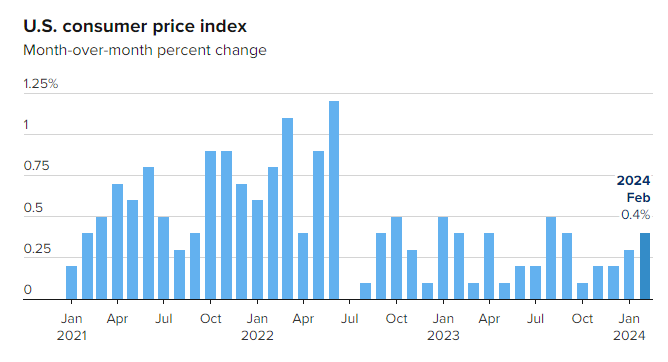

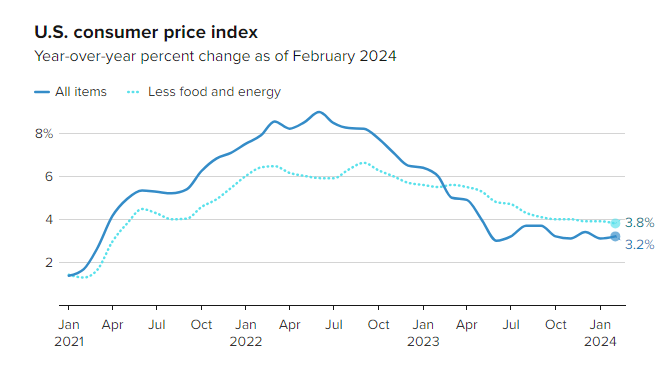

The U.S. Consumer Price Index, a comprehensive gauge of the cost of goods and services, rose by 0.4% for the month and increased by 3.2% compared to the previous year.

The annual rate was marginally higher than expected. The monthly rate was slightly above the forecast of 0.3%. This may likely direct the Federal Reserve to hold off on an interest rate reduction, at least until the summer of 2024. What will Wall Street make of it?

The core Consumer Price Index increased by 0.4% monthly and recorded an annual rise of 3.8%. Both figures exceeded forecasts by one-tenth of a percentage point.

An increase of 2.3% in energy costs contributed to the rise in the overall inflation figure. Food prices remained mostly unchanged for the month, while housing expenses saw a further increase of 0.4%.

U.S. consumer price index data for February 2024– Month on month

U.S. consumer price index data for February 2024 – Year on year

UK chancellor Jeremy Hunt revealed the British ISA as part of the Spring Budget 2024.

The British ISA aims to boost demand for UK businesses and encourage investment in UK-focused assets.

Key Features

Additional Allowance

The British ISA provides a separate £5,000 annual allowance in addition to the existing £20,000 ISA allowance.

Tax Advantages

Like other ISAs, investors in the British ISA will not pay tax on capital gains or income.

Investment Focus

While it’s not yet clear whether the new ISA will be exclusively for UK shares, it is expected to support UK-focused funds and investment trusts.

Eligibility Uncertainty

The inclusion of UK gilts or UK corporate bonds remains uncertain.

Consultation Period

The consultation period for the British ISA runs until June 6, 2024.

Potential Impact – Reviving UK Stock Market

The British ISA aims to revive interest in the UK stock market, which has faced challenges since the Brexit vote in 2016.

Supporting UK Companies

By providing tax-free savings opportunities, the ISA encourages investment in UK businesses.

Fund Industry Support

Fund management firms, including Premier Miton, lobbied for the British ISA’s creation.

Historical Context

The British ISA draws parallels with its predecessor, the personal equity plan (PEP), which focused on UK shares and funds.

ISAs replaced PEPs in 1999.

Conclusion

In summary, the British ISA introduces an additional allowance for UK-focused investments, supporting savers and UK companies alike. Its impact on the stock market and investor sentiment remains to be seen, but it represents a step toward bolstering the UK’s economic landscape

By ensuring that companies are valued fairly, a stronger stock market will facilitate the capital raising process for companies that seek to grow and attract more listings. This will have a positive impact on the economy and employment and is ultimately in everyone’s interest.

According to the revised official data, the Japan’s gross domestic product (GDP) grew by 0.4% in the fourth quarter of 2023 compared to the same period in the previous year.

According to this revision, the economy avoided a technical recession, which is usually defined as two successive quarters of negative growth.

On Monday 11th March 2024, Japan’s Cabinet Office released figures that indicated a 0.3% decline in private consumption for the quarter. Private consumption accounts for about 60% of the economy.

Nevertheless, the updated figures fell short of expectations, as some economists had predicted a higher revision in Q4.

In his Capitol Hill testimony on 6th March 2024, Federal Reserve Chairman Jerome Powell reiterated that was not yet time to begin cutting interest rates.

To fight inflation, which reached a rate of 9% in the summer of 2022, the central bank has significantly increased interest rates in recent times. However, prices are still stubborn, especially for things like housing and groceries.

Due to the robust economic performance in early 2024, the expected reduction in interest rates has been postponed. Instead of taking place this month, the rate cuts are now more probable in May or June 2024.

Powell reportedly said: ‘The Committee does not expect that it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.’

He reiterated the pledge to lower inflation to the 2% target and keep long-term inflation expectations stable.

UPDATE

On Thursday 7th March 2024 Powell also said: the Fed is ‘not far’ from the point of cutting interest rates

The U.S. national debt has been growing more quickly in recent months, increasing about $1 trillion nearly every 100 days.

U.S. debt permanently crossed over $34 trillion on 4th January 2024 according to data from the U.S. Department of the Treasury.

It reached $33 trillion on 15th September 2023, and $32 trillion on 15th June 2023. Before that, the $1 trillion move higher from $31 trillion took about eight months.

The U.S. national debt is the total amount of money that the federal government owes to its creditors. That can include, individuals, other countries and corporation. It is composed of two main components: federal debt held by the public and federal governmental debt.

The national debt has grown over time due to various factors, such as recessions, defense spending, and tax cuts. The debt-to-GDP ratio gives insight into whether the US has the ability to cover all of its debt. It also shows how it affects economic growth.

U.S. national debt pile is growing

U.S. national debt is piling up

The national debt increased by 13.3% under President Biden. Up from $27.77 trillion as of 1st March 2020 to $31.46 trillion as of 1st March 2023. The debt also grew by $1.5 trillion, or 5.6%, between the end of 2020 and the end of 2021.

The gross domestic product (GDP) measures the annual economic output of the entire country. The national debt exceeds this amount, which is very high.

As of the end of February 2024, the U.S. debt is almost $34.4 billion. This is the money that the federal government has to borrow to pay for its operating expenses.

The World Bank found that if the debt-to-GDP ratio exceeded 77% for an extended period, it slowed economic growth.

Euro zone inflation eased to 2.6% in February figures showed on Friday 1st March 2024, but both the headline and core figures were higher than expected.

Core inflation

Core inflation, removing the volatile elements of energy, food, alcohol and tobacco was 3.1% above the 2.9% rate expected.

The February figures will be a headache for EU policymakers, as core inflation is still holding above 3% even as the headline rate moves toward the ECB’s 2% target.

India is ‘easily’ the fastest growing economy in the world according to the IMF, as the country’s Q3 GDP growth soared past analysts’ estimates.

The world’s fastest growing major economy expanded 8.4% in the last three months of 2023.

8.4% GDP growth in Q3

At 8.4%, India’s economy expanded at its fastest pace in six quarters, data showed late Thursday, on strong private consumption and upbeat manufacturing and construction activity. Reuters estimates had pegged growth in the October to December period at 6.6%.

Prime Minister Narendra Modi posted on the social media platform X, that it shows ‘the strength of Indian economy and its potential.’

India economy due to jump ahead of Japan and Germany

India is forecast to leap ahead of Japan and Germany as the world’s third biggest economy in the next few years.

The better-than-expected growth was led by a strong performance by the country’s manufacturers, with the sector expanding by 11.6% in the period.

Private consumption, which makes up almost two-thirds of the country’s gross domestic product (GDP), also rose by 3.5%.

U.S. inflation climbed in line with expectations in January 2024, according to the preferred measure the Federal Reserve uses to make decisions on cutting interest rates.

The personal consumption expenditures (PCE) price index, excluding food and energy costs, increased 0.4% for the month and 2.8% from a year ago, as expected according to analyst’s predictions.

Headline PCE, including the volatile food and energy categories, increased 0.3% monthly and 2.4% on a 12-month basis according to the numbers released Thursday 29th February 2024 by the Commerce Department’s Bureau of Economic Analysis.

The data was released amid an unexpected jump in personal income, which rose 1%, well above the forecast for 0.3%. Spending decreased 0.1% vs. the estimate for a 0.2% gain.

Japan’s Nikkei 225 hit a record high of: 39098 on Thursday 22nd February 2024.

The rally was propelled by electronics, banking and consumer stocks as robust earnings and investor-friendly measures fuel a blistering rally in Japanese equities.

The Nikkei 225 jumped 2%, surpassing the previous record high of 38,915.87 reached in 1989.

Standout performance

Both the Nikkei and the broader Topix have been standout performers in Asia up more than 10% so far in 2024 after surging more than 25% in 2023. Their best annual gains in at least a decade.

Japan Inc’s solid third-quarter corporate earnings have prompted Bank of America analysts to upgrade their 2024 year-end forecasts for the Nikkei 225 to 41000 from 38500. They raised their forecasts for the Topix to 2,850 from 2,715.

The rally has also been supported by a weaker yen.

The U.K. logged a record £16.7 billion net budget surplus in January 2024, according to official figures released on Wednesday 21st February 2024

The Office for National Statistics noted that the country’s public finances usually run a surplus in January, unlike during other months, as receipts from annual self-assessment tax returns come in.

Combined self-assessment income and capital gains tax receipts totaled £33 billion in January, the ONS noted, down £1.8 billion from the same period of last year.

Total government tax receipts came in at a record £90.8 billion, up £2.9 billion compared to January 2023.

Government borrowing during the financial year spanning to the end of January 2024 was £96.6 billion, £3.1 billion lower than over the same 10-month period a year ago and £9.2 billion lower than the £105.8 billion previously forecast by the independent Office for Budget Responsibility.

That’s the fear spreading through Wall Street as another inflation reading on Friday 16th February 2024 came in hotter-than-expected.

The producer price index rose 0.3% in January 2024. The largest increase since August 2024 and higher than the 0.1% forecast. Excluding food and energy, core PPI jumped 0.5%, again well above consensus.

Stubborn

It is yet another sign of stubborn price pressures across the broader U.S. economy. And it came just days after an unexpectedly hot CPI reading, which gave markets a nasty jolt.

Both data have stoked investor worries on whether inflation is firmly under control. The latest developments also reinforce the Fed’s caution that it will need to see more evidence of disinflation before committing to lower rates.

Mohamed El-Erian, Allianz chief economic advisor, posted on X that like the CPI data, the PPI report was a further indication that the last mile of the inflation battle is more complex than many had assumed (and still assume).

Some economists even argue the jump in Friday’s data will likely push January’s personal consumption expenditures price index, the Fed’s preferred inflation gauge.

The PPI data means we can finalise our core PCE forecast for January, at 0.32%. That would be the biggest increase since September. But the three months since then all saw much smaller gains.

But investors will have to wait until later this month for PCE data when it’s released on 29th February 2024.

Retail sales rebounded in January as shoppers went on a determined spending spree, latest figures show.

ONS figures revealed a 3.4% jump in sales following a drop in December 2023.

Food sales at supermarkets rose strongly while department stores reported a good impact from January sales.

The Office for National Statistics (ONS) said that the value of goods people bought in January went up 3.9%, compared to the 3.4% increase in the volume of products purchased.

Inflation, which measures the pace of price rises, has slowed significantly but at 4% it remains higher than the Bank of England’s (BoE) 2% target.

Sales increased across nearly all retail sectors, and it was a particularly strong month for supermarkets according to the ONS.

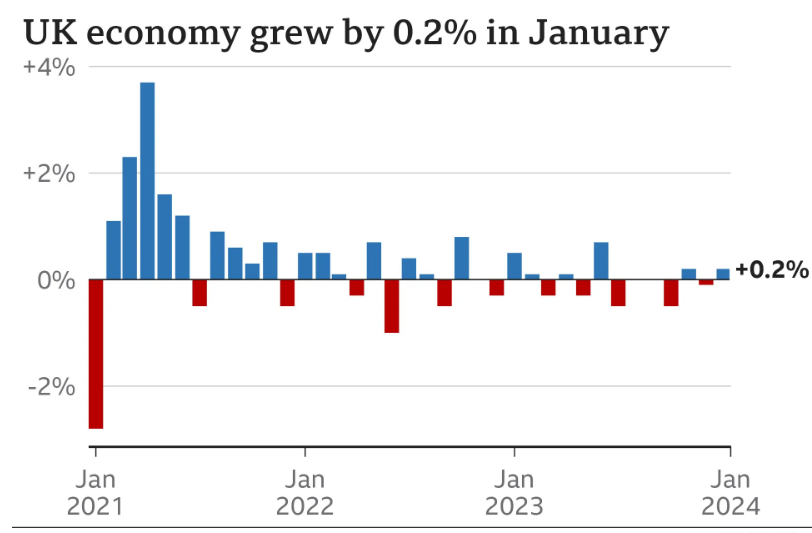

The UK fell into recession during the final three months of 2023, official figures show, after the economy shrank by more than expected.

The Office for National Statistics said U.K. gross domestic product shrank by 0.3% in the final three months of the year, giving the second consecutive quarterly decline.

That follows a fall between July and September 2023. The UK is considered to be in recession if GDP falls for two successive three-month periods.

All three main sectors of the economy contracted in Q4, with declines of 0.2% in services, 1% in production and 1.3% in construction output, the ONS reported.

Technical recession

A technical recession is a term used to describe two consecutive quarters of decline in output. It is measured by the Gross Domestic Product (GDP), which is the overall output of goods and services in a country.

A ‘technical’ recession is usually caused by slowing growth or an isolated event rather than a major underlying cause.

Japan’s economy slipped into a technical recession, after the economy unexpectedly contracted again in the October-December 2023period, government data showed Thursday 15th February 2024.

High inflation affected domestic demand and private consumption in what’s now the world’s fourth-largest economy.

Provisional gross domestic product contracted 0.4% in the fourth quarter compared with a year ago, after a revised 3.3% slump in the July-September period. This was below the estimate of a 1.4% growth.

The Japanese economy also contracted 0.1% in the fourth quarter from the previous quarter, after shrinking a revised 0.8% in the Q3. This was also weaker than the expected 0.3% expansion.

Nikkei one year chart to 15th February 2024

Nikkei one year chart to 15th February 2024

Japan has lost its spot as the world’s third-largest economy to Germany, as the country unexpectedly slipped into recession.

Technical recession

A technical recession is a term used to describe two consecutive quarters of decline in output. It is measured by the Gross Domestic Product (GDP), which is the overall output of goods and services in a country.

A technical recession is usually caused by slowing growth or an isolated event rather than a major underlying cause.

The UK’s inflation rate remained at 4% in January 2024, despite the first monthly fall in food prices in two years, ONS figures show.

January U.K. inflation held steady at 4% year-on-year benefitting from easing prices for furniture and household goods, food and non-alcoholic beverages.

According to the latest figures from the Office for National Statistics (ONS), prices for food and non-alcoholic beverages fell on a monthly basis by 0.4%, marking the first decrease since September 2021.

The core CPI figure excluding volatile food, energy, alcohol and tobacco prices annual reading was 5.1%, below the 5.2% estimate – but only a micro 0.1% difference.

The latest inflation data is a reflection of what is happening in the labour market: a tight labour supply is sustaining high wage growth and thus underlying inflationary pressure.

Stocks dropped on Tuesday 13th February 2024 after hotter-than-expected inflation data for January caused Treasury yields to spike

The new inflation figure raised doubts that the Federal Reserve would be able to cut rates several times this year, a key part of the equity market bull run case.

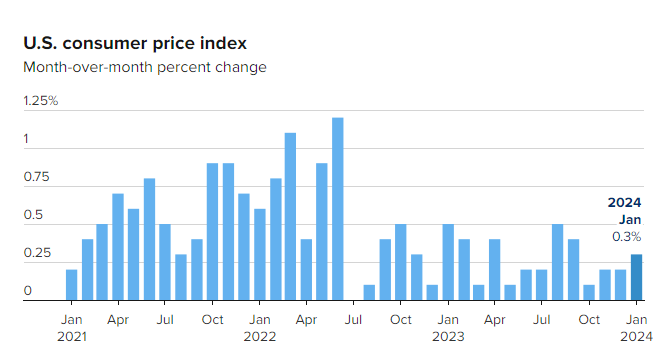

The consumer price index rose 0.3% in January 2024 from December 2023. CPI was up 3.1% year-to-year. Economists expected CPI to have increased by 0.2% month over month in January and 2.9% from a year earlier.

U.S. inflation ticks back up in January 2024 figures

The S&P 500 climbed to a new all-time high of 5026 on 9th February 2024

Stocks rose on Friday 9th February 2024 after December’s revised inflation reading came in lower than first reported, and the S&P 500 closed above the key 5,000 level as strong earnings and economic news came in.

A solid earnings season, easing inflation data and a resilient economy have charged 2024′s market rally. It propelled the S&P 500 to close above the 5,000 level after first touching the milestone during the trading week. The index first crossed 4,000 in April 2021.

We are enjoying good news at an economic and earnings level, and the market is reacting positively. The longer the good news story plays out, the more likely it will be that the market will hold from here.

But it won’t take much to spoil the party, right now I don’t know what that might be…?

S&P 500 1-year chart 9th February 2024 – new all-time high of 5026

S&P 500 1 year chart 9th February 2024 – new all-time high of 5026

FOMO or the fear of missing out is likely playing its part here too.

After a decade-long bull run throughout the 1980’s, the Nikkei 225 index reached an all-time high of 38,915 on December 29, 1989, the last trading day of the year.

Few could have imagined, on New Year’s Eve of 1989, that the index would be lower 34 years later. As the New Year arrived, the bubble burst.

And now, Japan’s stock markets are on a tear and closing in on that elusive 38195 high of 1989 – but there’s a catch – the Zombies are coming.

Zombie companies

Zombie firms are businesses that are unprofitable and struggling to keep afloat. They don’t have excess capital to invest and grow the business, or to pay down the loan capital.

Concerns about zombie firms are coming into focus as the Bank of Japan is tipped to raise interest rates in 2024 for the first time since 2007.

It comes as the Nikkei 225 rises to its highest point in almost 34 years

Japan’s stock markets have been on a meteoric run since the start of 2023, repeatedly breaching 33-year highs and outperforming the rest of Asia.

However, there are rising concerns that so called ‘zombie’ firms, which are unprofitable and struggling to keep afloat, could cut short that rally. The Bank of Japan is widely expected to raise interest rates this year, and that could easily tip many of these firms into bankruptcy, which could have a broader impact on the economy and stock market,

Nikkei 225 1-year chart 9th February 2024

Nikkei 225 1-year chart 9th February 2024

Bankrupt businesses

Zombie firms are nothing new in Japan. They first emerged after the stock ‘bubble’ and subsequent crash of the 1990s, when banks continued to support companies that would have otherwise gone bankrupt.

The pandemic of 2020 accelerated the problem of zombie businesses, with the number of zombie firms in Japan reportedly jumping by around 33% between 2021 and 2022.

At the end of 2023, Japan reportedly had around 250,000 companies that are technically zombie businesses

Some experts argue that zombie firms are a drag on Japan’s productivity, innovation, and growth, as they occupy resources and crowd out more efficient firms. The debate on how to deal with zombie firms is ongoing and may have implications for Japan’s economic recovery and future prospects.

Others suggest that zombie firms may have a positive effect, such as preserving employment, social stability, and industrial diversity.

Surely, there is no room for inefficiently run businesses making little or no profit in any economy.

U.S. stocks have had a good year in 2023, and a great start to 2024 with new record highs being set.

Many major indices have recorded double-digit gains. However, some analysts have warned that the rally may not last, as it has been driven by a few large-cap technology and growth stocks, while many other sectors and regions have lagged behind.

A stock market rally is a broad and rapid rise in share prices, often defined as a 20% increase from a recent low.

This could indicate a lack of breadth and sustainability in the rally, and potentially signal a market pullback, correction or even a crash in the future.

Bull bear, bull?

Chartists with their technical analysis might see a pattern that points to a substantial upside, but they should not get too carried away with their own observations, right now would be a sensible time for markets to find level ground, if only temporarily.

The bullish view is that the ‘laggards’ should catch up the ‘mega cap’ stalwarts once again. The bearish view is that the ‘mega cap’ stocks’ will realise they’ve gone too far and need to ride back to the rest of the market. Too few stocks in the same sector hold the balance of power – go check out the Magnificent 7 or even the old FANG stocks.

Catch-up

Either way, there ought to be an opportunity for underrepresented sectors and industries to gain lost ground.

The question is, will there be a pause to allow laggards to catch-up, or will the mega caps simply continue on their march?

The S&P 500 climbed again Wednesday 7th February 2024 and edged ever closer to the 5,000 level.

S&P 500 hit a new high of 4995

S&P 500 hit a new high of 4995 on 7th February 2024

The index, which first breached the 4,000 level in April 2021, added around 0.82% to close at 4,995.06. During session highs, the S&P hit 4,999.89. Quarterly results signalled a thriving U.S. economy.

The Nasdaq 100 jumped to a new high of 15,755

The Nasdaq 100 jumped to a new high of 15,755 on 7th February 2024

The Dow Jones Industrial Average rallied 156 points to close at 38,677 and an all-time high

DJIA closes at new high of 38677on 7th February 2024

Euphoric

Are investors getting swept away with the latest wave of AI related tech results? Quite possibly, as some of what we’re seeing could be based on FOMO (fear of missing out) as traders/investors don’t want to be left behind like they were last year.

However, one undeniable fact is that the U.S. economy isn’t facing as recession any time soon as predicted by many.

Job creation in the U.S. surged in January 2024, as the economy continued to defy predictions of a slowdown

The U.S. economy added 353,000 jobs and average hourly pay jumped, while the unemployment rate held steady at 3.7%, the Labour Department said.

The report extended more job gains that has surprised economists, who have expected a jump in interest rates since 2022 to slow the economy. It hasn’t. No recession or slowdown in the economy so far.

Early rate cut less likely according to these figures

Average hourly earnings increased 0.6%. Year-on-year basis, wages jumped 4.5%, above the 4.1% forecast.

Non-farm payrolls expanded by 353,000 for the month, well above the 185,000 estimate. The unemployment rate held at 3.7%.

Job growth was widespread in January 2024. Professional and business services 74,000. Other sectors included health care 70,000 and retail trade 45,000.

Analysts now say the job market gain and strength make an early interest rate cut less likely.

The U.S. employment data delivered quite a shock, easily beating expectations, with earnings much higher than expected. Stock markets gained and are at elevated levels for the Dow, Nasdaq and the S&P 500. Record highs have been set – are the highs?

Market analysts said these numbers show the U.S. economy is strong and will change the mindsets of those expecting an early interest rate cut.

Expectations of a recession are off the table too, for now.

The world is looking at a debt crisis that will span the rest of this decade and well into the next

$307.4 trillion of world debt!

It’s not going to end well; economists warn with global borrowings hitting a record of $307.4 trillion in September 2023.

Debt at this level is unsustainable.

Both emerging markets and high-income countries have seen a substantial rise in their debt levels. These levels have grown by a some $100 trillion from 10 years ago. The debt has been fueled in part by a higher interest rate environment.

Initially, with borrowing costs at historic lows, countries have benefitted from very low interest rate for the debt. That’s changed.

The next 10 years will likely become known as the ‘Decade of Debt.’

Debt globally is coming to a head.

As a share of the global gross domestic product, debt has risen to 336%. This compares to an average debt-to-GDP ratio of 110% in 2012 for advanced economies, and 35% for emerging economies.It was 334% in the fourth quarter of 2022, according to the most recent global debt monitor report by the Institute of International Finance.

To meet debt payments, it is estimated that around 100 countries will have to cut spending on critical infrastructure including health, education and social projects.

Countries that manage to improve their fiscal situation could benefit by attracting capital, labour and investment. However, those that do not could lose talent and revenue and further increase their debt burden.

In January 2024, inflation logged its biggest monthly jump since August with a 6.7% rise from December 2023.

Year-on-year inflation hit nearly 65%, according to the Turkish Central Bank’s figures released Monday 5th January 2024

The consumer price index (CPI) for the country of 85 million people increased by 64.86% annually, up slightly from the 64.77% of December.

Sectors with the largest monthly price rises were health at 17.7%, hotels, cafes and restaurants at 12%, and miscellaneous goods and services at just over 10%. Clothing and footwear were the only sectors showing a monthly price decrease, with -1.61%.

Food, beverages and tobacco, as well as transportation, all increased between roughly 5% and 7% month-on-month, while housing was up 7.4% since December 2024.

Federal Reserve Chair Jerome Powell said in a U.S. TV interview on Sunday 4th January 2024 that the central bank will proceed carefully with interest rate cuts this year and likely will move at a considerably slower pace than the market expects.

Election year rate cuts?

In the interview and after last week’s Federal Open Market Committee meeting (FOMC), Powell expressed confidence in the economy. However, he promised he wouldn’t be swayed by this year’s presidential election and said the pain he feared from rate hikes never really materialised.

“With the economy strong like that, we feel like we can approach the question of when to begin to reduce interest rates carefully,” he reportedly said.

“We want to see more evidence that inflation is moving sustainably down to 2%,” Powell added. “Our confidence is rising. We just want some more confidence before we take that very important step of beginning to cut interest rates.”

Powell indicated that it was unlikely the FOMC will make that first move in March 2024, which markets have been anticipating.

Gold demand hit record highs in 2023 on the back of persistent geopolitical tensions and continued weakness in some world economies, particularly China according to the World Gold Council.

Total gold demand stood at 4,899 tons in 2023 compared to 4,741 tons in 2022. Gold purchases from central banks led to last year’s surge, with purchases exceeding 1,000 tons for two consecutive years.

Prices reached an all-time high of around $2,135 an ounce in December 2023 as central banks and retail buyers increased their gold investments.

Carats at Costco

Buyers have many outlets from which to make their gold purchases. Costco recently reported selling over $100 million worth of gold bars in the final quarter of December 2023. Weird to think that we can now buy carats with carrots.

Gold bars for sale at Costco

Gold demand in 2024?

According to some analysts’ gold purchases this year are unlikely to meet 2023 levels, but a fall in inflation could prevent a drastic drop in demand.

When inflation drops significantly, consumers will start to feel ‘better-off’, and this could mitigate some of the drop in demand.

Gold carat

A Gold carat is a unit used to measure the purity of gold, with a carat representing 1/24th part of the whole.

Pure gold is 24 carats, meaning that it is 100% gold with no other metals added. However, gold used for jewellery and other applications is rarely pure, and its purity is measured in carats to determine its value.