Globalisation is a process that has woven the world together, creating interconnected networks of trade, culture, technology, and governance.

At its core, globalisation refers to the increased interaction and integration between people, companies, and governments across the globe.

This phenomenon has profound economic, political, and cultural implications, shaping the way we live and think.

Historically speaking

Historically, globalisation is not a recent occurrence; it has been evolving for centuries. The roots of globalisation can be traced back to ancient civilizations when trade routes like the Silk Road emerged around 130 BCE during the Han Dynasty of China.

The Silk Road connected Asia, the Middle East, Europe, and North Africa, facilitating the exchange of goods, ideas, religions, and innovations. While it was primarily a trade route, it also marked the first notable instances of cross-cultural interaction on a global scale.

However, the modern wave of globalisation began much later. Many historians point to the Age of Exploration in the late 15th and early 16th centuries as a pivotal moment.

European explorers like Christopher Columbus and Vasco da Gama sought new trade routes to Asia and the Americas, leading to the establishment of colonial empires.

These explorations were driven by ambitions of trade, wealth, and power, further intertwining economies and cultures.

Adam Smith, the 18th-century economist and philosopher, can also be credited with significantly influencing globalisation through his ideas. His seminal work, The Wealth of Nations (1776), laid the foundation for modern economics and advocated for free-market trade.

His philosophies supported the idea of open international markets, which became a cornerstone of globalisation in later years.

Industrial revolution

Fast forward to the 19th and 20th centuries, the Industrial Revolution and advancements in technology supercharged globalisation.

Railroads, steamships, telegraphs, and later airplanes and the internet, reduced distances and enhanced global connectivity.

This period also saw the establishment of international organisations such as the United Nations and the World Trade Organisation, further embedding globalisation into global policies.

Evolution

Today, globalisation continues to evolve. While it has brought unparalleled access to goods, services, and information, it has also sparked debates about its impact on inequality, environmental sustainability, and cultural homogenisation.

As nations and individuals grapple with its implications, globalisation remains a defining characteristic of our interconnected world. Its history is a testament to humanity’s constant quest to connect, collaborate, and innovate.

Tariffs

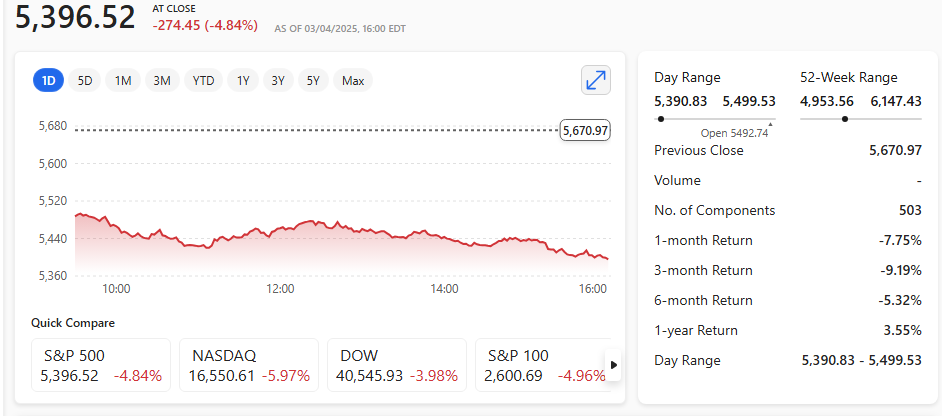

The introduction of ‘protectionist’ policies and ideals will likely lead back to globalisation in the end. Are Trump’s protectionist tariff ideals about protectionism or more about a drive to level the imbalance of global trade differences? Gobal trade will not end!

The tariffs are more about aiming to settle trade imbalances, at least according to U.S. President Trump.

Trump’s tariffs have had a significant impact on globalisation, challenging its trajectory. By imposing sweeping tariffs on imports, including a baseline 10% on goods from various countries, Trump aimed to reduce the U.S. trade deficit and reshore U.S. manufacturing.

While this approach sought to protect domestic industries, it disrupted global trade networks and raised concerns about inflation and economic instability.

These tariffs marked a shift away from decades of free trade policies that had fostered globalisation. Critics argue that such measures could lead to higher consumer prices and strained international relations.

On the other hand, proponents believe they might encourage self-reliance and industrial growth within the U.S.

The long-term effects on globalisation remain uncertain. While some see this as a step toward de-globalisation, others view it as a recalibration of trade dynamics.

The future will likely depend on how nations adapt to these changes and whether they seek collaboration or confrontation in global trade.

Globalisation is too big for it to simply… stop!