence and spending, and its delay undermines timely decision-making across government and financial sectors.

But the problems run deeper. Labour market statistics—once a gold standard—have been plagued by collapsing response rates. The Labour Force Survey, a cornerstone of employment analysis, now garners responses from fewer than 20% of participants, down from 50% a decade ago.

This erosion has left institutions like the Bank of England flying blind on crucial metrics such as wage growth and economic inactivity.

Trade data and producer price indices have also suffered from delays and revisions, prompting the Office for Statistics Regulation (OSR) to demand a full overhaul.

In June, a review led by Sir Robert Devereux identified “deep-seated” structural issues within the ONS, calling for urgent modernisation.

The resignation of ONS chief Ian Diamond in May, citing health reasons, added further instability to an already beleaguered institution.

Critics argue that the failings are not merely technical but systemic. Funding constraints, outdated methodologies, and a culture resistant to reform have all contributed to the malaise.

As Dame Meg Hillier, chair of the Treasury Select Committee, reportedly warned: ‘Wrong decisions made by these institutions can mean constituents defaulting on mortgages or losing their livelihoods’.

Efforts are underway to replace the flawed Labour Force Survey with a new ‘Transformed Labour Market Survey’, but its rollout may not be completed until 2027.

Meanwhile, the ONS is attempting to integrate alternative data sources—such as VAT records and rental prices—to bolster its national accounts. Yet progress remains slow.

In an era where data drives policy, the failings of the ONS are more than bureaucratic hiccups—they are a threat to informed governance.

Without swift and transparent reform, Britain risks making economic decisions based on statistical guesswork.

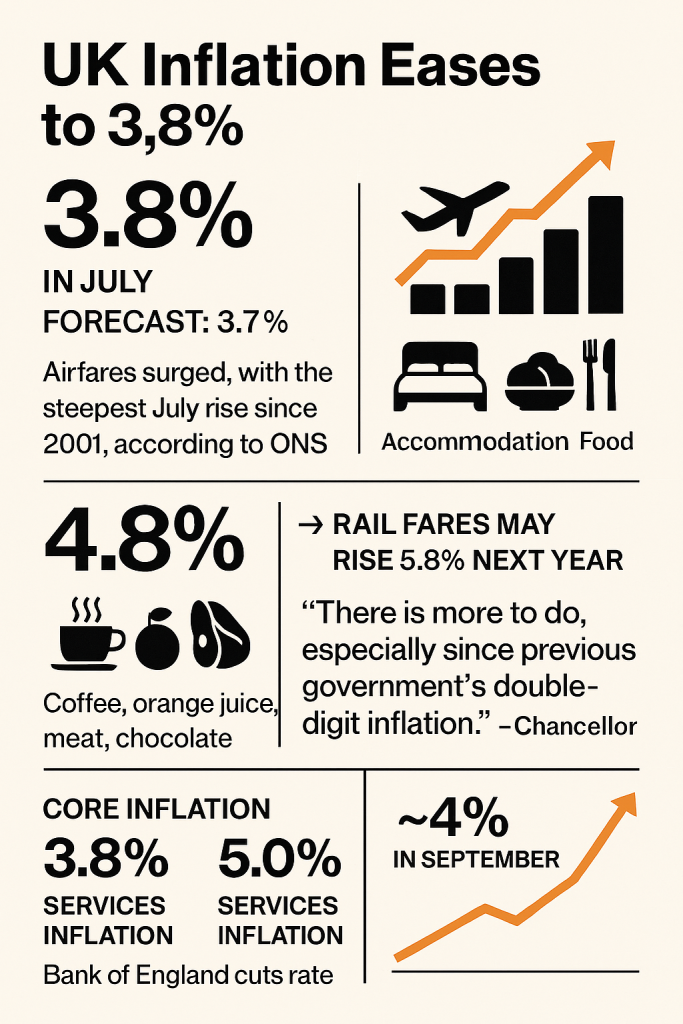

The UK’s annual inflation rate climbed to 3.8% in July, marking its highest level since January 2024 and outpacing economists’ forecasts of 3.7%.

The Office for National Statistics (ONS) attributed the unexpected rise to soaring airfares, elevated accommodation costs, and persistent food price pressures.

Transport costs were the primary driver, with airfares experiencing their steepest July increase since monthly tracking began in 2001.

Analysts suggest the timing of school holidays and a spike in demand—possibly amplified by high-profile events like the Oasis reunion tour—contributed to the surge.

Food inflation also continued its upward trend, with notable increases in coffee, fresh orange juice, meat, and chocolate.

The Retail Prices Index (RPI), which influences rail fare caps, rose to 4.8%, potentially signalling a 5.8% hike in regulated train fares next year.

Core inflation, which excludes volatile items such as energy and food, matched the headline rate at 3.8%, suggesting underlying price pressures remain stubborn.

Services inflation rose to 5%, reinforcing concerns that inflation may be embedding itself more deeply in the economy.

Despite the Bank of England’s recent rate cut to 4%, policymakers face a delicate balancing act. With inflation still nearly double the Bank’s 2% target, further monetary easing may be limited.

UK inflation July 2025 infographic

Chancellor Rachel Reeves acknowledged the challenge, stating that while progress has been made since the previous government’s double-digit inflation, ‘there’s more to do to ease the cost of living’.

Measures such as raising the minimum wage and expanding free school meals aim to cushion households from rising prices.

As inflation edges closer to a projected 4% peak in September 2025, the coming months will test both fiscal and monetary resilience.

Japan’s economy has hit a troubling patch, with July 2025 marking its sharpest export contraction in over four years.

The Ministry of Finance reported a 2.6% year-on-year drop, driven largely by tariff led trade tensions and weakening global demand.

The most dramatic impact came from the United States, where exports fell 10.1%, led by a 28.4% plunge in automobile shipments.

This follows the U.S. administration’s decision to impose 25% tariffs on Japanese vehicles and auto parts in April—a move that has rattled Japan’s automotive sector, long a pillar of its export economy.

Despite a partial tariff rollback to 15% in July, the damage was already done. Japanese carmakers absorbed much of the cost to maintain shipment volumes, which only fell 3.2%, but the value loss was substantial.

Japan – July export data infographic

Exports to China also declined by 3.5%, underscoring broader regional weakness. Meanwhile, imports dropped 7.5%, signalling sluggish domestic consumption and further strain on Japan’s trade balance, which recorded a 117.5 billion yen deficit.

Economists warn that if the export downturn continues, Japan could face a recession. Although Q2 GDP showed modest growth of 0.3%, the July figures suggest that momentum may be fading.

The Bank of Japan is now expected to hold off on interest rate hikes, with its next policy meeting scheduled for 19th September 2025.

As global markets digest the implications, Japan’s export slump serves as a stark reminder of how vulnerable even advanced economies can be to shifting trade policies and geopolitical headwinds.

The UK economy (GDP) grew by 0.3% in the second quarter of 2025, outperforming forecasts of just 0.1% growth (not difficult).

This marks a slowdown from the robust 0.7% expansion seen in Q1, but June’s rebound helped offset weaker activity in April and May 2025.

📊 Key Highlights:

Monthly growth: +0.4% in June, following a slight dip in May.

Sector drivers: Services led the charge, with gains in computer programming, health, vehicle leasing, and scientific R&D. Construction also rose, while production dipped slightly.

Updated data: April’s contraction was revised to show a milder decline than previously estimated.

💬 Expert commentary:

Economists caution that the momentum may not last, citing a softening labour market and inflationary pressures.

The Bank of England recently cut interest rates to 4%, aiming to balance inflation control with economic support.

Chancellor Rachel Reeves welcomed the figures but stressed the need for deeper reform to unlock long-term growth.

Despite the sunny headline, analysts remain wary of headwinds from global weakness, tax changes, and cautious consumer sentiment.

The outlook for Q3 is more muted, with hopes of a sharp rebound likely to be tempered.

In a sweeping rally that spanned continents and sectors, major global indices surged to fresh record highs yesterday, buoyed by cooling inflation data,renewed hopes of U.S. central bank rate cuts, and easing trade tensions.

U.S. inflation figures released 12th August 2025 for July came in at: 2.7% – helping to lift markets to new record highs!

U.S. Consumer Price Index — July 2025

Metric

Value

Monthly CPI (seasonally adjusted)

+0.2%

Annual CPI (headline)

+2.7%

Core CPI (excl. food & energy)

+0.3% monthly, +3.1% annual

Despite concerns over Trump’s sweeping tariffs, the U.S. July 2025 CPI came in slightly below expectations (forecast was 2.8% annual).

Economists noted that while tariffs are beginning to show up in certain categories, their broader inflationary impact remains modest — for now.

Global Indices Surged to Record Highs Amid Rate Cut Optimism and Tariff Relief

Tuesday, 12 August 2025 — Taking Stock

📈 S&P 500: Breaks Above 6,400 for First Time

Closing Level: 6,427.02

Gain: +1.1%

Catalyst: Softer-than-expected U.S. CPI data (+2.7% YoY) boosted bets on a September rate cut, with 94% of traders now expecting easing.

Sector Drivers: Large-cap tech stocks led the charge, with Microsoft, Meta, and Nvidia all contributing to the rally.

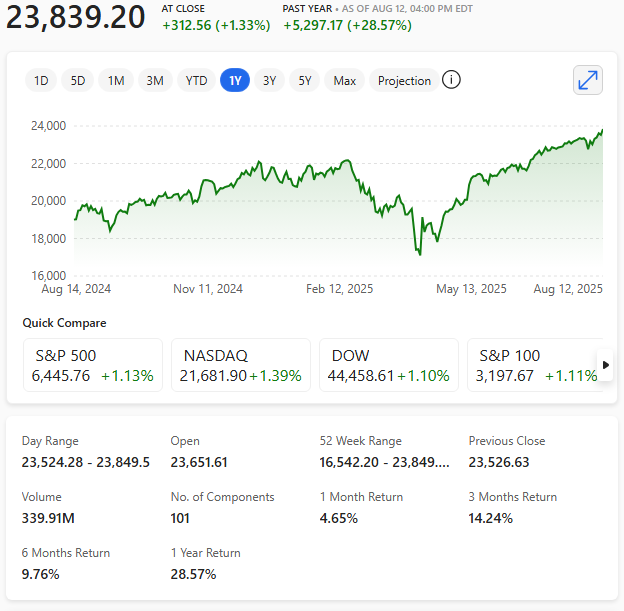

💻 Nasdaq Composite & Nasdaq 100: Tech Titans Lead the Way

Nasdaq Composite: Closed at a record 21,457.48 (+1.55%)

Nasdaq 100: Hit a new intraday high of 23,849.50, closing at 23,839.20 (+1.33%)

Highlights:

Apple surged 4.2% after announcing a $600 billion U.S. investment plan.

AI optimism continues to fuel gains across the Magnificent Seven stocks.

Nasdaq 100 chart 12th August 2025

Nasdaq 100 chart 12th August 2025

🧠 Tech 100 (US Tech Index): Momentum Builds

Latest High: 23,849.50

Weekly Gain: Nearly +3.7%

Outlook: Traders eye a breakout above 24,000, with institutional buying accelerating. Analysts note a 112% surge in net long positions since late June.

🇯🇵 Nikkei 225: Japan Joins the Record Club

Closing Level: 42,718.17 (+2.2%)

Intraday High: 43,309.62

Drivers:

Relief over U.S. tariff revisions and a 90-day pause on Chinese levies.

Strong earnings from chipmakers like Kioxia and Micron.

Speculation of expanded fiscal stimulus following Japan’s recent election results.

🧮 Market Sentiment Snapshot

Index

Record Level Reached

% Gain Yesterday

Key Driver

S&P 500

6,427.02

+1.1%

CPI data, rate cut bets

Nasdaq Comp.

21,457.48

+1.55%

AI optimism, Apple surge

Nasdaq 100

23,849.50

+1.33%

Tech earnings, institutional buying

Tech 100

23,849.50

+1.06%

Momentum, bullish sentiment

Nikkei 225

43,309.62

+2.2%

Tariff relief, chip rally

📊 Editorial Note: While the rally reflects strong investor confidence, analysts caution that several indices are approaching technical overbought levels.

The Nikkei’s RSI, for instance, has breached 75, often a precursor to short-term pullbacks.

On 7th August 2025, the Bank of England’s Monetary Policy Committee voted narrowly—5 to 4—in favour of reducing the base interest rate by 0.25% to 4%, marking its lowest level since March 2023.

This is the fifth rate cut in a year, aimed at stimulating growth amid sluggish GDP and persistent inflation, which currently stands at 3.6%.

Governor Andrew Bailey reportedly described the decision as part of a ‘gradual and careful’ easing strategy, balancing inflation risks with signs of a softening labour market.

While some committee members reportedly advocated for a larger cut, others urged caution, reflecting deep divisions over the UK’s economic trajectory.

The move is expected to ease borrowing costs for homeowners and businesses, with tracker mortgage rates falling immediately. However, savers will be losing out as rates continue to drop.

However, analysts warn that future cuts may hinge on upcoming fiscal decisions and inflation data, leaving the path forward uncertain.

There are increasingly credible signs that U.S. stocks may be heading into a deeper adjustment phase.

Here’s a breakdown of the key indicators and risks that suggest the current stumble could be more than a seasonal wobble. It’s just a hypothesis, but…

S&P 500 clinging to its 200-day moving average: While the long-term trend remains intact, short-term averages (5-day and 20-day) have turned negative.

Volatility Index (VIX) rising: A 7.61% surge in the 20-day average VIX suggests growing unease, even as prices remain elevated.

Diverging ADX readings: The S&P 500’s ADX (trend strength) is weak at 7.57, while the VIX’s ADX is strong at 45.37—classic signs of instability brewing.

🧠 Sentiment & Positioning: Optimism with Defensive Undercurrents

Investor sentiment is bullish (40.3%), but rising put/call ratios and a complacent Fear & Greed Index hint at hidden caution.

Historical parallels: Similar sentiment setups preceded corrections in 2021 and 2009. We’re not at extremes yet, but the complacency is notable.

🌍 Macroeconomic Risks: Tariffs, Fed Policy, and Structural Headwinds

Tariff escalation: Trump’s recent executive order raised effective tariffs to 15–20%, with new duties on rare earths and tech-critical imports.

Labour market weakening: July’s jobs report showed just 73,000 new jobs, with massive downward revisions to prior months. Unemployment ticked up to 4.2%.

Fed indecision: The central bank is split, with no clear path on rate cuts. This uncertainty is amplifying volatility.

Structural drag: Reduced immigration and R&D funding are eroding long-term growth potential.

🛡️ Strategic Implications: How Investors Are Hedging

Defensive sectors like utilities, healthcare, and gold are gaining traction.

VIX futures and Treasury bonds are being used to hedge against volatility.

Emerging markets with trade deals (e.g., Vietnam, Japan) may outperform amid global realignment.

🗓️ Seasonal Weakness: August and September Historically Slump

August is the worst month for the Dow since 1988, and the second worst for the S&P 500 and Nasdaq.

Wolfe Research reportedly notes average declines of 0.3% (August) and 0.7% (September) since 1990.

While the broader market still shows resilience—especially in mega-cap tech—the underlying signals point to fragility.

Elevated valuations, weakening macro data, and geopolitical uncertainty are converging. A deeper correction isn’t guaranteed, but the setup is increasingly asymmetric: limited upside, growing downside risk.

President Donald Trump has announced a sweeping 100% tariff on imported semiconductors and microchips—unless companies are actively manufacturing in the United States.

The move, unveiled during an Oval Office event with Apple CEO Tim Cook, is aimed at turbocharging domestic production in a sector critical to everything from smartphones to defence systems.

Trump’s vow comes on the heels of Apple’s pledge to invest an additional $100 billion in U.S. operations over the next four years.

While the tariff exemption criteria remain vague, Trump emphasised that firms ‘committed to build in the United States’ would be spared the levy.

The announcement adds pressure to global chipmakers like Taiwan Semiconductor (TSMC), Nvidia, and GlobalFoundries, many of which have already initiated U.S. manufacturing projects.

According to the Semiconductor Industry Association, over 130 U.S.-based initiatives totalling $600 billion have been announced since 2020.

Critics warn the tariffs could disrupt global supply chains and raise costs for consumers, while supporters argue it’s a bold step toward tech sovereignty.

With AI, automotive, and defence sectors increasingly reliant on chips, the stakes couldn’t be higher.

Whether this tariff threat becomes a turning point or a trade war flashpoint remains to be seen.

Trump has a habit of unravelling as much as he ‘ravels’ – time will tell with this tariff too.

On 30th July 2025, the Federal Reserve opted to keep its benchmark interest rate unchanged at 4.25%–4.50%, defying mounting pressure from President Trump to initiate cuts.

The decision, reached by a 9–2 vote, marked the first time since 1993 that two governors—Michelle Bowman and Christopher Waller—formally dissented, advocating for a quarter-point reduction.

Fed Chair Jerome Powell cited “moderated” economic growth and “somewhat elevated” inflation as reasons for maintaining the current stance.

Despite a robust Q2 GDP reading of 3%, Powell emphasised the need for caution, particularly amid uncertainty surrounding Trump’s tariff policies.

Markets reacted with disappointment, as hopes for a dovish pivot were dashed. Powell remained non-committal about September’s outlook, reportedly stating, ‘We have made no decisions about September’.

With inflation still above target and political tensions rising, the Fed’s wait-and-see approach underscores its commitment to data-driven policy.

After a lacklustre start to 2025, the U.S. economy posted a surprising comeback in the second quarter, with GDP rising at an annualised rate of 3.0%, according to data released today.

The sharp upswing follows a 0.5% contraction in Q1, catching analysts off-guard and fuelling speculation about the durability of the recovery.

📈 A Rebound Built on Consumers and Imports

At the heart of the turnaround lies a 1.4% increase in consumer spending, led by strong demand in sectors like healthcare, finance, and automotive sales.

But what really moved the needle was a dramatic collapse in imports — down 30.3%, reversing the Q1 surge and effectively boosting the GDP calculation.

While exports and business investment both shrank modestly, the overall picture was buoyed by domestic strength and favourable trade math.

💰 Inflation Retreats — Temporarily?

ThePersonal Consumption Expenditures (PCE) Price Index, a key measure of inflation, ticked up just 2.1%, down from 3.7% in the previous quarter.

The Core PCE, which excludes volatile food and energy prices, landed at 2.5%, easing pressure on the Federal Reserve to act aggressively.

Yet policymakers are watching warily. A surge in tariffs—particularly those scheduled for August—could distort prices and consumer behaviour in the months ahead.

🧠 Fed and Market Implications

The GDP bounce gives the Federal Reserve some breathing room, but not total confidence. Investment weakness and subdued export activity could signal structural fragilities beneath the headline growth.

With tariff uncertainty, election-year dynamics, and a cautious jobs market all in play, rate policy may stay frozen until the economic picture becomes clearer.

It looks like investor sentiment is shifting away from obsessing over tariffs—though not because they’ve disappeared.

Instead, there’s a growing sense that tariffs may be settling into a predictable range, especially in the U.S., where President Trump signalled a blanket rate of 15–20% for countries lacking specific trade agreements.

Here’s how that’s playing out

🌐 Why Investors Are Moving On

Predictability over Panic: With clearer expectations around tariff levels, markets may no longer treat them as wildcards.

Muted Market Reaction: The recent U.S.-EU trade deal barely nudged the S&P 500 or European indexes after moving the futures initially, signalling tariffs aren’t the hot trigger they once were.

Economists Cooling Expectations: Revisions to tariff impact estimates suggest future trade deals might not generate outsized optimism on Wall Street.

📈 Effects on the Markets

Focus Shift: Investors are turning to earnings—particularly from the ‘Magnificent Seven’ tech giants—and macroeconomic data for momentum.

Cautious Optimism: While stocks haven’t rallied hard, they’re not dropping either. Traders seem to be waiting for a new catalyst, like U.S. consumer strength or signs of a bull phase in certain indexes.

Geopolitical Undercurrents: A new deadline for Russia to reach a peace deal and threats of ‘secondary tariffs’ could still stir volatility, depending on how global partners react.

So, in short tariffs aren’t gone, but they’ve become background noise. Investors are tuning in to the next big signals.

If you’re keeping an eye on retail, tech earnings, or commodity flows, this shift could have ripple effects worth dissecting.

European and American financial markets rallied following the announcement of a new trade pact between the EU and the U.S on Sunday 27th July 2025., easing months of escalating tensions.

The deal introduces a 15% tariff on most EU exports to the United States—well below the previously threatened 30% rate—providing greater predictability across key sectors.

Global markets surged on Monday following the announcement of a landmark trade agreement between the European Union and the United States, announced by President Donald Trump and European Commission President Ursula von der Leyen at Trump’s Turnberry golf resort in Scotland.

The deal imposes a 15% tariffon most EU exports to the U.S., significantly lower than the previously threatened 30% rate.

It would appear that Trump’s global tariff rate will end up between 15% – 20%

While still a sharp increase from pre-2025 levels—when many goods faced tariffs under 3%—the agreement has been hailed as a pragmatic compromise that averts a full-blown transatlantic trade war.

In exchange, the EU has reportedly committed to $750 billion in U.S. energy purchases and $600 billion in investment into the American economy, with further spending on military equipment also expected.

European negotiators secured zero tariffs on strategic goods such as aircraft components, select chemicals, and semiconductor equipment

Strategic exemptions for aircraft components, semiconductors and select chemicals help preserve supply chain efficiency, while agricultural and consumer goods will adapt to the new rate over time.

In return, the EU has reportedly committed to over $1.3 trillion in investments focused on U.S. infrastructure, renewable energy and defence technologies.

Investors responded positively to the agreement as futures surged

The FTSE 100 futures hit 9,172 overnight

Euro Stoxx 50 futures rose 1.3%.

DAX hit overnight futures high of: 24,550

S&P 500 and Nasdaq Tech 100 hit overnight futures highs of: 6,422 and 23,440

Wall Street’s major indices extended futures gains, boosted by trade optimism and tech strength.

However, European stocks trimmed back ‘futures’ gains after the opening bell.

While some concerns remain over unresolved steel and pharmaceutical tariffs, analysts view the pact as a turning point that restores confidence.

The deal sets the stage for further cooperation on digital standards, regulation and intellectual property later in 2025.

This step toward economic stability is expected to foster stronger ties and benefit export-driven industries across both regions.

Trump is getting his deals, but how good are they really?

The British retail sector saw a modest lift in June 2025, with sales volumes rising 0.9% month-on-month, according to figures released today by the Office for National Statistics.

☀️ Weather Wins Following May’s steep 2.8% decline, the warmest June on record helped drive spending on fuel ⛽, clothing 👕, and drinks 🥤. Supermarkets saw a 0.7% rise after last month’s slump, and automotive fuel sales jumped 2.8%, the strongest gain in over a year.

💻 Online Resilience E-commerce continued to thrive, with online retail up 2.3%, now accounting for 27.8% of all UK retail transactions.

Non-store sales have steadily outpaced traditional footfall, which remains weak in categories like household goods 🛋️ and second-hand stores.

📉 Cautious Optimism Despite the improvement, quarterly growth was a tepid 0.2%, and consumer confidence remains shaky amid inflationary pressure (CPI 3.6%) and speculation about forthcoming tax changes.

📍 Long View Retail volumes are still 1.6% below pre-pandemic benchmarks, highlighting a recovery that’s inching forward rather than sprinting.

The S&P 500 closed above 6,300 for the first time in history on Monday 21st July 2025, while the Nasdaq Composite notched yet another record, finishing at 20,974.17.

Investor enthusiasm for upcoming tech earnings has eclipsed broader concerns over looming global tariffs, fuelling a rally in major indexes.

Despite marginal losses in the Dow Jones Industrial Average, the tech-heavy Nasdaq rose 0.38% while the S&P 500 climbed 0.14%, buoyed by gains in heavyweights like Meta Platforms, Alphabet, and Amazon.

With over 60 S&P 500 companies having reported so far this earnings season, more than 85% have exceeded expectations, according to FactSet.

S&P 500 and Nasdaq Comp at new record highs 21st July 2025

S&P 500 and Nasdaq Comp at new record highs 21st July 2025

Alphabet shares advanced over 2% ahead of Wednesday’s results, and Tesla headlines the ‘Magnificent Seven’ group expected to drive the bulk of earnings growth this quarter. And not necessarily for the right reason.

Analysts reportedly expect the group to deliver 14% growth year-on-year, far outpacing the remaining S&P constituents’ average of 3.4%.

S&P 500

Despite tariff tensions simmering — with the U.S. setting a 1st August deadline for levy enforcement — investor sentiment remains bullish.

Bank of America estimates Q2 earnings are tracking a 5% annual increase, suggesting resilience amid geopolitical headwinds.

Strategists warn of potential volatility, as earnings surprises or policy shifts could spark swift market reactions.

Still, some analysts see space for further upside, projecting a potential S&P climb to 6,600 before any meaningful pullback.

As the tech titans prepare to report, all eyes are on whether optimism can keep the rally alive — or if tariffs will return to centre stage.

From FANG stocks, MAG 7 stocks to AI – the tech titans just keep giving.

Since a little after Donald Trump’s declaration of ‘Liberation Day’ and renewed tariff threats, global markets have shown a remarkable degree of indifference.

While equities dipped briefly in April, investors appear increasingly unshaken by the looming 1st August deadline.

Several factors underpin this resilience. First, market participants have grown accustomed to political brinkmanship.

Traders now view tariff announcements as bargaining tools rather than certainties, adopting a wait-and-see approach before pricing in long-term consequences.

The episodic nature of past trade spats has dulled their impact, especially without immediate legislative backing and with Trump often pulling back last minute or extending deadlines.

The media have labelled this … TACO!

TACO – Trump Always Chickens Out: Definition – A satirical acronym coined by financial commentators to describe Donald Trump’s predictable pattern of announcing aggressive tariffs, then softening or delaying them under market pressure.

Second, economic fundamentals remain firm. Corporate earnings continue to surpass expectations, and key indicators—such as job growth and consumer spending—suggest sustained momentum in major economies.

As a result, the tariff narrative has taken a back seat to earnings reports and central bank manoeuvres.

Third, diversification strategies have matured since the 2018–2020 trade wars. Many multinationals have already restructured supply chains, buffered risk through regional trade agreements, and hedged exposure to volatile sectors.

This strategic evolution makes markets less sensitive to unilateral tariff threats, especially if they lack multilateral support.

Analysts note that Trump’s rhetoric still carries weight politically, but the financial world operates on evidence, not headlines. As one strategist quipped, ‘Markets don’t trade on bluster; they trade on impact’.

That’s all very well – but markets can be fickle and reflect sentiment too.

With investors focused on earnings and monetary policy, tariff drama may remain background noise—unless policy becomes policy.

Until then, the markets seem content to roll with it!

Excluding 2020, when factories were closed during Covid-19 lockdowns, U.K. vehicle production in May 2025 dropped to its lowest level since 1949 – that’s the worst performance in 75 years!

The significant drop in car production is largely attributed to ongoing model updates, restructuring efforts, and the effects of Trump’s tariffs, according to SMMT.

The UK jobs market continued to lose momentum, with fresh data from the Office for National Statistics highlighting a notable slowdown.

Unemployment has climbed to 4.7%, reaching its highest level in four years, while job vacancies fell for a third consecutive year to 727,000—the lowest in a decade, excluding the pandemic dip.

Pay growth also eased, with average annual wage increases slowing to 5% in the March–May 2025 period.

Economists suggest the Bank of England may consider an interest rate cut next month to support employment, although rising inflation remains a complicating factor.

Firms appear hesitant to hire or replace staff, signalling broader economic uncertainty. While the ONS has urged caution around the collection of unemployment data, the trend points to mounting pressure in the UK’s jobs landscape.

As of June 2025, the U.S. annual inflation rate rose to 2.7%, marking its highest level since February 2025.

This uptick was largely driven by new tariffs imposed by President Trump, which increased costs on goods like furniture, clothing, and appliances.

On a monthly basis, U.S. consumer prices climbed 0.3% from May to June, up from a modest 0.1% increase the previous month.

📊 Core inflation—which excludes food and energy—also edged up to 2.9% year-on-year, with a 0.2% monthly increase, suggesting underlying price pressures are building.

Summary

📈 Headline CPI: rose 2.7% year-over-year

🔍 Core inflation (excluding food and energy) climbed to 2.9% annually

📊 Monthly increases: 0.3% for headline CPI, 0.2% for core inflation

The FTSE 100 surged past the 9,000-point mark on 15th July 2025, setting a new all-time high and signalling renewed investor confidence in the UK’s economic outlook.

Driven by strong performances in energy, banking, and AI-adjacent tech firms, the benchmark index shattered psychological resistance with broad-based gains.

Much of the momentum came from robust earnings reports and upbeat forecasts from major constituents such as Shell and HSBC.

Analysts also pointed to growing international interest in UK equities, especially as sterling remains relatively stable amid global currency fluctuations.

The breakthrough follows months of resilience in the face of inflationary pressures and geopolitical uncertainty.

Investors appear to be rewarding UK equities as a steady alternative option against the backdrop of U.S. market turmoil – maybe the U.S.is running out of steam?

While traders welcomed the milestone, some caution against irrational exuberance. Crossing 9,000 is significant, but sustainability depends on whether earnings growth can be maintained

Nonetheless, market watchers view the rally as a strong signal of the FTSE 100’s ability to compete globally.

With fresh liquidity and stabilising rates, the index might not just pause at 9,000 — it may soon look to test even higher ground.

Despite President Donald Trump’s renewed push for sweeping tariffs, global markets appear unfazed.

Trump issued letters to 14 countries – including Japan, South Korea, and Malaysia—outlining new import levies ranging from 25% to 40%, set to take effect on 1st August 2025. More letters then followed.

Yet, major indices like the FTSE 100 and Nikkei 225 barely flinched, with some even posting modest gains.

So, who’s right—the president or the markets?

Trump insists tariffs are essential to redress trade imbalances and bring manufacturing back to the U.S. The EU also faces higher tariffs.

He’s floated extreme measures, including a 200% tariff on pharmaceuticals and a 50% levy on copper.

His administration argues these moves will strengthen domestic industry and reduce reliance on foreign supply chains.

However, investors seem to be betting on a familiar pattern: Trump talks tough but ultimately softens under pressure. Analysts have dubbed this the ‘TACO’ trade—Trump Always Chickens Out.

His own comments have added to the ambiguity, calling the August deadline ‘firm, but not 100% firm’.

The economic logic behind the tariffs is being questioned. Tariffs are paid by importers—often U.S. businesses and consumers—not foreign governments.

This could lead to higher prices and inflation, especially in sectors like healthcare and electronics. Some economists warn of recessionary risks for countries like Japan and South Korea.

In short, markets may be right to remain calm—for now. But if Trump follows through, the impact could be far-reaching.

With trade negotiations still in flux and only two deals (UK and Vietnam) finalised, the next few weeks will be critical. Investors may be wise not to ignore the warning signs entirely.

Whether this is brinkmanship or a genuine shift in trade policy, the stakes are high—and the clock is ticking.

Britain’s economy shrank by 0.1% in May 2025, marking its second consecutive monthly decline and casting fresh doubt over the strength of the post-pandemic recovery.

The latest figures from the Office for National Statistics defied analyst expectations of modest growth, underlining deepening concerns within the Treasury and among business groups.

The drop was largely driven by a sharp 0.9% fall in production output, particularly in oil and car manufacturing, alongside a 0.6% decline in construction activity.

These weaknesses come despite a slight uptick in services, which rose by 0.1%, buoyed by gains in legal services and software development.

Summary

🏭 Production output fell by 0.9%, led by declines inl oil and gas extraction and car manufacturing.

🏗️ Construction dropped 0.6%, reversing April’s gains.

🛍️ Services eked out a 0.1% rise, with legal services and computer programming offsetting a sharp fall in retail.

Finance Minister Rachel Reeves faces increasing pressure as her economic reboot agenda collides with rising domestic costs and global headwinds.

April’s national insurance hikes and Trump’s aggressive tariff policy have created economic drag, despite the UK having brokered a swift bilateral trade agreement with the U.S.

The three-month growth rate stands at 0.5%, but economists now predict a meagre 0.1% expansion for the second quarter.

With inflation edging back above 3% and interest rate cuts looming, the government must navigate a delicate balance between stimulus and stability.

The first official Q2 GDP estimate will be released on 14th August 2025, with markets braced for further volatility.

UK GDP figures February through May 2025

Month

% Change in GDP

Key Drivers/Comments

February

+0.5%

Strong services and frontloaded activity pre-tariffs

March

+0.2%

Moderate growth, tax rise concerns begin

April

–0.3%

Domestic tax hikes, Trump tariff shock

May

–0.1%

Production –0.9%, construction –0.6%; weak manufacturing

Following the passage of President Donald Trump’s sweeping tax and spending legislation, dubbed the One Big Beautiful Bill, the U.S. national debt has officially soared to nearly $37 trillion, with projections suggesting it could hit $40 trillion by year’s end.

The bill, which extends 2017 tax cuts and introduces expansive spending on defence, border security, and domestic manufacturing, has sparked fierce debate across Washington and Wall Street.

Critics argue the legislation lacks meaningful offsets, with no new taxes or spending cuts to balance its provisions.

Interest payments alone reached $1.1 trillion in 2024, surpassing the defence budget. The Congressional Budget Office estimates the bill could add $3.3 trillion to the deficit over the next decade.

Musk has labelled the bill a ‘disgusting abominatio’ and warned it undermines fiscal responsibility.

He has reportedly pledged to fund primary challengers against Republicans who supported the measure, accusing them of betraying their promises to reduce spending.

Musk’s concerns go beyond economics. He argues the bill reflects a broken political system dominated by self-interest, calling for the creation of a new political movement, the America Party, to restore accountability.

While the White House insists the bill will spur economic growth and eventually reduce the debt-to-GDP ratio, sceptics remain unconvinced.

With the debt ceiling raised by a record $5 trillion, the long-term implications for America’s financial stability are now front and centre.

As the dust settles, the clash between Trump’s fiscal vision and Musk’s warnings sets the stage for a turbulent political and economic period ahead.

In a fresh escalation of trade tensions, President Donald Trump has once again moved the goalposts on tariff policy, pushing the deadline for new trade deals to 1st August 2025.

This marks the second extension since the original April 2025 ‘Liberation Day’ announcement, which had already stirred global markets.

The latest twist includes a new 10% tariff targeting countries aligned with the BRICS bloc—Brazil, Russia, India, China, and South Africa – along with newer members such as Iran and the UAE.

Trump declared on Truth Social that ‘any country aligning themselves with the Anti-American policies of BRICS will be charged an ADDITIONAL 10% tariff. There will be no exceptions’.

The move has drawn sharp criticism from BRICS leaders, who condemned the tariffs as ‘indiscriminate’ and warned of rising protectionism. Industrial metals, including copper and aluminium, saw immediate price drops amid fears of disrupted supply chains.

While the White House insists the new deadline allows more time for negotiation, analysts warn the uncertainty could dampen global trade and investor confidence.

With letters outlining tariff terms expected to be sent this week, investors and market makers watch closely as Trump’s trade strategy continues to evolve or unravel.