China’s Hong Kong‑listed tech stocks have slipped decisively into a bear market, with the Hang Seng Tech Index now more than 20% below its October 2025 peak.

The downturn is being driven by a potent mix of tax concerns and global anxiety over the disruptive pace of artificial intelligence.

China’s Hong Kong‑listed technology sector has entered a sharp reversal after last year’s rally, with the Hang Seng Tech Index falling and officially breaching bear‑market territory.

The decline reflects a broader shift in sentiment as investors reassess the risks facing the sector.

AI Disruption and Global Risk Aversion

While tax worries have been widely cited, the global ‘AI effect’ is proving equally influential. Investors are increasingly concerned that rapid advances in artificial intelligence could reshape competitive dynamics across the tech landscape.

Companies perceived as lagging in AI development face heightened scrutiny, while uncertainty over regulatory responses adds further pressure.

This has contributed to a wave of risk aversion, particularly toward Chinese firms already navigating geopolitical and policy headwinds.

Policy Anxiety and VAT Concerns

Fears of potential tax hikes — including a possible increase in value‑added tax on internet services — have amplified the sell‑off.

Recent VAT changes in telecom services have made markets more sensitive to policy signals, prompting investors to reassess earnings expectations for major platform companies.

A Reversal of Momentum

The speed of the downturn has surprised many, given the strong rebound seen in 2025. Yet the combination of AI‑driven uncertainty, shifting regulatory expectations, and global market caution has created a challenging backdrop for Chinese tech stocks.

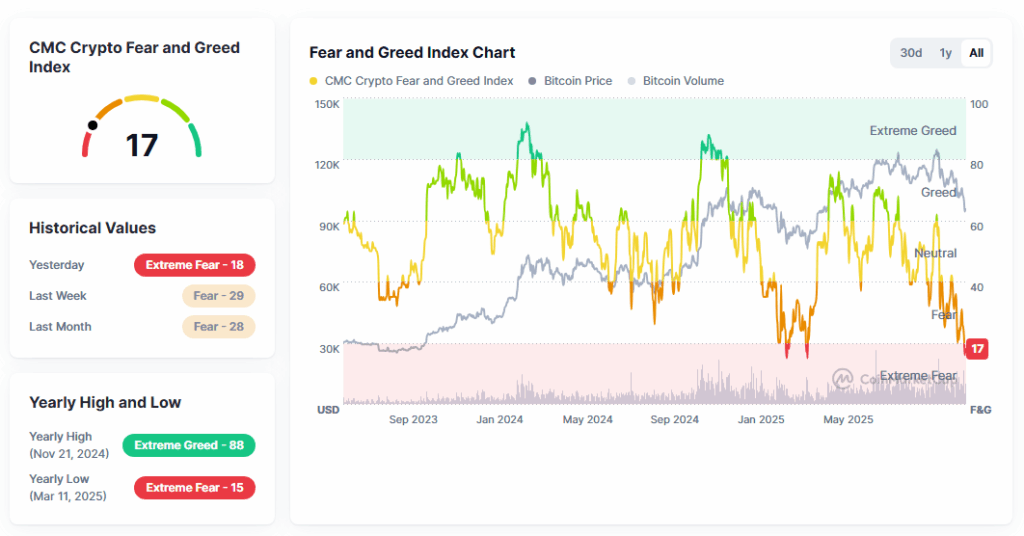

With sentiment fragile, analysts warn that volatility may persist until investors gain clearer visibility on both policy direction and the sector’s ability to adapt to accelerating AI disruption.

Is it coming to western stocks – especially in the U.S.?

It’s certainly possible that a similar dynamic could wash across Western markets, though not necessarily in the same form.

The extraordinary concentration of returns in a handful of U.S. mega‑cap AI leaders has created a structural imbalance: if investors begin to doubt the durability of AI‑driven earnings, or if regulatory pressure intensifies, the correction could be sharp because so much capital is leaning in the same direction.

Europe, meanwhile, faces a different vulnerability — a chronic under‑representation in frontier AI, which could leave its tech sector exposed if global capital rotates aggressively toward firms with demonstrable AI scale.

None of this guarantees a bear market, but the ingredients are present: stretched valuations, high expectations, and a technology cycle moving faster than many business models can adapt.

U.S. software companies are gradually feeling the impact—how long before the U.S. AI sector experiences a correction?