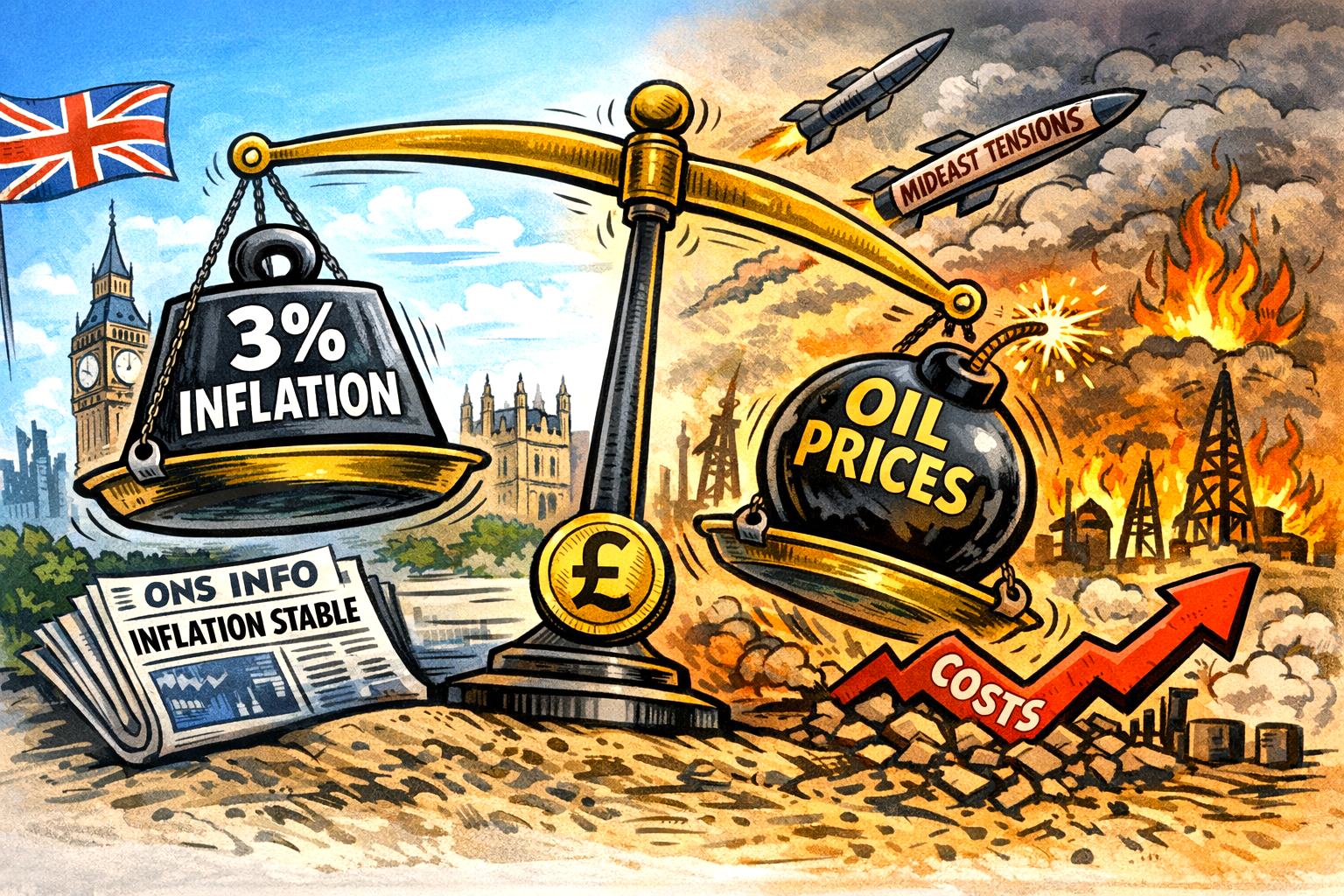

The UK’s inflation rate remained unchanged at 3% in February, according to the latest figures from the Office for National Statistics.

After months of gradual easing, the pause reflects a delicate moment for the UK economy, with price pressures beginning to shift beneath the surface.

Clothing was the biggest upward driver, with prices rising this year after falling during the same period in 2025.

This was offset by cheaper petrol, though those figures were captured before the recent surge in global oil prices triggered by the outbreak of war involving Iran.

While inflation is far below the peaks seen a few years ago, households are still contending with the reality that prices continue to rise—just more slowly.

ONS data

The ONS also introduced supermarket scanner data for the first time, offering a more accurate picture of food costs.

Economists warn that the conflict‑driven spike in oil and gas prices could push inflation higher again later in the year, with some forecasts suggesting a potential rise towards 4.6%.

Businesses already reliant on fuel, such as regional bus operators, report steep cost increases that may soon feed through to consumers.

The government insists it is working to ease cost‑of‑living pressures, though global events may limit its room for manoeuvre.