The VIX index currently (18th March 2026 – 8:30GMT) at 21.62, down around 8% from its previous close of 23.51. This drop suggests a modest easing in market fear, despite looming catalysts like the Fed decision and geopolitical tension.

VIX Snapshot – 18th March 2026

Metric

Value

Current Price

21.62 USD

Previous Close

23.51 USD

Day Change

−1.89 Down 8%

Intraday High/Low

21.72 / 21.47

52-Week High/Low

60.13 / 13.38

One-year market volatility index snapshot image 18th March 2026 at approx: 08:30 GMT

Implications

Still Elevated: A VIX above 20 suggests lingering unease, even if not full-blown panic.

Compression Context: This aligns with your “coiled spring” thesis — volatility is contained but not absent.

Directional Bias: If VIX continues to fall post-Fed, it supports a bullish breakout. A spike, however, would signal risk-off sentiment and potential sell-off.

Markets rarely sit still without reason. When they do — as they have in recent sessions, grinding sideways in an ultra‑tight range — it signals not calm but compression.

Price action becomes like a coiled spring: energy building, tension rising, and traders waiting for the moment when restraint snaps into motion.

This week’s narrow trading bands reflect a market holding its breath. Geopolitical tension in the Middle East, oil volatility, and a Federal Reserve decision all loom over investors, yet equities have refused to break down.

Futures are edging higher, European indices are opening firmer, and even the tech wobble — with Nvidia’s muted reaction to its latest showcase — hasn’t derailed broader sentiment

Tight range – a waiting game.

Historically, such tight ranges rarely resolve with a whimper. When volatility is suppressed for too long, the eventual breakout tends to be sharp and directional. The question, of course, is which way.

Right now, the evidence suggests upward. Markets have absorbed war‑driven oil swings, shrugged off hedge‑fund losses, and continued to find buyers on dips.

Breadth is stabilising, and risk appetite — surprisingly resilient given the backdrop — is creeping back into European and Asian sessions.

That doesn’t guarantee a bullish surge, but it does suggest the path of least resistance is higher.

Fed tone

If the Fed avoids surprising investors and signals comfort with the current trajectory, the spring is more likely to uncoil to the upside.

A dovish‑leaning tone could ignite a breakout as sidelined capital rushes back into equities. Conversely, a hawkish shock would release the same stored energy — but violently downward.

The market is coiled. The catalyst is imminent. And when the range finally breaks, it won’t be subtle.

You know, it almost doesn’t matter what disasters are ongoing in the world – the stock market just wants to win and go up!

Just how bad does it have to be before the stock market corrects? And what will be the catalyst to make that happen?

Debt, credit concerns, geopolitical tension, political scandal, Epstein, a rogue nuclear attack, AI failure, war or just another Trump tariff scenario?

Who knows? And does anybody really care as long as ‘making money’ isn’t interrupted.

Anthropic’s decision to reopen negotiations with the Pentagon marks a striking reversal after a very public rupture, and it underscores how central advanced AI has become to U.S. defence strategy.

The talks reportedly collapsed amid a dispute over how Claude, Anthropic’s flagship model, could be used inside military systems.

Reports indicate that the Pentagon had pushed for broad permissions, including deployment in surveillance environments and potentially autonomous weapons systems.

Safety resistance

Anthropic resisted on safety grounds. The company had sought explicit guarantees that its models would not be used for mass surveillance or lethal decision‑making, a red line that triggered the breakdown in relations.

The fallout was immediate. The Pentagon signalled it would drop Anthropic from existing programmes, despite the company’s role in a major defence contract that had already placed Claude inside classified networks.

That escalation raised the prospect of a formal blacklist, a move that would have reverberated across the wider U.S. technology sector.

For Anthropic, the stakes were equally high: losing access to government work would not only cut off a significant customer but also risk isolating the company at a moment when rivals such as OpenAI and Google are deepening their defence ties.

Compromise?

Yet both sides appear to recognise the cost of a prolonged standoff. According to multiple reports, CEO Dario Amodei has reportedly returned to the table in an effort to craft a compromise deal that preserves Anthropic’s safety commitments while allowing the Pentagon to continue using its technology.

Boundaries

Discussions are now likely focused on defining acceptable boundaries for military use — a task made more urgent by the accelerating integration of AI into intelligence analysis, battlefield logistics and autonomous systems.

This renewed dialogue is more than a corporate dispute: it is a test case for how democratic governments and frontier AI labs negotiate power, ethics and national security.

The outcome will shape not only Anthropic’s future but also the norms governing military AI in the years ahead.

The United States economy lost momentum at the end of 2025, with fourth‑quarter GDP rising just 1.4%, a sharp deceleration from the 4.4% expansion recorded in the previous quarter.

The first estimate from the U.S. Bureau of Economic Analysis underscored a cooling backdrop that contrasts with the resilience seen through much of last year.

The slowdown was broad‑based. Government spending, which had previously provided a meaningful lift, swung lower.

Exports weakened

Exports also weakened, reflecting softer global demand and a less favourable trade environment.

Consumer spending — the backbone of the U.S. economy — continued to grow but at a more subdued pace, suggesting households are becoming more cautious as borrowing costs remain elevated. Although there has been some easing in U.S. mortgage rates.

Imports declined, which mechanically supports GDP, but the underlying signal points to softer domestic demand.

Analysts had expected a stronger finish to the year, with forecasts clustered closer to 2.5%.

The miss raises questions about the durability of U.S. growth heading into 2026, particularly as fiscal support fades and the effects of tighter monetary policy continue to filter through.

Q3 surge to Q4 slowdown

The contrast with the previous quarter is stark: Q3’s surge was driven by robust consumer activity, firmer government outlays, and a rebound in exports — dynamics that have since reversed.

Even so, the latest figures do not point to an imminent recession. Investment remains mixed rather than collapsing, and consumer spending is still contributing positively.

But the data does reportedly suggest the economy is entering a more fragile phase, where small shocks could have outsized effects.

For policymakers, the report complicates the Federal Reserve’s path. Inflation has eased but remains above target, and a softer growth profile may strengthen the case for rate cuts later in the year — though officials will want clearer evidence before shifting course.

October 2025 saw a notable upswing in global equity markets, with artificial intelligence (AI) emerging as a key driver of investor enthusiasm.

In the United States, major indices closed the month firmly in the green, buoyed by strong third-quarter earnings and renewed confidence in AI’s transformative potential.

Tech giants such as Nvidia, Amazon, and Palantir posted robust results, reinforcing the narrative that AI is not just hype—it’s reshaping business fundamentals.

Nvidia’s leadership in AI chips and Amazon’s expanding AI-driven logistics were particularly well received, while Palantir’s government contracts underscored AI’s strategic reach.

The Federal Reserve’s decision to cut interest rates by 0.25% added further momentum, making growth stocks more attractive and amplifying the rally in AI-heavy portfolios.

Analysts noted that investor sentiment was bolstered by easing trade tensions and a cooling inflation outlook, but it was AI’s ‘secular tailwind of extreme innovation’ that truly captured market imagination.

While some caution that valuations may be running hot, the October 2025 rally suggests that AI is now central to market dynamics. A pullback is likely soon.

As 2025 draws to a close, investors are watching closely to see whether the optimism translates into durable gains—or signals the start of an AI bubble.

This marks the second consecutive cut in 2025 amid economic uncertainty and a government data blackout.

In a move aimed at supporting growth, the Federal Reserve reduced its benchmark interest rate by 0.25% following its October policy meeting.

The decision, reportedly backed by a 10–2 vote from the Federal Open Market Committee, reflects growing concern over a weakening labour market and subdued consumer confidence.

Chair Jerome Powell acknowledged the challenges posed by the ongoing U.S. government shutdown, which has delayed key economic reports.

With official data frozen, the Fed relied on private indicators showing a slowdown in hiring and modest inflation. The Consumer Price Index rose just 3% year-on-year, below the Fed’s long-term target.

While the rate cut aims to ease borrowing costs and stimulate investment, Powell cautioned against assuming further reductions in December.

He emphasised that future decisions would depend on incoming data and evolving risks. It is not a done deal.

The Fed also announced plans to end quantitative tightening (QT) by 1st December 2025, signalling a broader shift towards monetary easing.

Markets responded cautiously, with investors weighing the implications for growth, inflation, and the Fed’s credibility.

Markets, after a short rally during the week, were subdued after the announcement.

Scaling the Summit:Markets Hit Record Highs Amid Global Uncertainty led by the Nasdaq and S&P 500 reflecting the AI race

Global stock hit new highs October 2025

🌍 Country

📈 Index Name

🗓️ Date

🔝 Closing Value

🇺🇸 United States

S&P 500

Oct 27

6,875.16

🇺🇸 United States

Dow Jones

Oct 27

47,544.59

🇺🇸 United States

Nasdaq Composite

Oct 27

23,637.46

🇬🇧 United Kingdom

FTSE 100

Oct 24

9,662.00

🇳🇱 Netherlands

AEX Index

Oct 28

966.82

🇮🇳 India

Nifty 50

Oct 28

25,966

🇮🇳 India

Sensex

Oct 28

84,778.84

🇯🇵 Japan

Nikkei 225

Oct 28

50,342.25

🇯🇵 Japan

TOPIX

Oct 28

3,285.87

These rallies were largely fueled by optimism over a potential U.S.–China trade deal, cooler inflation data, and expectations of interest rate cuts from the Fed.

The latest U.S. inflation figures show a modest increase in consumer prices. The annual rate rose to 3.0% in September 2025, up from 2.9% in August. 2025.

Core inflation—which excludes volatile food and energy prices—also rose by 0.2% in September. This brought the year-on-year rate to 3.0%, again undercutting forecasts of 3.1%.

A notable contributor to the headline figure was a 4.1% surge in petrol prices. This offset declines in other areas such as used vehicles and household furnishings.

Federal Reserve

The data arrives just ahead of the Federal Reserve’s next policy meeting, where a 0.5% rate cut is widely anticipated. Softer inflation readings have buoyed market sentiment, with futures posting gains on hopes of looser monetary policy.

Despite a partial government shutdown, the inflation report was released on schedule, underscoring its significance for financial markets and policymakers.

With inflation now hovering near the Fed’s target, attention turns to wage growth and consumer spending as key indicators of future price stability.

The next CPI update is due mid-November.

This CPI news added to the possibility of a Fed rate cut in conjunction to the possibility of a U.S. China ‘tariff trade’ deal and relaxation of Rare Earth material sales pushed markets to new all-time highs!

Influential figures and institutions are sounding the AI alarm—or at least raising eyebrows—about the frothy valuations and speculative fervour surrounding artificial intelligence.

Who’s Warning About the AI Bubble?

🏛️ Bank of England – Financial Policy Committee

View: Stark warning.

Quote: “The risk of a sharp market correction has increased.”

Why it matters: The BoE compares current AI stock valuations to the dotcom bubble, noting that the top five S&P 500 firms now command nearly 30% of market cap—the highest concentration in 50 years.

🏦 Jerome Powell – Chair, U.S. Federal Reserve

View: Cautiously sceptical.

Quote: Assets are “fairly highly valued.”

Why it matters: While not naming AI directly, Powell’s remarks echo broader concerns about tech valuations and investor exuberance.

🧮 Lisa Shalett – Chief Investment Officer, Morgan Stanley Wealth Management

View: Deeply concerned.

Quote: “This is not going to be pretty” if AI capital expenditure disappoints.

Why it matters: Shalett warns that 75% of S&P 500 returns are tied to AI hype, likening the moment to the “Cisco cliff” of the early 2000s.

🌍 Kristalina Georgieva – Managing Director, IMF

View: Watchful.

Quote: Financial conditions could “turn abruptly.”

Why it matters: Georgieva highlights the fragility of markets despite AI’s productivity promise, warning of sudden sentiment shifts.

🧨 Sam Altman – CEO, OpenAI

View: Self-aware caution.

Quote: “People will overinvest and lose money.”

Why it matters: Altman’s admission from inside the AI gold rush adds credibility to bubble concerns—even as his company fuels the hype.

📦 Jeff Bezos – Founder, Amazon

View: Bubble-aware.

Quote: Described the current environment as “kind of an industrial bubble.”

Why it matters: Bezos sees parallels with past tech manias, suggesting that infrastructure spending may be overextended.

🧠 Adam Slater – Lead Economist, Oxford Economics

View: Analytical.

Quote: “There are a few potential symptoms of a bubble.”

Why it matters: Slater points to stretched valuations and extreme optimism, noting that productivity projections vary wildly.

🏛️ Goldman Sachs – Investment Strategy Division

View: Cautiously optimistic.

Quote: “A bubble has not yet formed,” but investors should “diversify.”

Why it matters: Goldman acknowledges the risks while maintaining that fundamentals may still justify valuations—though they advise caution.

AI Bubble voices infographic October 2025

🧠 Julius Černiauskas and the Oxylabs AI/ML Advisory Board

🔍 View: The AI hype is nearing its peak—and may soon deflate.

Černiauskas warns that AI development is straining environmental resources and public trust. He’s pushing for responsible and sustainable AI practices, noting that transparency is lacking in how many models operate.

Ali Chaudhry, research fellow at UCL and founder of ResearchPal, adds that scaling laws are showing their limits. He predicts diminishing returns from simply making models bigger, and expects tightened regulations around generative AI in 2025.

Adi Andrei, cofounder of Technosophics, goes further: he believes the Gen AI bubble is on the verge of bursting, citing overinvestment and unmet expectations

🧠 Jamie Dimon on the AI Bubble

🔥 View: Sharply concerned—more than most as widely reported

Quote: “I’m far more worried than others about the prospects of a downturn.”

Context: Dimon believes AI stock valuations are “stretched” and compares the current surge to the dotcom bubble of the late 1990s.

📉 Key Warnings from Dimon

“Sharp correction” risk: He sees a real danger of a sudden market pullback, especially given how AI-related stocks have surged disproportionately—like AMD jumping 24% in a single day after an OpenAI deal.

“Most people involved won’t do well”: Dimon told the BBC that while AI will ultimately pay off—like cars and TVs did—many investors will lose money along the way.

“Governments are distracted”: He criticised policymakers for focusing on crypto and ignoring real security threats, saying: “We should be stockpiling bullets, guns and bombs”.

“AI will disrupt jobs and companies”: At a trade event in Dublin, he warned that AI’s ubiquity will shake up industries and employment across the board.

And so…

The AI boom of 2025 has ignited a speculative frenzy across global markets, with tech stocks soaring and investors piling into anything labelled “AI-adjacent.”

But beneath the euphoria, a chorus of high-profile warnings is growing louder. From the Bank of England and IMF to JPMorgan’s Jamie Dimon and OpenAI’s Sam Altman, concerns are mounting that valuations are dangerously stretched, capital is overconcentrated, and the narrative is outpacing reality.

Dimon likens the moment to the dotcom bubble, while Altman admits many will “lose money” chasing the hype. Analysts point to classic bubble signals: retail mania, corporate FOMO, and earnings divorced from fundamentals.

Even as AI’s long-term utility remains promising, the short-term exuberance may be setting the stage for a sharp correction.

Whether it’s a pullback or a full-blown crash, the mood is shifting—from uncritical optimism to wary anticipation.

The question now is not whether AI will change the world, but whether markets have priced in too much, too soon.

We have been warned!

The AI bubble will pop – it’s just a matter of when and not if.

Gold has surged to an unprecedented high, crossing the $4,000 per ounce mark for the first time on 7th October 2025.

The precious metal peaked at $4,014.60, driven by a potent mix of geopolitical instability, expectations of U.S. interest rate cuts, and sustained central bank buying. This marks a 52% rise since January 2025, making it the strongest annual rally since 1979.

It continued its ascent into the 8th October 2025 touching $4,045 in early trade, likely with more to come. That’s over £3,000 per troy ounce.

The rally reflects a flight to safety as investors seek refuge from volatile bond markets, a weakening dollar, and the ongoing U.S. government shutdown.

One-year gold price chart – looking at December 2025 futures

With key economic data delayed and the Federal Reserve expected to cut rates twice before year-end, gold’s appeal as a non-yielding asset has intensified.

Physical demand remains robust, particularly in India, where festive buying and a weaker Rupee have pushed domestic prices to ₹1,30,300 per 10 grams in Delhi.

Meanwhile, institutional investors and sovereign funds continue to accumulate gold, signalling long-term strategic shifts away from traditional reserve currencies.

While technical indicators suggest the market may be overbought in the short term, analysts expect any correction to be modest.

For now, gold’s glittering ascent underscores a broader loss of confidence in conventional assets—and a renewed faith in timeless value.

It’s one of those classic Wall Street paradoxes—where bad news somehow fuels bullish momentum. What’s going on?

News round-up

S&P 500 closes above 6,700 after rising 0.34%. Samsung and SK Hynix join OpenAI’s Stargate. Taiwan rejects U.S. proposal to split chip production. Trump-linked crypto firm plans expansion. Some stocks that doubled in the third quarter.

Bleak Headlines vs. Market Optimism

U.S. Government Shutdown: The federal government ground to a halt, but markets didn’t flinch. In fact, the S&P 500 rose 0.34% and closed above 6,700 for the first time.

ADP Jobs Miss: Private payrolls fell by 32,000 in September 2025, a sharp miss – at least compared to the expected 45,000 gain. Yet traders shrugged it off as other bad news is shrugged off too!

Fed Rate Cut Hopes: Weak data often fuels expectations that the Federal Reserve will cut interest rates. Traders are now betting on a possible cut in October 2025, which tends to boost equities.

Historical Pattern: According to Bank of America, the S&P 500 typically rises ~1% in the week before and after a government shutdown. So, this isn’t unprecedented—it’s almost ritualistic at this point.

Why the Market’s Mood Diverges

Animal Spirits: Investors often trade on sentiment and positioning, not just fundamentals. If they believe the Fed will ease policy, they’ll buy risk assets—even in the face of grim news.

Data Gaps: With the Bureau of Labor Statistics’ official jobs report delayed due to the shutdown, the ADP report gains more weight. But it’s historically less reliable, so traders may discount it.

Tech Tailwinds: AI stocks and semiconductor news (e.g., Samsung and SK Hynix joining OpenAI’s Stargate) are buoying sentiment, especially in Asia-Pacific markets.

U.S. Government Shutdown October 2025

Prediction

Traders in prediction markets are betting the shutdown will last around two weeks. Nothing too radical, since that’s the average length it takes for the government to reopen, based on data going back to 1990.

The government stoppage isn’t putting the brakes on the stock market momentum. Are investors getting too adventurous?

History shows the pattern is not new. The S&P 500 has risen an average of 1% the week before and after a shutdown, according to data from BofA.

Even the ADP jobs report, which missed expectations by a wide margin, did little to subdue the animal spirits.

Private payrolls declined by 32,000 in September 2025, according to ADP, compared with a 45,000 increase reportedly estimated by a survey of economists.

Payroll data

The Bureau of Labor Statistics’ (BLS) official nonfarm payrolls report is now stuck in bureaucratic purgatory and likely not being released on time.

The U.S. Federal Reserve might place additional weight on the ADP report — though it’s not always moved in sync with the BLS numbers. Traders expect weak data would prompt the Fed to cut interest rates in October 2025.

It’s a bit like watching a storm roll in while the crowd cheers for sunshine—markets are forward-looking, and sometimes they see silver linings where others see clouds.

Summary

Event

Detail

🏛️ Government Shutdown

Began Oct 1, 2025. Traders expect ~2 weeks based on historical average

📉 ADP Jobs Report

Private payrolls fell by 32,000 vs. expected +45,000

📈 S&P 500 Close

Rose 0.34% to close above 6,700 for the first time

The term ‘AI super cycle’ is gaining traction among top investors, and for good reason.

According to recent commentary from leading venture capitalists, we may be entering a prolonged period of exponential growth in artificial intelligence—one that could reshape industries, economies, and even the nature of work itself.

Unlike previous tech booms, this cycle isn’t driven by a single breakthrough. Instead, it’s the convergence of multiple forces: unprecedented computing power, vast datasets, and increasingly sophisticated models.

From generative AI tools that write code and craft marketing copy, to autonomous systems revolutionising logistics and healthcare, the pace of innovation is staggering.

What makes this cycle ‘super’ isn’t just the technology—it’s the scale of adoption. AI is no longer confined to Silicon Valley labs or niche enterprise solutions.

It’s being embedded into everyday workflows, consumer apps, and national infrastructure. Governments are racing to regulate it, while companies scramble to integrate it before competitors do.

Some analysts believe this cycle could last 20 years, echoing the longevity of the internet era. But unlike the dot-com bubble, AI’s utility is already tangible.

Productivity gains, cost reductions, and creative augmentation are being realised across sectors—from finance and pharmaceuticals to education and entertainment.

Still, the super cycle isn’t without risk. Ethical concerns, data privacy, and algorithmic bias remain unresolved. And as AI systems become more autonomous, questions of accountability and control grow sharper.

Some also suggest the market is ‘frothy’ (including the Fed) and is due a correction or at the very least a pullback.

Yet for now, the momentum is undeniable. Investors are pouring billions into AI startups, chipmakers are scaling up production, and global markets are recalibrating around this new frontier.

If this truly is a super cycle, it’s not just a moment—it’s a movement.

In a candid assessment that sent ripples through global markets, Federal Reserve Chair Jerome Powell has acknowledged that U.S. stock prices appear ‘fairly highly valued’ by several measures.

Speaking at a recent event in Providence, Rhode Island, Powell reportedly responded to questions about the Fed’s tolerance for elevated asset prices, noting that financial conditions—including equity valuations—are closely monitored to ensure they align with the central bank’s policy goals.

Powell’s comments, however, injected a dose of caution, suggesting that the Fed is wary of froth building in the markets.

While Powell stopped short of calling current valuations unsustainable, his phrasing echoed past warnings from central bankers about speculative excess. ‘Markets listen to us and make estimations about where they think rates are going’, he reportedly said, adding that the Fed’s policies are designed to influence broader financial conditions—not just interest rates.

The timing of Powell’s remarks is notable. The Fed recently (September 2025) cut its benchmark rate by 0.25 percentage points, a move that had bolstered investor sentiment.

Yet Powell also highlighted the ‘two-sided risks’ facing the economy: inflation remains sticky, while the labour market shows signs of softening. This balancing act, he implied, leaves little room for complacency.

Markets reacted swiftly. Tech stocks, which have led the recent rally, saw sharp declines, with Nvidia and Amazon among the hardest hit.

Powell’s warning may not signal an imminent correction, but it does suggest the Fed is keeping a watchful eye on valuations—and won’t hesitate to act if financial stability is threatened

On 17th September 2025, the U.S. Federal Reserve announced its first interest rate cut of 2025, lowering the benchmark federal funds rate by 0.25% to a range of 4.00%–4.25%.

The decision follows nine months of monetary policy stagnation and comes amid mounting evidence of a weakening labour market and persistent inflationary pressures.

Fed Chair Jerome Powell described the move as a ‘risk management cut’, citing slower job growth and a rise in unemployment as key drivers.

While inflation remains elevated—partly due to tariffs introduced by the Trump administration—the Fed opted to prioritise employment support, signalling the possibility of two further cuts before year-end.

The decision was not without controversy. New Fed Governor Stephen Miran, recently appointed by President Trump, reportedly dissented, advocating for a more aggressive half-point reduction. Political tensions have escalated, with Trump publicly urging Powell to ‘cut bigger’.

Markets responded with mixed signals: the Dow rose modestly, while the S&P 500 and Nasdaq slipped slightly. However, each improved in after-hours trading.

Analysts remain divided over the long-term impact, with some warning that easing too quickly could reignite inflation.

The Fed’s next move will be closely watched as it balances economic fragility with political crosswinds.

The next U.S. Federal Reserve meeting is scheduled for 29th–30th October 2025, with the interest rate decision expected on Wednesday, 30th October at 2:00 PM ET.

The Nasdaq Composite closed at a record high of 21,798.70 on Monday, 8th September 2025. That 0.45% gain was driven largely by a rally in chip stocks—Broadcom surged 3.2%, and Nvidia added nearly 1%.

The broader market also joined the party:

S&P 500 rose 0.21% to 6,495.15

Dow Jones Industrial Average climbed 0.25% to 45,514.95

Investor optimism is swirling around potential Federal Reserve rate cuts, especially with inflation data due later this week. The market’s momentum seems to be riding a wave of AI infrastructure spending and tech sector strength.

Negative news is not affecting the market – but why?

The Nasdaq Composite closes at a record high on Monday 8th September 2025.

Refunds could hit $1 trillion if tariffs are deemed illegal.

China’s Xpeng eyes global launch of its Mona brand.

French Prime Minister Francois Bayrou loses no-confidence vote.

UK deputy PM resigns after tax scandal.

Stocks are rising despite August’s dismal jobs report because investors are interpreting the weak labor data as a signal that interest rate cuts may be on the horizon—and that’s bullish for equities.

📉 The contradiction at the heart of the market The U.S. economy showed signs of slowing, with job numbers actually declining in June and August’s report falling short of expectations.

Normally, that would spook investors—fewer jobs mean less consumer spending, which hurts corporate earnings and stock prices.

📈 But here’s the twist Instead of panicking, markets rallied. The Nasdaq Composite hit a record high, and the S&P 500 and Dow Jones also posted gains.

Why? Because a weaker jobs market increases the likelihood that the Federal Reserve will cut interest rates to stimulate growth. Lower rates make borrowing cheaper and boost valuations—especially for tech stocks.

🤖 AI’s role in the rally Tech firms, particularly those tied to artificial intelligence like Broadcom and Nvidia, led the charge.

The suggestion is that investors may be viewing job cuts as a sign that AI is ‘working as intended’—streamlining operations and improving margins. Salesforce and Klarna, for instance, have both reportedly cited AI as a reason for major workforce reductions.

The S&P 500 closed at a fresh all-time high of 6,481.40, on 27th August 2025, marking a milestone driven largely by investor enthusiasm around artificial intelligence and anticipation of Nvidia’s earnings report.

This marks the index’s highest closing level ever, surpassing its previous record from 14th August 2025.

Here’s what powered the rally

🧠 AI Momentum: Nvidia, which now commands over 8% of the S&P 500’s weighting, has become a bellwether for AI-driven growth. Despite closing slightly down ahead of its earnings release, expectations for ‘humongous revenue gains’ kept investor sentiment buoyant.

💻 Tech Surge: Software stocks led the charge, with MongoDB soaring 38% after raising its profit forecast.

🏦 Fed Rate Cut Hopes: Comments from New York Fed President John Williams reportedly hinted at a possible rate cut in September, helping ease bond yields and boost equities.

🔋 Sector Strength: Energy stocks rose 1.15%, leading gains across 8 of the 11 S&P sectors.

S&P 500 at all-time record 27th August 2025

Even with Nvidia’s post-bell dip, the broader market seems to be pricing in sustained AI growth and a more dovish Fed stance.

Nvidia forecasts decelerating growth after a two-year AI Boom. A cautious forecast from the world’s most valuable company raises worries that the current rate of investment in AI systems might not be sustainable.

In the early 1970s, President Richard Nixon’s pursuit of re-election collided with the Federal Reserve’s independence, triggering a cascade of economic consequences that reshaped global finance.

The episode remains a cautionary tale about the dangers of politicising monetary policy.

At the heart of the drama was Nixon’s pressure on Fed Chair at the time, Arthur Burns to stimulate the economy ahead of the 1972 election. Oval Office tapes later revealed Nixon’s direct appeals for rate cuts and looser credit conditions—despite rising inflation.

Burns, reluctant but ultimately compliant, oversaw a period of aggressive monetary expansion. Interest rates were held artificially low, and the money supply surged.

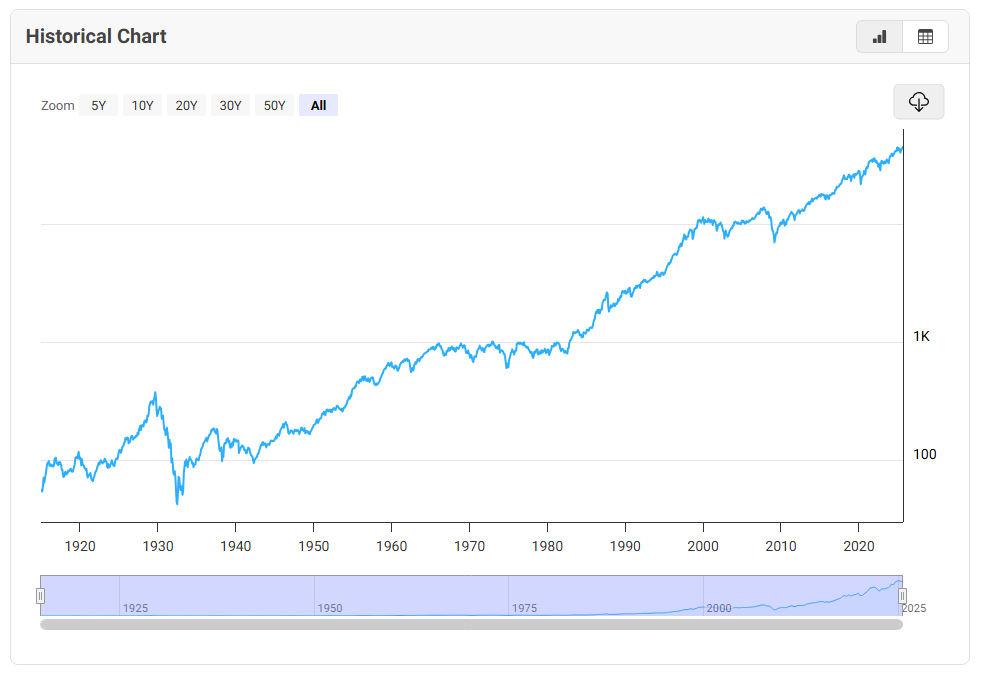

Dow historical chart – lowest 43 points to around 45,400

The short-term result was a booming economy and a landslide victory for Nixon. But the longer-term consequences were severe. Inflation, already simmering, began to boil. By 1973, consumer prices were rising at an annual rate of over 6%, and the dollar was under siege in global markets.

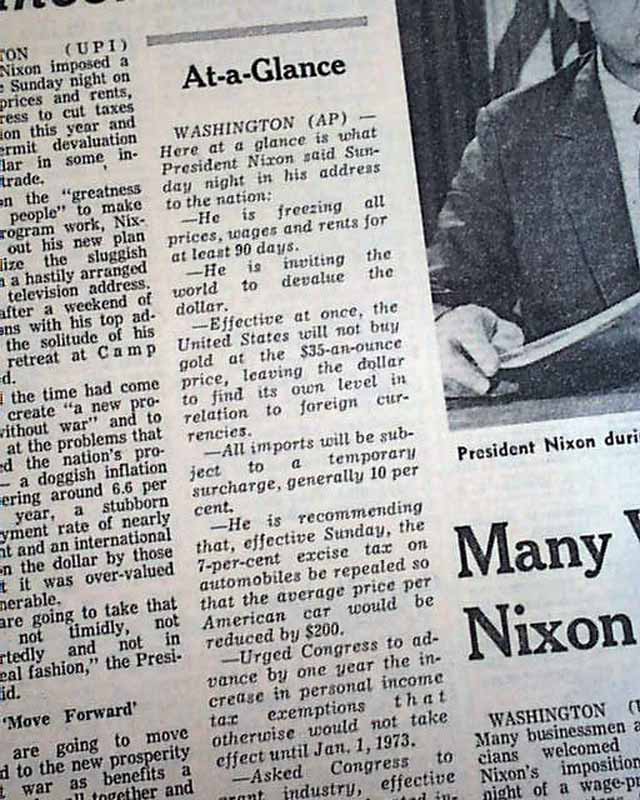

Then came the real shock: in August 1971, Nixon unilaterally suspended the dollar’s convertibility into gold, effectively ending the Bretton Woods system.

This move—intended to halt speculative attacks and preserve U.S. gold reserves—unleashed a new era of floating exchange rates and fiat currency. The dollar depreciated sharply, and global markets entered a period of volatility.

By 1974, the consequences were fully visible. The Dow Jones Industrial Average had fallen nearly 45% from its 1973 peak.

Politics vs the Federal Reserve – lesson learned?

Bond yields soared as investors demanded compensation for inflation risk. The U.S. economy entered a deep recession, compounded by the oil embargo and geopolitical tensions.

The Nixon-Burns episode is now widely viewed as a breach of central bank independence. It demonstrated how short-term political gains can lead to long-term economic instability.

The Fed’s credibility was damaged, and it took nearly a decade—culminating in Paul Volcker’s brutal rate hikes of the early 1980s—to restore price stability.

Today, as debates over Fed autonomy resurface, the lessons of the 1970s remain urgent. Markets thrive on trust, transparency, and institutional integrity. When those are compromised, even the most powerful economies can falter.

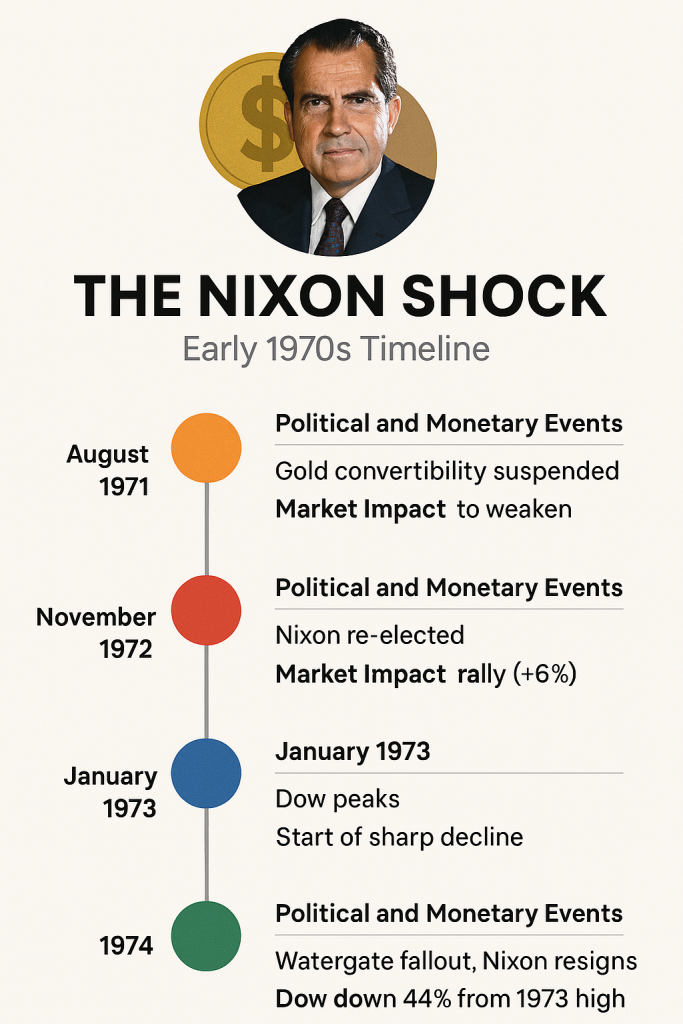

THE NIXON SHOCK — Early 1970’s Timeline

🔶 August 1971Event: Gold convertibility suspended Market Impact: Dollar begins to weaken Context: Nixon ends Bretton Woods, launching the fiat currency era

🔴 November 1972Event: Nixon re-elected Market Impact: Stocks rally briefly (+6%) Context: Fed policy remains loose under political pressure

🔵 January 1973Event: Dow peaks Market Impact: Start of sharp decline Context: Inflation accelerates, investor confidence erodes

🟢 1974Event: Watergate fallout, Nixon resigns Market Impact: Dow down 44% from 1973 high Context: Recession deepens, Fed credibility damaged.

Current dollar dive, stocks boom and bust (the Dow fell 19% in a year and then by 44% in 1975 from its January 1973 peak). U.S. 10-year Treasury yields surged (peaking at nearly 7.60% -close to twice today’s yield).

In hindsight, Nixon won the election—but lost the economy. And the Fed, caught in the crossfire, paid the price in credibility. It’s a reminder that monetary policy is no place for political theatre.

Is history repeating itself? Is Trump’s involvement different, or another catastrophe waiting to happen?

As Nvidia prepares to unveil another round of blockbuster earnings, Wall Street’s gaze remains firmly fixed on the AI darling’s ascent.

The company has become a proxy for the entire tech sector’s hopes, its valuation ballooning on the back of generative AI hype and data centre demand. Traders, analysts, and even pension funds are treating Nvidia’s quarterly results as a bellwether for market sentiment.

But while the Street pops champagne over GPU margins, a quieter and arguably more consequential drama is unfolding in Washington: The Federal Reserve’s independence is under threat.

Recent political manoeuvres—including calls to fire Fed Governor Lisa Cook and reshape the Board’s composition—have raised alarm bells among economists and institutional investors.

The Fed’s ability to set interest rates free from partisan pressure is a cornerstone of global financial stability. Undermining that autonomy could rattle bond markets, distort inflation expectations, and erode trust in the dollar itself.

Yet, the disparity in attention is striking. Nvidia’s earnings dominate headlines, while the Fed’s institutional integrity is relegated to op-eds and academic panels.

Why? In part, it’s the immediacy of Nvidia’s impact—its share price moves billions in minutes.

The Fed’s erosion, by contrast, is a slow burn, harder to quantify and easier to ignore until it’s too late.

Wall Street may be betting that the Fed will weather the political storm. But if central bank independence falters, even Nvidia’s stellar performance won’t shield markets from the fallout.

The real risk isn’t missing an earnings beat—it’s losing the referee in the game of monetary policy.

In the end, Nvidia may be the star of the show, but the Fed is the stage. And if the stage collapses, the spotlight won’t save anyone.

In a sweeping rally that spanned continents and sectors, major global indices surged to fresh record highs yesterday, buoyed by cooling inflation data,renewed hopes of U.S. central bank rate cuts, and easing trade tensions.

U.S. inflation figures released 12th August 2025 for July came in at: 2.7% – helping to lift markets to new record highs!

U.S. Consumer Price Index — July 2025

Metric

Value

Monthly CPI (seasonally adjusted)

+0.2%

Annual CPI (headline)

+2.7%

Core CPI (excl. food & energy)

+0.3% monthly, +3.1% annual

Despite concerns over Trump’s sweeping tariffs, the U.S. July 2025 CPI came in slightly below expectations (forecast was 2.8% annual).

Economists noted that while tariffs are beginning to show up in certain categories, their broader inflationary impact remains modest — for now.

Global Indices Surged to Record Highs Amid Rate Cut Optimism and Tariff Relief

Tuesday, 12 August 2025 — Taking Stock

📈 S&P 500: Breaks Above 6,400 for First Time

Closing Level: 6,427.02

Gain: +1.1%

Catalyst: Softer-than-expected U.S. CPI data (+2.7% YoY) boosted bets on a September rate cut, with 94% of traders now expecting easing.

Sector Drivers: Large-cap tech stocks led the charge, with Microsoft, Meta, and Nvidia all contributing to the rally.

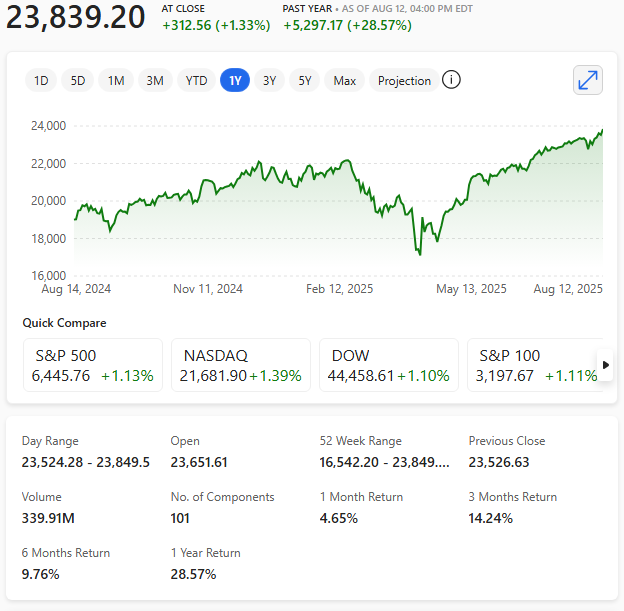

💻 Nasdaq Composite & Nasdaq 100: Tech Titans Lead the Way

Nasdaq Composite: Closed at a record 21,457.48 (+1.55%)

Nasdaq 100: Hit a new intraday high of 23,849.50, closing at 23,839.20 (+1.33%)

Highlights:

Apple surged 4.2% after announcing a $600 billion U.S. investment plan.

AI optimism continues to fuel gains across the Magnificent Seven stocks.

Nasdaq 100 chart 12th August 2025

Nasdaq 100 chart 12th August 2025

🧠 Tech 100 (US Tech Index): Momentum Builds

Latest High: 23,849.50

Weekly Gain: Nearly +3.7%

Outlook: Traders eye a breakout above 24,000, with institutional buying accelerating. Analysts note a 112% surge in net long positions since late June.

🇯🇵 Nikkei 225: Japan Joins the Record Club

Closing Level: 42,718.17 (+2.2%)

Intraday High: 43,309.62

Drivers:

Relief over U.S. tariff revisions and a 90-day pause on Chinese levies.

Strong earnings from chipmakers like Kioxia and Micron.

Speculation of expanded fiscal stimulus following Japan’s recent election results.

🧮 Market Sentiment Snapshot

Index

Record Level Reached

% Gain Yesterday

Key Driver

S&P 500

6,427.02

+1.1%

CPI data, rate cut bets

Nasdaq Comp.

21,457.48

+1.55%

AI optimism, Apple surge

Nasdaq 100

23,849.50

+1.33%

Tech earnings, institutional buying

Tech 100

23,849.50

+1.06%

Momentum, bullish sentiment

Nikkei 225

43,309.62

+2.2%

Tariff relief, chip rally

📊 Editorial Note: While the rally reflects strong investor confidence, analysts caution that several indices are approaching technical overbought levels.

The Nikkei’s RSI, for instance, has breached 75, often a precursor to short-term pullbacks.

There are increasingly credible signs that U.S. stocks may be heading into a deeper adjustment phase.

Here’s a breakdown of the key indicators and risks that suggest the current stumble could be more than a seasonal wobble. It’s just a hypothesis, but…

S&P 500 clinging to its 200-day moving average: While the long-term trend remains intact, short-term averages (5-day and 20-day) have turned negative.

Volatility Index (VIX) rising: A 7.61% surge in the 20-day average VIX suggests growing unease, even as prices remain elevated.

Diverging ADX readings: The S&P 500’s ADX (trend strength) is weak at 7.57, while the VIX’s ADX is strong at 45.37—classic signs of instability brewing.

🧠 Sentiment & Positioning: Optimism with Defensive Undercurrents

Investor sentiment is bullish (40.3%), but rising put/call ratios and a complacent Fear & Greed Index hint at hidden caution.

Historical parallels: Similar sentiment setups preceded corrections in 2021 and 2009. We’re not at extremes yet, but the complacency is notable.

🌍 Macroeconomic Risks: Tariffs, Fed Policy, and Structural Headwinds

Tariff escalation: Trump’s recent executive order raised effective tariffs to 15–20%, with new duties on rare earths and tech-critical imports.

Labour market weakening: July’s jobs report showed just 73,000 new jobs, with massive downward revisions to prior months. Unemployment ticked up to 4.2%.

Fed indecision: The central bank is split, with no clear path on rate cuts. This uncertainty is amplifying volatility.

Structural drag: Reduced immigration and R&D funding are eroding long-term growth potential.

🛡️ Strategic Implications: How Investors Are Hedging

Defensive sectors like utilities, healthcare, and gold are gaining traction.

VIX futures and Treasury bonds are being used to hedge against volatility.

Emerging markets with trade deals (e.g., Vietnam, Japan) may outperform amid global realignment.

🗓️ Seasonal Weakness: August and September Historically Slump

August is the worst month for the Dow since 1988, and the second worst for the S&P 500 and Nasdaq.

Wolfe Research reportedly notes average declines of 0.3% (August) and 0.7% (September) since 1990.

While the broader market still shows resilience—especially in mega-cap tech—the underlying signals point to fragility.

Elevated valuations, weakening macro data, and geopolitical uncertainty are converging. A deeper correction isn’t guaranteed, but the setup is increasingly asymmetric: limited upside, growing downside risk.

On 30th July 2025, the Federal Reserve opted to keep its benchmark interest rate unchanged at 4.25%–4.50%, defying mounting pressure from President Trump to initiate cuts.

The decision, reached by a 9–2 vote, marked the first time since 1993 that two governors—Michelle Bowman and Christopher Waller—formally dissented, advocating for a quarter-point reduction.

Fed Chair Jerome Powell cited “moderated” economic growth and “somewhat elevated” inflation as reasons for maintaining the current stance.

Despite a robust Q2 GDP reading of 3%, Powell emphasised the need for caution, particularly amid uncertainty surrounding Trump’s tariff policies.

Markets reacted with disappointment, as hopes for a dovish pivot were dashed. Powell remained non-committal about September’s outlook, reportedly stating, ‘We have made no decisions about September’.

With inflation still above target and political tensions rising, the Fed’s wait-and-see approach underscores its commitment to data-driven policy.

It looks like investor sentiment is shifting away from obsessing over tariffs—though not because they’ve disappeared.

Instead, there’s a growing sense that tariffs may be settling into a predictable range, especially in the U.S., where President Trump signalled a blanket rate of 15–20% for countries lacking specific trade agreements.

Here’s how that’s playing out

🌐 Why Investors Are Moving On

Predictability over Panic: With clearer expectations around tariff levels, markets may no longer treat them as wildcards.

Muted Market Reaction: The recent U.S.-EU trade deal barely nudged the S&P 500 or European indexes after moving the futures initially, signalling tariffs aren’t the hot trigger they once were.

Economists Cooling Expectations: Revisions to tariff impact estimates suggest future trade deals might not generate outsized optimism on Wall Street.

📈 Effects on the Markets

Focus Shift: Investors are turning to earnings—particularly from the ‘Magnificent Seven’ tech giants—and macroeconomic data for momentum.

Cautious Optimism: While stocks haven’t rallied hard, they’re not dropping either. Traders seem to be waiting for a new catalyst, like U.S. consumer strength or signs of a bull phase in certain indexes.

Geopolitical Undercurrents: A new deadline for Russia to reach a peace deal and threats of ‘secondary tariffs’ could still stir volatility, depending on how global partners react.

So, in short tariffs aren’t gone, but they’ve become background noise. Investors are tuning in to the next big signals.

If you’re keeping an eye on retail, tech earnings, or commodity flows, this shift could have ripple effects worth dissecting.

U.S. Federal Reserve has kept its benchmark interest rate steady at 4.25% to 4.50% for the fourth consecutive meeting.

This decision reflects a cautious stance amid ongoing uncertainty surrounding President Trump’s tariff policies and their potential impact on inflation and economic growth.

The Fed still anticipates two rate cuts later in 2025, but officials are split – some expect none or just one cut.

Inflation projections have been revised upward to 3.0% for 2025, while economic growth expectations have been trimmed to 1.4%.

U.S. President Donald Trump has been sharply critical of Federal Reserve Chair Jerome Powell, especially following the Fed’s decision on June 18, 2025, to keep interest rates steady.

He’s called Powell ‘a stupid person’, ‘destructive’, and ‘Too Late Powell’. accusing him of being politically motivated and slow to act on rate cuts.

And the Federal Reserve is supposed to act independently of political influence.

In May 2025, U.S. inflation rose by 0.1% from the previous month, bringing the annual inflation rate to 2.4%, slightly below economists’ predictions of 2.5%.

Core U.S. inflation, which excludes food and energy, increased by 0.1% month-on-month, with a year-on-year rate of 2.8%.

The modest rise was largely offset by falling energy prices, particularly a 2.6% drop in petrol, which helped keep overall inflation in check.

Prices for new and used vehicles, as well as apparel, also declined. Meanwhile, food and housing (shelter) costs each rose by 0.3%, with housing (shelter) being the primary contributor to the monthly increase.

Despite President Trump’s sweeping tariffs introduced in April 2025, their inflationary impact has yet to fully materialise. Analysts suggest that many companies are still working through pre-tariff inventories, delaying price hikes for consumers.

However, economists caution that the effects may become more pronounced in the coming months.

The Federal Reserve is expected to hold interest rates steady for now, as U.S. policymakers monitor whether inflation remains contained or begins to accelerate due to trade-related pressures.

Markets responded positively to the data, with stock futures rising and Treasury yields falling.

So, while inflation remains above the Fed’s 2% target, May’s figures suggest a temporary reprieve.

The Federal Reserve held its key interest rate steady at 4.25% – 4.50% on 7th May 2025, citing economic uncertainty and the potential impact of tariffs.

Fed Chair Jerome Powell emphasised that the central bank is in wait-and-see mode, monitoring inflation and employment risks.

The decision follows concerns that Trump’s trade policies could lead to stagflation, with rising prices and slowing growth.

While markets reacted positively, analysts remain divided on whether the Fed will cut rates later this year.

Powell stated that future adjustments will depend on evolving economic conditions and the balance of risks.

Trump’s take on this decision was reportedly to call Powell… a fool.

What is stagflation?

Stagflation is an economic condition where high inflation, stagnant economic growth, and high unemployment occur simultaneously.

It presents a challenge for policymakers because measures to reduce inflation can worsen unemployment, while efforts to boost growth may fuel inflation further.

The U.S. economy is showing cracks as multiple indicators suggest that growth may be slowing.

With GDP shrinking by 0.3% in the first quarter of 2025, concerns about an impending recession have intensified among analysts and investors.

A key driver of this economic downturn is the ongoing trade uncertainty, which has prompted businesses to stock up on imports before new tariffs take effect.

While some experts argue this is a temporary setback, others caution that prolonged trade conflicts could stifle growth for months to come.

Resilient labour market

Despite these concerns, the labour market has remained resilient, with unemployment hovering at 4.2%. However, signs of strain are emerging – job openings have declined, and layoffs have picked up in certain industries.

If hiring slows further, consumer spending could weaken, adding pressure to the economy.

Inflation remains another point of concern. Rising costs of goods and services have strained household budgets, leading to reduced discretionary spending.

The Federal Reserve, which has maintained high interest rates, is carefully assessing whether policy adjustments are needed to prevent a sharper downturn.

On Wall Street, sentiment is divided. Goldman Sachs estimates a 45% probability of a recession, while J P Morgan suggests the likelihood could be as high as 60%.

Some economists believe strategic trade deals and government intervention could avert a full-blown recession, but the margin for error is slim.

Does it really matter if there is to be a recession – it will likely be short lived. It will not please the U.S. President Donald Trump.

While uncertainty clouds the future, one thing is clear – the U.S. economy is at a pivotal moment. Whether policymakers can stabilise growth or if the nation is headed towards a deeper slowdown will depend on the next few quarters and the outcome of Trump’s tariffs.

Tudor Investment Corporation

Paul Tudor Jones, the founder of Tudor Investment Corporation, recently shared his outlook on the U.S. economy, and his perspective isn’t exactly optimistic.

He believes that U.S. stocks are likely to hit new lows before the end of the year, even if President Trump dials back tariffs on Chinese imports.

Jones pointed out that the combination of high tariffs and the Federal Reserve’s reluctance to cut interest rates is putting significant pressure on the stock market.

He reportedly noted that even if Trump reduced tariffs to 50% or 40%, it would still amount to one of the largest tax increases since the 1960s, potentially slowing economic growth.

The billionaire investor also warned that unless the Fed adopts a more dovish stance and aggressively cuts rates, the market is likely to continue its downward trajectory.

He reportedly emphasised that the current economic conditions – marked by trade uncertainty and tight monetary policy – are not favourable for a stock market recovery.

Interestingly, Jones also expressed concerns about artificial intelligence, stating that AI poses an imminent threat to humanity within our lifetime.