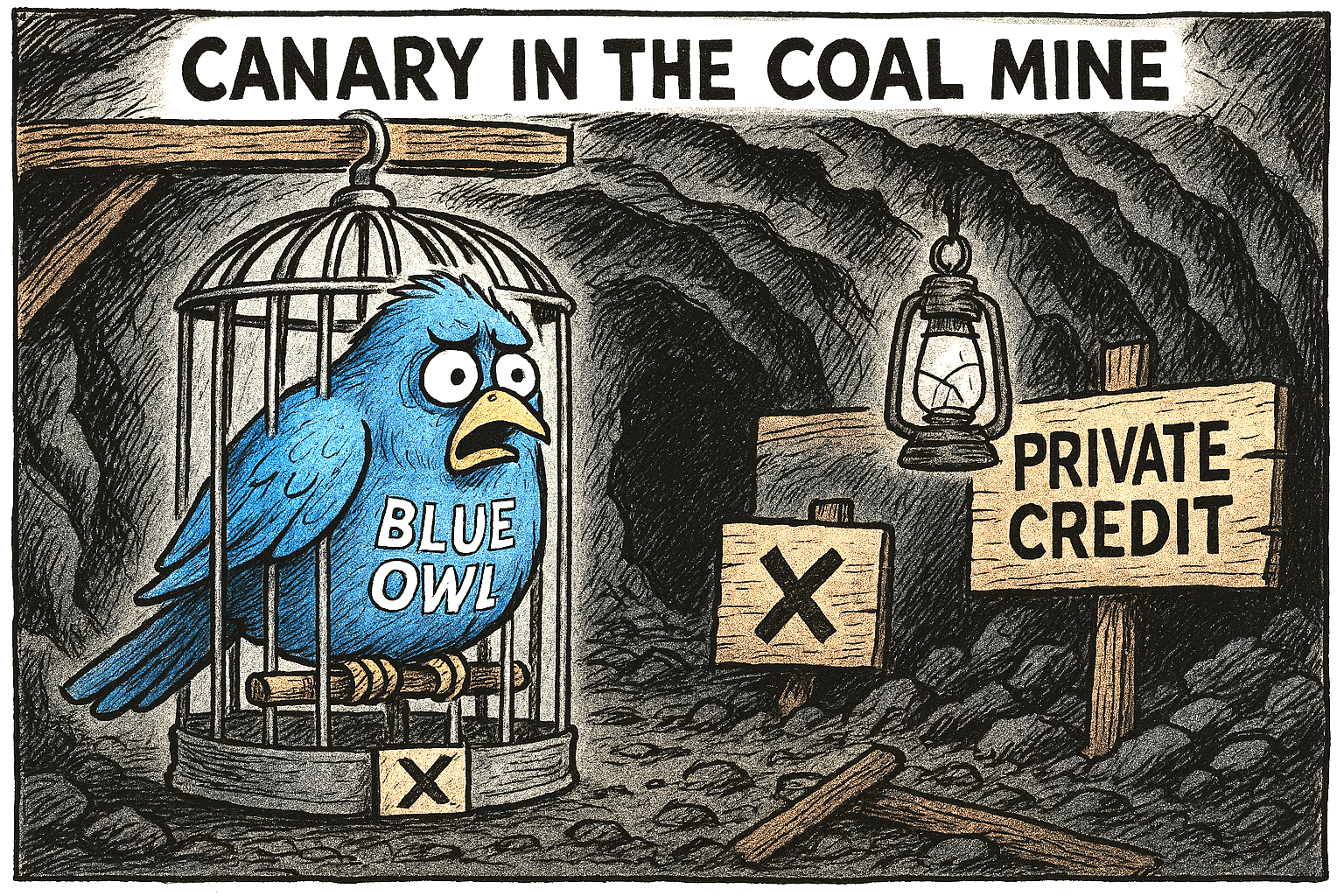

Blue Owl’s decision to halt investor withdrawals at one of its flagship retail‑focused private credit vehicles has sent a jolt through a market long celebrated for its resilience.

The move, centred on Blue Owl Capital Corporation II (OBDC II), marks one of the most significant stress signals yet in the rapidly expanding private credit sector.

Redemption

The firm confirmed that investors in OBDC II will no longer be able to redeem shares on a quarterly basis, ending a mechanism that previously allowed withdrawals of up to 5% of net asset value each quarter.

The redemption facility had already been paused in November 2025 as withdrawal requests accelerated, but the permanent halt represents a decisive shift.

To meet liquidity needs and prepare for a partial return of capital, Blue Owl has sold a substantial portion of its loan book.

Reportedly around $600 million of assets were offloaded from OBDC II as part of a wider $1.4 billion sale across three funds, with the firm planning to return 30% of the fund’s value to investors by the end of March.

Reaction

Markets reacted swiftly. Shares in Blue Owl fell between 6% and 10% across recent trading sessions, touching their lowest levels in more than two years.

The sell‑off was fuelled not only by the redemption freeze but also by broader concerns about the firm’s exposure to software‑sector borrowers — an area facing valuation pressure and heightened sensitivity to disruption from artificial intelligence.

The episode has reignited debate about the structural vulnerabilities of private credit, a market now estimated at $1.8 trillion.

The model relies on illiquid loans packaged into vehicles that promise periodic liquidity to investors — a mismatch that works only as long as redemption requests remain manageable.

Blue Owl’s move suggests that, under stress, even well‑established managers may be forced into asset sales or wind‑down scenarios.

Contagion?

Contagion fears quickly spread across the sector. Shares of major alternative‑asset managers, including Apollo, Blackstone and TPG, all declined sharply as investors reassessed liquidity risks in retail‑facing credit products.

For now, Blue Owl insists that capital will continue to be returned through loan repayments and asset sales.

But the permanent closure of redemptions at OBDC II stands as a stark reminder: the private credit boom is entering a more volatile phase, and liquidity — once taken for granted — is becoming the industry’s most fragile commodity.