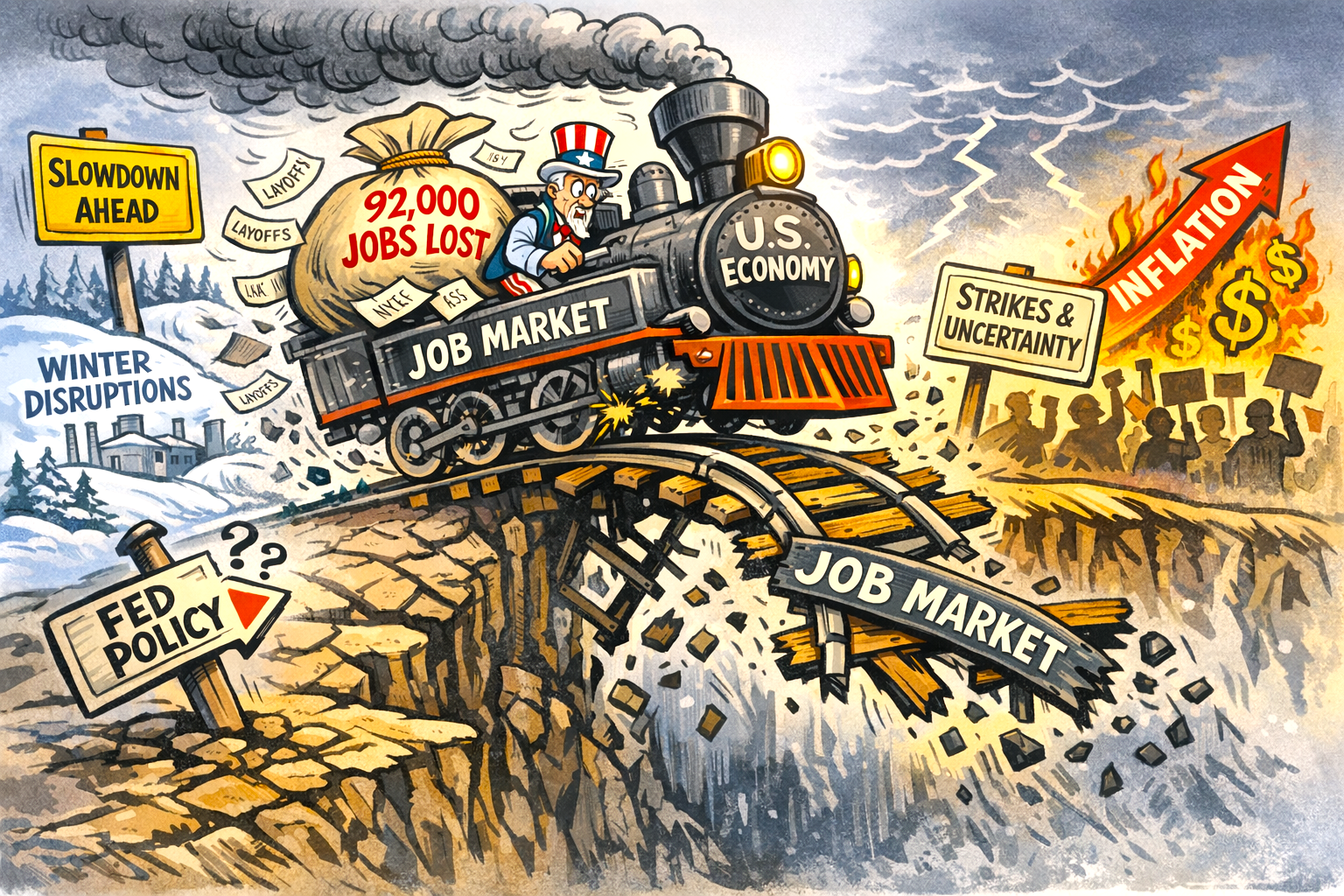

The latest U.S. payroll figures delivered an unexpected jolt to markets, with February’s nonfarm employment falling by 92,000 — a far deeper contraction than economists had anticipated.

Consensus forecasts had pointed to a modest 50,000 decline, but the Bureau of Labor Statistics’ report revealed a labour market losing traction for the third time in five months.

Several temporary factors contributed to the downturn, including severe winter weather and a major strike at Kaiser Permanente, which reportedly sidelined more than 30,000 health‑care workers across Hawaii and California.

Job losses reach across sectors

Even so, the breadth of job losses across sectors — from manufacturing to information services — suggests underlying fragility.

Health care, previously the most reliable engine of job creation, shed 28,000 roles during the survey period, while manufacturing and transportation each posted notable declines.

Despite the weak headline number, wage growth accelerated. Average hourly earnings rose 0.4% month‑on‑month and 3.8% year‑on‑year, both slightly above expectations.

This combination — softening employment but firm wage pressures — complicates the Federal Reserve’s policy decision.

With inflation still printing above target and oil prices rising, policymakers face a narrowing path between supporting growth and preventing renewed price pressures.

Financial markets reacted swiftly. Traders moved to price in earlier interest‑rate cuts, pulling expectations forward to July and increasing the likelihood of two reductions before year‑end.

Caution

Yet Fed officials have signalled caution, noting that recent labour data has been volatile and may not reflect a sustained trend.

The wider economic picture remains mixed. Services and manufacturing activity continue to expand, and consumer spending — albeit increasingly concentrated among higher‑income households — has held up.

Still, February’s payroll shock underscores rising downside risks.

If job losses persist beyond temporary disruptions, the narrative of a resilient U.S. economy may be harder to sustain.