The debate over the dysfunction of international organisations has intensified in recent years, driven by a growing sense that institutions built for the post‑war order are struggling to operate in today’s fragmented global landscape.

Analysts note that many of these bodies now survive more through prestige than performance, with their ability to prevent conflict, enforce rules, or deliver meaningful global governance increasingly questioned.

Criticism

A central criticism is that organisations such as the UN, IMF, and various specialised agencies were designed for a world with clearer power structures and more limited public expectations.

Today’s environment—marked by empowered populations, rapid information flows, and complex transnational challenges—demands institutions that are more responsive, inclusive, and capable of decisive action.

Instead, many remain bureaucratic, state‑centric, and constrained by outdated governance models, leaving them ill‑equipped to address issues such as climate change, technological disruption, and inequality.

Weak Enforcement and Political Paralysis

A recurring theme in recent assessments is the weak enforcement capacity of these organisations. Without the ability to compel compliance, many bodies function more as forums for discussion than engines of action.

This has contributed to failures in peacekeeping, global financial regulation, and climate commitments.

Some institutions have even become part of the problem, with their directives blurring political accountability or reinforcing the interests of dominant powers rather than serving global needs.

Declining Relevance, Not Just Poor Performance

Research also suggests that while international organisations may not be collapsing in absolute terms, they are experiencing a relative decline in influence.

Mentions of these bodies in major diplomatic forums have fallen, indicating that states increasingly look elsewhere—regional blocs, ad‑hoc coalitions, or unilateral action—to solve problems.

This shift signals a reduced centrality of global institutions in international relations, even if they continue to exist structurally.

A System in Need of Renewal

Despite their shortcomings, international organisations remain vital for coordinating responses to global crises. Yet their funding models, governance structures, and enforcement mechanisms are widely seen as inadequate.

Scholars argue that without meaningful reform—or entirely new models of cooperation—these institutions risk further erosion of legitimacy and effectiveness.

The emerging consensus is clear: the world has changed, but its international institutions have not kept pace. Unless they adapt, their relevance will continue to fade, leaving a vacuum in global governance at a time when coordinated action is needed more than ever.

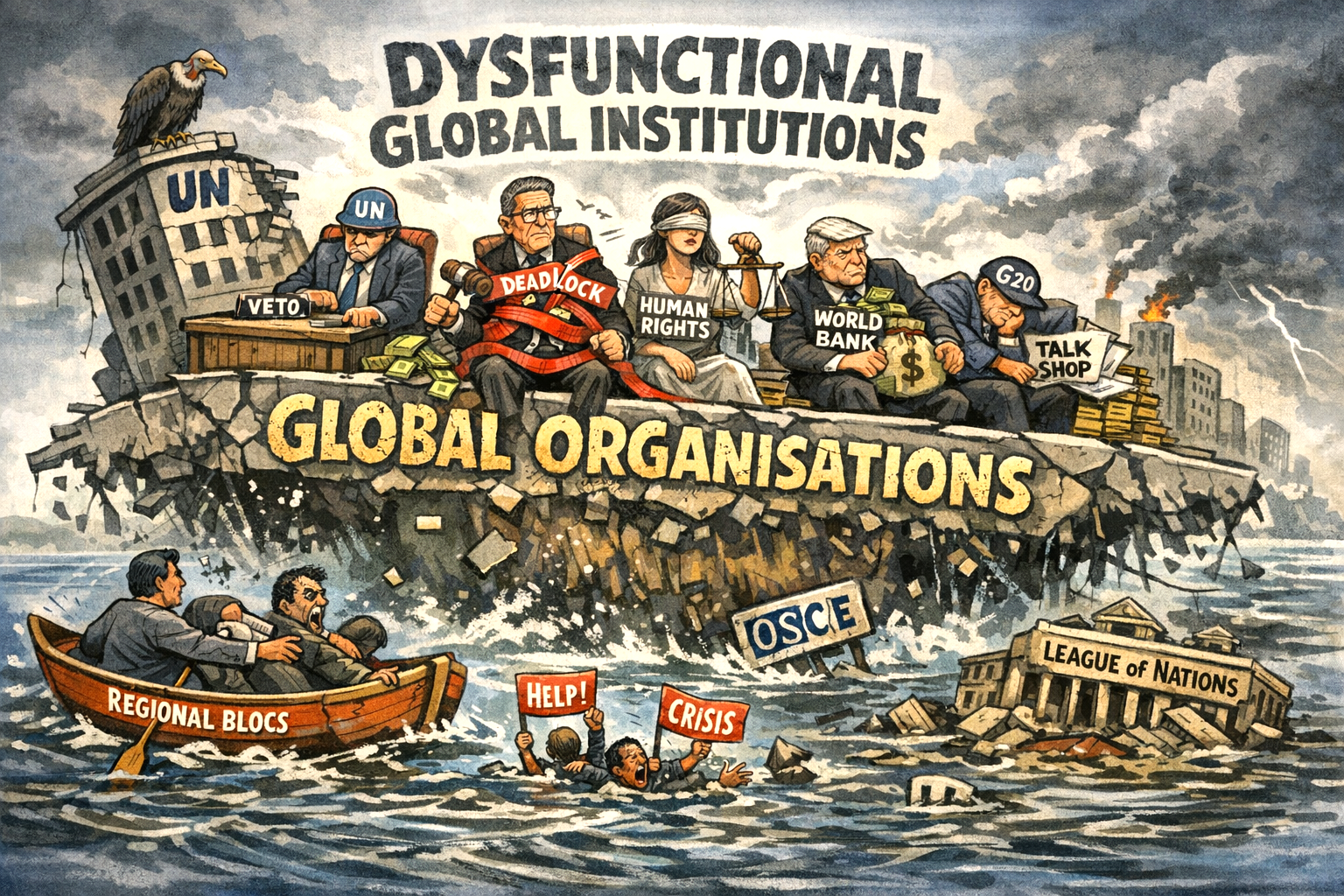

Top 12 Underperforming / Uderperforming / Threatened International Organisations

| Rank | Organisation | Why It Is Seen as Failing / Underperforming |

|---|---|---|

| 1 | United Nations (UN) | Has failed to prevent conflict; increasingly bureaucratic; survives more through prestige than performance; weak enforcement. |

| 2 | UN Security Council (UNSC) | Veto paralysis blocks action; structure frozen in 1945; unable to respond effectively to modern conflicts. |

| 3 | World Trade Organization (WTO) | Dispute system paralysed; states bypass it; too slow for modern trade cycles; struggles with major issues like subsidies and IP. |

| 4 | International Monetary Fund (IMF) | Criticised for austerity‑heavy loan conditions, governance dominated by wealthy nations, and poor crisis performance. |

| 5 | World Bank | Accused of favouring rich nations, slow response, harmful loan conditions, governance imbalance, and data manipulation scandals. |

| 6 | UN Human Rights System (incl. HRC) | Human rights in global retreat; institutions unable to prevent abuses or uphold universality; politicisation undermines credibility. |

| 7 | G20 | Increasingly a discussion forum rather than a decision‑making body; weak enforcement; limited real‑world impact. |

| 8 | UN Specialised Agencies (e.g., WHO, UNHCR) | Bureaucratic, slow to respond to crises, and constrained by limited enforcement power; often reactive rather than strategic. |

| 9 | OSCE (Organisation for Security and Co‑operation in Europe) | Struggles to prevent conflict or protect rights; effectiveness eroded by geopolitical tensions and consensus‑based paralysis. |

| 10 | African Union (AU) | Ambitious mandates but limited capacity; struggles with enforcement, peacekeeping, and coordination across diverse member states. |

| 11 | OAS (Organisation of American States) | Deep political divisions, declining legitimacy, and inability to manage regional crises effectively. |

| 12 | Legacy Organisations That Have Already Collapsed (e.g., League of Nations, International Refugee Organization) | Historical examples showing that major IOs can die when performance collapses and demand for cooperation disappears. |

Why these 12 rise to the top

Across the sources, several themes recur

- Failure to prevent conflict — especially the UN, UNSC, OSCE.

- Weak enforcement — many bodies function as talking shops rather than action‑driving institutions.

- Bureaucratic inertia — slow, rigid structures built for 1945, not 2026.

- Loss of relevance — states increasingly bypass global bodies for regional or “minilateral” arrangements.

- Prestige over performance — organisations persist because dismantling them is costlier than letting them drift.

- Power imbalances — dominant states shape outcomes; smaller states join to avoid losing prestige.

These criticisms are consistent across GIS Reports, Oxford Academic, Meer, New Eastern Europe, and contemporary political commentary.

And then there is NATO?