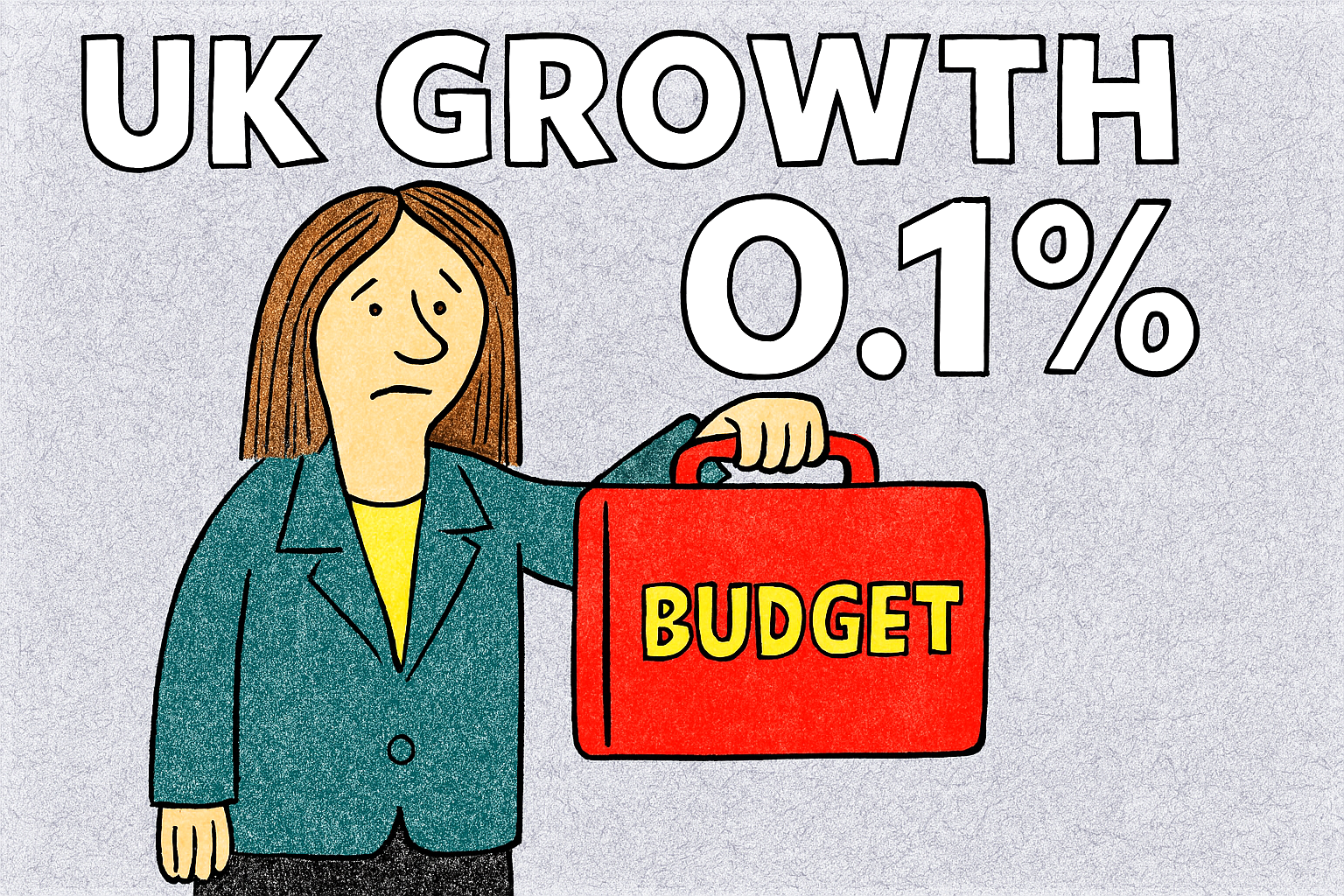

The Office for National Statistics confirmed that GDP expanded by a mere 0.1% between July and September 2025, down from 0.3% in the previous quarter and below economists’ low expectations of 0.2%.

This ‘painstakingly low and feeble growth’ reflects weak consumer demand, faltering production, and persistent inflationary pressures.

For Chancellor Rachel Reeves, who will deliver her Budget on 26th November 2025, the numbers present a difficult backdrop. With unemployment edging higher and household finances under strain, calls for fiscal support are intensifying.

Yet speculation continues that Reeves will likely opt for tax rises to shore up public finances, a move that risks dampening already fragile growth.

The Bank of England may provide some relief if it cuts interest rates at its final meeting of the year, but monetary easing alone cannot offset structural weaknesses.

Business investment remains subdued, and September’s 2% drop in manufacturing output highlights the challenges facing industry. The JLR debacle didn’t help.

The Budget will therefore be a balancing act: stimulating growth without undermining fiscal credibility.

Today’s figures underline the urgency of that task.

Note:

Rachel Reeves’ 2024 Autumn Budget aimed to lay the groundwork for long-term growth, but it was not widely seen as a ‘growth budget’.

Many business leaders and analysts criticised it for dampening entrepreneurial momentum.

Reeves framed her first Budget as a reset for economic stability, following Labour’s July 2024 election win.

And here we are one year on from 2024 budget with virtually ZERO growth.

So, where now?