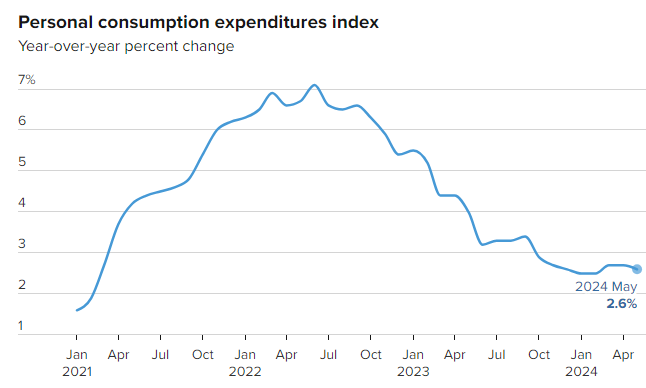

America’s latest inflation figures show price pressures proving far stickier than the Federal Reserve would like, with the core PCE index — the Fed’s preferred gauge — holding at 3% in February 2026.

Headline inflation came in slightly lower at 2.8%, but both measures remain well above the central bank’s 2% target.

What makes this reading particularly significant is its timing. The data captures the state of the economy just before the U.S. and Israel launched military action against Iran.

Energy chaos

A conflict that has since sent global energy markets into turmoil. Oil briefly surged past $100 a barrel, and U.S. petrol prices jumped by more than a dollar, none of which is reflected in February’s figures.

Beneath the surface, the numbers paint a mixed picture. Consumer spending rose 0.5%, suggesting households were still willing to open their wallets, yet personal income unexpectedly slipped 0.1%.

Stagflation?

Fourth‑quarter GDP for 2025 was revised down to a sluggish 0.5% annualised, reinforcing concerns that the U.S. may be drifting into a mild stagflationary phase — slow growth paired with persistent inflation.

Fed officials have been cautious in recent weeks, signalling openness to rate cuts later in the year but unwilling to commit while geopolitical risks and energy‑driven price spikes cloud the outlook.

With March’s CPI due imminently — and expected to show a sharp jump — policymakers face a narrowing path between supporting a cooling labour market and preventing inflation from becoming entrenched.

For now, the message is clear: underlying inflation was already proving stubborn before the shock of war.

The next few months will reveal whether the Fed can still engineer the soft landing it has been aiming for, or whether the global energy shock forces a rethink.