The U.K. economy flatlined in the third quarter, initial figures showed Friday 10th November 2023.

Gross domestic product (GDP) showed zero quarterly growth in the three months to the end of September 2023, following an increase of 0.2% in the previous quarter. In annual terms, the UK’s Q3 GDP was 0.6% higher than in the same period in 2022.

Services sector output dropped 0.1% on the quarter, but the decline was offset by a 0.1% increase in construction performance, while the production sector flatlined.

U.K. Chancellor of the Exchequer Jeremy Hunt said high inflation remains the ‘single greatest barrier to economic growth’ in the country, with the consumer price index remaining at 6.7% year-on-year in September 2023.

UK economy flatlines as inflation sticks at 6.7% year-on-year as at September 2023.

‘The best way to sustainably grow our economy right now is to stick to our plan and knock inflation on its head’, Hunt reportedly said.

It’s useful to know the government have a plan, even though they were very late to the inflation party! Guess they were sidetracked with all the other parties at No.10!

‘The Autumn Statement will focus on how we get the economy growing healthily again by unlocking investment, getting people back into work and reforming our public services so we can deliver the growth our country needs’.

Up until September 2023, the Bank of England (BoE) raised interest rates 14 consecutive times to try to influence the UK ‘product and service’ price climb.

Red flags

Interest rates are now at a 15-year high of 5.25%, and are expected to remain high for some time to come. Bank Governor Andrew Bailey reportedly said last week it was ‘much too early’ to be considering rate cuts.

Thank you Governor Baily – it so comforting and reassuring to know that the very people who missed the red inflation flags are still in charge of policy.

Transitory?

Remember, the BoE and others originally suggested inflation would be transitory – I suppose it is, if given years to move back down. What did you think was going to happen after all that borrowing and the country crawling back to work after the pandemic.

Nice job guys! Don’t forget to collect your paycheque on the way out!

Microsoft ended Tuesday’s trading session at a record high of $360.53, following fresh optimism about growth from a key partner in artificial intelligence (AI). The increase gives the company a market value of about $2.68 trillion.

At a tech event on Monday 6th November 2023, Microsoft’s AI partner, OpenAI, announced a batch of updates, including price cuts and plans to allow people to make custom versions of the ChatGPT chatbot.

Microsoft CEO Satya Nadella attended and emphasized that developers building applications with OpenAI’s tools could get to market quickly by deploying their software on Microsoft’s Azure cloud infrastructure.

Microsoft has invested a reported $13 billion in OpenAI, which has granted Microsoft an exclusive licence on OpenAI’s GPT-4 large language model that can generate human-like prose in response to a few words of text.

Fictitious AI robot learning from a digital human online

Last week, Microsoft announced the release of an AI add-on for its Office productivity app subscriptions and an assistant in Windows 11, both of which rely on OpenAI models.

The future is looking bright for Microsoft right now.

An old well established and trusted tech brand pivoting to AI that has a high dividend yield is IBM, which has been around for more than a century and is known for both its hardware and software products.

IBM is investing heavily in AI, cloud computing, and quantum computing, and has recently acquired several AI start-ups, such as Instana, Turbonomic, and Waeg.

IBM also has a partnership with OpenAI, one of the leading AI research organizations, to provide cloud infrastructure for its AI models.

Investors who love IBM expect the company to grow its earnings by around 10% annually over the next five years. Investors were also impressed with IBM’s dividend yield, which is currently around 4.5%. Dividends are a great way to generate passive income.

IBM is not the only tech company that is pivoting to AI. Google, Microsoft, and Anthropic are competing in the field of generative AI, which can create text, images, music, and more from natural language prompts.

Integrate generative AI

These companies are attempting to integrate generative AI into their products and services, such as search engines, maps, word processors, office applications, chatbots, and more. Generative AI is seen as a game-changer for many industries and applications, and could potentially disrupt the dominance of Big Tech.

Legacy companies can pivot to a platform model, which is a business strategy that connects producers and consumers of value through a digital interface. Platform companies like Facebook, Amazon, Google, and Tencent have created value at stunning rates, and have grown rapidly and own large market shares.

IBM mainframe from the 1970’s

Legacy companies can leverage their existing systems, such as customer relationships, data, and brand recognition, to create platforms that offer impressive and immersive products and services.

Other successful platform pivots are Disney+, which transformed Disney from a media producer to a media platform; Nike+, which connected Nike’s physical products with digital services; and John Deere, which created a platform for precision agriculture.

South Korea stocks surged on Monday, 6th November 2023 after the country imposed a ban on short selling, while most Asia-Pacific markets took the lead from a lighter than expected U.S. jobs report that helped reduce interest rate expectations.

Financial decision makers in South Korea said short selling will be banned until the end of June 2024. Short selling is when a trader sells borrowed shares to buy back at a lower price and pocket the difference.

The U.S. central bank has held its key interest rate at its current 22-year high as it seeks to stabilise price increases, which had recently reached near-record levels.

The Federal Reserve’s rate remains at 5.25%-5.5%.

The bank has been raising interest rates in an attempt to tame the economy and slow inflation, (the rate at which prices rise). Recent data showed the U.S. economy grew faster than expected.

Raising interest rates is a way for central banks tackle rising inflation. The idea is that by raising interest rates and making it more expensive to borrow, consumers will spend less and that would lead to slower price rises. In the U.S. however, the consumer is not slowing down. This may lead to higher rates, or higher for longer which in turn could push the U.S. into a recession.

The bank had faced criticism, with some suggesting that holding interest rates at higher levels could put the U.S. economy at risk of entering a recession.

If the Israel-Hamas conflict further intensifies, the risks to the global economy are growing, economist Mohamed el-Erian reportedly said Monday 30th October 2023.

The impact on global markets was initially limited, as investors viewed the conflict as contained. However, the prospect of a regional spillover has added to a sense of unease.

‘The longer this conflict goes on, the more likely it will escalate. The higher the risk of escalation, the higher the risk of contagion to the rest of the world in terms of economics and finance’, el-Erian said.

The Nasdaq is a stock market index that tracks the performance of over 3,000 companies, mostly in the technology sector.

Correction

A correction is a term used to describe a decline of 10% or more from a recent peak in the price of an asset. The Nasdaq entered correction territory on Wednesday 25th October 2023, as it closed at 12,922, which was 10% lower than its previous high of 14,358 on 19th July 2023.

The main reason for the Nasdaq’s correction is believed to be the rise in long-term Treasury yields, which increased the borrowing costs for companies and reduced the attractiveness of growth stocks. The 10-year Treasury yield rose to 4.95% on Wednesday 25th October 2023, the highest level since June 2021. Higher interest rates also make future earnings for tech companies much more difficult.

Disappointing Q3 results

Another factor that contributed to the Nasdaq’s correction was the disappointing third-quarter earnings reports from some of the biggest tech companies, such as Alphabet (Google), Amazon, and Meta (Facebook fame).

These companies reported lower-than-expected revenue growth, profit margins, and cloud computing performance, which weighed on their stock prices and dragged down the Nasdaq. Investors expect more, especially with AI – now the new kid-on-the-block.

Concerns

The Nasdaq’s correction has raised concerns among investors about the outlook for the tech sector and the broader stock market. However, some analysts have argued that the correction could be a healthy and temporary adjustment that creates buying opportunities for long-term investors.

They have pointed out that the Nasdaq is still up 22.5% year-to-date as of Wednesday 25th October 2023, and that the fundamentals of the tech industry remain strong despite the challenges posed by inflation, regulation, yields and competition.

The idea is simple – pick good companies and hold them for the long-term.

Every time you buy shares in a company, you have purchased a piece of that company. And as a share owner, you are entitled to a ‘share’ of the profits.

When it comes to investing, the goal is to find great companies, super companies. Buy shares in these companies at good prices. And then behave like owners of these companies and enjoy all of the successes.

Then… HOLD those shares for as long as possible – as if you own the company.

Ask yourself this question: ‘Would you buy the company?’

If the answer is yes – then go buy the shares.

Holding on as long as possible means that as long as you believe a company is still a great, you are more likely to keep the shares. But if something changes and it’s no longer a good choice, then it may be time to sell up.

The message here is to believe in a long-term investing strategy – because it works!

Short-Term versus Long-Term Investing

What you must not do is gamble on shares or any other high-risk activity or product. Share prices go up and they go down all the time. And in some cases, prices continue to move even after the stock market has closed!

Long term investing is a long-term winner!

Most people aren’t successful trying to ‘bet’ on when a share is going to go up or down especially short-term bets laced over minutes, hours, days or weeks. You can’t build wealth this way. In fact, there are plenty of traders out there with tragic stories to tell of failed ‘dumb money bets’. This is one of the fastest ways to lose your hard-earned cash; just don’t do it!

Platforms

There are many investing platforms available today that offer all sorts of trading solutions, from day trading, CFDs (contract for differences), spread betting, and more recently, cryptocurrencies. These instruments aren’t really designed to assist a long-term strategy but rather a short-term punt or bet. It’s an endless game where someone, somewhere is always left with nothing. These systems will happily take your money.

Please read the small print for these services. Do not be surprised to see disclosures that read something like, ‘75%+ of retail traders lose money’. It’s true, they do, and it could be you! Its far far easier to learn to become financially successful over the long term.

Long-Term Investing

Diversify

A hard truth about investing is that sometimes you’ll get it wrong, we all do.

The term for this is firm-specific risk (sometimes referred to as unsystematic risk). And every company in the world, even industry behemoths like Amazon, Apple or Microsoft get it wrong sometimes too. It’s unavoidable.

Fortunately, such risk can be mitigated through diversification. By owning a number of companies, the returns of one successful investment can easily offset the losses of several losers.

It is wise to aim to build a portfolio over time of around say 10 – 20 quality businesses that you believe in. If you would be prepared to ‘buy’ the company; buying shares in it is the next best option.

Have Patience

In the short term, the movements of the stock market are chaotic, unpredictable or volatile even. But over a longer period of time, a recurring pattern starts to emerge among quality businesses.

Select quality companies and hold them!

Companies can’t magically double their profits overnight. Building a massive multi-billion or even trillion-pound enterprise takes time. But the investors who have the patience and financial prudence to invest in quality businesses with such long-term potential can unlock enormous wealth.

Invest consistently

Getting started with investing is the first major step. The second is to keep investing over time. Little and often. It’s not easy to ‘free up’ cash but the more money you put to work by investing in stocks, the better your portfolio will do overall.

It is easy for me to suggest for you to go invest and spend your money, you most likely need the money spare to be able to go do this in the first place. So, a little invested spread over time will help open that ‘wealth’ door as time trickles by.

However, there is a caveat to this rule. You should only invest money you don’t need to live. Invest only what you have spare or can ‘free up’.

This is the way!

Long-term investing requires holding investments for years or even decades. This strategy works – this is the way! It’s easier said than done, but a little invested now will go a long way later. It’s also a matter of priorities and sacrifice to ‘free up’ some spare cash to invest instead of buying that new must have gadget (that you don’t really need).

Also, the last place you want to find yourself in is where you are forced to sell your investment before it’s had time to ‘climb’ because you’re short on cash. Or even worse, forced to sell your holding during a stock market crash when prices are extremely low. That’s an awful place to be – don’t go there if you can avoid it. However, buying after a crash is a different matter – but again, buy only good quality companies.

Select super good companies and hold them.

In short, invest consistently. But only the money you can afford. Don’t borrow, don’t use credit. Only invest what you can afford. It will work for you over time. But invest wisely in good high quality comapnies,

Don’t panic – volatility happens!

The stock market will crash; this is an inevitable fact of investing. Naive investors, who panic during these volatile times, often end up selling their shares that are either completely unaffected by the catalysts of the crash or perfectly capable of weathering the storm.

Just take a look at what happened with Applein 2008. The tech giant fell by over 50% in the space of 12 months despite having no exposure to the U.S. housing market – even Apple got caught up in the sub-prime lending fiasco. And while the subsequent recession did impact sales, recessions, just like stock market crashes, are temporary. Apple share price recovered, as did many other top-notch companies too.

As horrible a stock market crash is, this is actually one of the best times to buy shares, especially when investing for the long-term. And these opportunities only come around once a decade or so. So, don’t miss out on these incredible opportunities to buy fantastic businesses at major discounts if you have the cash spare.

Let your winners run

Portfolio management is something every investor has to do. Yet a common mistake, is to sell shares in thriving companies too soon. This is usually an error – bear in mind that winners have a tendency to keep winning! But I get that – I understand you may want to sell as you need the money or want some of your investment back. Try and hold if you can – but not at any odds. Keep a close eye on the market – sentiment will change and that will alter the markets direction.

Let the winners run!

Having said that, there is an exception. It’s perfectly possible for a company that was just 2% of your portfolio to grow to 20% or even higher. In these scenarios, it can be wise to sell a few shares to reduce the risk of being over-exposed to a single investment.

But otherwise, let your winners win. LET THE WINNERS RUN!

You can do it!

There is no such thing as risk-free investing, even with a long-term approach. But many of these risk factors can be mitigated through strategies like diversification. Try and manage your portfolio, add stop losses and follow your investments through the newswires.

Remember to always do your research! No short cuts!

Apple and generative AI technology is a topic that has been generating a lot of interest and speculation lately.

According to various reports, Apple is working on developing its own large language model and chatbot, which could potentially enhance its products and services with new features and capabilities. However, some analysts and experts have also raised questions about whether Apple has missed an opportunity to be a leader in the generative AI field, as it seems to be lagging behind its competitors such as Google, Microsoft, and OpenAI.

Apple uses AI in its products but hasn’t launched a generative AI product along the lines of OpenAI’s ChatGPT or Google Bard. Instead, Apple’s AI is used for improving photos and autocorrecting text.

$1 billion per year plan

Apple is on track to spend $1 billion per year on developing its generative artificial intelligence products, Bloomberg reported.

Apple is looking to use AI to improve Siri, Messages and Apple Music.

The spending comes as the company plays catch-up to some competitors who have already debuted new AI products and features, such as Google, Microsoft and Amazon.

Apple was caught flat-footed when ChatGPT and other AI tools took the technology industry by storm.

Generative AI

Generative AI is a subfield of artificial intelligence that focuses on creating content such as text, images, videos, music, and more, based on data and algorithms. One of the most popular examples of generative AI is ChatGPT, a chatbot that can respond to questions and other prompts in a natural and human-like way.

Watercolour artwork impression – ChatGPT was released by OpenAI in 2022, and since then, it has been widely used and improved by various companies and researchers.

ChatGPT was released by OpenAI in 2022, and since then, it has been widely used and improved by various companies and researchers.

Apple slow response

Apple, on the other hand, has been relatively quiet about its generative AI efforts, until recently. In October 2023, Bloomberg reported that Apple was internally testing a ‘ChatGPT-like’ chatbot nicknamed ‘Apple GPT’, but it had not devised a clear strategy for releasing generative AI tools to the public. Apple’s CEO Tim Cook also confirmed that the company was working on generative AI for years, but it was approaching it ‘really thoughtfully and think about it deeply’ because of the potential risks and challenges.

Potential challenges Apple faces in developing and deploying generative AI

Privacy

Apple has always been more cautious than its competitors in handling user data, and it has built its reputation on being a privacy-focused company. However, generative AI requires a lot of data to train and improve its models, which could pose a dilemma for Apple. How can it balance the need for data with the respect for user privacy? How can it ensure that its generative AI does not leak or misuse personal information?

Design

Apple is known for its elegant and intuitive design philosophy, which applies to both its hardware and software products. However, generative AI is a complex and unpredictable technology, which could challenge Apple’s design principles. How can it make its generative AI features easy to use and understand for its customers? How can it avoid confusing or misleading users with its generative AI outputs?

Ethics

Apple has always been mindful of the social and ethical implications of its products, and it has often taken a stance on issues such as human rights, environmental sustainability, and diversity. However, generative AI could raise new ethical concerns, such as bias, misinformation and manipulation. But then that is a common problem for all generative AI systems.

Generative AI could raise new ethical concerns, such as bias, misinformation and manipulation.

These are some of the questions that Apple needs to answer before it can launch its generative AI products to the public. It is possible that Apple is taking its time to address these issues carefully and thoroughly, as it has done in the past with other technologies such as Face ID or Apple Pay. However, it is also possible that Apple has missed an opportunity to be a pioneer in the generative AI field, as it has done in the past with other technologies such as smart speakers or cloud computing.

While Apple is working on its generative AI projects internally, its competitors are already offering generative AI.

Google

Google has integrated its large language model LaMDA into various products and services, such as Google Assistant, Google Photos, Google Docs, Google Translate etc. LaMDA can generate natural and conversational responses to any query or prompt, as well as create images and videos based on text descriptions.

Microsoft

Microsoft has acquired OpenAI’s ChatGPT technology and made it available through its Azure cloud platform. ChatGPT can be used by developers and businesses to create chatbots, voice assistants, content generators, and more. Microsoft has also integrated ChatGPT into some of its products such as Outlook, Teams, PowerPoint, and more.

Amazon

Amazon has launched Alexa Conversations, a feature that allows Alexa users to have more natural and engaging conversations with the voice assistant. Alexa Conversations can also leverage Amazon’s vast e-commerce data to provide personalized recommendations and suggestions to users.

These are just some examples of how generative AI is being used by Apple’s competitors.

Robot chatting to human chatbot online

Apple has missed an opportunity to be a leader in the generative AI field by being too slow or too cautious in developing and deploying its own generative AI products.

However, it is highly likely that Apple is waiting for the right moment to surprise everyone with its innovative and unique generative AI features that will set it apart from its competitors.

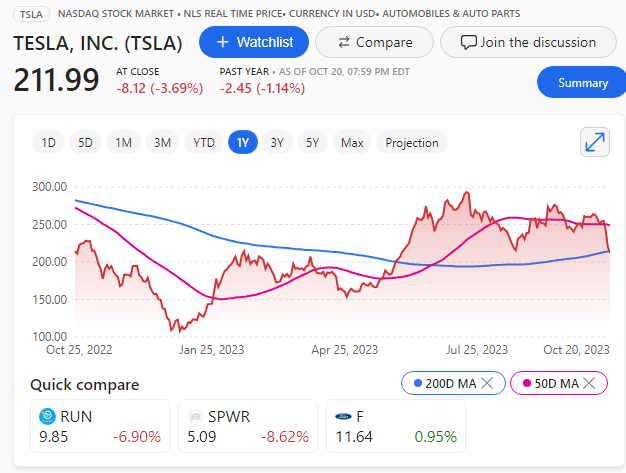

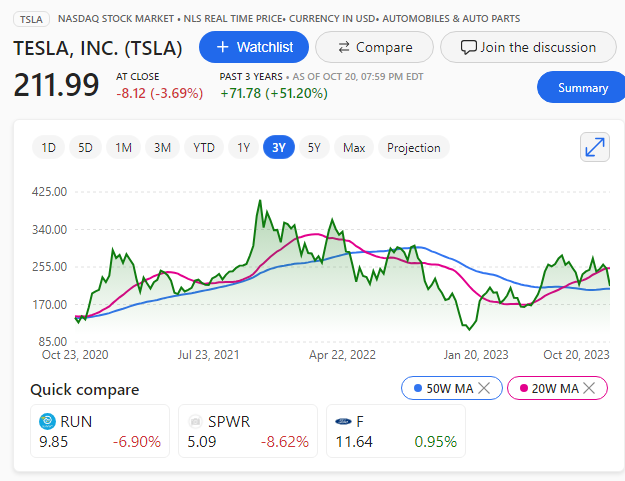

The stock dropped more than 15% over the last few days after the company posted third-quarter earnings on Wednesday 20th October 2023.

The earnings report showed that Tesla missed analysts’ expectations on revenue and earnings per share. Tesla also announced a recall of 475,000 vehicles in the US due to a potential battery fire risk.

Additionally, Tesla faced regulatory challenges in China, where it was banned from selling its AI chips due to national security concerns. These factors contributed to the negative sentiment around Tesla stock and increased its volatility.

Tesla stock has fallen 73% from its record high in November 2021. The stock is down 69% in 2022, more than double the decline in the Nasdaq.

Tesla price crossed below 200 day moving average this is a bearish indicator.

Tesla price crossed below 200 day moving average this is a bearish indicator.

Among major carmakers, Ford is down 46% and General Motors has fallen 43%. Since its IPO in 2010, Tesla has only fallen in one other year, an 11% drop in 2016. Some analysts and investors are still optimistic about Tesla’s long-term prospects, citing its innovation, leadership, and loyal customer base.

However, others are sceptical about Tesla’s valuation, profitability, and competition. Tesla’s stock performance in the coming months will depend on how it can overcome its current challenges and deliver on growth.

Don’t underestimate Elon Musk, but bear in mind other big car manufacturers are now catching and moving ahead of Tesla in the EV race.

Moody’s is a credit rating agency that evaluates the creditworthiness of countries, companies, and other entities.

It recently upgraded the UK’s credit outlook from negative to stable, citing policy predictability, softer EU trade stance, and tax reversals.

This means that Moody’s expects the UK to have a lower risk of defaulting on its debts and to have a more stable economic outlook. Moody’s also noted some challenges for the UK, such as low growth prospects, high inflation, and the need for large investments in water and energy sectors.

It follows S&P, which dropped its negative outlook in April this year.

Stocks retreated Friday as a surge in the 10-year Treasury yield prompted broader concerns about the state of the economy.

The Dow Jones Industrial Average (DJIA) is one of the most widely followed stock market indices in the world. It tracks the performance of 30 large U.S. companies from various sectors, such as Boeing, Coca-Cola, Apple and Walmart.

The DJIA is often used as a proxy for the overall health of the U.S. economy and investor sentiment.

Market pressure

Lately, the DJIA has been under pressure as U.S. Treasury yields have climbed to their highest levels in over sixteen years.

Treasury yields are the interest rates that the U.S. government pays to borrow money by issuing bonds. When Treasury yields rise, it means that investors are demanding higher returns to lend money to the government, which reflects their expectations of higher inflation and economic growth.

Treasury yields

Higher Treasury yields can have a negative impact on the stock market for several reasons. Firstly, they increase the borrowing costs for companies and consumers, which can affect spending and profits.

Secondly, they make bonds more attractive as an alternative investment to stocks, which can reduce the demand for equities.

Thirdly, they can signal that the Federal Reserve may tighten its monetary policy sooner than expected, which can also dampen the stock market’s momentum.

The DJIA has fallen by more than 300 points in recent days as Treasury yields climbed above 5%, a level not seen since 2007. The rise in yields was driven by strong economic data, such as the September 2023 consumer price index (CPI), which showed that inflation remained elevated at 3.7% year-over-year. But only 1.7% off the Fed target of 2%.

Dow Johns Industrial Average close 20th September 2023

U.S. 10-year Treasury yield hits 5% for the first time since 2007 – Dow closes down nearly 300 points

The S&P 500 lost 1.26% to 4,224. The Nasdaq dropped 1.53% to 12,984. The Dow Jones Industrial Average lost 287 points, or 0.86%, to end at 33,127.28.

The yield on the benchmark 10-year Treasury crossed 5% for the first time in 16 years on Thursday 19th October 2023, a level that could easily spread through the economy by raising rates on mortgages, credit cards, vehicle loans and more. It retreated slightly from this value on Friday 20th October 2023.

Not to mention, it offers investors an attractive alternative to stocks.

Nokia is planning to cut up to 14,000 jobs worldwide, or some16% of its workforce, as part of a cost-cutting plan following a 69% plunge in third-quarter profits.

The Finnish technology company said the planned measures are aimed at reducing its cost base by between €800 million and €1.2 billion by the end of 2026.

The cuts were announced as the company revealed a 20% drop in third-quarter sales, which fell to €4.98 billion from €6.24 billion a year earlier. The company’s biggest unit by revenue; the mobile networks business, declined 24% to €2.16 billion, driven mainly by weakness in the North American market.

Nokia’s CEO Pekka Lundmark said the company was taking decisive action on three levels: strategic, operational and cost. He also reportedly said he remained confident about the opportunities ahead of the company.

I guess there’s not much else he could have said really.

London has regained its status as Europe’s largest stock market from Paris, boosted by rising crude oil prices.

The combined market capitalization of primary listings in London but excluding ETFs and ADRs, is now $2,888.4 billion versus Paris’s $2,887.5 billion, as of 19th October, 2023.

London had lost its position as Europe’s biggest stock market in November 2022, extending a decline that started with Britain’s vote to leave the European Union in 2016.

London market

The London market, which has a large exposure to commodity stocks, such as Shell and BP, has outperformed recently due to the surge in oil prices, which reached a seven-year high this month.

Paris, on the other hand, has been weighed down by the slump in luxury stocks, such as LVMH and Kering, which have been hit by China’s crackdown on consumption and corruption.

Shares of Chinese electric vehicle manufacturers took a hit on Thursday 18th October 2023 after Tesla reported disappointing 3Q results on Wednesday 17th October 2023.

It was the first time Tesla, co-founded by Elon Musk, missed on both earnings and revenue since Q2 2019.

On Thursday morning, Hong Kong-listed shares of Chinese EV makers BYD and Xpeng fell approximately 2.18% and 8.76%. Li Auto slid 3.14%, while Nio and Geely dropped 8.36% and 3.97%.

Elon Musk reportedly cautioned that the Tesla Cybertruck, the electric full-size pickup truck model; would not deliver substantial positive cashflow for 12-18 months after production begins.

Musk reportedly said the company is working to bring down the prices of its cars amid high interest rates. ‘I’m worried about the high interest rate environment we’re in,’ he said, adding that it will be much harder for consumers to purchase cars if interest rates were to increase further.

Tesla shares down

Tesla shares closed 4.78% lower on Wednesday 17th October 2023. Other U.S. EV rivals Lucid and Rivian fell more than 9% on the same day. Lucid’s stock dropped a day earlier after it reported disappointing Q3 EV deliveries.

Tesla shares closed 4.78% lower on Wednesday 17th October 2023.

In the first six months of the year, BYD was the world’s top EV manufacturer, contributing 21% of global sales of EVs, according to research firm Canalys. Tesla trailed behind at second place with 15% market share while German carmaker Volkswagen held 7% market share in third place.

Price pressure

EV players are under pressure from a price war to gain market share amid intense competition.

Tesla introduced a number of price cuts over the last few months, especially in China – the world’s biggest EV market.

Rivals BYD, Nio, Li Auto and Xpeng have also joined Tesla in lowering the prices for some of their EV models.

Shares in BYD, (Build Your Dreams), jumped this week after it said it expected third-quarter profits to more than double compared with last year.

BYD is now ahead of Tesla in quarterly production – and second to the U.S. car maker in global sales.

The curbs are aimed at closing loopholes that became apparent after the U.S. announced export curbs on microchips in October 2022. The restrictions are designed to prevent China’s military from importing advanced semiconductors or equipment.

Nvidia has said in a filing that the new export restrictions will block sales of two high-end artificial intelligence chips it created for the Chinese market – A800 and H800. It said that one of its gaming chips will also be blocked.

Nvidia Corp one month chart – closed at 439.38 17th October 2023

Although the curbs also affect other chip makers, analysts believe Nvidia will be hit the hardest because China accounts for up to 25% of its revenues from data centre chip sales. Nvidia’s shares, which are considered a star stock, fell by as much as 4.7% in the wake of the announcement.

Semiconductor Industry Association

The Semiconductor Industry Association, which represents 99% of the U.S. semiconductor industry by revenue, said in a statement that the new measures are ‘overly broad‘ and ‘risk harmingthe U.S. semiconductor structure without advancing national security as they encourage overseas customers to source elsewhere’.

China reacts

A spokesperson for the Chinese embassy also said that it ‘firmly opposes‘ the new restrictions, which also target Iran and Russia and go into effect in 30 days.

Nvidia stock falls after restrictions on AI chip exports from U.S. to China

Two months ago, China retaliated by restricting exports of two materials, gallium and germanium, which are key to the semiconductor industry.

The materials are ‘minor metals‘, meaning that they are not usually found on their own in nature, and are often the by-product of other processes. It’s not only the U.S., Japan and the Netherlands – which is home to key chip equipment maker ASML – have also imposed chip technology export restrictions on China.

Fallout

The constant ‘fall-out’ between the world’s two biggest economies has raised concerns over the rise of so-called ‘resource nationalism‘ – a practice where governments hoard critical materials to exert influence over other countries.

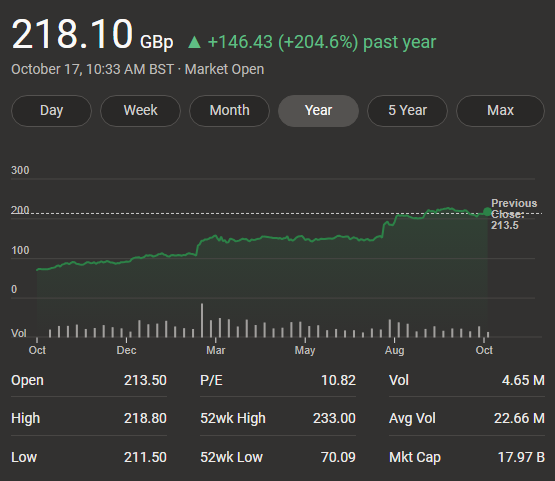

Rolls-Royce, the British manufacturer of aircraft engines, amongst many other products announced on Tuesday 16th October 2023, that it plans to axe up to 2,500 jobs worldwide. The company said that the decision is part of its plans for a simpler, more streamlined, and more efficient organisation.

The job cuts are expected to affect mostly non-engineering roles across its global operations, and are likely to impact UK staff.

The restructuring is one of the most significant steps taken by the new chief executive, who took over at the start of the year.

He has described the company as ‘a burning platform‘ and said one of its main subsidiaries had been ‘grossly mismanaged‘.

Challenge

The news comes as Rolls-Royce faces a challenging business environment due to the COVID-19 pandemic, which severely affected the aviation industry.

The company has already cut 9,000 jobs and raised capital from shareholders during the crisis. However, its share price has recovered in the last year, thanks to a resurgence in aviation demand and the early results of its transformation plan.

Rolls-Royce share price has enjoyed a healthy recovery in 2023

The company, which makes engines for aircraft, is based in Derby. It employs 42,000 people around the world with about half based in the UK.

It employs 13,700 people in Derby, and a further 3,400 people in Bristol.

The world may be facing ‘the most dangerous time… in decades’, bank boss Jamie Dimon has reportedly warned.

The chief executive of JP Morgan Chase told investors recently that he was concerned about the risks to the economy from rising geo-political tensions. He said wars in Ukraine and Israel could hit energy and food prices, and global trade.

Thousands have been killed in Israel and Gaza after an unprecedented attack by Palestinian militant group Hamas. Mr Dimon, who leads America’s biggest bank, was speaking as the firm revealed its latest quarterly results.

Banking the profits from higher interest rates

The bank reported $13 billion (£10.7 billion) in profit over the three months to September 2023, up 35% from the same period in 2022.

Dimon said the bank had benefited from U.S. households and business in healthy financial shape but warned that he remained cautious about the state of the global economy, given the many risks emerging. What about the effect of interest rate increases on profits the bank has benefitted from too?

‘My caution is that we are facing so many uncertainties out there,‘ he reportedly said. So helpful Mr. Dimon. He told investors they should be prepared to face higher interest rates, persistent inflation, as well as fallout from the violent conflicts.

How perceptive?

I wouldn’t necessarily call his comments very intuitive – interest, inflation and conflict is there for all to see.

Shame he didn’t use his super magical powers of detection to get ahead of the inflation problem earlier.

Microsoft’s $69 billion revised offer to buy Call of Duty-maker Activision Blizzard has been approved by UK regulators.

The Competition and Markets Authority (CMA) said the deal addressed its concerns, after the watchdog blocked the original $69bn (£59bn) bid in April 2023. The green light marks the culmination of a near two-year fight to secure the gaming industry’s biggest-ever takeover.

CMA criticised Microsoft’s conduct.

After the competition watchdog blocked the takeover earlier this year, Microsoft’s president hit out at the CMA’s decision which it said was ‘bad for Britain’.

The CMA chief executive reportedly said: ‘Businesses and their advisors should be in no doubt that the tactics employed by Microsoft are no way to engage with the CMA. Microsoft had the chance to restructure during our initial investigation but instead continued to insist on a package of measures that we told them simply wouldn’t work. Dragging out proceedings in this way only wastes time and money’.

The CMA also said the revised deal would ‘preserve competitive prices’ in the gaming industry and provide more choice and better services.

Prior to the approval, the deal, which makes Microsoft the owner of Call of Duty, World of Warcraft, Overwatch and Candy Crush, could not be finalised globally.

Under the restructured transaction, Microsoft will not acquire cloud rights for existing Activision PC and console games, or for new games released by Activision during the next 15 years. Instead, these rights will be divested to Ubisoft Entertainment before Microsoft’s acquisition of Activision, according to the CMA.

Vice Chair and President, Brad Smith seem happy after saying it would be ‘bad for Britain.

‘We’re grateful for the CMA’s thorough review and decision today. We have now crossed the final regulatory hurdle to close this acquisition, which we believe will benefit players and the gaming industry worldwide’.

Buying the dip means purchasing an asset, usually a stock, when its price has dropped. The expectation is that the drop is a short-term anomaly, and the asset’s price will soon go back up. It is a strategy that some traders and investors use to take advantage of price fluctuations and profit from market rebounds.

However, buying the dip can also be risky, as there is no guarantee that the price will recover or that the asset is not in a long-term downtrend. Therefore, it is important to do your research, use indicators, and have a risk management plan before buying the dip.

Current market situation and general ‘readout’

The S&P 500 is still ‘buy the dip’ for the next six months,’ some analysts suggest.

In some reports, it is expected that the profit cycle will be positive over the next six months and for data to improve before a consumer-spending led downturn leads to a selloff in U.S. stocks! That’s the ‘general’ readout.

Corporate profit expectations are behind much of that forecast for stocks. Analysts expect profit growth to accelerate over the next two quarters and see the S&P 500 in a range of 4,050 to 4,750. A mild recession in early or middle 2024 should lead to a higher risk premium, pushing the S&P 500 back close to 3,800. This is all conjecture.

Other analysts doubt the earnings uplift potential and anticipate stocks to fall back sooner as PE ratios sit at an already high level.

Take your pick

My view, for what it’s worth, is for stocks to climb for the time being through into the New Year and then to face pullback.

Truth is, no one knows. We can all make educated guesses.

Just watch the markets and be ready for the fall – that is coming for sure!

Cybersecurity is a very important and relevant topic in today’s world. It refers to the practice of protecting systems, networks, and programs from digital attacks that can harm individuals and organizations.

Cyberattacks will all have malicious intent, such as accessing, changing, or destroying sensitive information; extorting money from users via ransomware; or interrupting normal business processes.

Cybersecurity aims to prevent or mitigate these attacks by using various technologies, measures, and practices.

There are many types of cybersecurity, depending on the domain or layer of IT infrastructure that needs to be protected.

Critical infrastructure security

This protects the computer systems, applications, networks, data and digital assets that a society depends on for national security, economic health and public safety. For example, the power grid, the water supply, the transportation system, the health care system, etc.

In the United States, there are some guidelines and frameworks for IT providers in this area, such as the NIST cybersecurity framework and the CISA guidance.

Network security

This prevents unauthorized access to network resources and detects and stops cyberattacks and network security breaches in progress. For example, firewalls, antivirus software, encryption, VPNs, etc. Network security also ensures that authorized users have secure access to the network resources they need, when they need them.

Application security

This protects applications from cyberattacks by ensuring that they are designed, developed, tested, and maintained with security in mind. For example, code reviews, vulnerability scanning, penetration testing, secure coding practices, etc. Application security also involves educating users about safe and responsible use of applications.

Cyberattacks will all have malicious intent, such as accessing, changing, or destroying sensitive information; extorting money from users via ransomware; or interrupting normal business processes.

There are many more types of cybersecurity, such as cloud security, endpoint security, data security, identity and access management (IAM), etc. Each type of cybersecurity has its own challenges and solutions.

Companies to watch

Cybersecurity companies such as CrowdStrike, Okta, Zscaler and Palo Alto Networks are valuable assets with businesses willing to pay good money to protect against hackers.

Stocks rallied Friday 6th October 2023 even after the release of stronger-than-expected U.S. jobs data and an increase in Treasury yields.

The U.S. economy added 336,000 jobs in September 2023, the Labour Department said. Economists expected 170,000 jobs.

Confused?

Stocks posted a surprise turnaround on Friday, 6th October 2023 after initially falling on a hotter-than-expected jobs report. At its session low, the Dow had fallen some 270 points, then surged by more than 400 points at in intraday trading. The Nasdaq and the S&P 500 also lost ground too only but then quickly recovered the losses.

Unclear

Traders were unclear as to the reason for the intraday reversal. Some noted it could be the softer wage number in the jobs report that made investors rethink their earlier bearish stance. Others noted the pullback in yields from the day’s highs.

Rally

The rally may just be because the market had been extremely oversold with the S&P 500 at one point in the week down more than 8% from its high earlier this year.

Yields initially surged after the report, with the 10-year Treasury rate trading near its highest level in 16 years. The benchmark rate later eased from those levels, but was still up around 6 basis points at 4.78%.

Extreme market movements maybe here for a while yet.

The stock market is influenced by many factors, such as economic data, earnings reports, geopolitical events, investor sentiment, and technical indicators.

Some analysts have suggested that the recent sell-off in the market may have created some oversold conditions that could lead to a relief rally or a bounce back in the near future.

Stochastics oscillation

One of the technical indicators that some traders use to identify buy and sell signals is the stochastics oscillator, which measures the momentum of price movements. The stochastics oscillator consists of two lines: the %K line and the %D line.

The %K line shows the current position of the price relative to its high and low range over a certain period of time, usually 14 days. The %D line is a moving average of the %K line, usually a three-day average. When the %K line crosses above the %D line, it is considered a bullish signal, indicating that the price may be reversing from a downtrend to an uptrend.

When the %K line crosses below the %D line, it is considered a bearish signal, indicating that the price may be reversing from an uptrend to a downtrend.

80/20 analysis

The stochastics oscillator also has two levels: 20 and 80. When the %K line falls below 20, it means that the price is oversold, meaning that it has fallen too much and may be due for a rebound. When the %K line rises above 80, it means that the price is overbought, meaning that it has risen too much and may be due for a pullback.

Careful research before buying is paramount to successful trade

The FTSE 100 index, which tracks the performance of 100 large companies listed on the London Stock Exchange, has recently fallen below 20 on the stochastics oscillator, indicating that it may be oversold and ready for a bounce back.

No guarantee

However, this is not a guarantee, as other factors may also affect the market direction. Therefore, it is advisable to use stochastics in conjunction with other tools, such as trend lines, support and resistance levels, moving averages, and other technical indicators.

Additionally, some traders use different settings for the stochastics oscillator, such as changing the time period or the smoothing factor, to suit their own trading style and preferences. Always though, long term investing produces far better results over time as it smooths out the ‘ups and downs’.

In summary, there is no definitive answer to whether the stock market is building up to a major buy signal again right now, as different traders will have different opinions and strategies and views. But one possible way to gauge the market sentiment and momentum is to use the stochastics oscillator, which can provide some clues about potential reversals and opportunities in the market.

Note

This indicator should not be used in isolation, but rather in combination with other tools and analysis – it is just that, a tool. Good well-established companies that have good track records over many many years are a good place to look for long term returns. But even then, do your thorough research first.

So, what next?

The interest-rate/inflation correlation is crucial, because nominal company earnings grow faster when inflation is higher. That does not mean investors should welcome inflation, since higher inflation also means that future years’ earnings must be discounted at a higher rate.

But for many behavioural reasons, investors place greater weight on the negative impact of the greater discount rate than on the higher nominal earnings-growth rate that typically accompanies higher inflation.

Inflation illusion

Economists refer to this investor error as ‘inflation illusion’. Perhaps the seminal study documenting how this error impacts the stock market was conducted by Jay Ritter of the University of Florida and Richard Warr of North Carolina State University. They found that investors systematically undervalue stocks in the presence of high inflation.

Investors will make the same error, in reverse, when inflation and interest rates start to come down. That’s why the foundation of a likely big buy signal is currently being built.

Maybe the buy signal is about to go green for a quick buying opportunity. But be careful, in this environment it can switch again very quickly.

Remember, always do your own research carefully before buying.

The Nikkei 225 index, is a stock market index for the Tokyo Stock Exchange.

The Nikkei 225 reached its all-time high on 29 December 1989, during the peak of the Japanese asset price bubble, when it reached an intra-day high of 38,957.44, before closing at 38,915.87. This was after a decade-long bull run throughout the 1980s, when the index grew sixfold.

Since then, the index has never surpassed this level, and has experienced several periods of decline and stagnation. As of October 4, 2023, the index closed at 30,526.88, down by 2.28% from the previous day and 8389 points off its all-time high.

Dow Jones Industrial Average (Dow) performance on 3rd October 2023.

The Dow fell more than 400 points, turning negative for the year. The main reason for the drop was the surge in U.S. Treasury yields, which reached their highest levels in 16 years.

Higher yields mean higher borrowing costs for businesses and consumers, which could hurt the economic recovery and the housing market.

S&P 500 on 3rd October 2023

Nasdaq on 3rd October 2023

The tech-heavy Nasdaq Composite gained a 0.7% on October 3rd, 2023, as some investors saw an opportunity to buy some of the high-growth stocks that had been under pressure recently.