The phrase ‘everything bubble‘ has gained traction among investors and commentators who fear that multiple asset classes in the United States are simultaneously overvalued.

Unlike past episodes where excess was concentrated in one sector—such as technology in the late 1990s or housing in the mid‑2000s—the current concern is that equities, property, and credit markets are all inflated together, leaving little room for error.

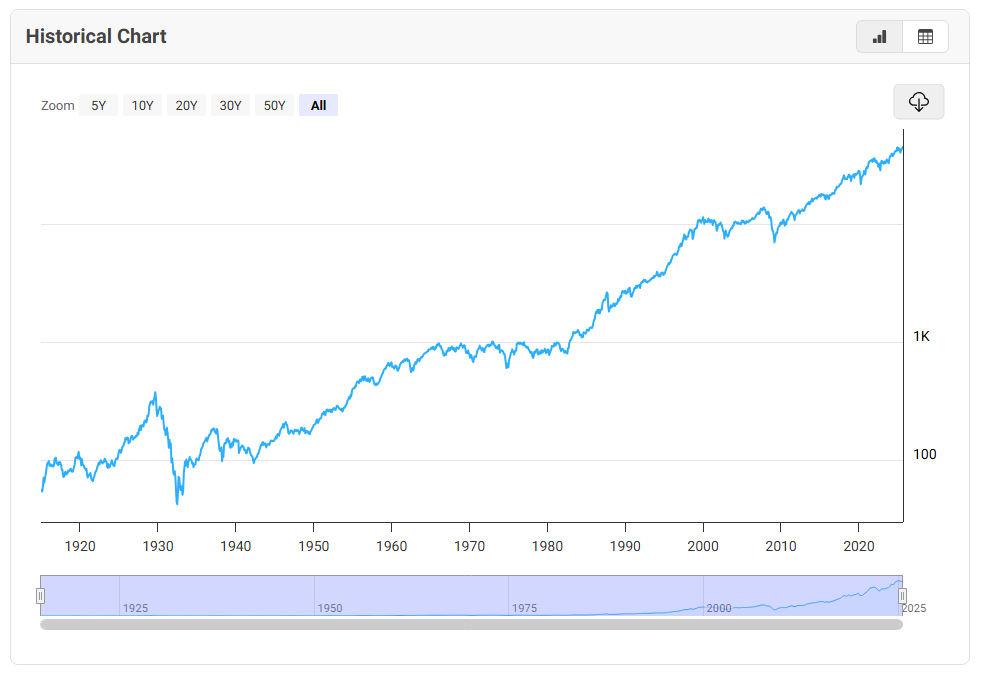

Equities are the most visible part of the story. Major U.S. indices have surged to record highs, driven by enthusiasm for artificial intelligence, cloud computing, and digital infrastructure.

Valuations in leading technology firms are stretched, with price‑to‑earnings ratios far above historical averages. Critics argue that investors are extrapolating future growth too aggressively, while ignoring the risks of higher interest rates and slowing global demand.

Market breadth has also narrowed, with a handful of companies accounting for most of the gains, a pattern often seen before corrections.

Housing

Housing provides another layer of concern. Despite higher mortgage rates, U.S. home prices remain elevated, supported by limited supply and strong demand in metropolitan areas.

This resilience has surprised analysts, but it also raises the question of sustainability. If borrowing costs remain high, affordability pressures could eventually weigh on the market, exposing households to financial stress.

Credit markets

Credit markets add a third dimension. Corporate debt issuance has slowed, and investors have become more selective, demanding higher yields to compensate for risk. Some deals have been pulled altogether, signalling caution beneath the surface.

When credit tightens, it often foreshadows broader economic weakness, as companies struggle to refinance or fund expansion.

Yet it would be simplistic to declare that everything is a bubble. The rapid adoption of AI and accelerated computing reflects genuine structural change, not mere speculation.

Demand for advanced chips and data centres is tangible, and some firms are generating real cash flows from these trends. Similarly, housing shortages are rooted in years of under‑building, suggesting that supply constraints, rather than speculative mania, are keeping prices high.

The truth may lie in between. U.S. markets are undeniably expensive, and vulnerabilities are widespread.

But not all sectors are equally fragile, and some are underpinned by lasting shifts in technology and demographics.

Investors should therefore resist blanket labels and instead distinguish between genuine transformation and speculative excess.

In doing so, they can navigate a landscape that is frothy in places, but not uniformly illusory.