Global markets have shown resilience in the past three days, rebounding from recent downturns as technology stocks rally amid cautious optimism.

The boost in investor confidence follows strong earnings reports from major tech firms, highlighting their ability to weather economic uncertainty.

However, lingering concerns about international trade tensions raise questions about how sustainable this recovery truly is.

Technology stocks have led the charge, with companies in artificial intelligence, cloud computing, and semiconductor production posting better-than-expected growth figures.

Investors have flocked to these sectors, hoping that innovation will drive forward profitability even amid broader market volatility.

This renewed enthusiasm has helped offset concerns over ongoing global trade disputes, which have led to tariffs and economic slowdowns in key sectors such as manufacturing and consumer goods.

Yet, beneath this recovery, risks persist. Geopolitical uncertainties, including unresolved trade negotiations between major economies, continue to cast a shadow over financial markets.

Inflationary pressures, alongside tightening monetary policies by central banks, also threaten to cool investor enthusiasm. Analysts warn that without concrete progress on trade agreements; the rebound may be short-lived.

As investors weigh the competing forces of technological optimism and trade anxieties, the market remains in a delicate balance.

The question remains: Is this recovery a sign of renewed growth, or merely a temporary respite before further economic turbulence?

With the next wave of financial reports and policy decisions on the horizon, market makers will be closely monitoring whether the tech sector’s momentum can sustain broader economic confidence – or whether trade headwinds will ultimately pull markets back into uncertainty again.

Tech gains ground again

Stocks jumped Thursday 24th April 2024 thanks to strong gains in Mega Cap tech names.

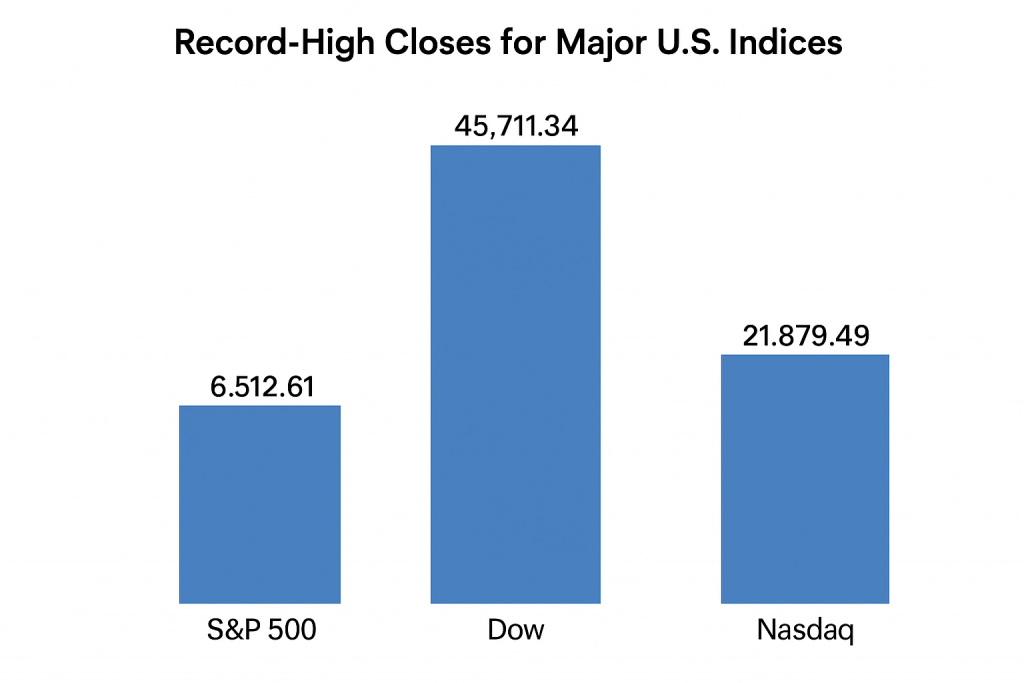

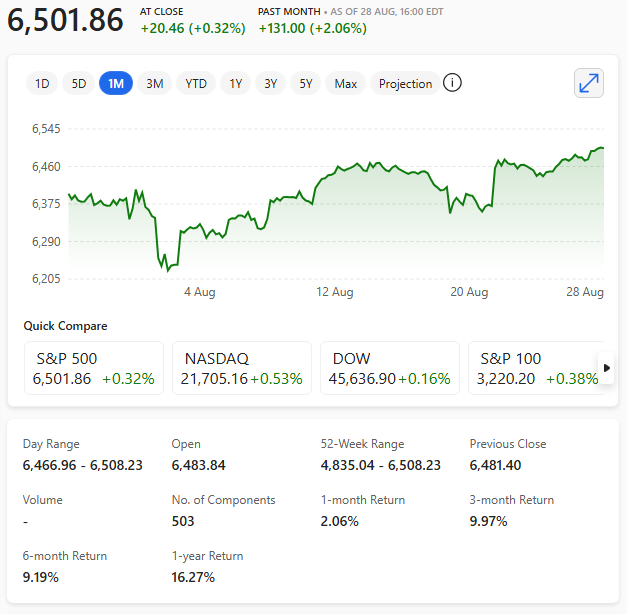

The S&P 500 ended up 2.03%, while the tech-heavy Nasdaq Composite added 2.74%.

The S&P 500 index was able to exit correction territory, ending at least 10% above its recent low set in the wake of President Donald Trump’s 2nd April 2025 ‘liberation day’ tariffs.

For the S&P 500 to maintain its rapid exit from correction territory – it now has to witness Trump’s tariff walk-back and the ‘cooling’ of a potential Fed fight.

Trump seems to be the first to have ‘blinked’ on his self-imposed tariffs suggesting the tariffs are too high and will not go any higher – thy are high enough!

China has reportedly said there are no ‘ongoing’ trade talks?

The Dow Jones Industrial Average lagged the other two indexes but still added 1.23% and retook the 40,000 for the first time since 15th April 2025.

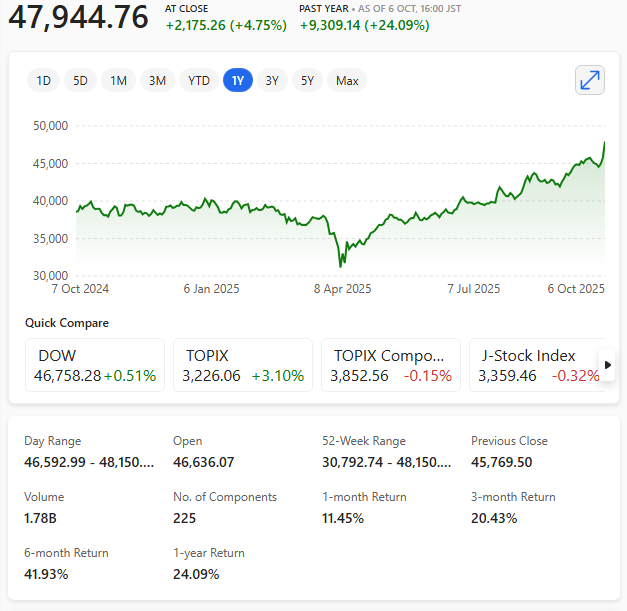

Japan’s Nikkei 225 up almost 2% and leading gains.

Alphabet shares climb after better than expected results

Alphabet reported stronger-than-expected first-quarter growth on Thursday 24th April 2025.

Alphabet’s search and advertising units are still showing strong growth despite AI competition heating up, according to its first-quarter earnings report.

The company’s overall revenue grew 12% year-on-year, higher than the 10% Wall Street expected.

Shares rose more than 5% in after-hours trading.

However, Alphabet reportedly indicated to expect ‘slight headwind’ to ads business this year.

Intel also posts results beat, but warns of tariff impact

Intel reported first-quarter results on 24th April 2025 that beat analysts’ estimates but also reportedly issued disappointing guidance.

Second-quarter revenue will come in below estimates due to elevated uncertainty driven by the macro environment, the company warned.

Intel was reported saying that President Donald Trump’s tariffs and retaliation from other countries had increased the likelihood of a U.S. recession.

Big tech gains drive markets but the uncertainty surrounding Trump’s tariffs remain.