Americans are using their credit cards more than ever, pushing the total balance to over $1 trillion for the first time in history, according to a report from the New York Federal Reserve.

The report, released August 2023, showed that credit card balances rose by $45 billion to $1.03 trillion in the second quarter of 2023, reflecting robust consumer spending as well as higher prices due to inflation. The increase was the largest quarterly gain since 2008 and surpassed the previous record of $1.02 trillion set in 2019.

The rise in credit card debt also coincided with a higher payment failure rate, which measures the share of borrowers who are at least 30 days behind on their payments. The failure measure climbed to 7.2% in the second quarter, up from 6.5% in the first quarter and the highest level since 2012.

The New York Fed reportedly said that the increase in failure rates may reflect a normalization to pre-pandemic levels, as many lenders offered relief programs and forbearance options to borrowers during the Covid-19 crisis. However, some analysts warned that the high level of credit card debt could pose a risk to the financial stability of households and the economy if interest rates rise or incomes fall.

Expensive debt

Credit card debt is one of the most expensive forms of debt, and it can quickly spiral out of control if not managed. ‘Consumers should aim to pay off their balances in full every month, or at least pay more than the minimum due, to avoid paying unnecessary interest and fees.

The burden of debt is all to consuming!

Interest rates and fees on credit cards are one of the highest payable and if you fall into the debt spiral it can be almost impossible to liberate yourself from that consuming debt.

Younger users

The New York Fed also noted that credit card usage has become more widespread among Americans, especially among younger and lower-income borrowers. The share of adults with at least one credit card increased from 76% in 2019 to 79% in 2021, while the share of those with four or more cards rose from 18% to 21% over the same period.

Tool

The report suggested that credit cards have become an essential tool for many consumers to access credit and smooth purchases over time, especially during periods of economic uncertainty and volatility. However, it also cautioned that credit cards can also lead to overborrowing and financial distress if not used responsibly.

It is one of the most expensive ways to borrow money and far too easy to access.

China’s consumer price index (CPI) fell by 0.3% in August from a year ago, while the producer price index (PPI) fell by 4.4% last month. This is the first time since February 2021 that the CPI has fallen, and the 10th consecutive month that the PPI has contracted. This indicates that China is experiencing deflation pressure as demand in the world’s second-largest economy weakens.

Factors that contribute to the deflation risk

A prolonged property market slump, which reduces investment and consumption.

A plunging demand for exports, due to the global economic slowdown and trade tensions with the United States.

A subdued consumer spending, due to the coronavirus pandemic and rising unemployment.

Deflation can have negative effects on the economy

Lowering profits and incomes for businesses and households.

Increasing the real value of debt and making it harder to repay.

Reducing incentives for investment and innovation.

Creating a downward spiral of falling prices and demand.

The Chinese government and the central bank have taken some measures to stimulate the economy and prevent deflation.

Cutting interest rates and reserve requirement ratios for banks.

Increasing fiscal spending and issuing special bonds for infrastructure projects.

Providing tax relief and subsidies for businesses and consumers.

However, these measures have not been enough to offset the deflationary pressure, and some analysts expect more monetary easing and fiscal support in the coming months.

Deflation definition

Deflation is the opposite of inflation. It means that the prices of goods and services are going down over time. This may sound good for consumers, who can buy more with the same amount of money. But deflation can also have negative effects on the economy.

Deflation can be caused by a decrease in the supply of money and credit, a fall in demand, or an increase in productivity. To prevent or reverse deflation, the central bank and the government can use monetary and fiscal policies to stimulate the economy, much the same as we are now seeing to deal with ‘inflation’.

According to latest figures the country’s trade fell more sharply than expected in July 2023, as both global and domestic demand receded amid the pandemic and ongoing tensions with the United States.

China’s exports fell by 14.5% in July 2023 from a year ago, the biggest drop since February 2020, while imports dropped by 12.4%, according to Chinese data. This was much worse than the 5% decline in both exports and imports analysts were expecting.

Poor trade performance

Some of the reasons for the poor trade performance are the rising costs of raw materials, the global shortage of semiconductors, the Covid-19 outbreaks in some regions, and the U.S. sanctions on some Chinese companies.

China’s trade with the U.S., its largest trading partner, fell in the first seven months of the year. The trade slump has added pressure on China to provide more support for the economy, which has lost momentum after a strong recovery in late 2020 and early 2021.

China’s trade drop July 2023 more than expected

China’s trade situation is also closely watched by other countries, as it reflects the health of the global economy and demand for goods. Some analysts have warned that China’s trade slowdown could signal a broader weakening of consumer spending in developed economies, which could lead to recessions later this year. China’s trade data also has implications for inflation and monetary policy, as lower import prices could ease inflationary pressures and allow central banks to keep interest rates low.

China’s export to the U.S. and EU down

China’s exports to the U.S. plunged by 23.1% year-on-year in July 2023, while those to the European Union fell by 20.6%, CNBC analysis of customs data showed. Exports to the Association of Southeast Asian Nations fell by 21.4%, according to the data. Chinese imports of crude oil dropped by 20.8% in July from a year ago, while imports of integrated circuits fell by nearly 17%.

China’s imports from Russia fell by around 8% in July 2023 from a year ago, the data showed.

A slowdown in U.S. and other major economies’ growth has dragged down Chinese exports this year. Meanwhile, China’s domestic demand has remained subdued.

Growth areas

Among the few higher-value export categories that saw a significant increase in the first seven months of the year were: cars, refined oil, suitcases and bags. And for imports: paper pulp, coal products and edible vegetable oil were among the categories seeing significant growth in the January to July period from a year ago.

Chancellor Jeremy Hunt has asked the City watchdog to speed up a probe into whether people have had bank accounts closed due to their political views

It follows a row over the closure of former UKIP leader Nigel Farage’s Coutts account.

Mr Hunt requested the Financial Conduct Authority (FCA) to ‘urgently investigate how widespread this practice is, and put a stop to it’. The FCA reportedly said Mr Hunt’s request is ‘in line with our plans‘.

It comes after Mr Farage obtained a report from Coutts which indicated his political views were considered as a factor in his account closure. Mr Farage had his account re-instated and has launched a campaign against account closures which has received support from government ministers.

Express or suppress?

The FCA is already preparing to look into this, and banks also face government reforms over account closures. Mr Hunt reportedly said: ‘You can agree or disagree with Nigel Farage but everyone wants to be able to express their opinions’.

‘In today’s society, you need a bank account function and so a threat to be de-banked is a threat to your right to express your opinions‘.

Mr Hunt expressed the FCA has the power to fine banks ‘very large sums of money if they find this practice widespread’.

The Bank of England’s forecasting, which has a major impact on the UK economy, is being reviewed and has been criticised.

After the Bank raised interest rates for a 14th time in a row in an effort to slow price rises in Augts 2023, officials have predicted inflation to fall from the current rate of 7.9%, to ‘around 5%‘ by the end of the year. The Bank puts rates up when they are concerned that too much spending will send prices spiralling.

So, in light of its estimating techniques being challenged, how much faith should we put in ‘5% by Christmas’?

For the last two years, the Bank of England has been underestimating the likely rate of inflation in the short term. MPs have been critical of the Bank’s forecast, and its officials have acknowledged they have got some judgements wrong in their forecasting.

The Central Bank has also announced a review into how it makes forecasts.

This was one of the questions put to the Bank of England governor

Mr Baron:Good morning, everyone. In looking at the bank rate going forward, some of us, it is fair to say, have long believed that central banks, including the Bank of England, have been well behind the curve with regard to inflation. As the Chair has said, forecasting has been awry. The Bank of England is one among others that has been too slow in raising interest rates, allowing inflation to mushroom well above the 2% target.

I have put it as strongly as suggesting that it has been a woeful neglect of duty. It is causing real pain out there for people and businesses. We should always remember, as we sit in our, sometimes, white ivory towers, having these debates, that we are talking about people’s lives and businesses that are having to grapple with double-digit inflation and interest rates perhaps going up too quickly. I think that you get it, but it is useful to remind ourselves of that.

Why should the public have confidence in your ability to get it right going forward? What lessons do you think that you have learned? What are you going to do differently? I am not hearing a satisfactory answer to that...

See the full report here – be prepared, it’s an acquired taste and a long read…

More wrong than right

However, some critics have argued that the BoE’s forecasts are often too optimistic or pessimistic, and that they fail to capture the impact of major shocks or structural changes in the economy. For example, the BoE was widely criticised for underestimating the severity of the 2008 financial crisis and overestimating the negative effects of Brexit on the economy. Some have also questioned the usefulness of the BoE’s forecasts for guiding monetary policy decisions, as they may be influenced by political or psychological factors.

Therefore, it may be wise to take the BoE’s forecasts with a grain of salt, and not to rely on them too much for making economic or financial decisions. The BoE’s forecasts are not useless, but they are not infallible either. They are one of many sources of information and analysis that can help us understand the state and prospects of the UK economy, but they should not be treated as gospel truth.

The Bank of England has been wrong with too many forecasts, so why bother? Target 2%, actual above 10%!

According to the chancellor Jeremy Hunt, the UK economy is caught in a trap

The UK and other advanced economies are facing a low-growth trap that is hard to escape. This means that the potential growth of the economy, which depends on factors such as productivity, innovation, investment, and labour force, is very low and insufficient to meet the demand and expectations of the people.

Brexit

The UK economy has been hit by huge global shocks that have disrupted its normal functioning and recovery. These include the Covid-19 pandemic, which caused lockdowns, restrictions, and health crises; the energy crisis, which led to soaring gas prices and supply shortages; and the Brexit transition, which created uncertainty and trade barriers.

Inflation

The UK economy is also struggling with high inflation, which erodes the purchasing power of consumers and businesses. Inflation is driven by various factors, such as rising energy costs, global supply chain bottlenecks, labour shortages, and pent-up demand.

‘Don’t you just love numbers?’

The Bank of England has raised interest rates to 5.25% as of August 2023 – the highest level since 2008, to curb inflation and maintain price stability. The Bank of England inflation target is 2%.

The plan?

The chancellor reportedly has vowed to stick to the plan that he believes will bring down inflation and boost growth in the long term.

He said that he will unveil a plan in the autumn statement that will show how the UK can break out of the low-growth trap and become one of the most entrepreneurial economies in the world. He also said that he will not ‘veer around like a shopping trolley‘ and change course in response to short-term pressures.

China has been leading the global electric vehicle (EV) market for years, thanks to its large domestic demand, generous government subsidies, and well-established battery and electronics industry. However, the west is not giving up on the race to electrify the transport sector and reduce greenhouse gas emissions.

Europe reportedly surpassed China in terms of new EV registrations in 2020, driven by stricter emission regulations, higher consumer awareness, and more diverse and affordable models. The United States also saw a growth in EV sales, despite the Covid-19 pandemic and lower fuel prices. How are western countries and companies now competing with China in the EV market?

Global automakers such are using advanced tech such as driver-assist software to compete in the world’s largest EV market – China. ‘China’s domestic brands are leading the market in the development and implementation of advanced assisted driving systems, capitalizing on their early-entry advantages in the electric and intelligent vehicle sector‘, a recent report suggests.

BofA reportedly said it expects China to still be the world’s largest EV market in 2025, standing at 40%-45% market share.

Strategy

One of the strategies is to invest more in research and development, innovation, and collaboration. Western automakers are trying to improve the performance, efficiency, and cost of their EVs by developing new technologies and designs, such as advanced batteries, smart and autonomous features, and sustainable materials. They are also partnering with other players in the EV ecosystem, such as battery suppliers, charging network operators, software developers, and regulators, to create synergies and overcome challenges.

EV

Another strategy is to adapt to local market conditions and consumer preferences. Western automakers are aware that China is not a homogeneous market, but rather a complex and dynamic one with different regional characteristics, customer segments, and competitive landscapes. They are tailoring their products and services to meet the specific needs and expectations of Chinese consumers, such as offering more connectivity options, longer driving ranges, and lower prices. They are also leveraging their global brand reputation, quality standards, and customer loyalty to differentiate themselves from local competitors.

Niche markets

A third strategy is to diversify their portfolio and target niche markets. Western automakers are not only focusing on passenger cars, but also exploring other types of EVs, such as commercial vehicles, motorcycles, scooters, and buses. They are also targeting niche markets that have high growth potential or specific demands, such as luxury cars, sports cars, or green cars. By doing so, they can tap into new customer segments and create more opportunities.

The EV market is expected to grow rapidly in the coming years, as more countries and regions adopt policies and measures to support the transition to low-carbon mobility. China will remain a dominant player in the global EV scene, but the west will not lag behind.

How do EV’s compare to traditional vehicles?

Electric vehicles (EVs) are becoming more popular and competitive with traditional cars in terms of performance and cost. Here are some of the main differences and similarities between EVs and traditional cars:

Performance: EVs have a faster acceleration and are more efficient than traditional cars. They can reach high speeds in a short time, thanks to their instant torque rovided by the electric motor. They also have a smoother and quieter ride, as they do not have gears or transmissions. However, traditional cars perform better at high speeds and have a longer driving range than EVs. They can also handle different terrains and weather conditions better than EVs, as they have more power and stability.

Cost: EVs have a higher retail price than traditional cars, on average. But EVs may be a better financial deal for consumers over the long term. That’s because maintenance, repair and fuel costs tend to be lower than those for fossil fuel cars. EVs have fewer moving parts and fluids, which means they require less servicing and repairs. They also run on electricity, which is cheaper and cleaner than fossil derived fuels. However, traditional cars have lower upfront costs and more financing options than EVs. They also have a higher resale value and more availability than EVs, as they are more common and therefore familiar to buyers.

Environmental impact: EVs are more environmentally friendly than traditional cars, as they do not emit greenhouse gases or pollutants that contribute to air quality problems. They can also use renewable energy sources, such as solar or wind power, to charge their batteries and use fossil derived energy too.

However, EVs are not completely carbon-neutral, as they still depend on the electricity grid, which still uses fossil fuels to generate power. They also produce emissions during their manufacture and disposal processes.

Traditional cars, on the other hand, are a major source of carbon emissions and environmental damage, as they burn fossil fuels and release harmful substances into the atmosphere such as carbon monoxide and carbon dioxide. They also consume natural resources and create waste during their production and operation.

Fossil fuels generate power for the electric vehicle

As the EV population grows, so too will the energy requirement – and it will most likely be met moreso by fossil fuels in the short term as well as by renewables.

According to various sources, electric cars are generally cheaper to run than petrol cars in terms of fuel, road tax, maintenance, and insurance. However, the initial purchase price of electric cars is usually higher than petrol cars, so the overall cost of ownership may depend on how long you plan to keep the car and how much you drive it.

Running cost examples of electric cars vs petrol cars – (Spring 2023 data)

According to British Gas – fully charging a typical 60kW electric car at home costs £15.10 and gives you a 200-mile range, whereas filling up a petrol car with a similar range costs over £104. Electric cars also pay zero road tax, while petrol cars pay between £30 to £2,365 per year depending on their CO2 emissions. Electric cars also tend to have lower maintenance and insurance costs than petrol cars.

According to Regit – charging an electric car like the Vauxhall Corsa-E costs roughly £9.50 in electricity for a 200-mile range, while fuelling a petrol car with a similar range costs £41.63 in petrol. Electric cars also save money on road tax, maintenance, and congestion charges compared to petrol cars.

According to Which? – the electric Mini Cooper SE costs £8,000 more to buy than the petrol Mini One, but it costs £2,591 less to run over three years, mainly due to fuel savings. The electric car also pays no road tax or congestion charges, while the petrol car pays £155 and £11.50 per day respectively.

According to Auto Express – the annual running costs of an electric car are 21% less than those of a petrol car, excluding the purchase price. The average annual running cost for an electric car is £1,742, compared to £2,205 for a petrol car.

According to RAC – the annual running costs of an electric car like the Nissan Leaf are £1,233 less than those of a petrol car like the Ford Focus, excluding the purchase price. The electric car costs £1,062 per year to run, while the petrol car costs £2,295

Conclusion

There are many factors that affect the running costs of electric cars vs petrol cars, and different sources may have different assumptions and methods of calculation. However, the general trend is that electric cars are cheaper to run than petrol cars in most cases.

Hydrogen and hybrids are fast becoming future contenders. Watch this space…

No, nor me – never heard of them, but they are extremely important elements needed in microchip manufacturing and China is the world’s largest producer.

Germanium and gallium are two elements that are used in the production of semiconductor chips, which are essential for various electronic devices and technologies. They have different properties and applications, and they are both considered critical materials.

Germanium

Germanium is a metalloid, which means it has properties of both metals and non-metals. It is a shiny, hard, gray-white element that is brittle and can be cut easily with a knife. It has a high melting point of 938°C and a low boiling point of 2830°C. It is mainly obtained as a by-product of zinc production, but it can also be extracted from coal.

Germanium is used in, solar cells, fibre optic cables, infrared lenses light-emitting diodes (LEDs), and transistors. It is also used in some alloys to improve their strength and hardness. Germanium is essential for the defence and renewable energy sectors, as well as for space technologies. It can resist cosmic radiation better than silicon, and it can enhance the performance and efficiency of some semiconductors.

Gallium

Gallium is a metal that has a very low melting point of 29.8°C, which means it can melt in your hand. It is a soft, silvery-white element that can be easily cut with a knife. It has a high boiling point of 2403°C. It is mainly obtained as a by-product of processing bauxite and zinc ores.

Gallium and Germanium considered critical elements required in the production of microchips

Gallium is used in the electronics industry to produce heat-resistant semiconductor wafers that can operate at higher frequencies than silicon-based ones. It is also used in LEDs, solar panels, microwave devices, sensors, and lasers. Gallium is important for the development of new technologies such as electric vehicles, high-end radio communications, and Blu-Ray players. It can also improve the power consumption and reliability of some semiconductors.

China the largest producer

China is the largest producer and exporter of both germanium and gallium, accounting for about 60% and 80% of the global supply. However, China has recently announced new export restrictions on these two elements, requiring special licences for exporters. This move is seen as a response to the western sanctions on China’s access to advanced microchip technology.

The export curbs could affect the global supply chain of semiconductor chips and have implications for various industries and markets

Latest reports suggest that the number of people heading out to the shops fell for the first time in July in 14 years as the UK struggled with one of the wettest months on record.

Overall footfall was down by 0.3% (that doesn’t seem high to me) – in the first drop in July since 2009, latest reports suggest. High Streets were hit hardest but shopping centres and retail parks got a boost in visitor numbers.

Not all bad

Soft play areas and cinemas have enjoyed a business boost. Also holiday parks are taking last minute bookings as discounts are offered.

Aside from the rain, the rising cost of living and rail disruption were also behind the fall. Shoppers have been battling with one of the wettest Julys on record, according to provisional reports.

Don’t be too surprised when it rains in the UK

High Streets in coastal towns were especially hard hit, with footfall dropping 4.6%, as the rain kept people away from beaches.

July’s figures also appeared to demonstrate the harsh reality of the impact of interest rate rises on consumers, combined with rain and the continuing transport and rail turmoil traveller have to endure in the UK.

Moving on

Digressing from the real report here, which is the slowdown in UK shopping habits due to the rain – we ought to remember that in the South West there is a hose pipe ban. This ban has been in force since summer 2022! And, the UK looses excessive amounts of water through leaks.

Ironic isn’t it. All that rain and we just don’t store enough! How do other ‘hot’ countries manage? Anyway, at least we can go shopping, or not as the case may be!

The U.S. has lost its top credit rating from Fitch Ratings, one of the three major credit rating agencies, due to its recent political gridlock over the debt ceiling and deteriorating fiscal situation. How much does this matter?

Fitch re-calculated the U.S.’s long-term foreign-currency issuer default rating (IDR) from AAA to AA+ early August 2023, reportedly saying it was because of a ‘steady deterioration in standards of governance‘ and a lack of confidence in fiscal management.

Fitch Rating Agency downgrade U.S. from AAA to AA+ August 2023

Downgrade

The downgrade comes despite the resolution of the U.S. debt ceiling crisis in June 2023, when Congress agreed to suspend the $31.4tn borrowing limit until January 2025. Fitch warned that the U.S. faces serious long-term fiscal challenges, such as rising debt levels, unfunded social security and Medicare obligations, and the real possibility of a recession.

Disagree

Janet Yellen, the U.S. Treasury Secretary and the White House strongly disagreed with Fitch’s decision, calling it ‘arbitrary’ and ‘bizarre‘. They stated that the U.S. economy is fundamentally strong and that Treasury securities remain the world’s safest and most liquid assets. They reportedly suggested that Fitch’s calculation model is flawed and outdated.

Downgrade rattles markets

The downgrade is unlikely to have a significant impact on the U.S.’s borrowing costs or reputation, as it still retains its triple ‘A’ rating from the other two major credit rating agencies, Standard & Poor’s and Moody’s.

However, it could increase market volatility and pressure the U.S. to address its fiscal imbalances. But according to Janet Yellen these do not exist and there is no problem…?

The UK government has announced a plan to issue over 100 new oil and gas licences in the North Sea, as part of its drive to make Britain more energy independent and reduce reliance on imports. The Prime Minister said that even when the UK reaches net zero by 2050, a quarter of its energy needs will still come from oil and gas.

Carbon Capture

The new licences will be subject to a climate compatibility test and will aim to unlock carbon capture and storage and hydrogen opportunities in the region. The government has also approved two new carbon capture projects in Scotland and the Humber, which are expected to be delivered by 2030.

Criticised

The move has been criticised by environmental groups, who argue that opening up new fossil fuel projects is incompatible with the UK’s climate goals and will undermine its leadership ahead of the COP26 summit in Glasgow.

They also question the claim that domestic production is cleaner than imports, as the UK’s oil and gas sector is still responsible for significant emissions.

The government has said that it will support the transition of the North Sea industry to low-carbon technologies and protect more than 200,000 jobs in the sector. The UK government has also pledged to invest in renewable energy sources, such as offshore wind, to diversify the UK’s energy mix.

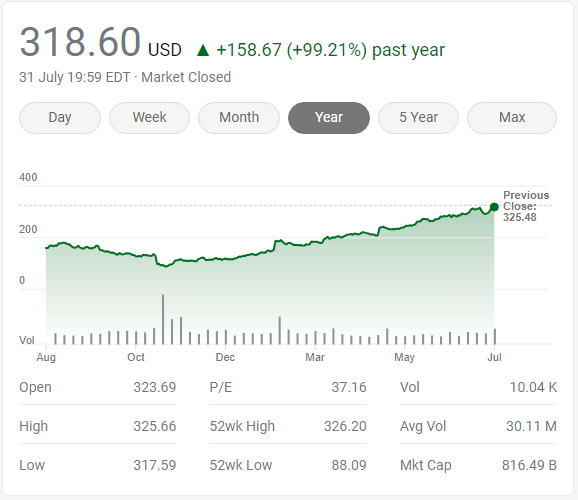

Meta Platforms, Inc. (Nasdaq: META), formerly known as Facebook, has seen its stock price soar in 2023, a straight nine month gain in a massive turnaround after a dismal performance in 2022.

Meta is the parent company of social media apps such as Facebook, Instagram, WhatsApp and Messenger, as well as the Oculus VR headset and other ventures.

Year of efficiency

Meta’s founder and CEO Mark Zuckerberg has declared 2023 as the ‘Year of Efficiency‘ for the company, as it tries to cut costs and streamline its operations. The company has also announced layoffs of about 10% of its workforce in 2022 and 2023, as part of its restructuring efforts.

Meta’s stock has almost doubled since January, making it among the top performers on the S&P 500. The company has also seen a boost in the number of daily active users on Facebook, reaching two billion as of the end of December 2022. Meta’s net worth is currently at $89.9 billion, making Zuckerberg the 12th wealthiest person on the planet, according to Bloomberg’s Billionaire Index.

Surge

Meta’s stock surge comes after a sharp decline in 2022, when the company faced regulatory scrutiny, public backlash and technical glitches over its plans to expand into the metaverse, a virtual reality world where people can interact with each other and through digital content.

Meta’s stock plummeted by over 60% last year, as Zuckerberg struggled to sell Wall Street on his vision for the future of social media.

Future

Meta is still betting on the metaverse as its long-term goal, and has been investing heavily in AI, VR and AR technologies. The company is reportedly working on a new social media app called ‘Instagram for your thoughts‘, which would allow users to share their thoughts and emotions using brain-computer interfaces.

The app could launch as soon as next month, according to latest reports.

UK house prices dropped at their fastest annual pace for 14 years in July 2023, according to Nationwide.

The building society said house prices dropped by 3.8%, which is the biggest decline since July 2009. Nationwide said mortgage interest rates remain high, making affordability a difficult for house-buyers. Mortgage costs hit the highest level for 15 years in July 2023 as lenders grappled with inflation and uncertainty over rates set by the (BoE) Bank of England. The BoE recently raised interest rates by 0.5% to 5% in a belated efforet to curb rampant inflation which is currently well above the 2% target.

Average UK house £260,828

The average price of a home in the UK is £260,828 – 4.5% below the August 2022 peak. Many first-time buyers would welcome a drop in house prices, which have climbed in recent years, including during the pandemic.

But despite July’s fall, higher mortgage rates mean housing affordability ‘remains stretched‘, Nationwide said.

Real average house price data from 1975 – 2022*

*Indicative guide only (prices adjusted for inflation).

Euro zone inflation fell in July, and new growth figures showed economic activity picking up in the second quarter of this year, but economists still fear a recession.

Headline inflation in the EU was 5.3% in July, according to preliminary data released end of July 2023, lower than the 5.5% registered in June. However, it still remains substantially above the European Central Bank’s 2% target.

EU GDP

GDP growth accelerated in the second quarter, expanding by 0.3%, higher than the 0.2% expected by analysts.

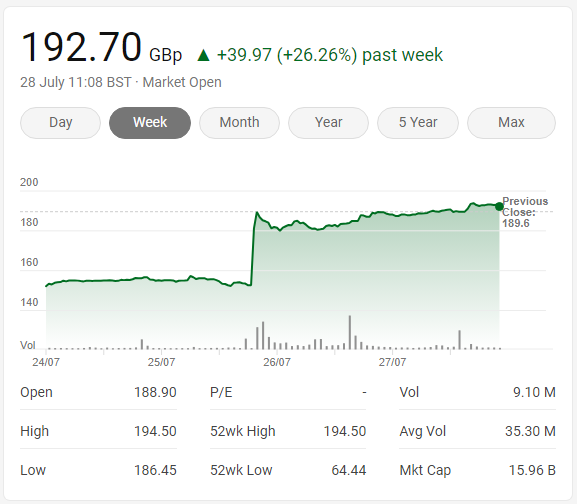

Rolls-Royce share price soared by 20% in july 2023 after it raised its profit guidance and reported strong demand in its jet engine and defence businesses.

The company, which makes engines for aeroplanes, ships and submarines, repoertedly said it expects to make between £1.2 billion and £1.4 billion in underlying operating profit this year, up from its previous forecast of £800 million to £1 billion.

The profit upgrade reflects the improvement in Rolls-Royce’s operations under its new chief executive, who took over in January with a mandate to turn the companyaround. A transformation programme was launched to boost productivity, efficiency and innovation across all divisions. It appears to be working.

Drivers

One of the main drivers of Rolls-Royce’s recovery is the revival in air travel and flying hours as Covid restrictions were eased. The company charges customers for the number of hours its jet engines run, which have dramatically rebounded from the slump caused by the pandemic. Rolls-Royce said it expects to generate £750 million in free cash flow this year, up from its previous target of £500 million.

Another factor behind Rolls-Royce’s growth is the increased defence spending following Russia’s invasion of Ukraine. The company makes propulsion systems for Royal Navy warships and submarines, as well as engines for military aircraft. Rolls-Royce reportedly said its defence unit had delivered ‘exceptional‘ performance and secured new contracts.

Share price hits 52 week high!

Rolls-Royce’s share price hit its highest level since March 2020, when the prospect of travel bans caused aviation-related stocks to plunge. The stock has almost doubled in value this year, making it the best-performing stock on the FTSE 100 over the past six months.

Analysts and investors have welcomed the signs of progress at Rolls-Royce, which had struggled with profitability and cash flow issues even before the pandemic.

Rolls-Royce is scheduled to report its half-year results next week, which are expected to show profits of between £660 million and £680 million some analysts suggest, more than double market expectations. The company said it remains confident in its medium-term outlook and its ability to deliver value for customers and shareholders.

Definitely one to watch. It’s been on my ‘share radar’ for a couple years now. Share price hit intraday high of £1.94 on 28th July 2023

UK house prices have defied expectations by increasing slightly in June 2023 but annual prices fell at the fastest rate since 2009 as soaring mortgage costs took a toll on the market, according to Nationwide Building Society.

The surprise monthly rise of 0.1% reversed a 0.1% fall in May 2023 and surprised economic forecasts of a 0.3% fall! It pushed the average cost of a house in the UK up slightly to £262,239. House prices were 3.5% lower in June 2023 compared with a year earlier, the sharpest rate of decline since 2009.

The sharp increase in borrowing costs is likely to exert a significant drag on near-term housing market activity

EZPC LOANS LTD. ‘How does 6% sound to you?’

It is important to note that the housing market is subject to fluctuations and can be influenced by various factors such as economic conditions, government policies, inflation, interest rate increases and global events.

The UK is facing a cost of living crisis as inflation has soared to its highest level in decades. The Bank of England has raised interest rates 13 times since December 2021 in an attempt to bring inflation back down to its original target of 2%. But what does this mean for consumers, savers and borrowers?

What is inflation and why is it rising?

The current UK interest rate is now: 5.0%

Inflation is the term used to describe rising prices. How quickly prices go up is called the rate of inflation. Inflation affects the purchasing power of money, meaning that the same amount of money buys less goods and services over time.

The rate of inflation in the UK is measured by two main indicators: the consumer price index (CPI) and the retail price index (RPI). The CPI is based on a basket of products and services that people typically buy, while the RPI also includes mortgage interest payments.

According to the Office for National Statistics (ONS), the CPI inflation rate was 8.7% in the year to May 2023, while the RPI inflation rate was 11.4%. This means that on average, prices were 8.7% and 11.4% higher respectively than they were a year ago.

The main drivers of inflation in the UK are:

Energy bills: Wholesale gas prices have surged due to global supply disruptions since the pandemic hit in 2020, geopolitical tensions, the war in Ukraine and increased demand. The government introduced an energy price guarantee to freeze energy prices for six months, but prices still went up 27% in October 2022. The energy price guarantee has been extended.

Shortages: The pandemic and Brexit have caused labour and supply chain issues that have affected many sectors, such as food, clothing, construction and hospitality. This has led to higher costs and lower availability of some goods and services.

Demand: As the economy recovers from the lockdowns, consumer spending has picked up, especially on leisure and travel activities. This has increased the demand for some goods and services, pushing up their prices.

How do interest rates affect inflation?

Interest rates are the cost of borrowing money or the reward for saving money. The Bank of England sets the bank rate, which is the interest rate it charges to commercial banks that borrow from it. The bank rate influences other interest rates in the economy, such as mortgage rates, loan rates and savings rates.

Interest rates climbed ever higher as the Bank of England lost control of inflation

The Bank of England uses interest rates as a tool to control inflation. The Bank has a target to keep inflation at 2%, but the current rate is more than five times that. When inflation rises, the Bank increases interest rates to make borrowing more expensive and saving more attractive. This reduces the amount of money circulating in the economy and slows down rising prices.

The Bank has raised interest rates 13 times since December 2021, from 0.1% to 5.0%. This is the highest level since March 2009, when interest rates were cut to a record low of 0.5% following the global financial crisis.

What does higher inflation mean for your money?

Higher inflation means that your money loses value over time. For example, if you had £100 in April 2022 and inflation was 8.7%, you would need £108.70 in April 2023 to buy the same amount of goods and services.

Higher inflation also affects your income, spending, saving and borrowing decisions.

Income: If your income does not keep up with inflation, you will have less purchasing power and lower living standards. For example, if your salary was £30,000 in April 2022 and increased by 2% in April 2023, you would earn £30,600. But if inflation was 8.7%, you would need £32,610 to maintain your purchasing power.

Spending: Higher inflation may encourage you to spend more now rather than later, as you expect prices to rise further in the future. However, this may also reduce your savings and increase your debt.

Saving: Higher inflation reduces the real return on your savings, meaning that your savings grow slower than prices. For example, if you had £10,000 in a savings account that paid 1% interest in April 2022, you would have £10,100 in April 2023. But if inflation was 8.7%, your savings would be worth only £9,300 in real terms.

Borrowing: Higher interest rates make borrowing more expensive, meaning that you have to pay more interest on your loans and mortgages. For example, if you had a £200,000 mortgage with a 25-year term and a 2% interest rate in April 2022, your monthly payment would be £848. But if the interest rate rose to 4.5% in April 2023, your monthly payment would increase to £1,111. Mortgage interest rates hit 6% in July 2023.

How can you protect your money from inflation?

There are some steps you can take to protect your money from inflation, such as:

Review your budget: Track your income and expenses and see where you can cut costs or increase income. Try to save more and spend less, especially on non-essential items.

Shop around: Compare prices and deals for the goods and services you need or want. Look for discounts, vouchers and cashback offers. Switch providers or suppliers if you can find better value elsewhere.

Pay off debt: This is a priority! If you have high-interest debt, such as credit cards or overdrafts, try to pay it off as soon as possible. This will reduce the amount of interest you pay and free up more money for saving or investing.

Save smartly: Look for savings accounts or products that offer interest rates higher than inflation (tricky to find). Consider diversifying your savings into different types of assets, such as stocks, bonds, property or gold. These may offer higher returns than cash in the long term, but bear in mind they also carry more risk and volatility.

Invest wisely: If you have a long-term goal, such as retirement or buying a house, you may want to invest some of your money in the stock market or other assets that can grow faster than inflation. However, you should only invest what you can afford to lose and be prepared for the ups and downs of the market. You should also seek professional advice before making any investment decisions.

Conclusion

Inflation and interest rates are two important factors that affect the UK economy and your personal finances. The UK is currently experiencing high inflation due to various factors, such as energy prices, shortages and demand. The Bank of England has raised interest rates to try to bring inflation back down to its target of 2%. Higher inflation and interest rates have implications for your income, spending, saving and borrowing decisions. You can take some steps to protect your money from inflation, such as reviewing your budget, shopping around, paying off debt, saving smartly and investing wisely.

How well has the Bank of England done to keep inflation at or close to 2%?

UK inflation rate remains high at 8.7% in May 2023

The UK inflation rate remained at 8.7% in the year to May 2023, according to the latest official figures from the Office for National Statistics (ONS). This is the same rate that was recorded in April, but down from the 10.1% level seen in March.

The ONS said that rising prices for air travel, recreational and cultural goods and services, and second-hand cars resulted in the largest upward contributions to the annual inflation rate. However, these were offset by falling prices for motor fuel and food and non-alcoholic beverages.

The ONS also reported that core inflation, which excludes energy, food, alcohol and tobacco, rose to 7.1% in May, up from 6.8% in April, and the highest rate since March 1992.

‘I’m just taking this calculator thingy to my boss, I thought it might help’. ‘Well, good idea, guess it can’t make it any worse’.

High inflation is the fault of everyone else other than the central bank

The inflation rate is measured by the Consumer Prices Index (CPI), which tracks the changes in the cost of a basket of goods and services that are typically purchased by households. The CPIH, which includes owner occupiers’ housing costs, rose by 7.9% in the year to May, up from 7.8% in April.

The high inflation rate has been driven by a combination of factors, including supply chain disruptions, labour shortages, higher energy costs, and strong consumer demand as the economy recovers from the coronavirus pandemic.

The Bank of England has a target to keep inflation at 2%, but it has said that it expects inflation to rise further in the coming months before falling back next year. The Bank has also signalled that it may raise interest rates sooner than expected to curb inflationary pressures.

However, June’s inflation reading came in below economists expectations at 7.3% A small but welcome reversal of high UK inflation. UK inflation is higher than the EU and U.S.

Are central banks doing a good job at controlling inflation? Bear in mind the inflation target is 2%…