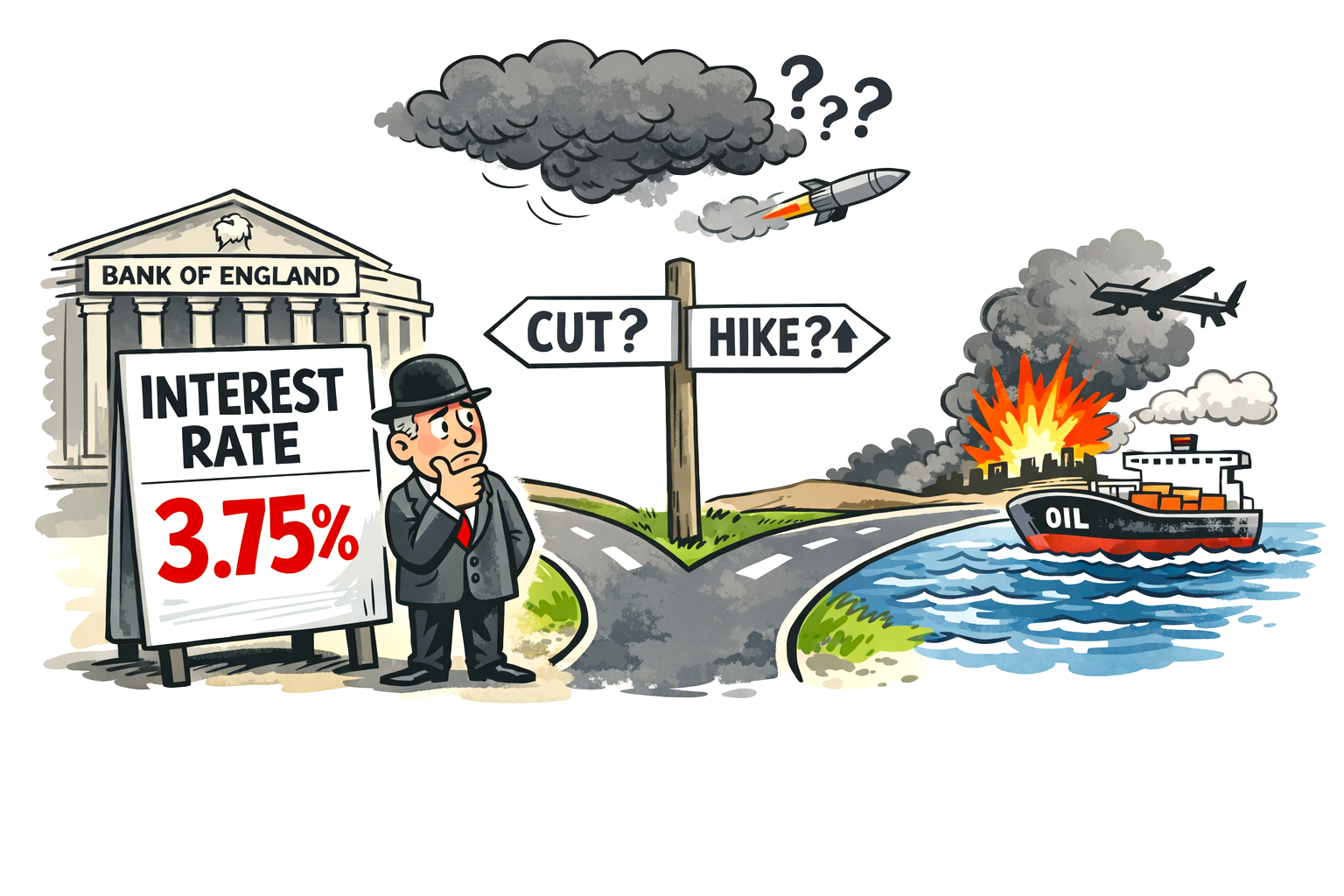

The Bank of England has held interest rates at 3.75%, opting for caution as the economic shock from the escalating conflict involving Iran ripples through global energy markets.

The Monetary Policy Committee delivered a unanimous vote to pause, a notable shift from earlier in the year when a spring rate cut had seemed almost inevitable.

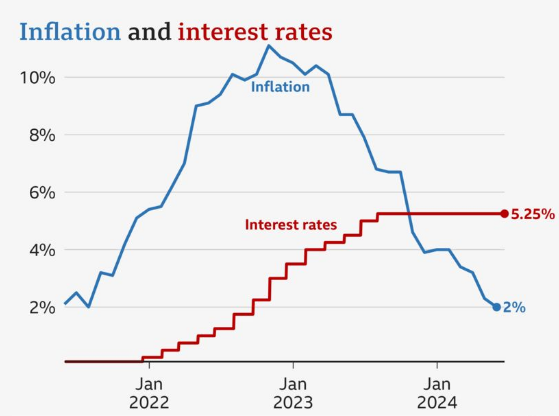

The Bank now expects inflation to rise again in the coming months, potentially reaching 3.5% as higher oil and gas prices feed through to fuel, household energy bills, and business costs.

Governor Andrew Bailey reportedly stressed that monetary policy cannot counteract a supply‑side shock of this nature, warning that the path of inflation will depend heavily on how quickly safe shipping routes through the Strait of Hormuz can be restored.

For households, the hold means no immediate relief on borrowing costs. Fixed‑rate mortgage deals have already been drifting higher as lenders price in the possibility of prolonged instability.

Some brokers report a surge in “panic buying” of mortgages as borrowers rush to lock in rates before they climb further. Savers, meanwhile, may see modestly improved offers, though competition remains muted.

Up or down?

The key question now is whether the next move is up or down. Before the conflict, markets had pencilled in two rate cuts for 2026.

That expectation has evaporated. Traders now see a non‑trivial chance of a rise to 4% later in the year, though economists caution that weak growth and a softening labour market could still restrain the Bank from tightening unless inflation accelerates sharply.

Over the next six weeks, policymakers will be watching energy prices, shipping conditions, and wage data closely.

For now, the Bank has chosen to wait, watch, and hope the shock proves temporary — but the margin for error is narrowing.