Fed Chair Jerome Powell reportedly said he and his colleagues remain steadfast in getting policy in line with their 2% inflation target, but ‘we are not confident that we have achieved such a stance’.

He stressed the Fed nevertheless can be cautious as the risks between doing too much and too little have come into closer balance.

Federal Reserve Chairman Jerome Powell reportedly said Thursday 9th November 2023 that he and his fellow policymakers are encouraged by the slowing pace of inflation but are unsure whether they’ve done enough to keep the momentum going.

Inflation battle

Speaking a little more than a week after the central bank voted to hold rates steady, Powell said in remarks aimed at the International Monetary Fund (IMF) gathering in Washington, D.C., that more work could be ahead in the battle against high prices.

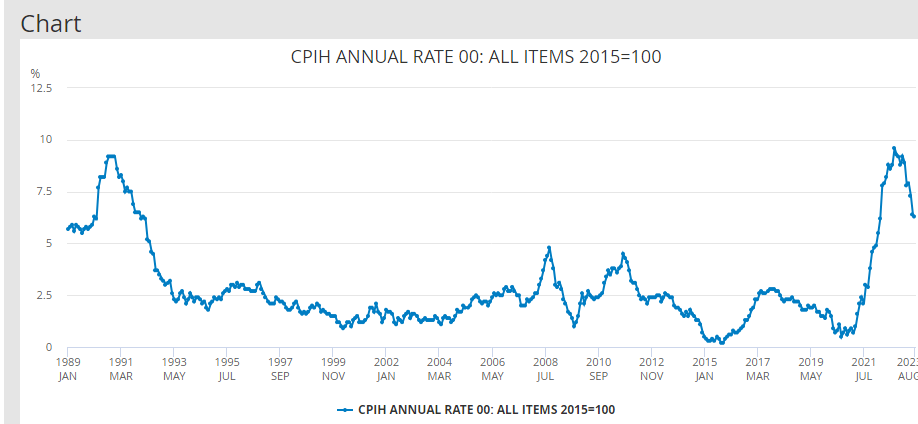

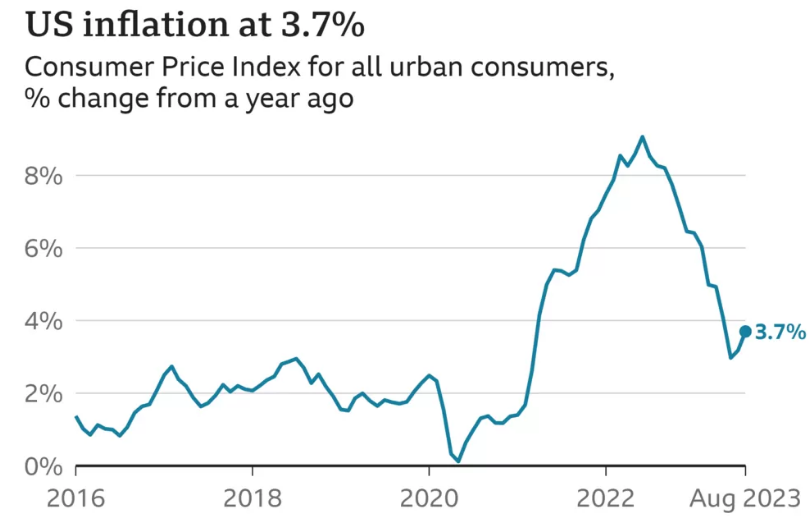

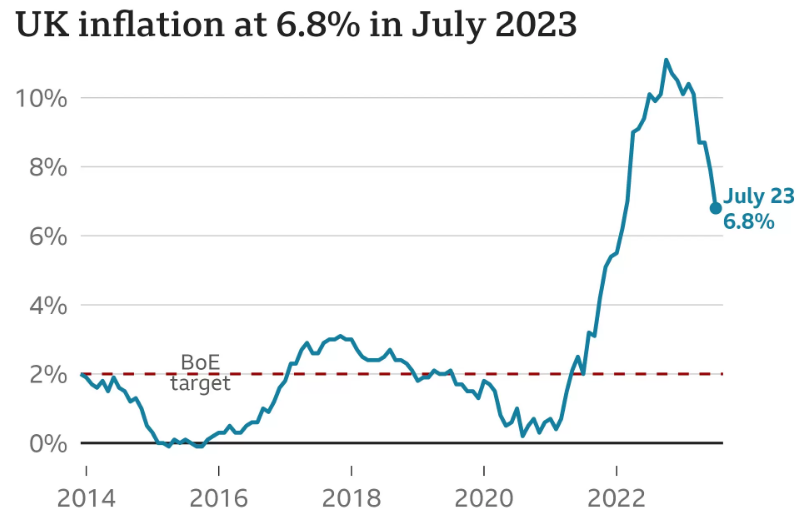

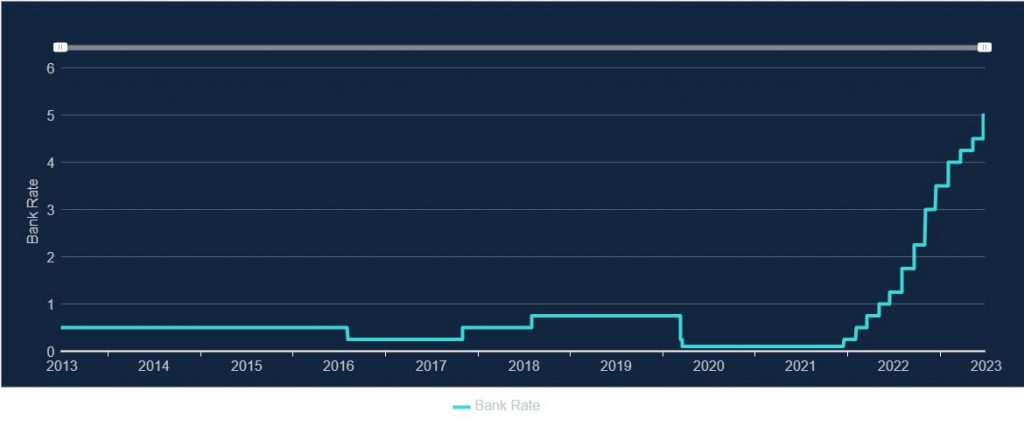

The statement comes with inflation still well above the Fed’s long-standing goal but also considerably below its peak levels in the first half of 2022. After 11 U.S. rate hikes, we have witnessed the most aggressive policy tightening since the early 1980s, the FOMC have increased rates from pretty much zero to a range of 5.25%-5.5%.

Those increases have coincided with the Fed’s preferred inflation gauge, the core personal consumption expenditures price index, to fall to an annual rate of 3.7%, from 5.3% in February 2022. The more widely followed consumer price index peaked above 9% in June of last year.

Progress

Powell referenced the progress the economy has made. Gross domestic product (GDP) accelerated at a ‘quite strong’ 4.9% annualised pace Q3 2023, though Powell also said the expectation is for growth to ‘moderate in coming quarters’. He described the economy as ‘just remarkable’ in 2023 in the face of a broad expectation that a recession was inevitable.

Nothing like a massive ‘self-pat’ on the back for a job well-done? Remember the Fed’s initial analysis? IT was for inflation to be ‘transitory’. They didn’t get that right either.

Futures pricing, according to the CME Group, suggested there’s less than a 10% chance that the FOMC will approve a final rate hike at its Dec. 12-13, 2023, meeting, even though committee members in September pencilled in an additional 0.25% rise before the end of 2023.

Traders anticipate the Fed will start cutting rates next year, probably around June 2024.