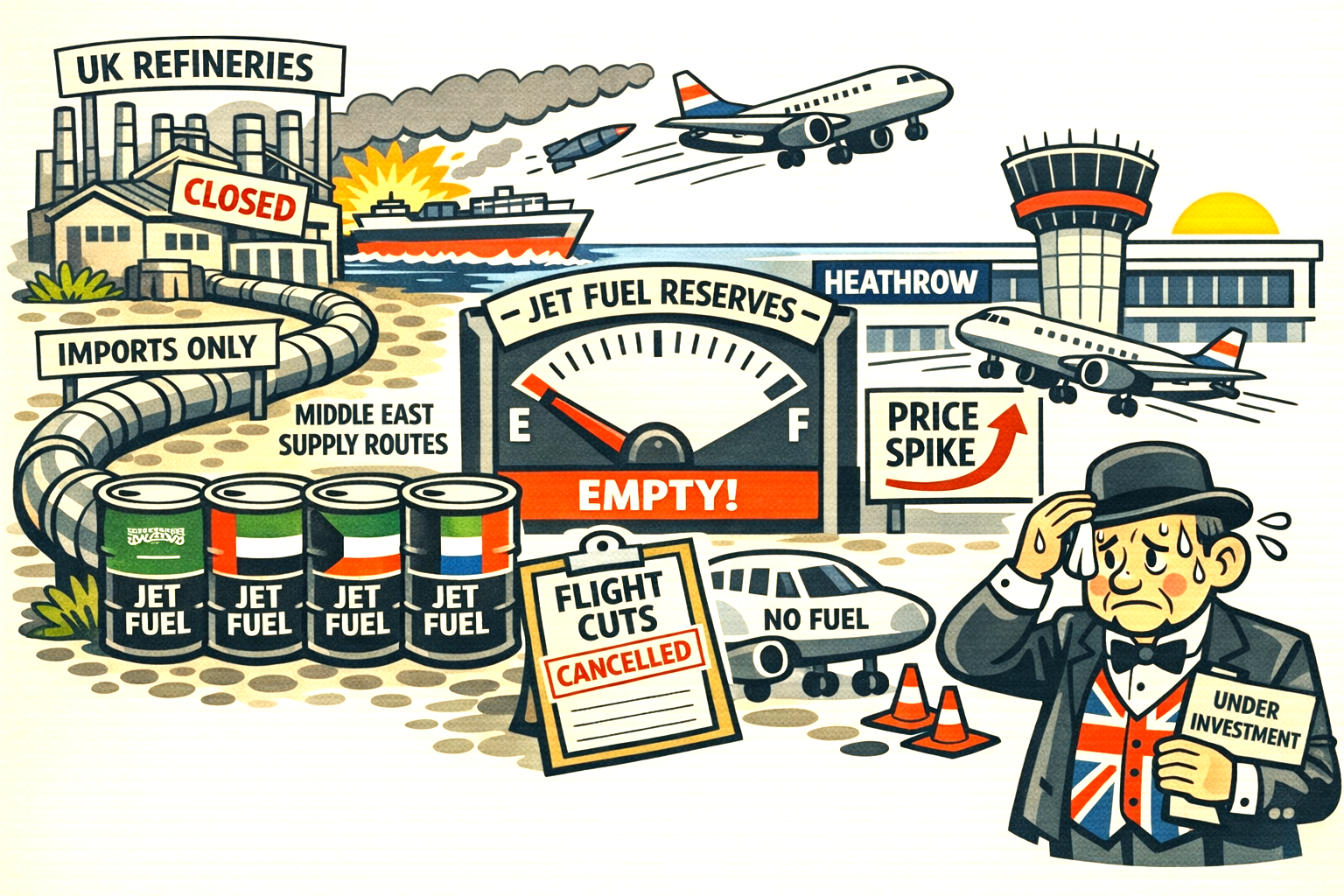

Britain’s jet fuel problem is the predictable result of a long, quiet erosion of refining capacity colliding with a geopolitical shock and decades of under investment.

The country now imports three times more kerosene than it produces, and the Middle East crisis has exposed just how thin those supply lines have become.

A system built on shrinking refineries

The UK once had 18 refineries; today it has just four. Closures at Lindsey and Grangemouth last year removed two critical plants, including Scotland’s only kerosene supplier.

The remaining refineries — Fawley, Humber, Pembroke and Stanlow — supply most domestic needs but cannot meet jet fuel demand.

Output has fallen 41% since 2000, driven by poor investment returns, high carbon costs, and the government’s push toward electrification reducing demand for other fuels.

This leaves Britain structurally dependent on imports for diesel and, crucially, kerosene.

The kerosene dependency

Jet fuel demand is unusually high because of Heathrow’s role as a global hub. In 2024, the UK was the second‑largest jet fuel consumer in the OECD, behind only the U.S.

Yet domestic production covers only a fraction of that. Britain reportedly imported around 3.1 times more kerosene than it produced in 2024.

And the sources of those imports are concentrated: 60% come from Saudi Arabia, the UAE and Kuwait, making the UK acutely exposed to any disruption in the Strait of Hormuz.

The real vulnerability: almost no stockpiles

Britain holds just one month’s worth of jet fuel reserves, far lower than most advanced economies. When Middle Eastern supply is threatened, the UK has no buffer.

European alternatives exist — notably the Netherlands and Antwerp — but prices have already doubled, and airlines are preparing to cut capacity.

The bigger picture

This is not a sudden crisis but the culmination of two decades of under‑investment, policy drift and over‑reliance on global markets.

Jet fuel is simply the first commodity where the structural weakness has become impossible to ignore.

The UK needs to get a grip!

A ‘systemic’ jet fuel shortage is brewing in Europe if the U.S. led Iran war crisis isn’t resolved soon.

There’s a growing sense that financial markets have drifted into a parallel reality. Not the usual detachment that comes with speculation, but something deeper — a structural break between what is happening in the world and what markets choose to see.

This is how the stock market feels at the moment. I might be wrong, but the overwhelming sense of despair feels so real. I believe the markets are broken at their core, and nobody seems to care. Markets make money and remain devoid of morality.

The system is morally bankrupt.

You can watch a crisis unfold in real time, with footage, statements, explosions and diplomatic failures, and yet the markets behave as though they’re responding to a completely different script.

A ceasefire that barely exists is treated as a turning point. A strategic waterway that is “open” only in the loosest, most cosmetic sense is priced as fully restored. The disconnect isn’t subtle. It’s brazen.

And yes — it feels deceptive

Not because traders are conspiring to mislead anyone, but because the modern market has evolved into something that no longer requires truth to function.

It only needs a narrative.

A headline. A phrase that can be interpreted as “less bad than yesterday”. That’s enough to ignite a rally, even if the underlying situation is deteriorating by the hour.

This wasn’t always the case. There was a time when markets, for all their volatility and irrationality, still behaved like instruments tethered to reality.

When a major shipping lane was threatened, prices moved accordingly. When a ceasefire collapsed, markets reflected the renewed danger. There was at least a rough correlation between events and valuations — imperfect, but recognisable.

Today, that correlation has snapped. The market trades on sentiment, not substance. On the idea of stability, not the presence of it.

Appearance

On the appearance of progress, even when the facts on the ground contradict every optimistic headline. A ceasefire announcement is enough to send equities higher, even if the ceasefire is violated before the ink dries.

A promise to reopen a strait is enough to calm oil prices, even if only a handful of ships actually move.

The deception is structural. It’s the product of algorithmic trading that reacts to keywords rather than conditions.

It’s the result of a decade of central bank intervention that has taught investors to treat every crisis as temporary and every dip as a buying opportunity. It’s reinforced by political communication that prioritises market stability over factual clarity.

The system rewards optimism, even when it’s unjustified. It punishes realism when it’s inconvenient.

Surreal

This is why the current moment feels so surreal. You can see the footage of strikes in Lebanon while reading headlines about “regional de‑escalation”. You can watch tankers stalled while analysts talk about “normalising flows”.

The market shrugs, because the narrative — however flimsy — is enough to sustain the illusion.

If markets don’t need truth, then they are, in effect, trading a deception. Not a deliberate deception, but a functional one.

Economic Truth

A deception that keeps prices elevated, volatility suppressed, and investors soothed.

A deception that allows the charts to climb even as the world beneath them fractures.

A deception that has become the operating principle of a system that no longer reflects reality, only the stories it finds convenient to believe.

This isn’t investing – this is pure manipulative gameplay and benefits only those who know how to play the game.

And ‘they’ set the rules.

Markets make the money but remain devoid of morality.

I feel like I am playing a video game without the controller or at least with a rule book.

Update:

U.S. announces it will blockade of the Strait of Hormuz, or rather Iranian ‘linked’ ships. And not in the Strait but further out in international waters. This is designed to reduce the risk of conflict.

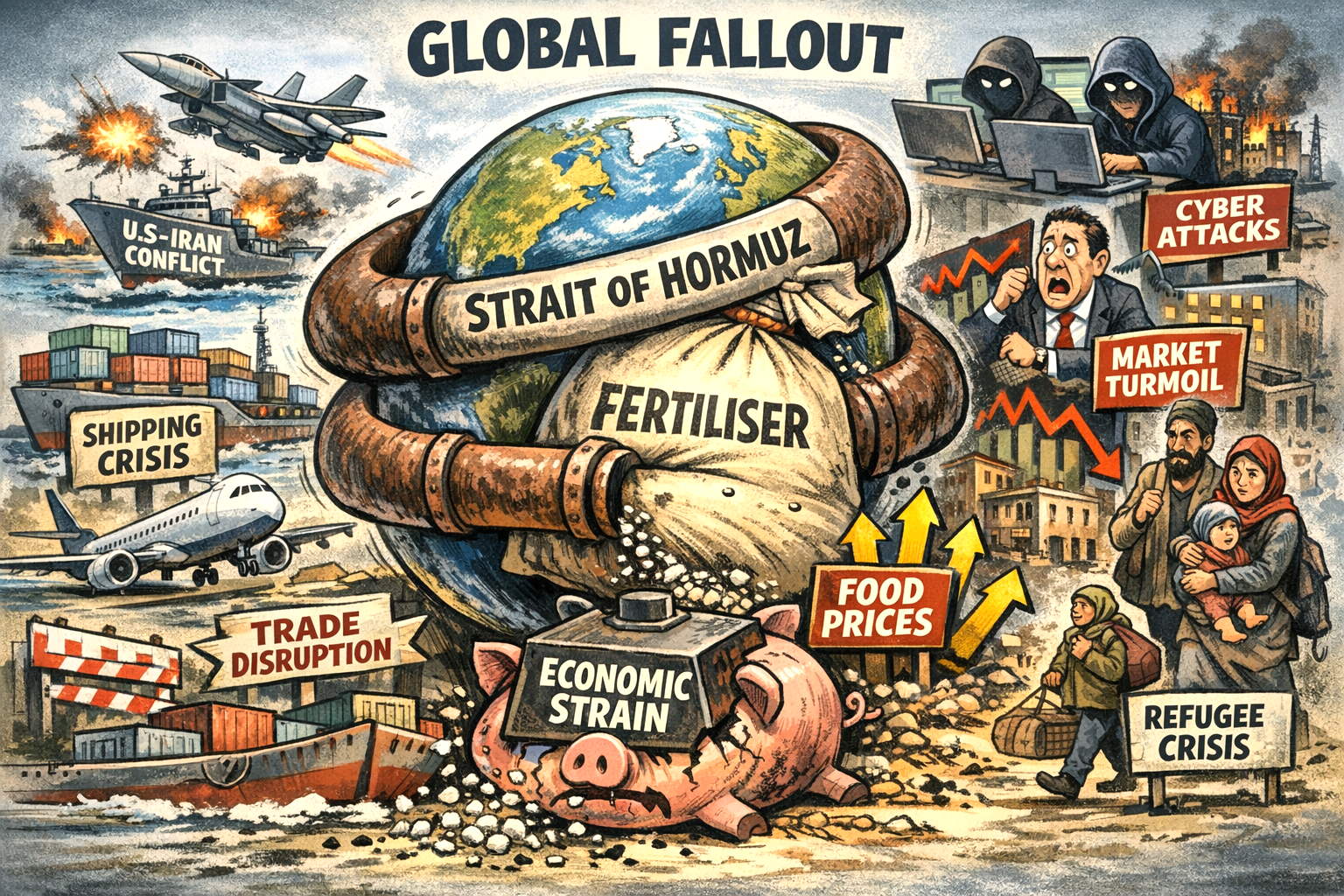

If the U.S.–Iran conflict drags on for weeks or months, the global impact will extend far beyond oil markets. Energy prices are only the first domino.

The deeper, more destabilising effects emerge through shipping disruption, fertiliser shortages, food‑price inflation, financial volatility, cyber escalation, and regional political instability.

For the UK — already wrestling with structural food‑system fragility — the conflict becomes a real‑world stress test.

This report outlines 15 potential major knock‑on effects that would shape the global economy if the conflict becomes protracted.

1. Global Shipping Disruption

The Strait of Hormuz is not just an oil artery; it is a global shipping chokepoint. As vessels reroute or halt operations:

Container shipping delays spread across Asia, Europe and the Gulf.

War‑risk insurance premiums spike for all vessels.

Freight costs rise, feeding into non‑energy inflation.

This is the mechanism by which a regional conflict becomes a global economic event.

2. Aviation and Travel Disruption

Iranian retaliation has already included strikes on Gulf airports and hotels. If this continues:

Airlines reroute or cancel flights across the Gulf, South Asia and East Africa.

Longer flight paths increase fuel burn and fares.

Tourism in the UAE, Oman, Bahrain and potentially Turkey contracts sharply.

Aviation is one of the fastest channels through which geopolitical instability hits consumers.

3. Financial Market Volatility

Markets dislike uncertainty, and this conflict delivers it in abundance.

Investors flee to gold, the dollar and U.S. Treasuries.

Emerging markets face capital outflows.

Equity volatility rises in shipping, aviation and manufacturing sectors.

The longer the conflict persists, the more entrenched this volatility becomes.

4. Fertiliser Disruption: The Hidden Trigger

Over one‑third of global fertiliser trade moves through the Strait of Hormuz. With shipments stranded:

Urea, ammonia, phosphates and sulphur prices surge.

Farmers worldwide face higher input costs.

Lower fertiliser availability leads to reduced crop yields.

This is the beginning of a food‑system shock that unfolds over months, not days.

5. Global Food‑Price Inflation

As fertiliser shortages ripple through agriculture:

Wheat, rice, maize and oilseed yields fall.

Livestock feed becomes more expensive, pushing up meat, dairy and egg prices.

Food‑importing regions face acute pressure.

Grain futures markets become more volatile.

This is how a conflict becomes a global cost‑of‑living crisis.

UK Exposure

The UK is particularly vulnerable because:

It imports a large share of its fertiliser and food.

Its agricultural sector is energy‑intensive.

Supermarket supply chains are sensitive to freight and insurance costs.

Bread, cereals, dairy and meat are the first categories to feel the squeeze.

6. Supply Chain Strain Beyond Food and Energy

A prolonged conflict disrupts:

Petrochemicals

Plastics

Fertilisers

Industrial metals

Gulf‑based manufacturing and logistics

This feeds into higher costs for everything from packaging to electronics.

7. Corporate Investment Freezes

Businesses hate uncertainty. Expect:

Delays or cancellations of Gulf megaprojects.

Slower investment in petrochemicals, logistics and tech hubs.

Reduced appetite for Gulf‑exposed assets.

This undermines diversification efforts like Saudi Vision 2030.

8. Cyber Escalation

Iran has a long history of cyber retaliation. Likely developments include:

Attacks on Western banks, utilities and government systems.

Disruptions to Gulf infrastructure, including airports and desalination plants.

Rising cybersecurity costs for businesses globally.

Cyber conflict is asymmetric, deniable and cheap — making it a likely pressure valve.

9. Regional Political Destabilisation

The killing of senior Iranian leadership has already shaken the region.

Possible outcomes include:

Internal instability within Iran.

Escalation involving Hezbollah, Iraqi militias, Syrian factions and the Houthis.

Pressure on Gulf monarchies if civilian infrastructure continues to be targeted.

This is where the conflict risks widening beyond its initial theatre.

10. Migration and Humanitarian Pressures

If the conflict intensifies:

Refugee flows from Iran, Iraq and Syria could rise.

Europe — especially Greece, Turkey and the Balkans — faces renewed border pressure.

Humanitarian budgets shrink as Western states divert funds to defence.

This adds a political dimension to the economic fallout.

11. Insurance Market Stress

War‑risk insurance is already spiking.

Expect:

Higher premiums for shipping, aviation and energy infrastructure.

Reduced insurer appetite for Gulf‑exposed assets.

Knock‑on effects on global trade costs and consumer prices.

Insurance is a silent amplifier of geopolitical risk.

12. Higher Global Borrowing Costs

Sustained conflict spending creates:

Budgetary strain for the U.S., UK, EU and Gulf states.

Reduced fiscal space for domestic programmes.

Higher global borrowing costs as markets price in sustained uncertainty.

This tightens financial conditions worldwide.

13. Pressure on Emerging Markets

Countries heavily reliant on imported energy or food face:

Worsening trade balances

Currency depreciation

Higher inflation

Greater risk of sovereign stress

This is especially acute in South Asia, North Africa and parts of Latin America.

14. Strain on Multilateral Institutions

A prolonged conflict diverts attention and resources from:

Climate finance

Development aid

Humanitarian relief

Global health programmes

Institutions already stretched by Ukraine, Gaza and climate disasters face further overload.

15. The Strategic Reordering of Alliances

A drawn‑out conflict may accelerate geopolitical realignment:

Gulf states hedge between Washington and Beijing.

India and Turkey pursue more independent foreign policies.

Europe faces renewed pressure to define its own security posture.

Russia benefits from higher energy prices and Western distraction.

This is the long‑term consequence: a shift in the global balance of power.

Conclusion: A Conflict That Radiates Far Beyond Oil

If the U.S.–Iran war limps on, the world will feel it in supermarket aisles, shipping lanes, financial markets and political systems.

The most consequential knock‑on effect is not oil — it is fertiliser. That is the hinge on which global food security turns.

For the UK, the conflict exposes the fragility of a food system dependent on imports, long supply chains and energy‑intensive agriculture.

This is not just a Middle Eastern conflict. It is a global economic event in slow motion.