Global equities have staged a striking recovery, erasing the losses triggered by the U.S.–Israel–Iran conflict and pushing into fresh record territory.

On the surface, this looks counter‑intuitive: the ceasefire remains fragile, diplomatic progress is uneven, and the threat of renewed escalation still hangs over the Strait of Hormuz. Yet markets have not only stabilised — they have surged.

It’s the AI boom stupid

The explanation lies less in geopolitics and more in positioning, psychology, and the gravitational pull of the AI boom.

The first phase of the conflict saw investors pile into defensive trades: higher oil, a stronger dollar, and a broad de‑risking across equities.

That created a sizeable war‑risk premium. Once even the possibility of a ceasefire emerged, that premium unwound at speed.

Analysts note that the rebound has been driven primarily by the rapid reversal of hedges rather than any fundamental improvement in the geopolitical outlook.

In other words, markets had priced in a worst‑case scenario — and when that scenario didn’t immediately materialise, the snap‑back was violent.

Short covering

This shift in sentiment was amplified by short‑covering, particularly among hedge funds that had positioned for prolonged disruption to energy flows.

As soon as investors judged the conflict likely to remain contained, the earlier sell‑off looked excessive. That alone was enough to propel global indices back above pre‑war levels. But it wasn’t the only force at work.

The macro backdrop has also proved more resilient than feared. U.S. labour market data has held up, and expectations for Federal Reserve rate cuts later in the year remain intact.

AI investment

Crucially, the AI‑driven investment cycle continues to dominate equity performance. Surging demand for compute, improving funding conditions, and strong earnings momentum in technology have provided a powerful counterweight to geopolitical anxiety.

For many investors, the structural growth story in AI simply outweighs the cyclical risks emanating from the Middle East.

Some caution

Still, the rally is not unqualified. Bond markets remain more cautious, with real yields and inflation expectations signalling that the risk of an energy‑driven slowdown has not disappeared.

And as peace talks wobble, equities have already begun to give back some gains — a reminder that this is a conditional rally, not a complacent one.

Markets may be hitting records, but they are doing so with one eye firmly on the horizon. The shadow of the conflict hasn’t lifted; investors have simply decided, for now, that it is not the dominant story.

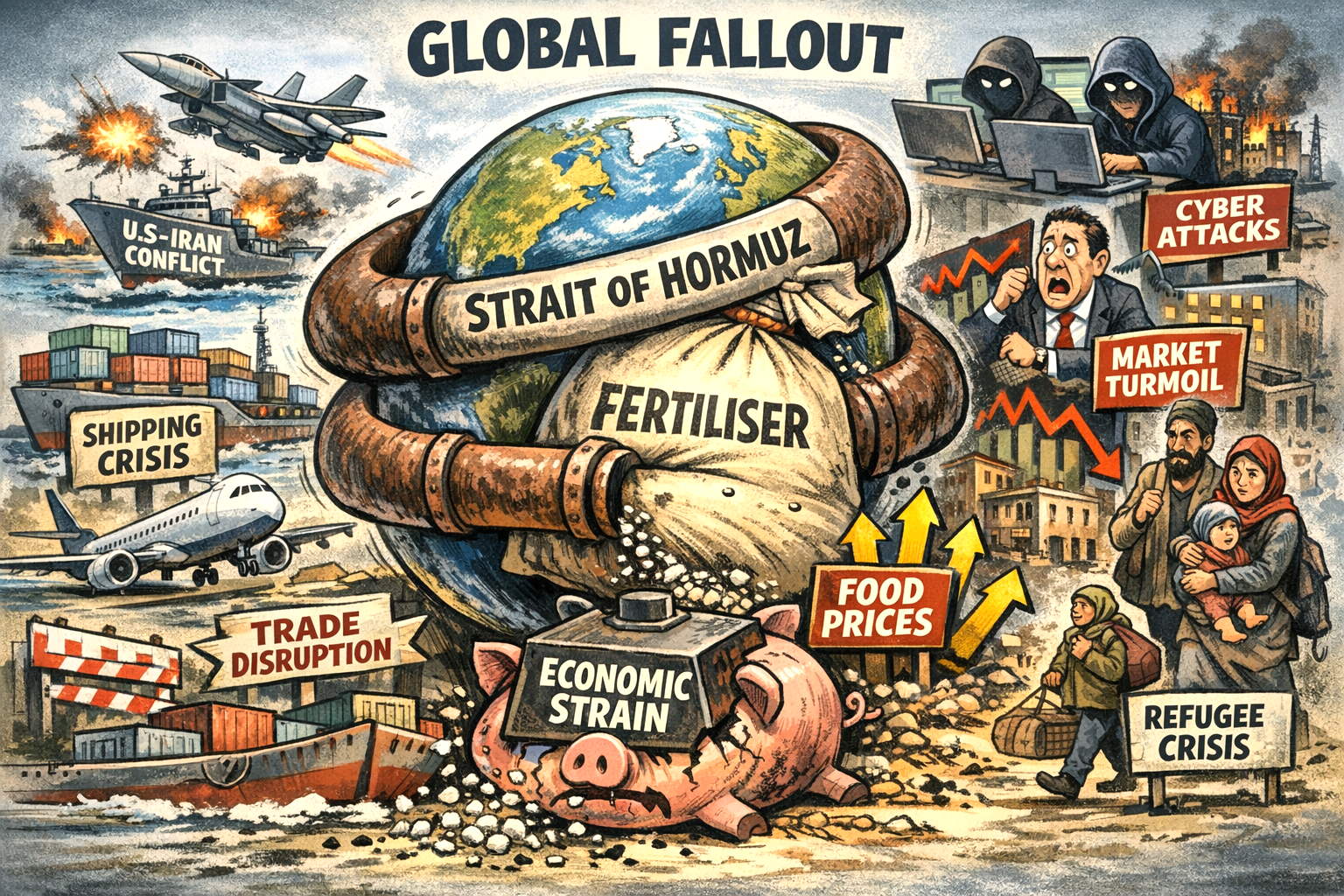

If the U.S.–Iran conflict drags on for weeks or months, the global impact will extend far beyond oil markets. Energy prices are only the first domino.

The deeper, more destabilising effects emerge through shipping disruption, fertiliser shortages, food‑price inflation, financial volatility, cyber escalation, and regional political instability.

For the UK — already wrestling with structural food‑system fragility — the conflict becomes a real‑world stress test.

This report outlines 15 potential major knock‑on effects that would shape the global economy if the conflict becomes protracted.

1. Global Shipping Disruption

The Strait of Hormuz is not just an oil artery; it is a global shipping chokepoint. As vessels reroute or halt operations:

Container shipping delays spread across Asia, Europe and the Gulf.

War‑risk insurance premiums spike for all vessels.

Freight costs rise, feeding into non‑energy inflation.

This is the mechanism by which a regional conflict becomes a global economic event.

2. Aviation and Travel Disruption

Iranian retaliation has already included strikes on Gulf airports and hotels. If this continues:

Airlines reroute or cancel flights across the Gulf, South Asia and East Africa.

Longer flight paths increase fuel burn and fares.

Tourism in the UAE, Oman, Bahrain and potentially Turkey contracts sharply.

Aviation is one of the fastest channels through which geopolitical instability hits consumers.

3. Financial Market Volatility

Markets dislike uncertainty, and this conflict delivers it in abundance.

Investors flee to gold, the dollar and U.S. Treasuries.

Emerging markets face capital outflows.

Equity volatility rises in shipping, aviation and manufacturing sectors.

The longer the conflict persists, the more entrenched this volatility becomes.

4. Fertiliser Disruption: The Hidden Trigger

Over one‑third of global fertiliser trade moves through the Strait of Hormuz. With shipments stranded:

Urea, ammonia, phosphates and sulphur prices surge.

Farmers worldwide face higher input costs.

Lower fertiliser availability leads to reduced crop yields.

This is the beginning of a food‑system shock that unfolds over months, not days.

5. Global Food‑Price Inflation

As fertiliser shortages ripple through agriculture:

Wheat, rice, maize and oilseed yields fall.

Livestock feed becomes more expensive, pushing up meat, dairy and egg prices.

Food‑importing regions face acute pressure.

Grain futures markets become more volatile.

This is how a conflict becomes a global cost‑of‑living crisis.

UK Exposure

The UK is particularly vulnerable because:

It imports a large share of its fertiliser and food.

Its agricultural sector is energy‑intensive.

Supermarket supply chains are sensitive to freight and insurance costs.

Bread, cereals, dairy and meat are the first categories to feel the squeeze.

6. Supply Chain Strain Beyond Food and Energy

A prolonged conflict disrupts:

Petrochemicals

Plastics

Fertilisers

Industrial metals

Gulf‑based manufacturing and logistics

This feeds into higher costs for everything from packaging to electronics.

7. Corporate Investment Freezes

Businesses hate uncertainty. Expect:

Delays or cancellations of Gulf megaprojects.

Slower investment in petrochemicals, logistics and tech hubs.

Reduced appetite for Gulf‑exposed assets.

This undermines diversification efforts like Saudi Vision 2030.

8. Cyber Escalation

Iran has a long history of cyber retaliation. Likely developments include:

Attacks on Western banks, utilities and government systems.

Disruptions to Gulf infrastructure, including airports and desalination plants.

Rising cybersecurity costs for businesses globally.

Cyber conflict is asymmetric, deniable and cheap — making it a likely pressure valve.

9. Regional Political Destabilisation

The killing of senior Iranian leadership has already shaken the region.

Possible outcomes include:

Internal instability within Iran.

Escalation involving Hezbollah, Iraqi militias, Syrian factions and the Houthis.

Pressure on Gulf monarchies if civilian infrastructure continues to be targeted.

This is where the conflict risks widening beyond its initial theatre.

10. Migration and Humanitarian Pressures

If the conflict intensifies:

Refugee flows from Iran, Iraq and Syria could rise.

Europe — especially Greece, Turkey and the Balkans — faces renewed border pressure.

Humanitarian budgets shrink as Western states divert funds to defence.

This adds a political dimension to the economic fallout.

11. Insurance Market Stress

War‑risk insurance is already spiking.

Expect:

Higher premiums for shipping, aviation and energy infrastructure.

Reduced insurer appetite for Gulf‑exposed assets.

Knock‑on effects on global trade costs and consumer prices.

Insurance is a silent amplifier of geopolitical risk.

12. Higher Global Borrowing Costs

Sustained conflict spending creates:

Budgetary strain for the U.S., UK, EU and Gulf states.

Reduced fiscal space for domestic programmes.

Higher global borrowing costs as markets price in sustained uncertainty.

This tightens financial conditions worldwide.

13. Pressure on Emerging Markets

Countries heavily reliant on imported energy or food face:

Worsening trade balances

Currency depreciation

Higher inflation

Greater risk of sovereign stress

This is especially acute in South Asia, North Africa and parts of Latin America.

14. Strain on Multilateral Institutions

A prolonged conflict diverts attention and resources from:

Climate finance

Development aid

Humanitarian relief

Global health programmes

Institutions already stretched by Ukraine, Gaza and climate disasters face further overload.

15. The Strategic Reordering of Alliances

A drawn‑out conflict may accelerate geopolitical realignment:

Gulf states hedge between Washington and Beijing.

India and Turkey pursue more independent foreign policies.

Europe faces renewed pressure to define its own security posture.

Russia benefits from higher energy prices and Western distraction.

This is the long‑term consequence: a shift in the global balance of power.

Conclusion: A Conflict That Radiates Far Beyond Oil

If the U.S.–Iran war limps on, the world will feel it in supermarket aisles, shipping lanes, financial markets and political systems.

The most consequential knock‑on effect is not oil — it is fertiliser. That is the hinge on which global food security turns.

For the UK, the conflict exposes the fragility of a food system dependent on imports, long supply chains and energy‑intensive agriculture.

This is not just a Middle Eastern conflict. It is a global economic event in slow motion.

Silver has surged with remarkable force, blasting to fresh record highs and reshaping market sentiment in the process.

Recent trading sessions have seen prices vault past previous milestones, climbing above $108 per ounce and even approaching the $109 mark as safe‑haven demand intensifies amid global uncertainty.

This dramatic meteoric ascent follows weeks of accelerating momentum, with technical indicators showing a firmly bullish structure and widening gaps between key moving averages.

Analysts note that silver’s rally has outpaced many other commodities, fuelled by its dual role as both a precious metal and an essential industrial input.

Silver one-year chart 26th January 2026

Industrial sectors—from photovoltaics to electric vehicles—are feeling the pressure as soaring prices push material costs sharply higher.

In some cases, silver now represents more than 30% of total solar module expenses, underscoring the far‑reaching impact of this surge.

With supply constraints tightening and investor appetite growing, silver’s explosive rise shows little sign of slowing down.

Gold’s recent surge—hitting over $3,550 per ounce (4th September 2025)—isn’t just a speculative blip.

It’s a convergence of deep structural shifts and short-term catalysts that are reshaping how investors, central banks, and governments think about value and stability.

Here’s why

🧭 Strategic Drivers (Long-Term Forces)

Central Bank Buying: Nearly half of surveyed central banks reportedly plan to increase gold reserves through 2025, citing inflation hedging, crisis resilience, and reduced reliance on the U.S. dollar.

Dollar Diversification: After Western sanctions froze Russia’s reserves in 2022, many countries began reassessing their exposure to dollar-denominated assets.

Fiscal Expansion & Debt Concerns: With U.S. debt surpassing $37 trillion and new legislation adding trillions more, gold is seen as a hedge against long-term dollar instability.

⚡ Tactical Catalysts (Short-Term Triggers)

Geopolitical Tensions: Ongoing wars, trade disputes, and questions around Federal Reserve independence have heightened uncertainty, boosting gold’s ‘fear hedge’ appeal.

Interest Rate Expectations: The Fed has held rates steady, but markets anticipate cuts. Lower yields make non-interest-bearing assets like gold more attractive.

Weakening U.S. Dollar: The dollar’s decline against the euro and yen has made gold cheaper for foreign buyers, increasing global demand.

ETF Inflows & Retail Demand: Physically backed gold ETFs saw their largest first-half inflows since 2020, while bar demand rose 10% in 2024.

Gold isn’t just a commodity—it’s a referendum on trust. When institutions wobble and currencies lose their shine, gold becomes the narrative anchor: a timeless, tangible vote of no confidence in the system.

Summary

🛡️ Safe Haven: Retains value during crisis.

📈 Inflation Hedge: Preserves purchasing power.

🧩 Portfolio Diversifier: Low correlation with other assets.

✋ Tangible Asset: Physical, unlike stocks or bonds.

The stock market is often seen as a barometer of economic health, but its relationship with the broader U.S. economy is more nuanced than it might appear.

Although there are links between the two, they do not always correlate. The intricacies of this relationship and its implications for investors and the general public are multifaceted.

The stock market – A snapshot of investor sentiment

The stock market is largely a reflection of investor sentiment and their expectations for future economic performance. When investors feel optimistic, stock prices generally increase. On the other hand, when they are pessimistic, stock prices are likely to decrease. Because the market is driven by sentiment, it can react to factors that don’t immediately affect the real economy, like geopolitical events, interest rate changes, or corporate earnings announcements.

Economic indicators: The real economy

The well-being of the U.S. economy is often assessed using various indicators such as Gross Domestic Product (GDP) growth, unemployment rates, consumer spending, and inflation. These metrics offer a broader perspective on the economic climate. For example, an expanding GDP coupled with low unemployment usually indicates a robust economy, despite any fluctuations in the stock market.

Divergence between the stock market and the economy

Occasionally, the stock market and the economy may move in different directions. For instance, during the COVID-19 pandemic, the stock market swiftly recovered from an initial downturn due to extraordinary fiscal and monetary stimulus measures. In contrast, the wider economy’s recovery was more protracted, marked by persistent high unemployment and substantial disruptions across numerous industries.

Likewise, the stock market might fall even amidst positive economic indicators. This occurs when investors foresee impending difficulties, such as possible increases in interest rates or geopolitical conflicts, that could affect corporate earnings.

Short-term vs. long-term perspectives

The stock market frequently responds to short-term factors and investor behaviours, such as speculation and market sentiment, leading to volatility that may not align with the underlying economic fundamentals. Conversely, economic indicators generally offer a more long-term perspective on the economy’s health.

The broader impact of the stock market

Although the stock market’s performance can influence the economy via wealth effects and corporate investments, it is not the only indicator of economic vitality. The performance of the stock market is significant to many U.S. citizens, especially those with investments through retirement plans.

However, the real economy, as measured by employment, production, and consumption, often has a more direct impact on people’s daily lives.

Conclusion

In conclusion, although the stock market is linked to the U.S. economy, they do not always move in tandem. The stock market reflects investor sentiment and anticipations for the future, yet it may not fully represent the present economic conditions.

Hence, for a thorough assessment of economic health, it is crucial to evaluate various economic indicators in addition to the performance of the stock market.