In his Capitol Hill testimony on 6th March 2024, Federal Reserve Chairman Jerome Powell reiterated that was not yet time to begin cutting interest rates.

To fight inflation, which reached a rate of 9% in the summer of 2022, the central bank has significantly increased interest rates in recent times. However, prices are still stubborn, especially for things like housing and groceries.

Due to the robust economic performance in early 2024, the expected reduction in interest rates has been postponed. Instead of taking place this month, the rate cuts are now more probable in May or June 2024.

Powell reportedly said: ‘The Committee does not expect that it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.’

He reiterated the pledge to lower inflation to the 2% target and keep long-term inflation expectations stable.

UPDATE

On Thursday 7th March 2024 Powell also said: the Fed is ‘not far’ from the point of cutting interest rates

UK interest rates have been left unchanged at 5.25% by the Bank of England as widely expected by commentators.

It is the fourth time in a row the Bank has held rates at 5.25%.

The Bank of England had previously raised rates 14 times in a row to curb inflation, leading to increases in mortgage rates but also creating better rates for savers.

Interest rate chart from 2007 to January 2024 demonstrates just how low interest were between 2009 and 2022

Interest rate chart from 2007 to January 2024 demonstrates just how low interest were between 2009 and 2022

Attitude shift

There is a noticeable shift in opinion as the committee entertained the possibility of discussing the feasibility of cuts.

There was a three-way split, with two members of the Monetary Policy Committee (MPC) voting to increase the bank rate to 5.5%; one to reduce it to 5%; and six were in favour of sticking with 5.25%.

With inflation falling it is very likely the interest rates will be reduced by 0.25% by March 2024. Just take a look at the reduction in savers rates that have already occurred.

The anticipation is for a rate reduction soon.

The clue is that savers rates are being cut.

But

The Bank of England Governor, Andrew Bailey, has made clear that for him the key question is: ‘For how long should we keep rates at the current level?’

There may be disappointment ahead then – but a rate cut is next and I still expect it by Easter.

The Federal Open Market Committee (FOMC) held interest rates steady and indicated a willingness stop raising interest rates.

But a cut anytime soon is unlikely until inflation is brought fully under control and nearer to the Fed’s 2% inflation target.

The Federal Reserve sent a signal that it is finished with raising interest rates but made it clear that it is not ready to start cutting, just yet. It also said there are no plans yet to cut rates with inflation still running above the central bank’s target.

Federal Reserve interest targets and increases since 2022 to January 2024

Turkey’s central bank on Thursday 25th January 2024 hiked its key interest rate to 45%.

It comes amid an ongoing struggle against double-digit inflation for Turkey’s policymakers, with the rate hike the latest step in that ongoing fight.

30 Turkish Lira to 1 U.S. dollar

Inflation in Turkey increased nearly 65% year-on-year in December 2023, up from 62% in November, and the country’s currency, the lira, hit a new record low against the U.S. dollar earlier in January 2024 at 30 Lira to $1.

Analysts predict this will be the last hike for some time, especially with local elections approaching in March 2024

Inflation, rose marginally to 4% in December, up from 3.9% in November 2023.

Economists had forecast a slight fall but unexpected rises in alcohol and tobacco prices were behind the surprise rise.

However, with energy bills predicted to come down in 2024, there are still expectations of interest rate cuts later this year.

On target still for 2%?

As we have seen in the Germany, the U.S., and France, inflation does not fall in a straight line, ‘but our plan is working and we should stick to it,‘ Jeremy Hunt reportedly said in a statement.

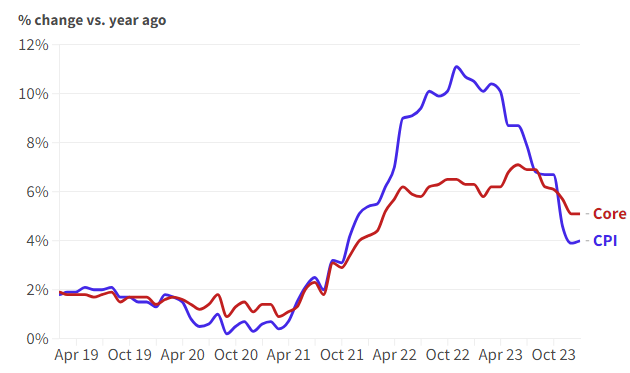

UK inflation from April 2019 to December 2023

UK inflation from April 2019 to December 2023

Unprepared for both the start and the end of the pandemic

Increases in the cost of energy and food costs, started by pandemic lockdowns ending exasperated further by Russia’s invasion of Ukraine and more recently the conflict in Israel have put household finances under extreme pressure.

The UK and other countries were woefully underprepared for all of these events as they ‘began’ and at the ‘end’. We did not prepare to come out of them – there was no exit plan!

Markets and traders are still expecting BoE to cut its base rate in 2024 due to the fast-falling inflation rate. It peaked at 11.1% in October 2022 – and now sits at 4%.

The question is: will the economic recovery be good enough to allow the Bank of England to start cutting rates?

The UK interest rate currently sits at 5.25%.

‘What’s inflation?’ ‘Dunno, but my beer’s gone up!’

Federal Reserve officials in December concluded that interest rate cuts are likely in 2024, though they appeared to provide little in the way of when that might occur, according to minutes from the meeting released Wednesday 3rd January 2024.

FOMC meeting minutes

The rate-setting Federal Open Market Committee (FOMC) agreed to keep its rate steady in a range between 5.25% and 5.5%. Members indicated they expect 0.75% cut by the end of 2024.

Uncertainty

However, the meeting summary noted a high level of uncertainty over how, or even if, that will happen. Markets have reacted negatively to this news.

The minutes noted an unusually elevated degree of uncertainty about the policy path. Several members said it might be necessary to keep the funds rate at an elevated level if inflation doesn’t cooperate, and others noted the potential for additional increases.

But, despite this cautionary tone from Fed officials, markets expect the central bank to cut rates in 2024.

Dot plot

The dot plot of individual members’ indications released following the meeting showed that members expect cuts over the coming three years. This will bring borrow back to the 2% desired target.

The minutes indicated that clear progress had been made against inflation, with a six-month measure of personal consumption expenditures even indicating that the inflation rate has edged below the Fed’s 2% target.

FOMC Dot plot projections through 2026

However, the document also noted that progress has been uneven across sectors, with energy and core goods moving lower but core services still moving higher.

The Dot plot – what is it?

The dot plot, in relation to the FED or FOMC, is a chart that shows the projections of the Federal Reserve Board members and Federal Reserve Bank presidents for the federal funds rate, which is the interest rate that U.S. banks charge each other for overnight loans.

The dot plot is updated four times a year, after each FOMC meeting, and reflects the individual views of the policymakers on the appropriate level of the federal funds rate for the current year, the next few years, and the longer run.

The graph (dot plot) can help markets and the general public understand the Fed’s monetary policy stance and expectations for the future path of interest rates.

However, the dot plot is not a policy commitment or a forecast, but rather a snapshot of the opinions of the FOMC participants at a given point in time. The dot plot can change over time as new information and economic conditions develop.

Mortgage lenders have started 2024 by cutting interest rates.

The UK’s biggest lender, the Halifax, has cut some interest rates by nearly a full 1%, with other lenders expected to follow suit. HSBC has announced it will also make cuts in January.

Halifax is reducing its rates, with interest on a two-year fixed deal being cut by up to 0.83%. HSBC is due to reduce rates on its two-year fixed rate for remortgages (for someone with at least 40% equity in their home) falling below 4.5% for the first time since early June last year.

Mortgage rate chart October 2021 – January 2024

The Bank of England’s (BoE) benchmark interest rate has been held three times at 5.25%, analysts now expect the next move to be down.

Federal Reserve members, in their most recent meeting, gave little indication of cutting interest rates anytime soon, particularly as inflation remains well above their goal of 2%, according to minutes released Tuesday 21st November 2023.

The detail of the meeting held 31st October – 1st November 2023, showed that Federal Open Market Committee (FOMC) members are still concerned that inflation could be stubborn or move higher, and that more may need to be done.

They indicated that policy would need to stay ‘restrictive’ at the very least, inflation is on a convincing move back to the central bank’s 2% goal.

Observing the data available at CME FedWatch the stock market does not seem to expect the Fed to start cutting rates aggressively anytime soon, this opinion is based on the current pricing data of the fed-funds futures market.

According to the CME FedWatch Tool, the probability of a rate cut in the next FOMC meeting on 13th December 2023 is very low. It is likely interest rates will be left unchanged.

The market seems to expect the Fed will hold the current rate of 5.25% until at least March 2024, but will then gradually lower it to 4.75% by December 2024.

The market seems to be more optimistic about the U.S. economic outlook and the Fed’s ability to control inflation. The mood on rates has been buoyed recently with inflation data coming in better than expected.

It is highly likely that the Fed will have to cut rates more aggressively in 2024 and 2025 to stimulate the economy and avoid a potential prolonged recession.

Fed Chair Jerome Powell reportedly said he and his colleagues remain steadfast in getting policy in line with their 2% inflation target, but ‘we are not confident that we have achieved such a stance’.

He stressed the Fed nevertheless can be cautious as the risks between doing too much and too little have come into closer balance.

Federal Reserve Chairman Jerome Powell reportedly said Thursday 9th November 2023 that he and his fellow policymakers are encouraged by the slowing pace of inflation but are unsure whether they’ve done enough to keep the momentum going.

Inflation battle

Speaking a little more than a week after the central bank voted to hold rates steady, Powell said in remarks aimed at the International Monetary Fund (IMF) gathering in Washington, D.C., that more work could be ahead in the battle against high prices.

The statement comes with inflation still well above the Fed’s long-standing goal but also considerably below its peak levels in the first half of 2022. After 11 U.S. rate hikes, we have witnessed the most aggressive policy tightening since the early 1980s, the FOMC have increased rates from pretty much zero to a range of 5.25%-5.5%.

Those increases have coincided with the Fed’s preferred inflation gauge, the core personal consumption expenditures price index, to fall to an annual rate of 3.7%, from 5.3% in February 2022. The more widely followed consumer price index peaked above 9% in June of last year.

Progress

Powell referenced the progress the economy has made. Gross domestic product (GDP) accelerated at a ‘quite strong’ 4.9% annualised pace Q3 2023, though Powell also said the expectation is for growth to ‘moderate in coming quarters’. He described the economy as ‘just remarkable’ in 2023 in the face of a broad expectation that a recession was inevitable.

Nothing like a massive ‘self-pat’ on the back for a job well-done? Remember the Fed’s initial analysis? IT was for inflation to be ‘transitory’. They didn’t get that right either.

Futures pricing, according to the CME Group, suggested there’s less than a 10% chance that the FOMC will approve a final rate hike at its Dec. 12-13, 2023, meeting, even though committee members in September pencilled in an additional 0.25% rise before the end of 2023.

Impression drawing of Fed Chair. The Fed is ‘not confident’ according to Jerome Powell.

Traders anticipate the Fed will start cutting rates next year, probably around June 2024.

The U.S. central bank has held its key interest rate at its current 22-year high as it seeks to stabilise price increases, which had recently reached near-record levels.

The Federal Reserve’s rate remains at 5.25%-5.5%.

The bank has been raising interest rates in an attempt to tame the economy and slow inflation, (the rate at which prices rise). Recent data showed the U.S. economy grew faster than expected.

Raising interest rates is a way for central banks tackle rising inflation. The idea is that by raising interest rates and making it more expensive to borrow, consumers will spend less and that would lead to slower price rises. In the U.S. however, the consumer is not slowing down. This may lead to higher rates, or higher for longer which in turn could push the U.S. into a recession.

The bank had faced criticism, with some suggesting that holding interest rates at higher levels could put the U.S. economy at risk of entering a recession.

House prices had the biggest monthly rise in October for more than a year, according to the Nationwide Building Society.

However, they were still down sharply on a year ago, the UK’s biggest building society noted. The rise in prices was most likely due to there not being enough properties to meet demand.

However, activity in the housing market is still extremely slow, as buyers struggle with higher mortgage rates.

Interest rates, which underpin mortgage pricing, have moderated recently but they are still well above the lows of 2021. The Bank of England has raised interest rates from lows of around 0.1% to 5.25% in its inflation battle.

Central banks, 18 months ago got it fundamentally wrong and they got it wrong on many other occasions too.

So why take any notice?

The Fed and other central banks insisted that inflation would be ‘transitory’ – it wasn’t. It reached 7%. That’s 5% above the target of 2%.

Along with the misdiagnosis on prices, Fed officials, according to projections released in March 2022, collectively saw the key interest rate rising to just 2.8% by the end of 2023. It is now 5.25%.

The Great Depression (1929–1939) was an economic bomb that affected countries across the world. It was a period of severe economic depression after a major fall in stock prices in the United States. It began around September 1929 and led to the Wall Street stock market crash on 24th October 1929 (Black Thursday). See Wikipedia article here.

It was the longest, deepest, and most widespread depression of the 20th century.

The Great Depression of 1929

The Great Inflation

The Fed pursued an overly expansionary monetary policy in the 1960s and 1970s, which fueled high inflation and eroded the value of the dollar. The Fed also underestimated the impact of oil shocks and other supply shocks on inflation and was slow to tighten monetary policy to restore price stability. The Fed eventually raised interest rates sharply in the late 1970s and early 1980s, which triggered a severe recession. And in1991 inflation surged to 8.5%.

The Great Recession

The Fed likely contributed to the build-up of financial imbalances and excessive risk-taking in the 2000s, (Dotcom bubble) – by keeping interest rates too low for too long and by failing to adequately supervise and regulate the financial system.

The Fed likely contributed to the build-up of financial imbalances and excessive risk-taking in the 2000s

The Fed also reacted too slowly to the emerging signs of distress in the housing market and the financial sector and was unprepared for the global financial crisis that erupted in 2008. Remember, ‘sub-prime’ lending. We can see signs of similar stress in the U.S. car loan market now.

The Fed and other central banks including the Bank of England initially underestimated the severity and duration of the pandemic and its impact on the economy. The Fed also overestimated the transitory nature of inflation, which surged to a 30-year high in 2021 due to supply chain disruptions, pent-up demand, fiscal stimulus, and base effects. The Fed maintained an ultra-accommodative monetary policy stance for too long, despite mounting evidence of overheating and inflationary pressures.

The Fed finally raised interest rates by 0.75% in December 2022, but faced criticism for being behind the curve and for communicating poorly with the markets.

Transitory inflation

The Fed said inflation would be transitory in 2021 and 2022. The Fed used this term to describe the higher-than-normal prices that emerged during the Covid-19 economic crisis, which were expected to be temporary and not part of a long-term trend. The Fed attributed the inflation surge to factors such as supply chain bottlenecks, pent-up demand, fiscal stimulus, and base effects.

The Fed also said that it would let inflation run above its 2% target for some time, to achieve an average inflation rate of 2% over time. However, as inflation remained high and persistent in 2021 and 2022, the Fed faced criticism for being behind the curve and for communicating poorly with the markets. The Fed eventually raised interest rates.

And now, much of the same. The Fed is again ‘tinkering’ with policy to manage ‘transitory’ inflation and will most probably engineer a recession as a result.

The average rate on the popular 30-year fixed mortgage rose to 7.72% on Tuesday 3rd October 2023, according to latest data

Mortgage rates follow loosely the yield on the 10-year Treasury, which has been climbing this week following strong economic data. Rates have not been this high since the end of 2000.

At the beginning of this year, the 30-year fixed rate dropped mortgage to around 6%, creating a short-lived burst of activity in the spring 2023. But it began rising steadily again over the summer months, causing sales to drop, despite strong demand. The current trend appears to be even higher, with the possibility of rates reaching over 8%.

U.S. mortgage rates, which are close to 8% according to some sources. This is a very high level compared to the recent years, and it may have significant implications for the housing market and the economy.

Main points

Some experts believe that rates could reach 8% later by the end of October, and possibly stay at that level for the remainder of the year. Others, however, think that rates may stabilize or decline slightly if the economic growth slows down or inflation eases.

30 year fixed mortgage rate at 7.72%

The average rate on the popular 30-year fixed mortgage rose to 7.72% as of Oct. 3, according to Mortgage News Daily. This is the highest rate since 2000.

Rates are rising as more economic indicators point to a strong U.S. economy, which increases the likelihood of the Federal Reserve to hike rates further. The 10-year Treasury yield, which closely tracks the mortgage rates, reached 4.8% on Tuesday, the highest level since August 2007.

Hitting 8% will be like crossing a psychological barrier for many buyers, as it will increase their monthly payments and reduce their affordability. It may also dampen the demand for housing, which has already been affected by low inventory and high prices.

Some buyers are already seeing 8% mortgage rates, especially those who have high loan-to-value ratios, high balance-conforming loans, or non-qualified mortgage loans. These could also be borrowers with lower credit scores or non-prime borrowers.

UK interest rates have been left unchanged at 5.25% by the Bank of England (BoE).

The decision comes a day after figures revealed an unexpected slowdown in UK nflation in August 2023.

The Bank had previously raised rates some14 times in a row to tackle inflation, leading to increases in mortgage payments, business loans and consumer borrowing. But it also delivered higher savings rates.

The Federal Reserve held interest rates steady in a decision released Wednesday 20th September 2023, while also indicating it still expects one more hike before the end of the year and fewer cuts than previously indicated next year.

That final increase, if realised, would be it for now according to data released at the end of the Fed two-day meeting. If the Fed goes ahead with the move, it would be the twelfth rate hike since policy tightening began in March 2022.

No change priced in

Markets had fully priced in no move at this meeting, which kept the fed funds rate targeted in a range between 5.25%-5.5%, the highest in some 22 years. The rate fixes what banks charge each other for overnight lending but also affects many other forms of consumer debt too.

While the no-hike was expected, there was plenty of uncertainty over where the rate-setting Federal Open Market Committee (FOMC), would go from here.

Judging from reports released Wednesday 20th September 2023, the bias appears towards more restrictive policy and a higher-for-longer approach to interest rates.

Eurozone interest rates have been hiked again to a record high by the European Central Bank (ECB).

The bank raised its key rate for the 10th time in a row, to 4% from 3.75%, as it warned inflation was expected to remain too high for too long.

The latest increase came after forecasts predicted inflation, which is the rate prices rise at, would be 5.6% on average in 2023. However, the ECB signalled that this latest hike could be the last for now.

‘The council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target’, the bank reportedly said. The central bank originally expected inflation to be ‘transitory’.

It added that it expected inflation in the 20-nation bloc to fall to around 2.9% next year and 2.2% in 2025.

As in other parts of the world, the eurozone has been hit by rising food and energy prices that have squeezed household budgets and from the Russia/Ukraine war. Central banks have been increasing interest rates in an attempt to tame inflation and slow rising prices.

More expensive to borrow

The theory behind increasing rates is that by making it more expensive for people to borrow money, the ‘consumer’ will then have less excess cash to spend, meaning households will buy fewer things and then price rises will ease. But it is a balancing act as raising rates too aggressively could cause a recession.

Interest rates in the UK are currently higher than in the eurozone at 5.25%, but UK inflation is also higher at 6.8%, and the Bank of England is expected to raise rates again next week.

The Nationwide Building Society says house prices are 5.3% lower compared to August last year, in the biggest annual decline since 2009.

Nationwide said the drop represented a fall of £14,600 on a typical home in the UK since house prices peaked in August 2022. It also said higher borrowing costs for buyers had led to a slowdown in activity in the housing market. Mortgage approvals are also about 20% below pre-Covid levels.

After 14 rate increases from the Bank of England – a two year fixed rate mortgage is now touching 6.7%

Since December 2021, the Bank of England (BoE) has raised interest rates 14 times in row in a bid to clamp down on rising inflation in the UK. The bank’s base rate now stands at 5.25%. This has led to lenders raising their mortgage rates, putting increased pressure on homebuyers.

The average two-year fixed mortgage rate on Friday was 6.7%, while the average five-year fix was 6.19%.

Average house prices in the UK peaked at £273,751 in August 2022 but fell to £259,153 last month.

The latest U.S. mortgage rates are the highest they have been in decades.

The average 30-year fixed-rate mortgage rose to 7.23% in the week ending 25th August 2023, up from 7.09% the week before, according to latest bank reports from U.S. This is the highest level since June 2001, when it was 7.24%.

The rate on a 30-year fixed mortgage increased to 7.31% in the week ended 18th August 2023, according to Mortgage Bankers Association data. This is the highest level since late 2000.

The 30-year fixed mortgage rate averaged 7.16% with 0.68 points as of August 16, according to U.S. News. This is up from 7.09% with 0.7 points the previous week. The adjustable-rate mortgage increased to 7.6%.

Inflation driving interest rates up

The rise in mortgage rates is driven by indications of ongoing economic strength and inflation pressures, which have also pushed up Treasury yields and the Federal Reserve’s interest rate expectations.

Higher mortgage rates make home buying more expensive and reduce the affordability of homeownership. They also discourage existing homeowners from selling or refinancing their homes, which contributes to the low inventory of available homes for sale.

As a result, home sales have declined and home prices have soared in many markets. Will interest rates touch 8%?

China’s central bank has cut one of its key interest rates for the second time in three months as the world’s second-largest economy struggles to bounce back from the pandemic.

The country’s post-Covid recovery has been hit by a property crisis, falling exports and weak consumer spending. In contrast, other major economies have raised rates to tackle high inflation. Raising interest rates to tackle inflation is likely creating a econmic problem all of its own for many contries caught in the inflation trap.

The PBOC last cut its one-year rate, on which most of China’s household and business loans are based, in June 2023 – demonstrating China’s commitment to reviving the economy. Economists had also expected the bank to lower its five-year loan rate, which the country’s mortgages are pegged to. However, this was unchanged at 4.2%. In a surprise move mid-August 2023, short and medium-term rates were also cut.

More stimulus

China will need a much bigger stimulus package to boost confidence to drive up consumption and growth. Without it, the economy is risking faltering into deflation which will make it even harder to recover. More rate cuts could be announced in conjunction with government spending, as well as targeted measures to help the property market.

China struggling to shake off the effect of the 2020 pandemic

Beijing is trying to restore confidence, but officials will also be mindful of the long-term implications of the policies may create. China’s economy has struggled to overcome several major issues in the wake of the pandemic, which saw much of the world shut down.

Property problems

Concerns with China’s property market still remain and were highlighted again when ongoing crisis-hit real estate giant Evergrande filed for bankruptcy protection in the U.S in August. The heavily-indebted company is attempting to arrange a multi-billion dollar deal with creditors.

Also, earlier this month, another of the country’s biggest property developers, Country Garden, warned that it could see a loss of up to $7.6bn (£6bn) for the first six months of the year. At the same time data showed China had slipped into deflation for the first time in more than two years. That was as the official consumer price index, a measure of inflation, fell by 0.3% last in July 2023 from a year earlier.

Exports, imports and youth employment figures

Official figures indicated that China’s imports and exports fell sharply in July 2023 as weaker global demand threatened the country’s recovery prospects.

China exports and imports slow July 2023

Beijing has also stopped releasing youth unemployment figures, which were seen by some as a key indication of the country’s slowdown. In June 2023, China’s jobless rate for 16 to 24-year-olds in urban areas climbed to a record high of more than 20%.

There is a serious ongoing message here of concern and worry for global stock markets, and not just from China – do we need to act now?

Russia’s central bank has announced a surprise hike in its key lending rate by 3.5%, from 8.5% to 12%, as the country’s economic recovery loses steam amid a resurgence of COVID-19 cases and weak domestic demand.

The decision was announced after an emergency meeting of the bank’s board of directors was called a day earlier as the ruble declined. The fall comes as Moscow increases military spending and Western sanctions weigh on its energy exports.

The Russian currency passed 101 roubles to the dollar on Monday, losing more than a third of its value since the beginning of the year and hitting the lowest level in almost 17 months. It had recovered slightly after the central bank announced the meeting.

The central bank blamed the weak ruble on ‘loose monetary policy‘, suggesting that bank has ‘all the tools necessary‘ to stabilize the situation.

More imports, less exports

By raising borrowing costs, the central bank is trying to fight price spikes as Russia imports more and exports less, especially oil and natural gas, with defense spending going up and sanctions taking a toll. Importing more and exporting less means a smaller trade surplus, which typically weighs on a country’s currency.

The bank also made a big rate hike of 1% last month, saying inflation is expected to keep rising and the fall in the ruble is adding to the risk.

After Western countries imposed sanctions on Russia over the invasion of Ukraine in February 2022, the ruble plunged to a low of 130 to the dollar, but the central bank enacted capital controls that stabilized its value.

The Bank of England’s forecasting, which has a major impact on the UK economy, is being reviewed and has been criticised.

After the Bank raised interest rates for a 14th time in a row in an effort to slow price rises in Augts 2023, officials have predicted inflation to fall from the current rate of 7.9%, to ‘around 5%‘ by the end of the year. The Bank puts rates up when they are concerned that too much spending will send prices spiralling.

So, in light of its estimating techniques being challenged, how much faith should we put in ‘5% by Christmas’?

For the last two years, the Bank of England has been underestimating the likely rate of inflation in the short term. MPs have been critical of the Bank’s forecast, and its officials have acknowledged they have got some judgements wrong in their forecasting.

The Central Bank has also announced a review into how it makes forecasts.

This was one of the questions put to the Bank of England governor

Mr Baron:Good morning, everyone. In looking at the bank rate going forward, some of us, it is fair to say, have long believed that central banks, including the Bank of England, have been well behind the curve with regard to inflation. As the Chair has said, forecasting has been awry. The Bank of England is one among others that has been too slow in raising interest rates, allowing inflation to mushroom well above the 2% target.

I have put it as strongly as suggesting that it has been a woeful neglect of duty. It is causing real pain out there for people and businesses. We should always remember, as we sit in our, sometimes, white ivory towers, having these debates, that we are talking about people’s lives and businesses that are having to grapple with double-digit inflation and interest rates perhaps going up too quickly. I think that you get it, but it is useful to remind ourselves of that.

Why should the public have confidence in your ability to get it right going forward? What lessons do you think that you have learned? What are you going to do differently? I am not hearing a satisfactory answer to that...

See the full report here – be prepared, it’s an acquired taste and a long read…

More wrong than right

However, some critics have argued that the BoE’s forecasts are often too optimistic or pessimistic, and that they fail to capture the impact of major shocks or structural changes in the economy. For example, the BoE was widely criticised for underestimating the severity of the 2008 financial crisis and overestimating the negative effects of Brexit on the economy. Some have also questioned the usefulness of the BoE’s forecasts for guiding monetary policy decisions, as they may be influenced by political or psychological factors.

Therefore, it may be wise to take the BoE’s forecasts with a grain of salt, and not to rely on them too much for making economic or financial decisions. The BoE’s forecasts are not useless, but they are not infallible either. They are one of many sources of information and analysis that can help us understand the state and prospects of the UK economy, but they should not be treated as gospel truth.

The Bank of England has been wrong with too many forecasts, so why bother? Target 2%, actual above 10%!

According to the chancellor Jeremy Hunt, the UK economy is caught in a trap

The UK and other advanced economies are facing a low-growth trap that is hard to escape. This means that the potential growth of the economy, which depends on factors such as productivity, innovation, investment, and labour force, is very low and insufficient to meet the demand and expectations of the people.

Brexit

The UK economy has been hit by huge global shocks that have disrupted its normal functioning and recovery. These include the Covid-19 pandemic, which caused lockdowns, restrictions, and health crises; the energy crisis, which led to soaring gas prices and supply shortages; and the Brexit transition, which created uncertainty and trade barriers.

Inflation

The UK economy is also struggling with high inflation, which erodes the purchasing power of consumers and businesses. Inflation is driven by various factors, such as rising energy costs, global supply chain bottlenecks, labour shortages, and pent-up demand.

‘Don’t you just love numbers?’

The Bank of England has raised interest rates to 5.25% as of August 2023 – the highest level since 2008, to curb inflation and maintain price stability. The Bank of England inflation target is 2%.

The plan?

The chancellor reportedly has vowed to stick to the plan that he believes will bring down inflation and boost growth in the long term.

He said that he will unveil a plan in the autumn statement that will show how the UK can break out of the low-growth trap and become one of the most entrepreneurial economies in the world. He also said that he will not ‘veer around like a shopping trolley‘ and change course in response to short-term pressures.

The Bank of England (BoE) announced another increase in its base rate, from 5% to 5.25%, the highest level in over 15 years as of 3rd August 2023. This is the 14th consecutive rise since December 2021, when the BoE started to tighten monetary policy in response to rising inflation.

The Bank said that inflation, which fell to 7.9% in June, remained well above its 2% target and that further action was needed to bring it down. It also cited the risks posed by the global economic situation, especially the conflict in Ukraine and the slowdown in China.

Affect on borrowers

The rate hike will affect millions of borrowers and savers across the UK. Fixed-rate mortgages will not change until the end of their term, but new deals will be hit borrowers hard. Savers may see some benefit from higher interest rates, but only if banks and building societies pass on the increase, which they are slow to do.

Bear in mind that for the past 15 years many have benefitted from ultra low interest rates and cheap money, this is not the ‘norm’. And now, as more ‘normal’ interest rates return it will initially disrupt financial stability for some, and it will be difficult for many for a time. But money has been cheap and mortgages have always been the cheapest way to borrow long term and that is still the case – even if it doesn’t feel like it right now.

Expected

The Bank of England’s decision was widely expected by market analysts, but some have warned that further rate rises could damage the UK economy, which is already showing signs of weakness. House prices are falling, manufacturing activity is contracting and consumer confidence is low.

The prime minister, Rishi Sunak, said he was disappointed that inflation was not falling faster, but claimed that he was making progress and that there was ‘light at the end of the tunnel‘.

And a train too if he isn’t careful!

UK has the highest interest rate in the G7

Interest rates have been increasing across the world in recent months.

The Bank of England’s latest rate hike means the UK now has the highest rates in the G7 – a group of the world’s seven largest so-called ‘advanced’ economies.

That’s higher than France, Germany, Italy, Japan, Canada and the U.S.

If you think the UK’s got it bad, spare a thought for these countries where interest rates are rampant

The UK is facing a cost of living crisis as inflation has soared to its highest level in decades. The Bank of England has raised interest rates 13 times since December 2021 in an attempt to bring inflation back down to its original target of 2%. But what does this mean for consumers, savers and borrowers?

What is inflation and why is it rising?

The current UK interest rate is now: 5.0%

Inflation is the term used to describe rising prices. How quickly prices go up is called the rate of inflation. Inflation affects the purchasing power of money, meaning that the same amount of money buys less goods and services over time.

The rate of inflation in the UK is measured by two main indicators: the consumer price index (CPI) and the retail price index (RPI). The CPI is based on a basket of products and services that people typically buy, while the RPI also includes mortgage interest payments.

According to the Office for National Statistics (ONS), the CPI inflation rate was 8.7% in the year to May 2023, while the RPI inflation rate was 11.4%. This means that on average, prices were 8.7% and 11.4% higher respectively than they were a year ago.

The main drivers of inflation in the UK are:

Energy bills: Wholesale gas prices have surged due to global supply disruptions since the pandemic hit in 2020, geopolitical tensions, the war in Ukraine and increased demand. The government introduced an energy price guarantee to freeze energy prices for six months, but prices still went up 27% in October 2022. The energy price guarantee has been extended.

Shortages: The pandemic and Brexit have caused labour and supply chain issues that have affected many sectors, such as food, clothing, construction and hospitality. This has led to higher costs and lower availability of some goods and services.

Demand: As the economy recovers from the lockdowns, consumer spending has picked up, especially on leisure and travel activities. This has increased the demand for some goods and services, pushing up their prices.

How do interest rates affect inflation?

Interest rates are the cost of borrowing money or the reward for saving money. The Bank of England sets the bank rate, which is the interest rate it charges to commercial banks that borrow from it. The bank rate influences other interest rates in the economy, such as mortgage rates, loan rates and savings rates.

Interest rates climbed ever higher as the Bank of England lost control of inflation

The Bank of England uses interest rates as a tool to control inflation. The Bank has a target to keep inflation at 2%, but the current rate is more than five times that. When inflation rises, the Bank increases interest rates to make borrowing more expensive and saving more attractive. This reduces the amount of money circulating in the economy and slows down rising prices.

The Bank has raised interest rates 13 times since December 2021, from 0.1% to 5.0%. This is the highest level since March 2009, when interest rates were cut to a record low of 0.5% following the global financial crisis.

What does higher inflation mean for your money?

Higher inflation means that your money loses value over time. For example, if you had £100 in April 2022 and inflation was 8.7%, you would need £108.70 in April 2023 to buy the same amount of goods and services.

Higher inflation also affects your income, spending, saving and borrowing decisions.

Income: If your income does not keep up with inflation, you will have less purchasing power and lower living standards. For example, if your salary was £30,000 in April 2022 and increased by 2% in April 2023, you would earn £30,600. But if inflation was 8.7%, you would need £32,610 to maintain your purchasing power.

Spending: Higher inflation may encourage you to spend more now rather than later, as you expect prices to rise further in the future. However, this may also reduce your savings and increase your debt.

Saving: Higher inflation reduces the real return on your savings, meaning that your savings grow slower than prices. For example, if you had £10,000 in a savings account that paid 1% interest in April 2022, you would have £10,100 in April 2023. But if inflation was 8.7%, your savings would be worth only £9,300 in real terms.

Borrowing: Higher interest rates make borrowing more expensive, meaning that you have to pay more interest on your loans and mortgages. For example, if you had a £200,000 mortgage with a 25-year term and a 2% interest rate in April 2022, your monthly payment would be £848. But if the interest rate rose to 4.5% in April 2023, your monthly payment would increase to £1,111. Mortgage interest rates hit 6% in July 2023.

How can you protect your money from inflation?

There are some steps you can take to protect your money from inflation, such as:

Review your budget: Track your income and expenses and see where you can cut costs or increase income. Try to save more and spend less, especially on non-essential items.

Shop around: Compare prices and deals for the goods and services you need or want. Look for discounts, vouchers and cashback offers. Switch providers or suppliers if you can find better value elsewhere.

Pay off debt: This is a priority! If you have high-interest debt, such as credit cards or overdrafts, try to pay it off as soon as possible. This will reduce the amount of interest you pay and free up more money for saving or investing.

Save smartly: Look for savings accounts or products that offer interest rates higher than inflation (tricky to find). Consider diversifying your savings into different types of assets, such as stocks, bonds, property or gold. These may offer higher returns than cash in the long term, but bear in mind they also carry more risk and volatility.

Invest wisely: If you have a long-term goal, such as retirement or buying a house, you may want to invest some of your money in the stock market or other assets that can grow faster than inflation. However, you should only invest what you can afford to lose and be prepared for the ups and downs of the market. You should also seek professional advice before making any investment decisions.

Conclusion

Inflation and interest rates are two important factors that affect the UK economy and your personal finances. The UK is currently experiencing high inflation due to various factors, such as energy prices, shortages and demand. The Bank of England has raised interest rates to try to bring inflation back down to its target of 2%. Higher inflation and interest rates have implications for your income, spending, saving and borrowing decisions. You can take some steps to protect your money from inflation, such as reviewing your budget, shopping around, paying off debt, saving smartly and investing wisely.

How well has the Bank of England done to keep inflation at or close to 2%?

UK inflation rate remains high at 8.7% in May 2023

The UK inflation rate remained at 8.7% in the year to May 2023, according to the latest official figures from the Office for National Statistics (ONS). This is the same rate that was recorded in April, but down from the 10.1% level seen in March.

The ONS said that rising prices for air travel, recreational and cultural goods and services, and second-hand cars resulted in the largest upward contributions to the annual inflation rate. However, these were offset by falling prices for motor fuel and food and non-alcoholic beverages.

The ONS also reported that core inflation, which excludes energy, food, alcohol and tobacco, rose to 7.1% in May, up from 6.8% in April, and the highest rate since March 1992.

‘I’m just taking this calculator thingy to my boss, I thought it might help’. ‘Well, good idea, guess it can’t make it any worse’.

High inflation is the fault of everyone else other than the central bank

The inflation rate is measured by the Consumer Prices Index (CPI), which tracks the changes in the cost of a basket of goods and services that are typically purchased by households. The CPIH, which includes owner occupiers’ housing costs, rose by 7.9% in the year to May, up from 7.8% in April.

The high inflation rate has been driven by a combination of factors, including supply chain disruptions, labour shortages, higher energy costs, and strong consumer demand as the economy recovers from the coronavirus pandemic.

The Bank of England has a target to keep inflation at 2%, but it has said that it expects inflation to rise further in the coming months before falling back next year. The Bank has also signalled that it may raise interest rates sooner than expected to curb inflationary pressures.

However, June’s inflation reading came in below economists expectations at 7.3% A small but welcome reversal of high UK inflation. UK inflation is higher than the EU and U.S.

Are central banks doing a good job at controlling inflation? Bear in mind the inflation target is 2%…