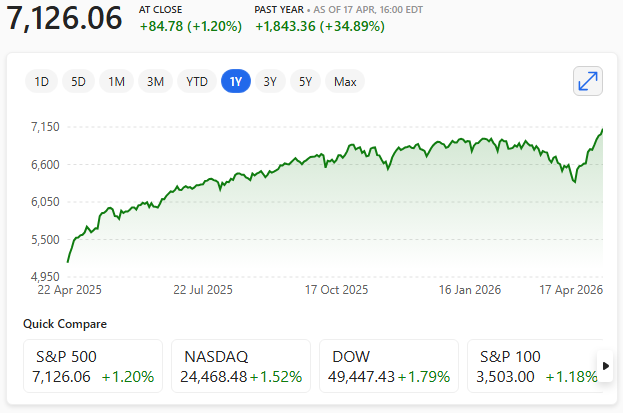

Global equities have staged a striking recovery, erasing the losses triggered by the U.S.–Israel–Iran conflict and pushing into fresh record territory.

On the surface, this looks counter‑intuitive: the ceasefire remains fragile, diplomatic progress is uneven, and the threat of renewed escalation still hangs over the Strait of Hormuz. Yet markets have not only stabilised — they have surged.

It’s the AI boom stupid

The explanation lies less in geopolitics and more in positioning, psychology, and the gravitational pull of the AI boom.

The first phase of the conflict saw investors pile into defensive trades: higher oil, a stronger dollar, and a broad de‑risking across equities.

That created a sizeable war‑risk premium. Once even the possibility of a ceasefire emerged, that premium unwound at speed.

Analysts note that the rebound has been driven primarily by the rapid reversal of hedges rather than any fundamental improvement in the geopolitical outlook.

In other words, markets had priced in a worst‑case scenario — and when that scenario didn’t immediately materialise, the snap‑back was violent.

Short covering

This shift in sentiment was amplified by short‑covering, particularly among hedge funds that had positioned for prolonged disruption to energy flows.

As soon as investors judged the conflict likely to remain contained, the earlier sell‑off looked excessive. That alone was enough to propel global indices back above pre‑war levels. But it wasn’t the only force at work.

The macro backdrop has also proved more resilient than feared. U.S. labour market data has held up, and expectations for Federal Reserve rate cuts later in the year remain intact.

AI investment

Crucially, the AI‑driven investment cycle continues to dominate equity performance. Surging demand for compute, improving funding conditions, and strong earnings momentum in technology have provided a powerful counterweight to geopolitical anxiety.

For many investors, the structural growth story in AI simply outweighs the cyclical risks emanating from the Middle East.

Some caution

Still, the rally is not unqualified. Bond markets remain more cautious, with real yields and inflation expectations signalling that the risk of an energy‑driven slowdown has not disappeared.

And as peace talks wobble, equities have already begun to give back some gains — a reminder that this is a conditional rally, not a complacent one.

Markets may be hitting records, but they are doing so with one eye firmly on the horizon. The shadow of the conflict hasn’t lifted; investors have simply decided, for now, that it is not the dominant story.