In February 2024, inflation decreased to 3.4%, a decline from January’s 4%, moving closer to the Bank of England’s self-imposed target of 2%

This reduction signifies that the cost of living is increasing at its least rapid rate since September 2021, when it was recorded at 3.1%.

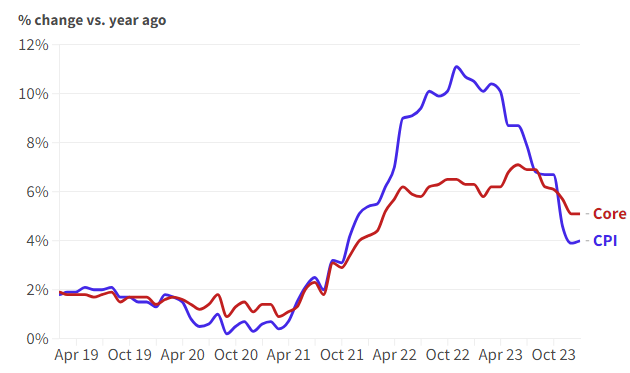

Since reaching a peak of 11.1% in October 2022, the highest in 40 years, inflation has been on a steady decline. In the big inflation picture, that’s a pretty good result.

It has only taken around 16 months to move the rate from 11.1% (a 40-year high) down to just 1.4% above the BoE’s target of 2%.

The primary factor contributing to this decrease, as reported by the Office for National Statistics (ONS), is the deceleration of food price inflation.

Inflation, rose marginally to 4% in December, up from 3.9% in November 2023.

Economists had forecast a slight fall but unexpected rises in alcohol and tobacco prices were behind the surprise rise.

However, with energy bills predicted to come down in 2024, there are still expectations of interest rate cuts later this year.

On target still for 2%?

As we have seen in the Germany, the U.S., and France, inflation does not fall in a straight line, ‘but our plan is working and we should stick to it,‘ Jeremy Hunt reportedly said in a statement.

UK inflation from April 2019 to December 2023

UK inflation from April 2019 to December 2023

Unprepared for both the start and the end of the pandemic

Increases in the cost of energy and food costs, started by pandemic lockdowns ending exasperated further by Russia’s invasion of Ukraine and more recently the conflict in Israel have put household finances under extreme pressure.

The UK and other countries were woefully underprepared for all of these events as they ‘began’ and at the ‘end’. We did not prepare to come out of them – there was no exit plan!

Markets and traders are still expecting BoE to cut its base rate in 2024 due to the fast-falling inflation rate. It peaked at 11.1% in October 2022 – and now sits at 4%.

The question is: will the economic recovery be good enough to allow the Bank of England to start cutting rates?

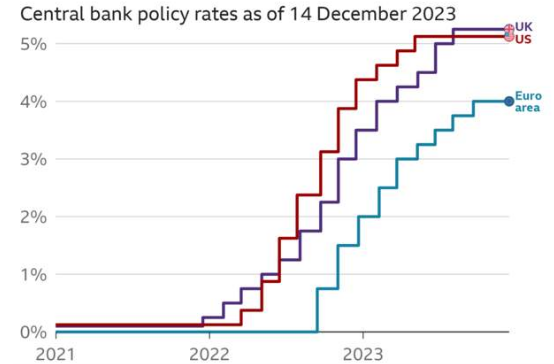

The UK interest rate currently sits at 5.25%.

‘What’s inflation?’ ‘Dunno, but my beer’s gone up!’

Mortgage lenders have started 2024 by cutting interest rates.

The UK’s biggest lender, the Halifax, has cut some interest rates by nearly a full 1%, with other lenders expected to follow suit. HSBC has announced it will also make cuts in January.

Halifax is reducing its rates, with interest on a two-year fixed deal being cut by up to 0.83%. HSBC is due to reduce rates on its two-year fixed rate for remortgages (for someone with at least 40% equity in their home) falling below 4.5% for the first time since early June last year.

Mortgage rate chart October 2021 – January 2024

The Bank of England’s (BoE) benchmark interest rate has been held three times at 5.25%, analysts now expect the next move to be down.

UK interest rates have been held at 5.25%. This is the third time in a row the Bank of England has opted to hold rates the same.

The decision, which was widely expected by financial markets, means borrowing costs will remain at their highest level for 15 years.

the Bank of England’s Monetary Policy Committee (MPC) voted 6-3 to keep rates at a 15-year high.

There was reportedly no discussion of cutting interest rates, and it’s still concerned that price rises might be stickier in the UK economy than in the U.S. or Eurozone.

The U.S. yesterday, 13th December 2023 indicated that 2024 could see three interest rate cuts. No such indication was forthcoming from the UK.

Britcoin is a potential British digital currency that would be issued by the Bank of England and backed by the Government.

It would be tied to the pound and have a stable value, unlike cryptocurrencies such as Bitcoin. It would be accessible through digital wallets and interchangeable with cash and bank deposits. The Treasury and the Bank of England are consulting on its launch, which could take place by 2030.

Britcoin could be used for everyday transactions, both in-store and online, and could make payments more efficient and enable innovation. However, some MPs have warned that Britcoin could cause severe financial damage and undermine the role of banks.

Some MPs have warned that Britcoin could cause severe financial damage and undermine the role of banks for several reasons.

Concerns about introducing a digital pound

Britcoin could increase the chance of bank runs, if customers were able to quickly and easily switch their bank deposits into digital pounds, especially during times of financial stress or panic. This could reduce the liquidity and solvency of banks and make them more vulnerable to failure.

Britcoin could also raise the cost of borrowing for banks and consumers, as banks would need to replace the funding that they would lose from deposits with more expensive sources. The Bank of England estimated that if 20% of bank deposits turned digital, it could result in a rise in interest rates on commercial loans.

Britcoin could pose risks to data privacy and security, as the government or third parties could potentially access, track, or control how users spend their digital funds. This could raise ethical and legal issues and require robust regulation and protection.

Britcoin could also have unintended consequences on the wider economy and society, such as affecting monetary policy, financial inclusion, innovation, and competition. The MPs said that the benefits and costs of Britcoin should be clearly evidenced before any decision is taken to introduce it.

Art illustration: Digital £ pound proposal – Britcoin

The development of a state-backed ‘digital pound’ should proceed with caution, MPs have warned.

The benefits of the currency are still unclear and there must be systems in place to protect cash access and privacy, the Treasury Committee said in a report.

The Bank of England (BoE) and the Treasury have been consulting on the idea since February 2023. They are currently designing what such a system could look like. The CBDC would be directly issued by the Bank of England (BoE), just like banknotes.

This means people would have all the same safety and security that they have with their cash currently, which is different to cryptocurrencies that fluctuate in value and are generally run by private companies.

The governor of the Bank of England, Andrew Bailey has raised concerns over economic growth as he warned again that interest rates will not be cut in the ‘foreseeable future’.

The bank boss said he was concerned over the UK economy’s potential to grow. It comes after the government’s forecaster cut its growth outlook for the UK, due to high inflation, interest rates, energy and food price increases which were exacerbated by the Covid pandemic and Russia’s invasion of Ukraine.

Inflation, which is the rate consumer prices rise at, has dropped sharply in recent months, falling to 4.6% in the year to October largely as a result of lower energy prices.

However, it is still more than double the Bank of England’s 2% target and Mr Bailey warned lowering inflation further would be ‘hard work’.

Interest rates are currently at 5.25%, a 15-year high, which has pushed up borrowing and mortgage costs.

UK inflation fell to 4.6% in October 2023, down from 6.7% in September 2023.

This is the lowest rate of price increases since 2021 and the bigger than expected fall should provide some relief to UK households gripped by the cost-of-living crisis.

The main factors that contributed to the drop in inflation were largely due to lower energy prices, food and non-alcoholic drink prices, and airfares. Economists suggested that the main reason inflation fell from its peak of 11.1% in October 2022 was due to the fall in the energy price cap, which limits what suppliers can charge consumers per unit of energy.

However, the UK still has the highest inflation rate of any G7 country, and some economists warn that the Bank of England (BoE) may need to raise interest rates to prevent inflation from rising again.

Target hit

The UK government will no doubt rejoice today as the end-of-year 5% has been achieved earlier than expected. But don’t party too early, the actual target is 2%. There is a limit to how much credit ministers can take for the fall as energy prices settle.

The FTSE100 was happy, it climbed some 100 points in morning trade.

The Bank of England (BoE) announced its latest interest rate decision on Thursday, 2nd November 2023 to hold the bank rate at 5.25%.

The Bank of England’s (BoE) Monetary Policy Committee (MPC) voted by a majority of 5-4 to maintain Bank Rate at 5.25%, the highest level in 15 years. However, four members preferred to increase the bank rate, to 5.5%.

The MPC also voted unanimously to reduce the stock of UK government bond purchases held for monetary policy purposes by £100 billion over the next twelve months, to a total of £658 billion.

The BoE’s decision was influenced by the weak economic outlook, the high inflation rate, and the uncertainty surrounding the Covid-19 pandemic and the Brexit saga.

The BoE said that the UK economy was likely to contract by 0.5% in Q3 2023, and that underlying growth in the second half of 2023 was also likely to be weaker than expected. The BoE also warned that there was a 50% chance of a recession in the next year (50/50). I think even I could guess with odds at 50/50.

2% target inflation to be hit by Q2 2025

The BoE also said that inflation, which was 6.7% in September 2023, was expected to peak at around 7% in Q4 2023, before falling back to the 2% target by 2025 Q2. The BoE said that the inflation spike was largely driven by temporary factors, such as higher energy and food prices, and that it would not respond to it.

The Bank of England was behind the curve calling it transitory. Can we trust any future forecasts?

The BoE’s decision was in line with the market expectations, as most analysts and investors had predicted that the BoE would keep rates on hold.

The interest the government pays on national debt has reached a 20-year high as the rate on 30-year bonds touches 5.05%.

A rise in the cost of borrowing comes at a difficult time for the chancellor, Jeremy Hunt, as he prepares for the autumn statement on 22nd November 2023. The chancellor has already made clear that tax cuts will not be announced in the autumn statement.

National debt £2,590,000,000,000

The total amount the UK government owes is called the national debt and it is currently about £2.59 trillion – £2,590,000,000,000.

The government borrows money by selling financial products called bonds. A bond is a promise to pay money in the future. Most require the borrower to make regular interest payments over the bond’s lifetime.

UK government bonds – known as ‘gilts’ – are normally considered very safe, with little risk the money will not be repaid. Gilts are mainly bought by financial institutions in the UK and abroad, such as pension funds, investment funds, banks and insurance companies.

QE

The Bank of England (BoE) has also bought hundreds of billions of pounds’ worth of government bonds in the past to support the economy, through a process called quantitative easing or QE.

A higher rate of interest on government debt will mean the chancellor will have to set aside more cash, to the tune of £23 billion to meet interest payments to the owners of bonds. This in-turn means the UK government may choose to spend less money on public services like healthcare and schools at a time when workers in key industries are demanding pay rises to match the cost of living.

Double debt

The current level of debt is more than double what was seen from the 1980s through to the financial crisis of 2008. The combination of the financial crash in 2007/8 and the Covid pandemic pushed the UK’s debt up from those historic lows to where it stands now. However, in relation to the size of the economy, today’s debt is still low compared with much of the last century.

UK debt £2,590,000,000,000

The U.S, German and Italian borrowing costs also hit their highest levels for more than a decade as markets adjusted to the prospect of a long period of high interest rates and the need for governments around the world to borrow.

It follows an indication from global central banks, including the United States Federal Reserve and the Bank of England (BoE), that interest rates will stay ‘higher for longer’ to continue their jobs of bringing down inflation.

£111billion on debt interest in a year

During the last financial year, the government spent £111 billion on debt interest – more than it spent on education. Some economists fear the government is borrowing too much, at too great a cost. Others argue extra borrowing helps the economy grow faster – generating more tax revenue in the long run.

The Office for Budget Responsibility (OBR), has warned that public debt could soar as the population ages and tax income falls. In an ageing population, the proportion of people of working age drops, meaning the government takes less in tax while paying out more in pensions, welfare and healthcare services.

Services output was the main contributor to growth in August 2023, adding 0.4% on the month to offset a fall in production output of 0.7% and a decline in construction output by 0.5%.

This data shows early signs of a cooldown in the labour market and thus, lower inflation further down the economic road.

Bank outlook

The data and outlook for the Bank of England (BoE) suggests that Bank rate increases do not have much upside from here and will most likely remain at current levels, but for a longer period.

The UK economy returning to growth in August 2023 has re-kindled expectations that interest rates will be left unchanged again in Novemeber 2023.

The economy grew marginally by 0.2% in August following a sharp fall in July 2023.

UK interest rates have been left unchanged at 5.25% by the Bank of England (BoE).

The decision comes a day after figures revealed an unexpected slowdown in UK nflation in August 2023.

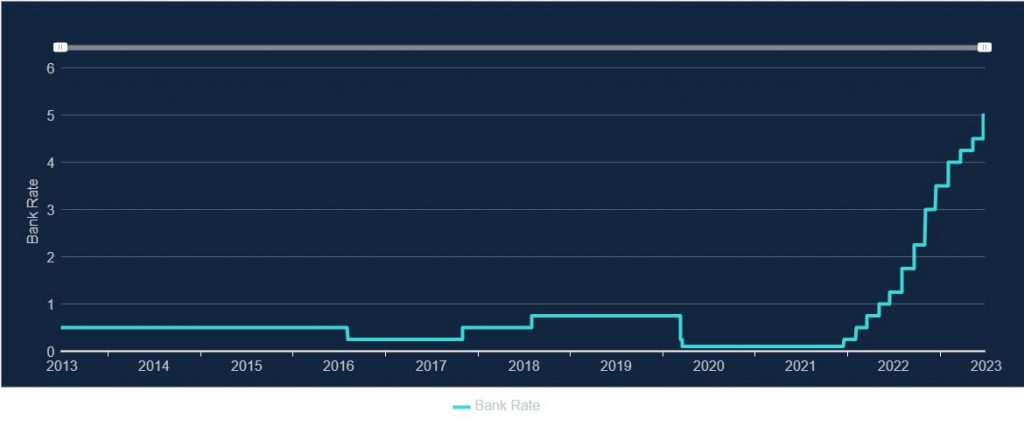

The Bank had previously raised rates some14 times in a row to tackle inflation, leading to increases in mortgage payments, business loans and consumer borrowing. But it also delivered higher savings rates.

Confidence in Bank of England (BoE) is a measure of how much the public trusts the central bank to control inflation, set interest rates and maintain economic stability.

According to the latest Inflation ‘Attitudes Survey‘ conducted by the Bank of England in August 2023, confidence in Bank of England has plummeted to an all-time low.

Survey

The survey found that only 19% of the respondents were satisfied with the way the Bank of England was doing its job to set interest rates to control inflation, while 40% were dissatisfied. The net satisfaction rate was -21%, which is the lowest since the survey began in 1999.

2% inflation please

The main reason for the low confidence is the high inflation rate that has been persisting in the UK for more than a year. Inflation reached a peak of 11.1% in December 2022, and was still at 6.8% in July 2023, well above the Bank of England’s target of 2%. The Bank of England has raised interest rates 14 times since the end of 2021, from 0.1% to 5.25%, to try to bring inflation down, but this has also increased the cost of borrowing and living for many households and businesses.

Slow

Some critics have argued that the Bank of England (BoE) acted too slowly and too cautiously to raise interest rates when inflation was rising, while others have warned that raising rates too high and too fast could harm the economic recovery from the Covid-19 pandemic.

The public’s expectations of future inflation are also high, with a median answer of 2.9% for inflation in five years’ time, almost one percentage point higher than the Bank’s target.

Credibility

Confidence in Bank of England (BoE) is important because it affects how people behave in terms of spending, saving, investing, and borrowing.

Bank of England hits all-time confidence low according to survey

Loss of faith

If people lose faith in the central bank’s ability to control inflation and maintain economic stability, they may act in ways that could worsen the situation, such as hoarding money, demanding higher wages, or taking on more debt.

Therefore, it is crucial for the Bank of England to communicate clearly and effectively with the public about its policies and actions, and to restore trust and confidence in its role as an independent and credible institution.

It is also useful to take notice of early warning signs, such as the economic red alert posed by inflation after the pandemic recovery started.

The value of UK mortgage arrears jumped by almost a third in April to June 2023 compared with the same period last year, according to the Bank of England (BoE).

Outstanding mortgage debt is now £16.9bn, the highest since 2016, it said.

Mortgage costs have risen for millions as the Bank has repeatedly hiked interest rates to slow soaring prices.

Some experts warn defaults will rise, but others say the number unable to repay remains relatively low.

According to the BoE, in April-June 16% of mortgages in arrears were new cases, which it said ‘was little changed compared to the previous quarter’.

It added that the proportion of mortgages in arrears was the highest since 2018.

The digital pound is a proposed new form of money that would be issued by the Bank of England and backed by the government. It would be similar to a digital banknote, enabling you to use it in-store or online to make payments.

It would not be intended to replace cash, but complement it. The digital pound is also known as digital sterling or Britcoin.

Bank of England and UK Government

The Bank of England and HM Treasury are looking at the idea of a digital pound because they think it might offer a new way to pay, help businesses, build trust in money, and better protect the UK’s financial system. They have published a Consultation Paper, which explores the need for the digital pound and proposes a set of design choices for it. They are also engaging with businesses and communities to get their views on the digital pound.

The digital pound is not a cryptocurrency or cryptoasset. Unlike cryptocurrencies, which have volatile values, the digital pound would be issued by the Bank of England and have a stable value, just like banknotes.

I promise to pay the bearer on demand the sum of £10.00

The digital £ is coming to a bank near you or more likely, an app near you

£10 in digital pounds would always have the same value as a £10 banknote.

The Nationwide Building Society says house prices are 5.3% lower compared to August last year, in the biggest annual decline since 2009.

Nationwide said the drop represented a fall of £14,600 on a typical home in the UK since house prices peaked in August 2022. It also said higher borrowing costs for buyers had led to a slowdown in activity in the housing market. Mortgage approvals are also about 20% below pre-Covid levels.

After 14 rate increases from the Bank of England – a two year fixed rate mortgage is now touching 6.7%

Since December 2021, the Bank of England (BoE) has raised interest rates 14 times in row in a bid to clamp down on rising inflation in the UK. The bank’s base rate now stands at 5.25%. This has led to lenders raising their mortgage rates, putting increased pressure on homebuyers.

The average two-year fixed mortgage rate on Friday was 6.7%, while the average five-year fix was 6.19%.

Average house prices in the UK peaked at £273,751 in August 2022 but fell to £259,153 last month.

The Bank of England’s forecasting, which has a major impact on the UK economy, is being reviewed and has been criticised.

After the Bank raised interest rates for a 14th time in a row in an effort to slow price rises in Augts 2023, officials have predicted inflation to fall from the current rate of 7.9%, to ‘around 5%‘ by the end of the year. The Bank puts rates up when they are concerned that too much spending will send prices spiralling.

So, in light of its estimating techniques being challenged, how much faith should we put in ‘5% by Christmas’?

For the last two years, the Bank of England has been underestimating the likely rate of inflation in the short term. MPs have been critical of the Bank’s forecast, and its officials have acknowledged they have got some judgements wrong in their forecasting.

The Central Bank has also announced a review into how it makes forecasts.

This was one of the questions put to the Bank of England governor

Mr Baron:Good morning, everyone. In looking at the bank rate going forward, some of us, it is fair to say, have long believed that central banks, including the Bank of England, have been well behind the curve with regard to inflation. As the Chair has said, forecasting has been awry. The Bank of England is one among others that has been too slow in raising interest rates, allowing inflation to mushroom well above the 2% target.

I have put it as strongly as suggesting that it has been a woeful neglect of duty. It is causing real pain out there for people and businesses. We should always remember, as we sit in our, sometimes, white ivory towers, having these debates, that we are talking about people’s lives and businesses that are having to grapple with double-digit inflation and interest rates perhaps going up too quickly. I think that you get it, but it is useful to remind ourselves of that.

Why should the public have confidence in your ability to get it right going forward? What lessons do you think that you have learned? What are you going to do differently? I am not hearing a satisfactory answer to that...

See the full report here – be prepared, it’s an acquired taste and a long read…

More wrong than right

However, some critics have argued that the BoE’s forecasts are often too optimistic or pessimistic, and that they fail to capture the impact of major shocks or structural changes in the economy. For example, the BoE was widely criticised for underestimating the severity of the 2008 financial crisis and overestimating the negative effects of Brexit on the economy. Some have also questioned the usefulness of the BoE’s forecasts for guiding monetary policy decisions, as they may be influenced by political or psychological factors.

Therefore, it may be wise to take the BoE’s forecasts with a grain of salt, and not to rely on them too much for making economic or financial decisions. The BoE’s forecasts are not useless, but they are not infallible either. They are one of many sources of information and analysis that can help us understand the state and prospects of the UK economy, but they should not be treated as gospel truth.

The Bank of England has been wrong with too many forecasts, so why bother? Target 2%, actual above 10%!

According to the chancellor Jeremy Hunt, the UK economy is caught in a trap

The UK and other advanced economies are facing a low-growth trap that is hard to escape. This means that the potential growth of the economy, which depends on factors such as productivity, innovation, investment, and labour force, is very low and insufficient to meet the demand and expectations of the people.

Brexit

The UK economy has been hit by huge global shocks that have disrupted its normal functioning and recovery. These include the Covid-19 pandemic, which caused lockdowns, restrictions, and health crises; the energy crisis, which led to soaring gas prices and supply shortages; and the Brexit transition, which created uncertainty and trade barriers.

Inflation

The UK economy is also struggling with high inflation, which erodes the purchasing power of consumers and businesses. Inflation is driven by various factors, such as rising energy costs, global supply chain bottlenecks, labour shortages, and pent-up demand.

‘Don’t you just love numbers?’

The Bank of England has raised interest rates to 5.25% as of August 2023 – the highest level since 2008, to curb inflation and maintain price stability. The Bank of England inflation target is 2%.

The plan?

The chancellor reportedly has vowed to stick to the plan that he believes will bring down inflation and boost growth in the long term.

He said that he will unveil a plan in the autumn statement that will show how the UK can break out of the low-growth trap and become one of the most entrepreneurial economies in the world. He also said that he will not ‘veer around like a shopping trolley‘ and change course in response to short-term pressures.

The Bank of England (BoE) announced another increase in its base rate, from 5% to 5.25%, the highest level in over 15 years as of 3rd August 2023. This is the 14th consecutive rise since December 2021, when the BoE started to tighten monetary policy in response to rising inflation.

The Bank said that inflation, which fell to 7.9% in June, remained well above its 2% target and that further action was needed to bring it down. It also cited the risks posed by the global economic situation, especially the conflict in Ukraine and the slowdown in China.

Affect on borrowers

The rate hike will affect millions of borrowers and savers across the UK. Fixed-rate mortgages will not change until the end of their term, but new deals will be hit borrowers hard. Savers may see some benefit from higher interest rates, but only if banks and building societies pass on the increase, which they are slow to do.

Bear in mind that for the past 15 years many have benefitted from ultra low interest rates and cheap money, this is not the ‘norm’. And now, as more ‘normal’ interest rates return it will initially disrupt financial stability for some, and it will be difficult for many for a time. But money has been cheap and mortgages have always been the cheapest way to borrow long term and that is still the case – even if it doesn’t feel like it right now.

Expected

The Bank of England’s decision was widely expected by market analysts, but some have warned that further rate rises could damage the UK economy, which is already showing signs of weakness. House prices are falling, manufacturing activity is contracting and consumer confidence is low.

The prime minister, Rishi Sunak, said he was disappointed that inflation was not falling faster, but claimed that he was making progress and that there was ‘light at the end of the tunnel‘.

And a train too if he isn’t careful!

UK has the highest interest rate in the G7

Interest rates have been increasing across the world in recent months.

The Bank of England’s latest rate hike means the UK now has the highest rates in the G7 – a group of the world’s seven largest so-called ‘advanced’ economies.

That’s higher than France, Germany, Italy, Japan, Canada and the U.S.

If you think the UK’s got it bad, spare a thought for these countries where interest rates are rampant

UK inflation rate remains high at 8.7% in May 2023

The UK inflation rate remained at 8.7% in the year to May 2023, according to the latest official figures from the Office for National Statistics (ONS). This is the same rate that was recorded in April, but down from the 10.1% level seen in March.

The ONS said that rising prices for air travel, recreational and cultural goods and services, and second-hand cars resulted in the largest upward contributions to the annual inflation rate. However, these were offset by falling prices for motor fuel and food and non-alcoholic beverages.

The ONS also reported that core inflation, which excludes energy, food, alcohol and tobacco, rose to 7.1% in May, up from 6.8% in April, and the highest rate since March 1992.

‘I’m just taking this calculator thingy to my boss, I thought it might help’. ‘Well, good idea, guess it can’t make it any worse’.

High inflation is the fault of everyone else other than the central bank

The inflation rate is measured by the Consumer Prices Index (CPI), which tracks the changes in the cost of a basket of goods and services that are typically purchased by households. The CPIH, which includes owner occupiers’ housing costs, rose by 7.9% in the year to May, up from 7.8% in April.

The high inflation rate has been driven by a combination of factors, including supply chain disruptions, labour shortages, higher energy costs, and strong consumer demand as the economy recovers from the coronavirus pandemic.

The Bank of England has a target to keep inflation at 2%, but it has said that it expects inflation to rise further in the coming months before falling back next year. The Bank has also signalled that it may raise interest rates sooner than expected to curb inflationary pressures.

However, June’s inflation reading came in below economists expectations at 7.3% A small but welcome reversal of high UK inflation. UK inflation is higher than the EU and U.S.

Are central banks doing a good job at controlling inflation? Bear in mind the inflation target is 2%…

The current interest rate in the UK is 5% as of June 2023.

This is the Bank Rate set by the Bank of England (BoE), which influences the interest rates that other banks charge borrowers and pay savers. The BoE has raised the Bank Rate 13 times in a row from 0.1% to 5% in a bid to control inflation, which is the rate at which the prices of goods and services increase over time. The BoE has a target of keeping inflation at 2%, but the current inflation rate is 8.7%, which is much higher than the target. This means that the purchasing power of money is decreasing and people have to pay more for the same things.

Summary

The Bank of England has increased the base rate to 5% – up from 4.5% in June 2023

It’s a bigger increase than most forecasters expected

The last time the base rate was 5% or higher was in 2008

Higher interest rates are intended to lower inflation, by giving mortgage-holders and consumers less to spend

The government’s target is to have inflation down to 5% by the end of the year

Rishi Sunak said: ‘I always said this would be hard – and clearly it’s got harder over the past few months’ – I am totally, 100%, on it, and it’s going to be OK‘

Seven of the nine members of the bank’s committee voted for the 5% rate – two wanted no change at all

Bank of England mission statement

Promoting the good of the people of the United Kingdom by maintaining monetary and financial stability.

Meet our new policy adviser

Well, the BoE has clearly done a good job here then with the UK interest rate now at 5%, again… and inflation at 8.7% after peaking at 11.1% in November 2022, a 41 year high! Great job!

And the UK PM said, ‘I always said this would be hard – and clearly it’s got harder over the past few months. I am totally, 100%, on it, and it’s going to be OK‘.

That’s good to know then – it’s going to be OK – so reassuring for borrowers! It’s going to be OK, so don’t worry!

Sorry PM, but that is so weak it’s bordering pathetic. Weren’t you the chancellor too?