After years in Silicon Valley’s policy sanctum, Nick Clegg has re-emerged on British soil with a warning: the AI sector is overheating.

The man who once fronted a coalition government, then pivoted to Meta’s global affairs desk, now cautions that the ‘absolute spasm’ of AI deal-making may be headed for a correction.

Is this his opinion or just borrowed from other commentators. I, for one, am not interested in what he has to say. I did once, but not anymore.

It’s a curious homecoming. Clegg left UK politics after his party was electorally eviscerated, only to rebrand himself as a transatlantic tech ‘diplomat’ or tech tourist.

Now, with the AI hype cycle in full swing, he returns not as a policymaker, but as a prophet of moderation—urging restraint in a sector he arguably helped legitimise from within.

His critique isn’t wrong. Valuations are frothy. Infrastructure costs are staggering. And the promise of artificial superintelligence remains more theological than technical. But Clegg’s timing invites scrutiny.

Is this a genuine call for realism, or a reputational hedge from someone who’s seen the inside of the machine?

There’s a deeper irony here: the same political class that once championed deregulation and digital optimism now warns of runaway tech. The same voices that embraced disruption now plead for caution.

It’s less a reversal than a ritual—an elite rite of return, where credibility is reasserted through critique.

Clegg’s message may be sound. But in a landscape saturated with recycled authority, the messenger matters.

And for many, his reappearance feels less like a reckoning and more like déjà vu in a different suit.

In a move that has stunned economists and ignited political debate, the United States has extended a $20 billion bailout to Argentina—a country long plagued by inflation, debt crises, and political volatility.

The lifeline, structured as a currency swap between the U.S. Treasury and Argentina’s central bank, aims to stabilise the peso and prevent a broader emerging market meltdown.

At the heart of the bailout is President Javier Milei, Argentina’s libertarian leader and a vocal ally of U.S. President Donald Trump.

Milei’s radical economic reforms—slashing public spending, deregulating markets, and firing thousands of civil servants—have earned praise from American conservatives but rattled domestic confidence.

Following a bruising electoral defeat last month, Argentina’s currency nosedived, prompting fears of default and capital flight.

Pre-emptive?

The U.S. Treasury, led by Secretary Scott Bessent, argues the bailout is a pre-emptive strike against contagion.

While Argentina poses little systemic risk on its own, its collapse could trigger panic across Latin American debt markets and commodity exchanges.

The swap provides Argentina with desperately needed dollar liquidity, while the U.S. hopes to anchor regional stability and protect its own financial interests.

Critics, however, accuse the Trump administration of prioritising political loyalty over economic prudence.

With the U.S. government itself mired in a shutdown and domestic industries reeling from trade tensions, the optics of rescuing a foreign ally are fraught. Democratic lawmakers have introduced bills to block the bailout, calling it “inexplicable” and “reckless”.

Whether this intervention proves a masterstroke of diplomacy or a costly miscalculation remains to be seen. For now, Argentina has bought time—and Washington has bet big on Milei’s vision of libertarian revival.

The UK economy recorded modest growth in August 2025, expanding by 0.1% according to the Office for National Statistics (ONS).

This slight gain follows a revised contraction of 0.1% in July 2025, underscoring the fragile nature of the recovery as the government prepares for next month’s Budget.

Manufacturing led the charge, growing by 0.7%, while services held steady. However, consumer-facing sectors and wholesale trade continued to drag, reflecting persistent cost pressures and subdued household confidence.

Over the three-month period to August 2025, the economy grew by 0.3%, offering a glimmer of resilience despite broader concerns.

Chancellor Rachel Reeves faces mounting pressure to address a projected £22bn shortfall. It always appears to be a £20-22 billion hole – it must be a ‘magical’ figure.

She has signalled potential tax and spending adjustments to ensure fiscal sustainability, though uncertainty around these measures may dampen business and consumer sentiment in the near term.

Some economists have warned that slowing wage growth and elevated living costs are likely to constrain household spending, with sluggish growth expected to persist.

Meanwhile, the IMF forecasts the UK to be the second-fastest-growing G7 economy this year, albeit with the highest inflation rate.

As Budget Day looms, the government’s challenge remains clear: stimulate growth without deepening the cost-of-living strain.

Tax increases are coming, despite government manifesto promises to the contrary.

U.S. stock markets are behaving like a mood ring in a thunderstorm—volatile, reactive, and oddly sentimental.

One moment, President Trump threatens a ‘massive increase’ in tariffs on Chinese imports, and nearly $2 trillion in market value evaporates.

The next, he posts that: ‘all will be fine‘, and futures rebound overnight. It’s not just policy—it’s theatre, and Wall Street is watching every act with bated breath.

This hypersensitivity isn’t new, but it’s been amplified by the precarious state of global trade and the towering expectations placed on artificial intelligence.

Trump’s recent comments about China’s rare earth export controls triggered a sell-off that saw the Nasdaq drop 3.6% and the S&P 500 fall 2.7%—the worst single-day performance since April.

Tech stocks, especially those reliant on semiconductors and AI infrastructure, were hit hardest. Nvidia alone lost nearly 5%.

Why so fickle? Because the market’s current rally is built on a foundation of hope and hype. AI has been the engine driving valuations to record highs, with companies like OpenAI and Anthropic reaching eye-watering valuations despite uncertain profitability.

The IMF and Bank of England have both warned that we may be in stage three of a classic bubble cycle6. Circular investment deals—where AI startups use funding to buy chips from their investors—have raised eyebrows and comparisons to the dot-com era.

Yet, the bubble hasn’t burst. Not yet. The ‘Buffett Indicator‘ sits at a historic 220%, and the S&P 500 trades at 188% of U.S. GDP. These are not numbers grounded in sober fundamentals—they’re fuelled by speculative fervour and a fear of missing out (FOMO).

But unlike the dot-com crash, today’s AI surge is backed by real infrastructure: data centres, chip fabrication, and enterprise adoption. Whether that’s enough to justify the valuations remains to be seen.

In the meantime, markets remain twitchy. Trump’s tariff threats are more than political posturing—they’re economic tremors that ripple through supply chains and investor sentiment.

And with AI valuations stretched to breaking point, even a modest correction could trigger a cascade.

So yes, the market is fickle. But it’s not irrational—it’s just balancing on a knife’s edge between technological optimism and geopolitical anxiety.

China’s latest tightening of rare earth exports has reignited global concerns over supply chain fragility and strategic resource dependence.

With Beijing now requiring special permits for the export of key rare earth elements—used in everything from electric vehicles to missile guidance systems—the move is widely seen as a geopolitical lever in an increasingly fractured global trade landscape.

Rare earths, despite their name, are not scarce—but China controls over 60% of global production and an even larger share of refining capacity. The new restrictions, framed as national security measures, have already begun to ripple through equity markets.

Shares of Western mining firms such as Albemarle and MP Materials surged on the news, as investors bet on alternative sources gaining traction. Meanwhile, defence and tech stocks in Europe dipped, reflecting fears of supply bottlenecks and rising input costs1.

This isn’t China’s first foray into rare earth brinkmanship. Similar curbs in 2010 triggered a scramble for diversification, but progress has been slow.

The current squeeze coincides with rising tensions over semiconductor access and military technology, suggesting a broader strategy of resource weaponisation.

For investors, the message is clear: rare earths are no longer just a niche commodity—they’re a geopolitical flashpoint. Expect increased volatility in sectors reliant on high-performance magnets, batteries, and advanced optics.

Countries like the US, Australia, and Canada are accelerating domestic mining initiatives, but scaling up remains a long-term play.

In the short term, China’s grip on rare earths is tightening—and markets are reacting accordingly.

As the global economy pivots toward electrification and AI-driven infrastructure, the battle over these elemental building blocks is only just beginning. The stocks may rise and fall, but the strategic stakes are climbing ever higher.

China’s sweeping export restrictions on rare earths have triggered a sharp rally in related stocks, especially among U.S.-based producers and processors.

The market is interpreting Beijing’s move as both a supply threat and a strategic opportunity for non-Chinese firms to gain ground.

📈 Some companies in the spotlight

USA Rare Earth surged nearly 15% in a single day and is up 94% over the past five weeks, buoyed by speculation of a potential U.S. government investment and its vertically integrated magnet production pipeline.

NioCorp Developments, Ramaco Resources, and Energy Fuels all posted gains of approximately between 9–12%.

MP Materials, the largest U.S. rare earth miner, rose over 6% following news of tighter Chinese controls. The company recently secured a strategic equity deal with the U.S. Department of Defence.

Albemarle, Lithium Americas, and Trilogy Metals also saw modest gains, reflecting broader investor interest in critical mineral plays.

Company / Sector

Stock Movement

Strategic Note

MP Materials (US)

↑ +6%

DoD-backed, key US supplier

USA Rare Earth

↑ +15%

Magnet pipeline, gov’t investment buzz

NioCorp / Ramaco / Energy Fuels

↑ +9–12%

Domestic mining surge

European Defence Stocks

↓ 2–4%

Supply chain fears

Chinese Magnet Producers

↔ / ↓

Export permit uncertainty

China’s new rules, effective December 1st, require export licences for any product containing more than 0.1% rare earths or using Chinese refining or magnet recycling tech. This has intensified scrutiny on global supply chains and elevated the strategic value of domestic alternatives.

🧭 Investor sentiment is shifting toward companies that can offer secure, non-Chinese sources of rare earths—especially those with downstream capabilities like magnet manufacturing. The rally suggests markets are pricing in long-term geopolitical risk and potential government backing.

Weekend update

Is President Trump in control of the stock market? A comment on TruthSocial suggesting that more China tariffs might be introduced in response to China’s restrictions on rare earth materials reportedly wipes out around $2 trillion from U.S. stocks.

Then it reverses as Trump says, ‘All will be fine’. Stocks climb back up. What’s going on?

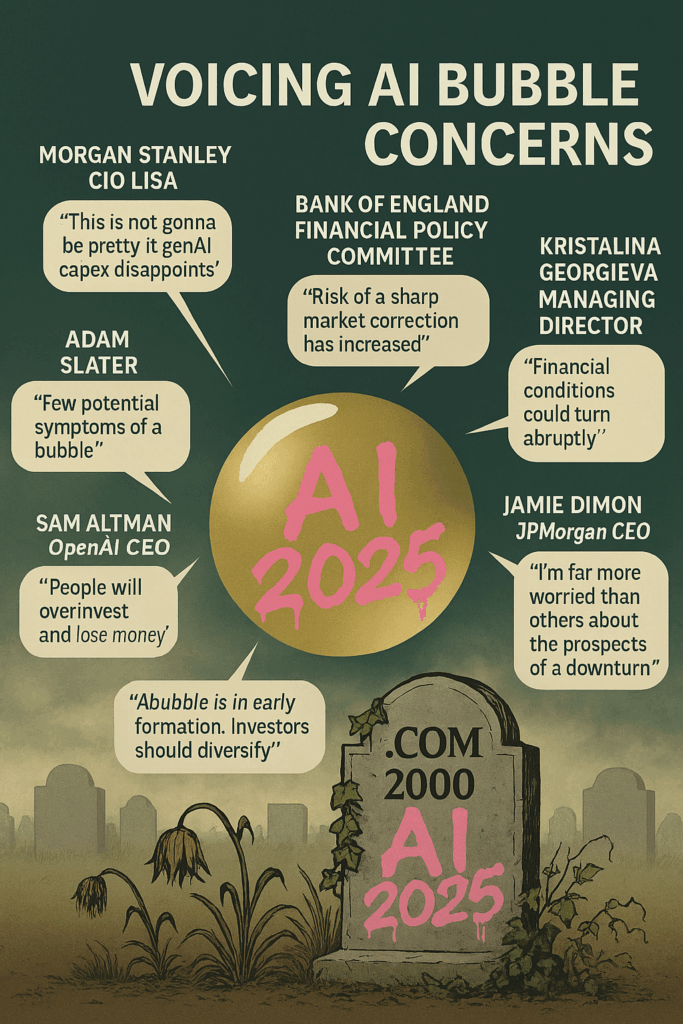

Influential figures and institutions are sounding the AI alarm—or at least raising eyebrows—about the frothy valuations and speculative fervour surrounding artificial intelligence.

Who’s Warning About the AI Bubble?

🏛️ Bank of England – Financial Policy Committee

View: Stark warning.

Quote: “The risk of a sharp market correction has increased.”

Why it matters: The BoE compares current AI stock valuations to the dotcom bubble, noting that the top five S&P 500 firms now command nearly 30% of market cap—the highest concentration in 50 years.

🏦 Jerome Powell – Chair, U.S. Federal Reserve

View: Cautiously sceptical.

Quote: Assets are “fairly highly valued.”

Why it matters: While not naming AI directly, Powell’s remarks echo broader concerns about tech valuations and investor exuberance.

🧮 Lisa Shalett – Chief Investment Officer, Morgan Stanley Wealth Management

View: Deeply concerned.

Quote: “This is not going to be pretty” if AI capital expenditure disappoints.

Why it matters: Shalett warns that 75% of S&P 500 returns are tied to AI hype, likening the moment to the “Cisco cliff” of the early 2000s.

🌍 Kristalina Georgieva – Managing Director, IMF

View: Watchful.

Quote: Financial conditions could “turn abruptly.”

Why it matters: Georgieva highlights the fragility of markets despite AI’s productivity promise, warning of sudden sentiment shifts.

🧨 Sam Altman – CEO, OpenAI

View: Self-aware caution.

Quote: “People will overinvest and lose money.”

Why it matters: Altman’s admission from inside the AI gold rush adds credibility to bubble concerns—even as his company fuels the hype.

📦 Jeff Bezos – Founder, Amazon

View: Bubble-aware.

Quote: Described the current environment as “kind of an industrial bubble.”

Why it matters: Bezos sees parallels with past tech manias, suggesting that infrastructure spending may be overextended.

🧠 Adam Slater – Lead Economist, Oxford Economics

View: Analytical.

Quote: “There are a few potential symptoms of a bubble.”

Why it matters: Slater points to stretched valuations and extreme optimism, noting that productivity projections vary wildly.

🏛️ Goldman Sachs – Investment Strategy Division

View: Cautiously optimistic.

Quote: “A bubble has not yet formed,” but investors should “diversify.”

Why it matters: Goldman acknowledges the risks while maintaining that fundamentals may still justify valuations—though they advise caution.

AI Bubble voices infographic October 2025

🧠 Julius Černiauskas and the Oxylabs AI/ML Advisory Board

🔍 View: The AI hype is nearing its peak—and may soon deflate.

Černiauskas warns that AI development is straining environmental resources and public trust. He’s pushing for responsible and sustainable AI practices, noting that transparency is lacking in how many models operate.

Ali Chaudhry, research fellow at UCL and founder of ResearchPal, adds that scaling laws are showing their limits. He predicts diminishing returns from simply making models bigger, and expects tightened regulations around generative AI in 2025.

Adi Andrei, cofounder of Technosophics, goes further: he believes the Gen AI bubble is on the verge of bursting, citing overinvestment and unmet expectations

🧠 Jamie Dimon on the AI Bubble

🔥 View: Sharply concerned—more than most as widely reported

Quote: “I’m far more worried than others about the prospects of a downturn.”

Context: Dimon believes AI stock valuations are “stretched” and compares the current surge to the dotcom bubble of the late 1990s.

📉 Key Warnings from Dimon

“Sharp correction” risk: He sees a real danger of a sudden market pullback, especially given how AI-related stocks have surged disproportionately—like AMD jumping 24% in a single day after an OpenAI deal.

“Most people involved won’t do well”: Dimon told the BBC that while AI will ultimately pay off—like cars and TVs did—many investors will lose money along the way.

“Governments are distracted”: He criticised policymakers for focusing on crypto and ignoring real security threats, saying: “We should be stockpiling bullets, guns and bombs”.

“AI will disrupt jobs and companies”: At a trade event in Dublin, he warned that AI’s ubiquity will shake up industries and employment across the board.

And so…

The AI boom of 2025 has ignited a speculative frenzy across global markets, with tech stocks soaring and investors piling into anything labelled “AI-adjacent.”

But beneath the euphoria, a chorus of high-profile warnings is growing louder. From the Bank of England and IMF to JPMorgan’s Jamie Dimon and OpenAI’s Sam Altman, concerns are mounting that valuations are dangerously stretched, capital is overconcentrated, and the narrative is outpacing reality.

Dimon likens the moment to the dotcom bubble, while Altman admits many will “lose money” chasing the hype. Analysts point to classic bubble signals: retail mania, corporate FOMO, and earnings divorced from fundamentals.

Even as AI’s long-term utility remains promising, the short-term exuberance may be setting the stage for a sharp correction.

Whether it’s a pullback or a full-blown crash, the mood is shifting—from uncritical optimism to wary anticipation.

The question now is not whether AI will change the world, but whether markets have priced in too much, too soon.

We have been warned!

The AI bubble will pop – it’s just a matter of when and not if.

In the world of stock markets, few phenomena are as captivating—or as perilous—as bull runs and speculative bubbles.

Though often conflated, these two forces represent distinct psychological and financial dynamics that shape investor behaviour and market outcomes.

Bull Markets: Confidence with Momentum

A bull market is defined by sustained price increases across major indices. Typically driven by strong economic fundamentals, corporate earnings growth, and investor optimism.

In the U.S., iconic bull runs include the post-World War II expansion. The 1980s Reagan-era boom, and the tech-fuelled rally of the 2010s. The Dot-Com bull run, and subsequesnt crash is probably the most famous.

Bull markets feed on confidence: low interest rates, rising employment, and technological innovation often act as catalysts. Investors pile in, believing the upward trajectory will continue—sometimes for years.

But even bulls can lose their footing. When valuations stretch beyond reasonable earnings expectations, the line between bullish enthusiasm and irrational exuberance begins to blur.

Bubbles: Euphoria Untethered from Reality

A bubble occurs when asset prices inflate far beyond their intrinsic value. This is fuelled not by fundamentals but by speculation and herd mentality.

The dot-com bubble of the late 1990s is a textbook example. Companies with no profits—or even products—saw their valuations soar simply for having ‘.com’ in their name.

Similarly, the U.S. housing bubble of the mid-2000s was driven by easy credit and the belief that property prices could only go up.

Bubbles often follow a predictable arc: stealth accumulation, media attention, public enthusiasm, and finally, a euphoric peak.

When reality sets in—be it through disappointing earnings, regulatory shifts, or macroeconomic shocks—the bubble bursts! Leaving behind financial wreckage and a trail of disillusioned investors.

Spotting the Difference

While bull markets can be healthy and sustainable, bubbles are inherently unstable. The key distinction lies in valuation discipline.

Bulls are supported by earnings and growth; bubbles are driven by hype and fear of missing out (FOMO).

Tools like the cyclically adjusted price-to-earnings (CAPE) ratio and historical trend analysis can help investors discern whether they’re riding a bull or inflating a bubble.

📉 The Aftermath and Opportunity Ironically, the collapse of a bubble often sows the seeds for the next bull market. As excesses are purged and valuations reset, long-term investors find opportunities in the rubble.

The challenge lies in resisting the emotional extremes—greed during the rise, panic during the fall—and maintaining a clear-eyed view of value.

In markets, as in life, not every rise is rational, and not every fall is fatal

As of October 2025, many analysts argue that the U.S. stock market is exhibiting classic signs of a bubble. Valuations stretched across major indices and speculative behaviour intensifying—particularly in mega-cap tech stocks and passive index funds.

The S&P 500 recently hit record highs despite a backdrop of political gridlock and a government shutdown. This suggests a disconnect between price momentum and underlying economic risks.

Indicators like Market Cap to Gross Value Added (GVA) and excessive investor sentiment point to a speculative mania. Some experts are calling it the largest asset bubble in U.S. history.

While a full-blown crash hasn’t materialised yet, the market’s frothy conditions and historical October volatility have many bracing for a potential correction.

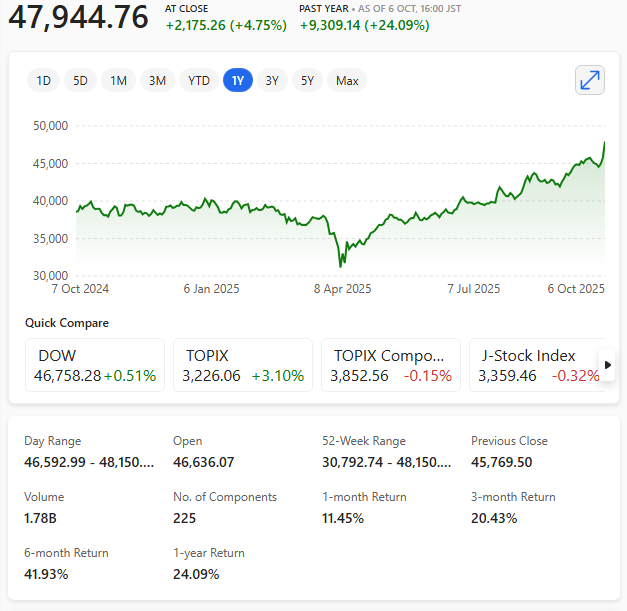

Japan’s benchmark Nikkei 225 index soared past the symbolic 48,000 mark on Monday 6th October 2025 in intraday trading, marking a new all-time high and underscoring investor confidence in the country’s shifting political landscape.

The index closed at 47944.76, up approximately 4.15% from Friday’s session, driven by a wave of optimism surrounding the Liberal Democratic Party’s leadership transition.

Nikkei 225 smashes to new record high October 6th 2025

Sanae Takaichi, a staunch conservative with deep ties to former Prime Minister Shinzo Abe, has emerged as the frontrunner to lead the party—and potentially become Japan’s first female prime minister.

Her pro-growth stance, admiration for Margaret Thatcher, and commitment to industrial revitalisation have sparked hopes of continued economic liberalisation.

The yen weakened boosting export-heavy sectors such as automotive and electronics. Toyota and Sony led the charge, with gains of 5.1% and 4.8% respectively.

Analysts also pointed to easing U.S. bond yields and a rebound on Wall Street as contributing factors.

While the rally reflects renewed market enthusiasm, it also raises questions about Japan’s long-term structural challenges—from demographic decline to mounting public debt.

For now, however, the Nikkei’s ascent offers a potent symbol of investor faith in Japan’s evolving political and economic narrative.

The Resilient Stock Market: A Double-Edged Shield Against Recession

In a year marked by political volatility, Trumps tariff war, soft labour data, and persistent inflation anxieties, one pillar of the economy has stood tall: the stock market.

Defying expectations, major indices like the Nasdaq, Dow Jones and S&P 500 have surged, buoyed by AI-driven optimism and industrial strength. This resilience has helped stave off a technical recession—but not without raising deeper concerns about economic fragility and inequality.

At the heart of this phenomenon lies the ‘wealth effect’. As equity portfolios swell, high-net-worth households feel richer and spend more freely.

This consumer activity props up GDP figures and masks underlying weaknesses in wage growth, job creation, and productivity.

August’s economic data showed surprising strength in consumer spending and housing, despite lacklustre employment figures and fading stimulus support.

But here’s the rub: this buoyancy is not broadly shared. According to the University of Michigan’s sentiment index, confidence has declined sharply since January, especially among those without significant stock holdings.

Balance

The U.S. economy, in effect, is being held aloft by a narrow slice of the population—those with the means to benefit from rising asset prices. For everyone else, the recovery feels distant, even illusory.

This divergence creates a dangerous illusion of stability. Policymakers may hesitate to intervene—whether through fiscal support or monetary easing—because headline indicators look healthy. Yet beneath the surface, vulnerabilities abound.

If the market were to correct sharply, the spending it fuels could evaporate overnight, exposing the economy’s dependence on asset inflation.

Moreover, the market’s resilience may be distorting capital allocation. Companies flush with investor cash are prioritising stock buybacks and speculative ventures over wage growth or long-term investment. This can exacerbate inequality and erode the foundations of sustainable growth.

In short, while the stock market’s strength has delayed a recession, it has also deepened the disconnect between Wall Street and Main Street.

The danger lies not in the market’s success, but in mistaking it for economic health. A resilient market may be a shield—but it’s not a cure. And if that shield cracks, the consequences could be swift and severe.

The challenge now is to look beyond the indices and ask harder questions: Who is benefitting? What are we neglecting?

And how do we build an economy that’s resilient not just in numbers, but in substance, regardless of nation.

It’s one of those classic Wall Street paradoxes—where bad news somehow fuels bullish momentum. What’s going on?

News round-up

S&P 500 closes above 6,700 after rising 0.34%. Samsung and SK Hynix join OpenAI’s Stargate. Taiwan rejects U.S. proposal to split chip production. Trump-linked crypto firm plans expansion. Some stocks that doubled in the third quarter.

Bleak Headlines vs. Market Optimism

U.S. Government Shutdown: The federal government ground to a halt, but markets didn’t flinch. In fact, the S&P 500 rose 0.34% and closed above 6,700 for the first time.

ADP Jobs Miss: Private payrolls fell by 32,000 in September 2025, a sharp miss – at least compared to the expected 45,000 gain. Yet traders shrugged it off as other bad news is shrugged off too!

Fed Rate Cut Hopes: Weak data often fuels expectations that the Federal Reserve will cut interest rates. Traders are now betting on a possible cut in October 2025, which tends to boost equities.

Historical Pattern: According to Bank of America, the S&P 500 typically rises ~1% in the week before and after a government shutdown. So, this isn’t unprecedented—it’s almost ritualistic at this point.

Why the Market’s Mood Diverges

Animal Spirits: Investors often trade on sentiment and positioning, not just fundamentals. If they believe the Fed will ease policy, they’ll buy risk assets—even in the face of grim news.

Data Gaps: With the Bureau of Labor Statistics’ official jobs report delayed due to the shutdown, the ADP report gains more weight. But it’s historically less reliable, so traders may discount it.

Tech Tailwinds: AI stocks and semiconductor news (e.g., Samsung and SK Hynix joining OpenAI’s Stargate) are buoying sentiment, especially in Asia-Pacific markets.

U.S. Government Shutdown October 2025

Prediction

Traders in prediction markets are betting the shutdown will last around two weeks. Nothing too radical, since that’s the average length it takes for the government to reopen, based on data going back to 1990.

The government stoppage isn’t putting the brakes on the stock market momentum. Are investors getting too adventurous?

History shows the pattern is not new. The S&P 500 has risen an average of 1% the week before and after a shutdown, according to data from BofA.

Even the ADP jobs report, which missed expectations by a wide margin, did little to subdue the animal spirits.

Private payrolls declined by 32,000 in September 2025, according to ADP, compared with a 45,000 increase reportedly estimated by a survey of economists.

Payroll data

The Bureau of Labor Statistics’ (BLS) official nonfarm payrolls report is now stuck in bureaucratic purgatory and likely not being released on time.

The U.S. Federal Reserve might place additional weight on the ADP report — though it’s not always moved in sync with the BLS numbers. Traders expect weak data would prompt the Fed to cut interest rates in October 2025.

It’s a bit like watching a storm roll in while the crowd cheers for sunshine—markets are forward-looking, and sometimes they see silver linings where others see clouds.

Summary

Event

Detail

🏛️ Government Shutdown

Began Oct 1, 2025. Traders expect ~2 weeks based on historical average

📉 ADP Jobs Report

Private payrolls fell by 32,000 vs. expected +45,000

📈 S&P 500 Close

Rose 0.34% to close above 6,700 for the first time

The United States government has once again entered a shutdown, marking the first lapse in federal funding in nearly seven years.

As of 12:01 a.m. Eastern Time on Wednesday 1st October 2025, Congress failed to pass a spending bill, triggering the closure of non-essential government services and furloughing hundreds of thousands of federal workers.

This latest impasse stems from a partisan standoff over healthcare subsidies and broader budget priorities.

Senate Democrats demanded the extension of Affordable Care Act tax credits, while Republicans insisted on passing a ‘clean’ funding bill without concessions. With neither side willing to compromise, the shutdown became inevitable.

The last government shutdown occurred from 22nd December 2018 to 25th January 2019, during President Trump’s first term.

That 35-day closure—the longest in U.S. history—was driven by a dispute over funding for a U.S.-Mexico border wall. It cost the economy an estimated $3 billion in lost GDP and left federal workers unpaid for weeks.

Shutdowns in the U.S. are not uncommon, but their frequency and duration have increased in recent decades. They typically occur when Congress fails to agree on annual appropriations bills before the start of the fiscal year on 1st October 2025.

While essential services like defence and air traffic control continue, most civilian agencies grind to a halt, delaying everything from passport processing to scientific research.

This latest shutdown is expected to have wide-reaching effects, including disruptions to veterans’ services, nutrition programmes, and disaster relief funding.

Both parties are under pressure to resolve the deadlock swiftly, but with political tensions running high, a quick resolution remains uncertain.

As the shutdown unfolds, the American public is left to navigate the consequences of a deeply divided government—one that seems increasingly unable to fulfil its most basic function: keeping the lights on.

Many traditional CPU-centric server farms are being retrofitted to support GPU-heavy or heterogeneous architectures.

Some legacy racks are adapted for edge computing, non-AI workloads, or low-latency services that don’t require massive AI computing power.

🧹 Decommissioning and Disposal

Obsolete hardware—especially older CPUs and low-density racks—is being decommissioned.

Disposal is a growing concern: e-waste regulations are tightening, and sustainability targets mean companies must recycle or repurpose responsibly.

🏭 Secondary Markets and Resale

Some older servers are sold into secondary markets—used by smaller firms, educational institutions, or regions with less AI demand.

There’s also a niche for refurbished hardware, especially in countries where AI infrastructure is still nascent.

🧊 Cold Storage and Archival Use

Legacy systems are sometimes shifted to cold storage roles—archiving data that doesn’t require real-time access.

These setups are less power-intensive and can extend the life of older tech without compromising performance.

⚠️ Obsolescence Risk

The pace of AI innovation is so fast that even new data centres risk early obsolescence if they’re not designed with future workloads in mind.

Rack densities are climbing—from 36kW to 80kW+—and cooling systems are shifting from air to liquid, meaning older infrastructure simply can’t keep up.

🧭 A Symbolic Shift

This isn’t just about servers—it’s about sovereignty, sustainability, and the philosophy of obsolescence. The old tech isn’t just being replaced; it’s being relegated, repurposed, or ritually retired.

There’s a tech history lesson unfolding about digital mortality, and how each new AI cluster buries a generation of silicon ancestors.

Infographic: ‘New’ AI tech replacing ‘Old’ tech in data centres

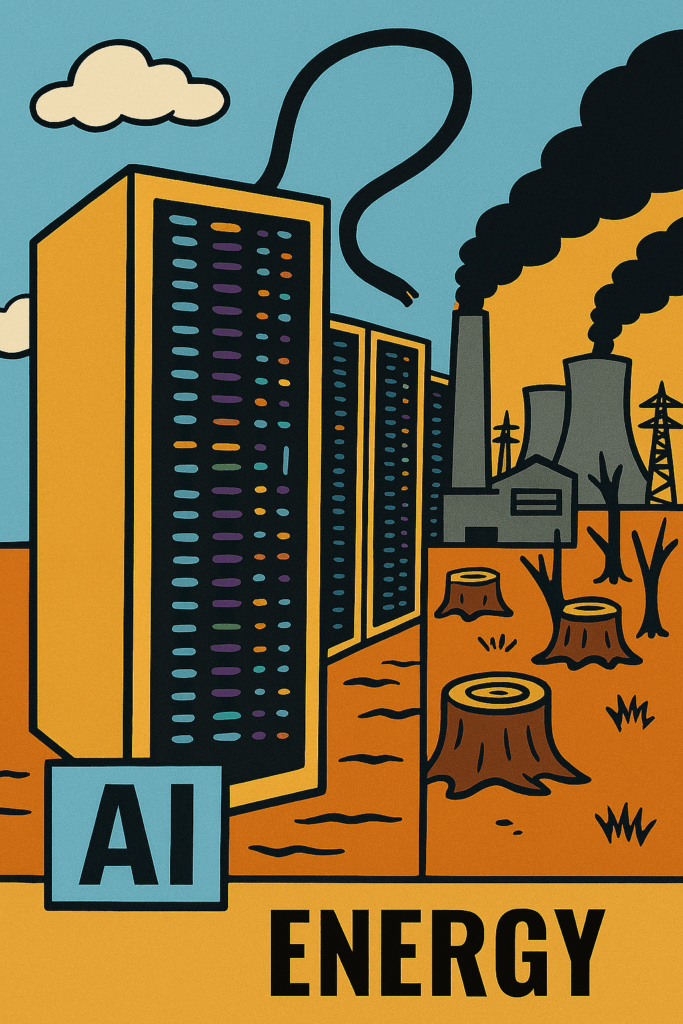

🌍 The Green Cost of the AI Boom

⚡ Energy Consumption

AI data centres are power-hungry beasts. In 2023, they consumed around 2% of global electricity—a figure expected to rise by 80% by 2026.

Nvidia’s H100 GPUs, widely used for AI workloads, draw 700 watts each. With millions deployed, the cumulative demand is staggering.

💧 Water Usage

Cooling these high-density clusters often requires millions of litres of water annually. In drought-prone regions, this is sparking local backlash.

🧱 Material Extraction

AI infrastructure depends on critical minerals—lithium, cobalt, rare earths—often mined in ecologically fragile zones.

These supply chains are tied to geopolitical tensions and labour exploitation, especially in the Global South.

🗑️ E-Waste and Obsolescence

As new AI chips replace older hardware, legacy servers are decommissioned—but not always responsibly.

Without strict recycling protocols, this leads to mountains of e-waste, much of which ends up in landfills or exported to countries with lax regulations.

The Cloud Has a Shadow

This isn’t just about silicon—it’s about digital colonialism, resource extraction, and the invisible costs of intelligence. AI may promise smarter sustainability, but its infrastructure is anything but green unless radically reimagined.

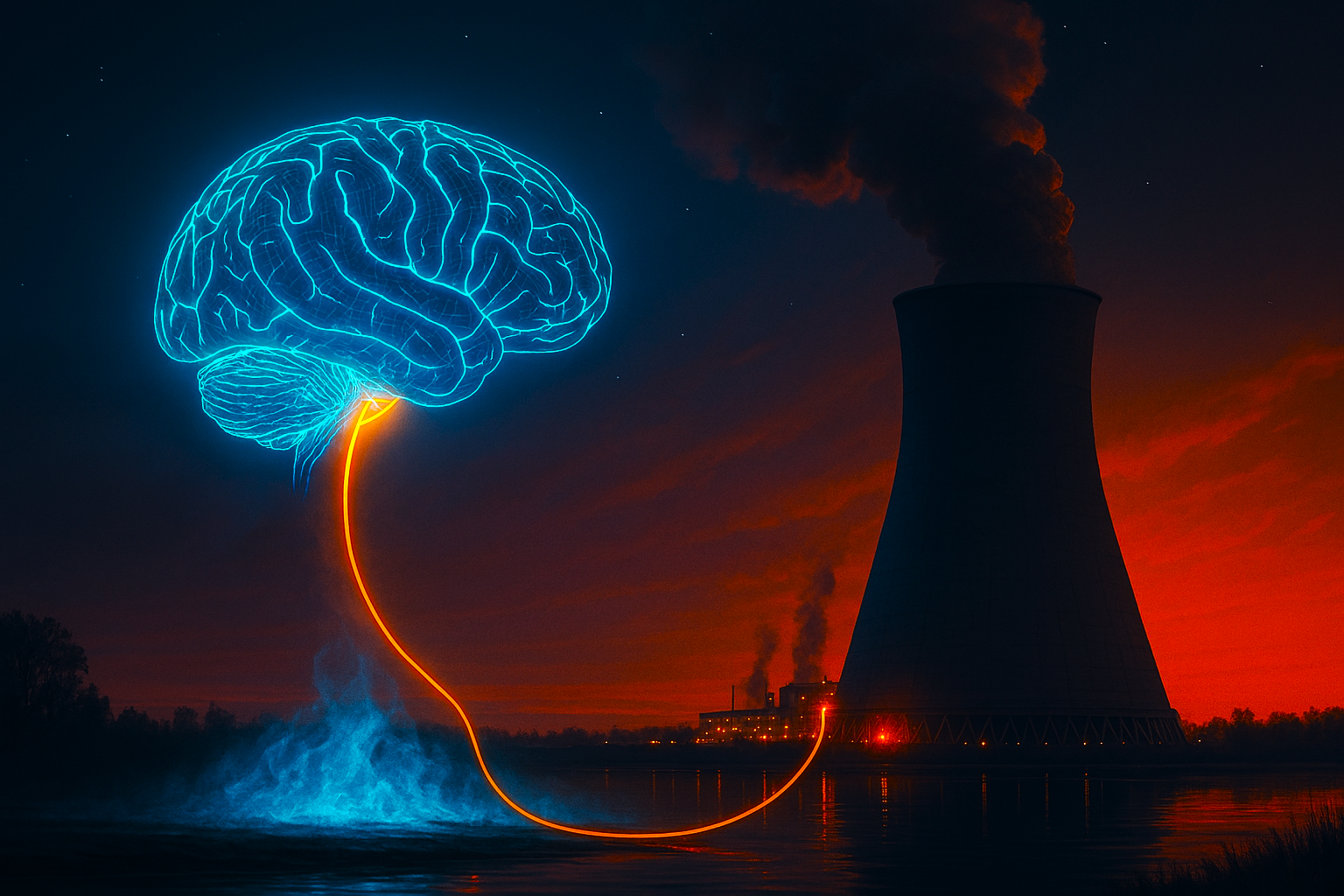

⚡ The Energy Cost of Intelligence

🔋 Surging Power Demand

AI data centres are projected to drive a 165% increase in global electricity consumption by 2030, compared to 2023 levels.

In the U.S. alone, data centres could account for 11–12% of total power demand by 2030—up from 3–4% today.

A single hyperscale facility can draw 100 megawatts or more, equivalent to powering 350,000–400,000 electric vehicles annually.

AI and Energy supply

🧠 Why AI Is So Power-Hungry

Training large models like OpenAI Chat GPT or DeepSeek requires massive parallel processing, often using thousands of GPUs.

Each AI query can consume 10× the energy of a Google search, according to the International Energy Agency.

Power density is rising—from 162 kW per square foot today to 176 kW by 2027, meaning more heat, more cooling, and more infrastructure.

🌍 Environmental Fallout

Cooling systems often rely on millions of litres of water annually. For example, in Wisconsin, two AI data centres will consume 3.9 gigawatts of power, more than the state’s nuclear plant.

Without renewable energy sources, this surge risks locking regions into fossil fuel dependency, raising emissions and household energy costs. We are not ready for this massive increase in AI energy production.

This isn’t just about tech—it’s about who pays for progress. AI promises smarter cities, medicine, and governance, but its infrastructure demands a hidden tax: on grids, ecosystems, and communities.

AI is a hungry beast, and it needs feeding. The genie is out of the bottle!

Trump’s latest tariff salvo is already rattling pharma stocks. Branded drugs now face a 100% levy unless firms build plants in the U.S.

Trump’s Drug Tariffs: A protectionist prescription policy?

In a move that’s rattled pharmaceutical markets across Asia and Europe, President Trump has announced a sweeping 100% tariff on branded, patented drugs imported into the United States—unless manufacturers relocate production to American soil.

The policy, unveiled via executive order, is part of a broader push to ‘restore pharmaceutical sovereignty’ and reduce reliance on foreign supply chains.

The impact was immediate. Asian pharma stocks tumbled, with major exporters in India, South Korea, and Japan facing sharp declines. It is uncertain how this will affect the UK.

European firms, already grappling with regulatory headwinds, now face a stark choice: invest in U.S. manufacturing or risk losing access to one of the world’s most lucrative drug markets.

Critics argue the move is less about health security and more about economic nationalism. “This isn’t about safety—it’s about leverage,” said one analyst. “Trump’s team is using tariffs as a blunt instrument to force industrial relocation.”

Supporters, however, hail the policy as long overdue. With drug shortages and supply chain fragility exposed during the pandemic, the White House insists the tariffs will incentivise domestic resilience and job creation.

Yet the devil lies in the dosage. Smaller biotech firms may struggle to absorb the costs of relocation, potentially stifling innovation. And with branded drugs often tied to complex global patents and licensing agreements, the legal fallout could be significant.

The symbolism is potent: medicine, once a universal good, is now a battleground for economic identity. Trump’s tariff salvo reframes pharmaceuticals not as tools of healing, but as tokens of sovereignty. Whether this prescription cures or corrupts remains to be seen.

U.S. President Donald Trump has also stated that said plans to impose a 25% tariff on imported heavy trucks from 1st October 2025.

In a candid assessment that sent ripples through global markets, Federal Reserve Chair Jerome Powell has acknowledged that U.S. stock prices appear ‘fairly highly valued’ by several measures.

Speaking at a recent event in Providence, Rhode Island, Powell reportedly responded to questions about the Fed’s tolerance for elevated asset prices, noting that financial conditions—including equity valuations—are closely monitored to ensure they align with the central bank’s policy goals.

Powell’s comments, however, injected a dose of caution, suggesting that the Fed is wary of froth building in the markets.

While Powell stopped short of calling current valuations unsustainable, his phrasing echoed past warnings from central bankers about speculative excess. ‘Markets listen to us and make estimations about where they think rates are going’, he reportedly said, adding that the Fed’s policies are designed to influence broader financial conditions—not just interest rates.

The timing of Powell’s remarks is notable. The Fed recently (September 2025) cut its benchmark rate by 0.25 percentage points, a move that had bolstered investor sentiment.

Yet Powell also highlighted the ‘two-sided risks’ facing the economy: inflation remains sticky, while the labour market shows signs of softening. This balancing act, he implied, leaves little room for complacency.

Markets reacted swiftly. Tech stocks, which have led the recent rally, saw sharp declines, with Nvidia and Amazon among the hardest hit.

Powell’s warning may not signal an imminent correction, but it does suggest the Fed is keeping a watchful eye on valuations—and won’t hesitate to act if financial stability is threatened

As artificial intelligence surges into every corner of modern life—from predictive finance to generative art—the question isn’t just what AI can do, but what it consumes to do it.

The energy appetite of large-scale AI models is no longer a footnote; it’s the headline.

Training a single frontier model can devour as much electricity as hundreds of UK homes use in a year. And once deployed, these systems don’t slim down—they scale up.

Every query, every image generation, every chatbot exchange draws from vast data centres, many powered by fossil fuels or water-intensive cooling systems.

The irony? AI is often pitched as a tool for climate modelling, yet its own carbon footprint is ballooning.

This isn’t just a technical dilemma—it’s a moral one. The race to build smarter, faster, more responsive AI has become a kind of energy arms race. Tech giants tout efficiency gains, but the underlying logic remains extractive: more data, more compute, more power.

Meanwhile, communities near data centres face water shortages, grid strain, and rising costs—all for services they may never use.

Future direction

Where is this heading? On one side, we’ll see ‘greenwashed’ AI—models marketed as sustainable thanks to token offsets or renewable pledges. On the other, a growing movement for ‘degrowth AI’: systems designed to be lean, local, and ethically constrained. Think smaller models trained on curated datasets, prioritising transparency over scale.

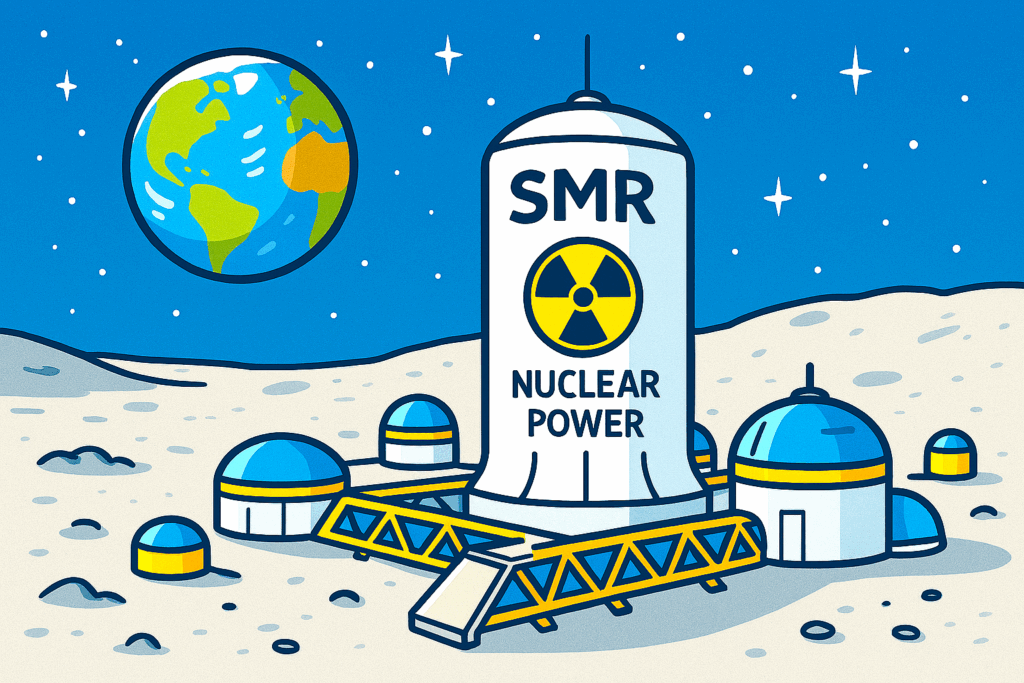

AI power – the energy hunger game! NASA’s ambition is to place nuclear power on the moon

Governments are waking up, too. The EU and UK are exploring energy disclosure mandates for AI firms, while some U.S. states are scrutinising water usage and land rights around data infrastructure. But regulation lags behind innovation—and behind marketing.

Ultimately, the energy hunger game isn’t just about watts and emissions. It’s about values. Do we want AI that mirrors our extractive habits, or one that challenges them? Can intelligence be decoupled from excess?

The next frontier isn’t smarter models—it’s wiser ones. And wisdom, unlike raw compute, doesn’t need a megawatt to shine.

Why Nuclear Is Back on the Table

Global Momentum: Thirty-one countries have pledged to triple nuclear capacity by 2050, framing it as a cornerstone of clean energy strategy.

AI’s Power Problem: With data centres projected to consume more energy than Japan by 2026, nuclear is being pitched as the only scalable, low-carbon solution that can deliver round-the-clock power.

Baseload Reliability: Unlike solar and wind, nuclear doesn’t flinch at nightfall or cloudy skies. That makes it ideal for powering critical infrastructure—especially AI, which can’t afford downtime.

🧪 Next-Gen Tech on the Horizon

Small Modular Reactors (SMRs): These compact units promise faster deployment, lower costs, and safer operation. China and Russia already have some online.

Fusion Dreams: Still experimental, but if cracked, fusion could offer near-limitless clean energy. It’s the holy grail—though still more sci-fi than supply chain.

⚖️ The Catch? Cost, Waste, and Public Trust

Nuclear remains expensive to build and politically fraught. Waste disposal and safety concerns haven’t vanished, and public opinion is split—especially in the UK.

Even with advanced designs, the spectres of Chernobyl and Fukushima linger in the cultural memory. That’s a narrative hurdle as much as a technical one.

🛰️ Moonshots and Geopolitics

NASA’s push to deploy a nuclear reactor on the moon by 2029 underscores how strategic this tech has become—not just for Earth, but for space dominance.

The U.S.–China race isn’t just about chips anymore. It’s about who controls the energy to power them.

Nuclear is staging a comeback—not as a relic of the past, but as a potential backbone of the future.

Whether it becomes the dominant force or a transitional ally depends on how fast we can build, how safely we can operate, and how wisely we choose to deploy.

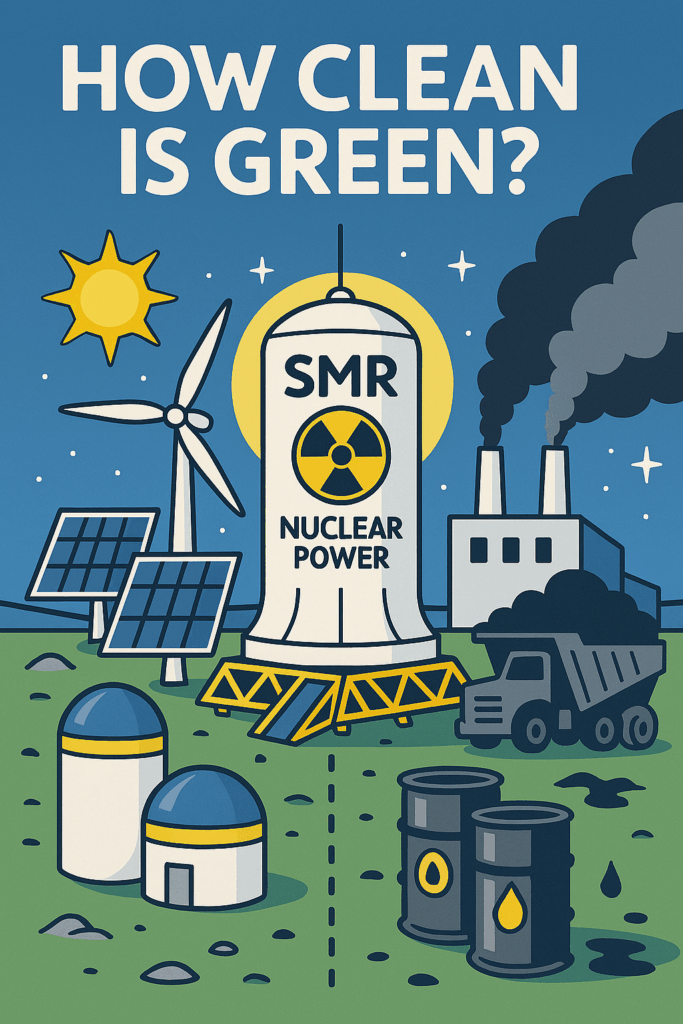

🌍 How ‘clean’ is green?

According to MIT’s Climate Portal, no energy source is perfectly clean. Even solar panels, wind turbines, and nuclear plants come with embedded emissions—from mining rare metals to manufacturing components and transporting them.

So, while they don’t emit greenhouse gases during operation, their setup and maintenance do leave a footprint.

Huawei has unveiled a bold new AI chip cluster strategy aimed squarely at challenging Nvidia’s dominance in high-performance computing.

At its Connect 2025 conference in Shanghai, Huawei introduced the Atlas 950 and Atlas 960 SuperPoDs—massive AI infrastructure systems built around its in-house Ascend chips.

These clusters represent China’s most ambitious attempt yet to bypass Western semiconductor restrictions and assert technological independence.

The technical stuff

The Atlas 950 SuperPoD, launching in late 2026, will integrate 8,192 Ascend 950DT chips, delivering up to 8 EFLOPS of FP8 compute and 16 EFLOPS at FP4 precision. (Don’t ask me either – but that’s what the data sheet says).

It boasts a staggering 16.3 petabytes per second of interconnect bandwidth, enabled by Huawei’s proprietary UnifiedBus 2.0 optical protocol. It is reportedly claimed to be ten times faster than current internet backbone infrastructure.

This system is reportedly designed to outperform Nvidia’s NVL144 cluster, with Huawei asserting a 6.7× advantage in compute power and 15× in memory capacity.

In 2027, Huawei reportedly plans to release the Atlas 960 SuperPoD, doubling the specs with 15,488 Ascend 960 chips. This reportedly will give 30 EFLOPS FP8 compute, and 34 PB/s bandwidth.

These SuperPoDs will be linked into SuperClusters. The Atlas 960 SuperCluster is reportedly projected to reach 2 ZFLOPS of FP8 performance. This potentially rivals even Elon Musk’s xAI Colossus and Nvidia’s future NVL576 deployments.

Huawei’s roadmap includes annual chip upgrades: Ascend 950 in 2026, Ascend 960 in 2027, and Ascend 970 in 2028.

Each generation promises to double computing power. The chips will feature Huawei’s own high-bandwidth memory variants—HiBL 1.0 and HiZQ 2. These are designed to optimise inference and training workloads.

Strategy

This strategy reflects a shift in China’s AI hardware approach. Rather than competing on single-chip performance, Huawei is betting on scale and system integration.

By controlling the entire stack—from chip design to memory, networking, and interconnects—it aims to overcome fabrication constraints imposed by U.S. sanctions.

While Huawei’s software ecosystem still trails Nvidia’s CUDA, its CANN toolkit is gaining traction. Chinese regulators discourage purchases of Nvidia’s AI chips.

The timing of Huawei’s announcement coincides with increased scrutiny of Nvidia in China, suggesting a coordinated push for domestic alternatives.

In short, Huawei’s AI cluster strategy is not just a technical feat—it’s a geopolitical statement.

Whether it can match Nvidia’s real-world performance remains to be seen, but the ambition is unmistakable.

On 17th September 2025, the U.S. Federal Reserve announced its first interest rate cut of 2025, lowering the benchmark federal funds rate by 0.25% to a range of 4.00%–4.25%.

The decision follows nine months of monetary policy stagnation and comes amid mounting evidence of a weakening labour market and persistent inflationary pressures.

Fed Chair Jerome Powell described the move as a ‘risk management cut’, citing slower job growth and a rise in unemployment as key drivers.

While inflation remains elevated—partly due to tariffs introduced by the Trump administration—the Fed opted to prioritise employment support, signalling the possibility of two further cuts before year-end.

The decision was not without controversy. New Fed Governor Stephen Miran, recently appointed by President Trump, reportedly dissented, advocating for a more aggressive half-point reduction. Political tensions have escalated, with Trump publicly urging Powell to ‘cut bigger’.

Markets responded with mixed signals: the Dow rose modestly, while the S&P 500 and Nasdaq slipped slightly. However, each improved in after-hours trading.

Analysts remain divided over the long-term impact, with some warning that easing too quickly could reignite inflation.

The Fed’s next move will be closely watched as it balances economic fragility with political crosswinds.

The next U.S. Federal Reserve meeting is scheduled for 29th–30th October 2025, with the interest rate decision expected on Wednesday, 30th October at 2:00 PM ET.

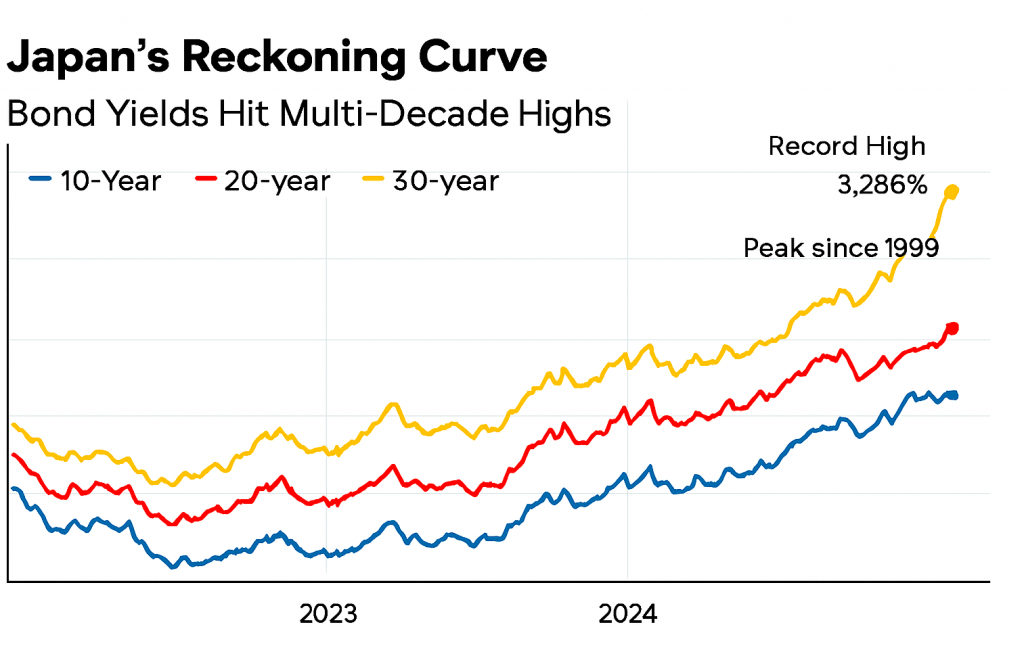

After decades of economic sedation, Japan’s long-term bond yields are rising with a vengeance.

The 30-year government bond has breached 3.286%—its highest level on record—while the 20-year yield has climbed to 2.695%, a peak not seen since 1999.

These aren’t just numbers; they’re seismic signals of a nation confronting its delayed past, now its deferred future.

Indicative Yield Curve for Japan

For years, Japan’s yield curve was a monument to inertia. Negative interest rates, yield curve control, and relentless bond-buying by the Bank of Japan created an artificial calm—a kind of economic Zen garden, raked smooth but eerily still.

That era is ending. Inflation has persisted above target for three years, and the BOJ’s retreat from monetary intervention has unleashed market forces long held at bay.

This steepening curve is more than financial recalibration—it’s a symbolic reckoning. Rising yields demand accountability: from policymakers who masked structural fragility, from investors who chased safety in stagnation, and from a society that postponed hard choices on demographics, debt, and productivity.

The bond market, once a passive witness, now acts as judge. Each basis point is a moral verdict on Japan’s economic past.

The shadows of the Lost Decades—deflation, aging populations, and overspending—are being dispelled not by command, but through the process of price discovery.

In this new era, Japan’s yield curve resembles a serpent uncoiling—no longer dormant but rising with intent.

The question isn’t whether the curve will flatten again, but whether Japan can meet the moment it has long delayed.

China’s exports to the United States fell sharply in August 2025, marking a six-month low and underscoring the growing strain in global trade dynamics.

According to recent data, shipments from China to the U.S. dropped by 33% year-on-year, reflecting both weakening demand and the ongoing effects of geopolitical tensions.

This decline is part of a broader slowdown in China’s export sector, which saw overall outbound shipments contract for the sixth consecutive month.

Analysts point to several contributing factors: tighter monetary policy in the U.S., shifting supply chains, and a cooling appetite for Chinese goods amid rising tariffs and trade barriers.

Down 33%

The 33% plunge is particularly striking given the scale of bilateral trade. The U.S. remains one of China’s largest export markets, and such a steep drop signals deeper economic recalibrations.

Sectors hit hardest include electronics, machinery, and consumer goods—industries that once formed the backbone of China’s export dominance.

Economists warn that this trend could have ripple effects across global markets. For China, it raises questions about domestic resilience and the need to pivot toward internal consumption.

For the U.S., it may accelerate efforts to diversify supply chains and invest in domestic manufacturing.

The timing is also politically charged. With President Trump’s tariff policies still in effect and China navigating its own economic headwinds, trade relations remain tense.

This downturn may prompt renewed negotiations—or further decoupling.

Despite the ongoing slump in trade, the U.S. continues to be China’s largest export destination among individual countries.

China’s electric vehicle (EV) powerhouse is rewriting the global automotive playbook—but not without homegrown company damage.

BYD, now the world’s largest EV manufacturer by volume, has been caught in the crossfire of a domestic price war.

Damaging price war

The price war is damaging margins. It is unnerving investors and revealing the perils of hyper-competition in the world’s most aggressive car market.

In Q2 2025, BYD posted a 30% drop in net profit to 6.4 billion yuan (£700 million), its first earnings decline in over three years.

Despite a 145% surge in overseas sales, the company’s sweeping discounts across 22 models have eroded profitability at home.

Gross margins slipped to around 16%, and its Hong Kong-listed shares tumbled 8% to a five-month low.

Analysts reportedly now question whether BYD can hit its ambitious 5.5-million-unit sales target, having reached only 45% by July 2025.

The price war, ignited by BYD’s aggressive cuts in May 2025, has forced rivals like Geely, Chery, and SAIC-GM to follow suit. Entry-level EVs now start below (£6,500), with features like driver assistance and smart infotainment once reserved for premium models.

But the race to the bottom has drawn concern from regulators and industry leaders. The China Association of Automobile Manufacturers (CAAM) warned of “disorderly competition”, while executives fear quality compromises and supplier strain.

Yet even as BYD stumbles, the broader Chinese EV machine is gaining global momentum. In Europe, BYD overtook Tesla in July sales, capturing 1.1% market share versus Tesla’s 0.7%.

Chinese EV car brands account for around 10% of new UK car sales

Chinese brands now account for around 10% of new car sales in the UK. There are over 30 affordable EV models priced under £30,000.

Their edge lies in battery supply chains, manufacturing efficiency, and software integration. Transforming cars into ‘smartphones on wheels’ tailored to digitally connected consumers.

China’s EV revolution is no longer just a domestic shake-up—it’s a global reordering. Legacy automakers are retreating from the budget segment. But Chinese firms flooding international markets with sleek, connected, and competitively priced vehicles.

BYD’s profit dip may be a temporary wobble. The long-term trajectory is clear: China isn’t just building cars—it’s building the future of mobility.

For global rivals, the message is unmistakable: adapt, or be outpaced by the dragon’s electric roar.

Infographic: China’s BYD and other EVs

Summary

BYD’s Q2 2025 net profit drop of 30% to 6.4 billion yuan: This figure aligns with recent earnings reports and analyst commentary. The drop is consistent with margin pressure from domestic price cuts.

Gross margin falling to 16.3%: Matches industry estimates for BYD’s automotive segment, which has seen compression due to aggressive discounting.

Overseas sales up 145% YoY: BYD’s international expansion—especially in Europe, Southeast Asia, and Latin America—has been rapid. This growth rate is plausible and supported by export data.

BYD reaching only 45% of its 5.5 million unit sales target by July: This tracks with cumulative delivery figures through mid-year, suggesting a potential shortfall unless H2 volumes accelerate.

Price war triggered by BYD’s cuts across 22 models in May: Confirmed by industry reports and BYD’s own promotional campaigns. Other automakers like Geely and Chery have responded with similar discounts.

CAAM warning of “disorderly competition”: This quote has appeared in official statements and media coverage, reflecting regulatory concern over unsustainable pricing.

Chinese EVs gaining market share in Europe and UK: BYD overtaking Tesla in July 2025 sales in Europe is supported by registration data. Chinese brands now account for ~10% of UK new car sales, with many models priced under £30,000.

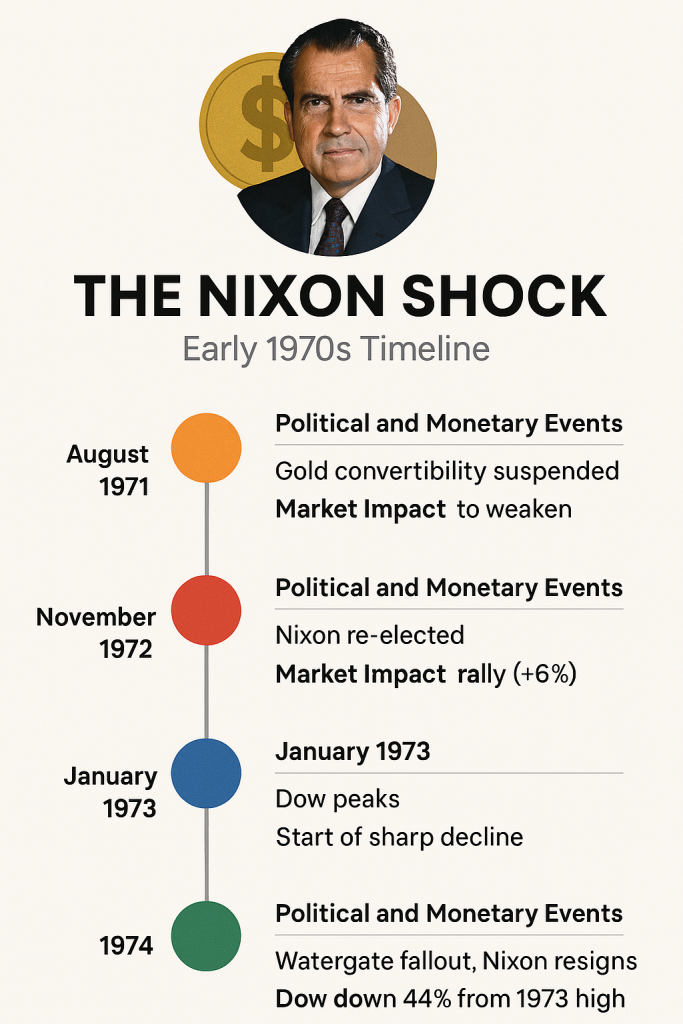

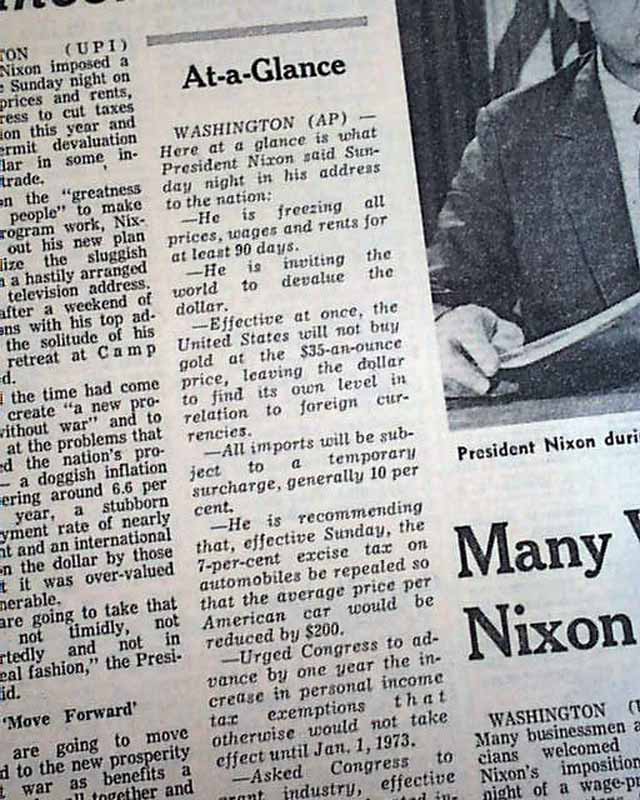

In the early 1970s, President Richard Nixon’s pursuit of re-election collided with the Federal Reserve’s independence, triggering a cascade of economic consequences that reshaped global finance.

The episode remains a cautionary tale about the dangers of politicising monetary policy.

At the heart of the drama was Nixon’s pressure on Fed Chair at the time, Arthur Burns to stimulate the economy ahead of the 1972 election. Oval Office tapes later revealed Nixon’s direct appeals for rate cuts and looser credit conditions—despite rising inflation.

Burns, reluctant but ultimately compliant, oversaw a period of aggressive monetary expansion. Interest rates were held artificially low, and the money supply surged.

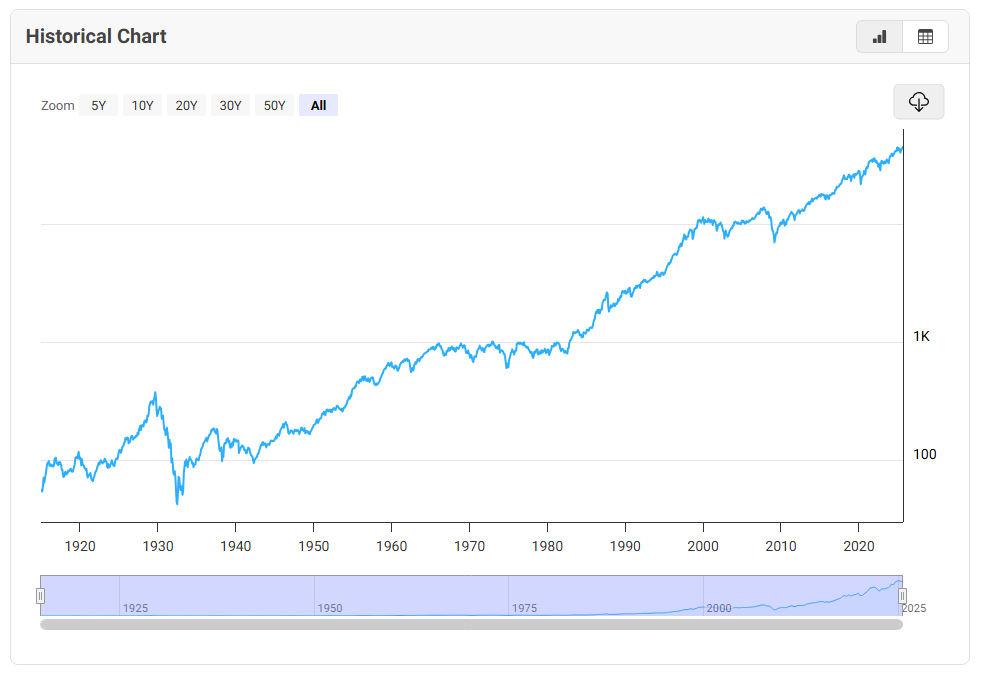

Dow historical chart – lowest 43 points to around 45,400

The short-term result was a booming economy and a landslide victory for Nixon. But the longer-term consequences were severe. Inflation, already simmering, began to boil. By 1973, consumer prices were rising at an annual rate of over 6%, and the dollar was under siege in global markets.

Then came the real shock: in August 1971, Nixon unilaterally suspended the dollar’s convertibility into gold, effectively ending the Bretton Woods system.

This move—intended to halt speculative attacks and preserve U.S. gold reserves—unleashed a new era of floating exchange rates and fiat currency. The dollar depreciated sharply, and global markets entered a period of volatility.

By 1974, the consequences were fully visible. The Dow Jones Industrial Average had fallen nearly 45% from its 1973 peak.

Politics vs the Federal Reserve – lesson learned?

Bond yields soared as investors demanded compensation for inflation risk. The U.S. economy entered a deep recession, compounded by the oil embargo and geopolitical tensions.

The Nixon-Burns episode is now widely viewed as a breach of central bank independence. It demonstrated how short-term political gains can lead to long-term economic instability.

The Fed’s credibility was damaged, and it took nearly a decade—culminating in Paul Volcker’s brutal rate hikes of the early 1980s—to restore price stability.

Today, as debates over Fed autonomy resurface, the lessons of the 1970s remain urgent. Markets thrive on trust, transparency, and institutional integrity. When those are compromised, even the most powerful economies can falter.

THE NIXON SHOCK — Early 1970’s Timeline

🔶 August 1971Event: Gold convertibility suspended Market Impact: Dollar begins to weaken Context: Nixon ends Bretton Woods, launching the fiat currency era

🔴 November 1972Event: Nixon re-elected Market Impact: Stocks rally briefly (+6%) Context: Fed policy remains loose under political pressure

🔵 January 1973Event: Dow peaks Market Impact: Start of sharp decline Context: Inflation accelerates, investor confidence erodes

🟢 1974Event: Watergate fallout, Nixon resigns Market Impact: Dow down 44% from 1973 high Context: Recession deepens, Fed credibility damaged.

Current dollar dive, stocks boom and bust (the Dow fell 19% in a year and then by 44% in 1975 from its January 1973 peak). U.S. 10-year Treasury yields surged (peaking at nearly 7.60% -close to twice today’s yield).

In hindsight, Nixon won the election—but lost the economy. And the Fed, caught in the crossfire, paid the price in credibility. It’s a reminder that monetary policy is no place for political theatre.

Is history repeating itself? Is Trump’s involvement different, or another catastrophe waiting to happen?

Where is the standard for the tariff line? Is this fair on the smaller businesses and the consumer? Money buys a solution without fixing the problem!

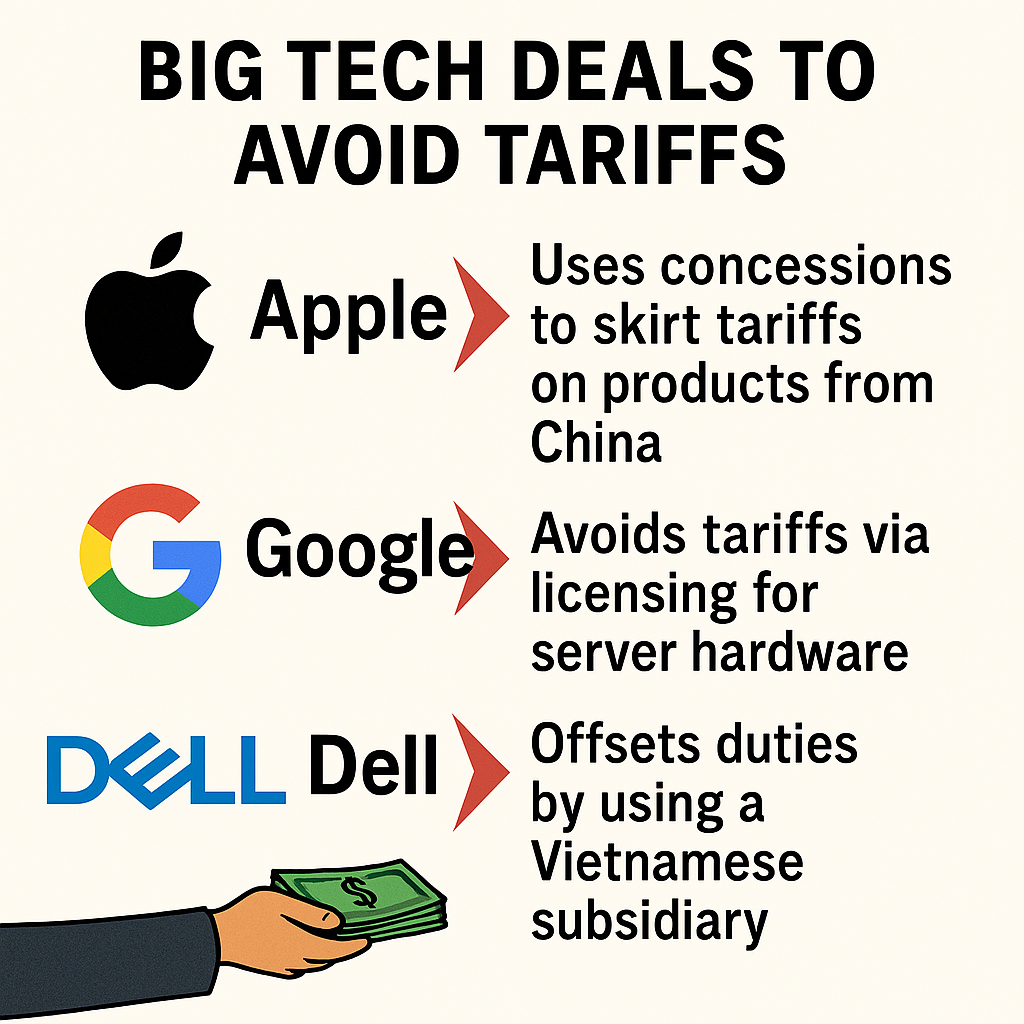

Nvidia and AMD have struck a deal with the U.S. government: they’ll pay 15% of their China chip sales revenues directly to Washington. This arrangement allows them to continue selling advanced chips to China despite looming export restrictions.

Apple, meanwhile, is going all-in on domestic investment. Tim Cook announced a $600 billion U.S. investment plan over four years, widely seen as a strategic move to dodge Trump’s proposed 100% tariffs on imported chips.

🧩 Strategic Motives

These deals are seen as tariff relief mechanisms, allowing companies to maintain access to key markets while appeasing the administration.

Analysts suggest Apple’s move could trigger a ‘domino effect’ across the tech sector, with other firms following suit to avoid punitive tariffs.

Tariff avoidance examples

⚖️ Legal & Investor Concerns

Some critics call the Nvidia/AMD deal a “shakedown” or even unconstitutional, likening it to a tax on exports.

Investors are wary of the arbitrary nature of these deals—questioning whether future administrations might play kingmaker with similar tactics.

Big Tech firms are striking strategic deals to sidestep escalating tariffs, with Apple pledging $600 billion in U.S. investments to avoid import duties, while Nvidia and AMD agree to pay 15% of their China chip revenues directly to Washington.

These moves are seen as calculated trade-offs—offering financial concessions or domestic reinvestment in exchange for continued market access. Critics argue such arrangements resemble export taxes or political bargaining, raising concerns about legality and precedent.

As tensions mount, these deals reflect a broader shift in how tech giants navigate geopolitical risk and regulatory pressure.

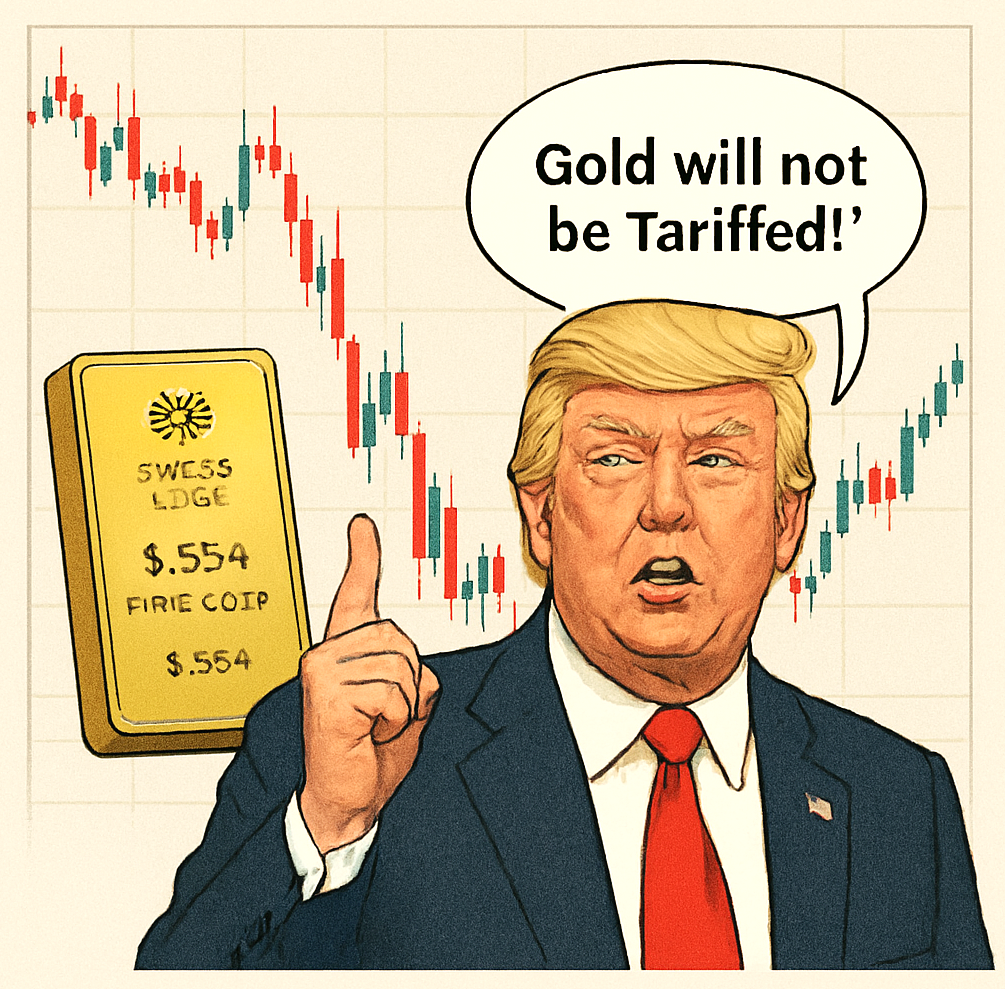

Trump’s latest flurry of tariff U-turns has left global markets whiplashed but oddly resilient.

From threatening Swiss gold bars with a 39% levy to abruptly tweeting ‘Gold will not be Tariffed!’ The former president’s reversals have become a hallmark of his political tactic.

Investors now brace for volatility not from policy itself, but from its rapid retraction. With China tariffs delayed, praise for previously criticised CEOs, and shifting stances on Ukraine and Russia, Trump’s tactics seem less about strategy and more about spectacle.

Yet despite the chaos, markets appear unfazed—suggesting that unpredictability may now be priced in

🧠 Why So Many U-Turns?

Market Sensitivity: Many reversals follow stock market dips or investor backlash.

Diplomatic Pressure: Allies like Switzerland, India, Ukraine, Canada and Australia have pushed back hard.

Narrative Control: Trump often uses Truth Social to pivot public messaging rapidly.

Strategic Ambiguity: Some analysts argue it’s part of a negotiation tactic—others call it chaos.

🔁 Latest Trump U-Turns

Topic

Initial Position

Reversal

Date

Gold Tariffs

Swiss gold bars to face 39% tariff

Trump tweets “Gold will not be Tariffed!”

7 Aug 2025

China Tariffs

145% reciprocal tariffs to begin

Delayed for 90 days

12 Aug 2025

Intel CEO Lip-Bu Tan

“Must resign, immediately”

“His success and rise is an amazing story”

11 Aug 2025

Russia-Ukraine Arms

Paused military aid to Ukraine

Resumed shipments after backlash

8 Jul 2025

India’s Role in Peace Talks

Criticised India’s neutrality

Praised India’s diplomatic efforts

9 Aug 2025

Global Tariffs

Imposed sweeping import taxes

Suspended most tariffs within 13 hours

9 Apr 2025

Epstein Files

Promised full declassification

Now downplaying and deflecting

Ongoing

TACO – Trump Always Chickens Out! Tactics or turmoil?

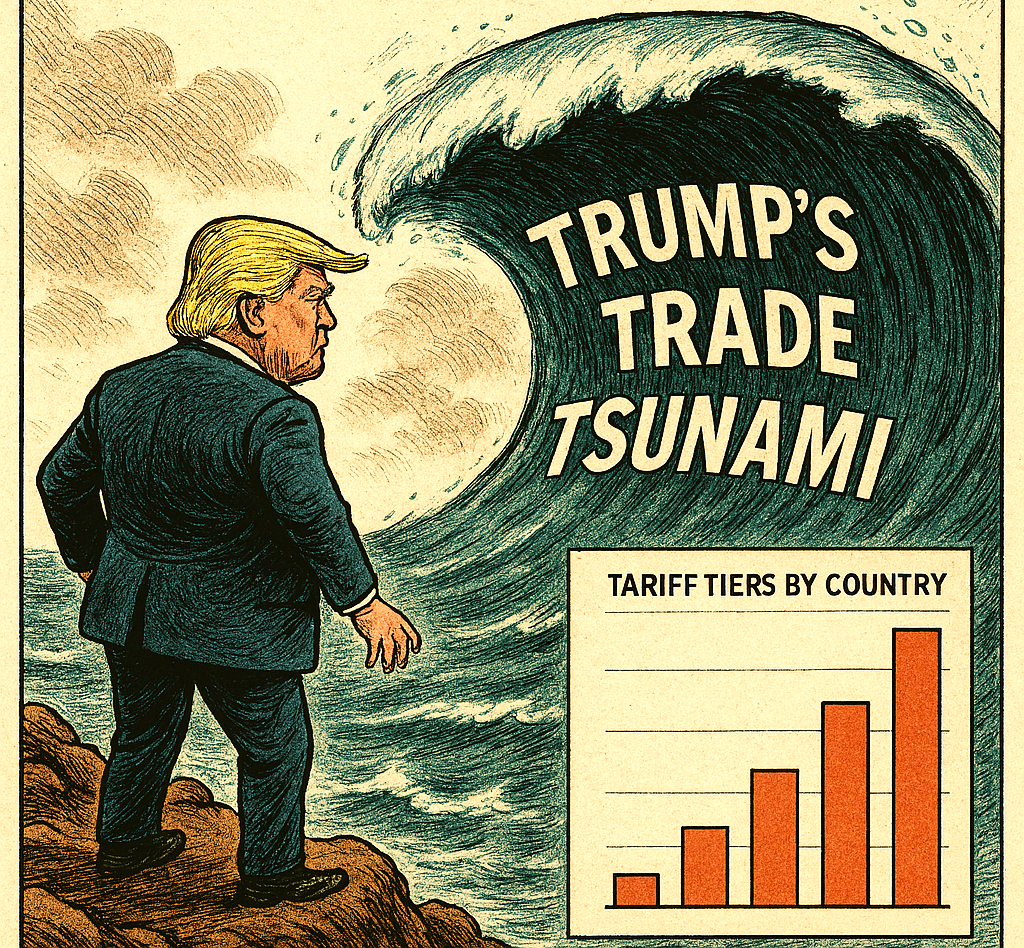

Despite the scale and aggression of Donald Trump’s 2025 tariff attack—averaging approximately 27% and targeting nearly 100 countries—financial markets have shown a surprisingly muted response.

Here’s a breakdown of why that might be

🧠 1. Markets Have Priced in the Chaos

Trump’s protectionist rhetoric and erratic trade moves have been a fixture since his first term. Investors have grown desensitized to tariff threats and now treat them as part of the geopolitical noise.

The April ‘Liberation Day’ announcement triggered initial volatility, but subsequent delays, exemptions, and partial deals (e.g. with the UK, EU, Japan) softened the blow.

🧮 2. Selective Impact and Exemptions

Tariffs are not blanket: electronics, smartphones, and some pharmaceuticals are exempt.

Countries like the UK and Australia face relatively low rates (10%), while others like Brazil and Switzerland are hit harder (50% and 39%).

For India, even the steep 50% tariff affects only 4.8% of its global exports.

🔄 3. Supply Chain Adaptation

Companies are already pivoting manufacturers are reshoring or shifting production to tariff-friendly countries like Vietnam and Bangladesh.

Agri-tech and automation investments are helping offset cost pressures in affected sectors.

💰 4. Short-Term Pain, Long-Term Strategy

The US expects $2.4 trillion in tariff revenue by 2035, despite $587 billion in dynamic losses.

Investors are recalibrating portfolios toward resilient sectors (semiconductors, automation) and geographic diversification.

🧊 5. Political Fatigue and Uncertainty Premium

Trump’s tariff moves are seen as political theatre, especially with his threats often followed by renegotiations or delays.

Markets may be holding back deeper reactions until retaliatory measures (especially from China) fully materialise.

Where now?

These tariffs spanned sectors from automotive and pharmaceuticals to semiconductors—where a 100% duty was imposed unless firms manufactured in the U.S.

While Trump framed the measures as a push to revive domestic industry and reduce trade deficits, critics argued they were legally dubious and economically disruptive, with a federal court later ruling them unconstitutional.

Despite the aggressive scope, global markets showed surprising resilience, suggesting investors had grown desensitised to Trump’s brinkmanship and were instead focusing on broader economic signals.

On 7th August 2025, the Bank of England’s Monetary Policy Committee voted narrowly—5 to 4—in favour of reducing the base interest rate by 0.25% to 4%, marking its lowest level since March 2023.

This is the fifth rate cut in a year, aimed at stimulating growth amid sluggish GDP and persistent inflation, which currently stands at 3.6%.

Governor Andrew Bailey reportedly described the decision as part of a ‘gradual and careful’ easing strategy, balancing inflation risks with signs of a softening labour market.

While some committee members reportedly advocated for a larger cut, others urged caution, reflecting deep divisions over the UK’s economic trajectory.

The move is expected to ease borrowing costs for homeowners and businesses, with tracker mortgage rates falling immediately. However, savers will be losing out as rates continue to drop.

However, analysts warn that future cuts may hinge on upcoming fiscal decisions and inflation data, leaving the path forward uncertain.

President Donald Trump has announced a sweeping 100% tariff on imported semiconductors and microchips—unless companies are actively manufacturing in the United States.

The move, unveiled during an Oval Office event with Apple CEO Tim Cook, is aimed at turbocharging domestic production in a sector critical to everything from smartphones to defence systems.

Trump’s vow comes on the heels of Apple’s pledge to invest an additional $100 billion in U.S. operations over the next four years.

While the tariff exemption criteria remain vague, Trump emphasised that firms ‘committed to build in the United States’ would be spared the levy.

The announcement adds pressure to global chipmakers like Taiwan Semiconductor (TSMC), Nvidia, and GlobalFoundries, many of which have already initiated U.S. manufacturing projects.

According to the Semiconductor Industry Association, over 130 U.S.-based initiatives totalling $600 billion have been announced since 2020.

Critics warn the tariffs could disrupt global supply chains and raise costs for consumers, while supporters argue it’s a bold step toward tech sovereignty.

With AI, automotive, and defence sectors increasingly reliant on chips, the stakes couldn’t be higher.

Whether this tariff threat becomes a turning point or a trade war flashpoint remains to be seen.

Trump has a habit of unravelling as much as he ‘ravels’ – time will tell with this tariff too.