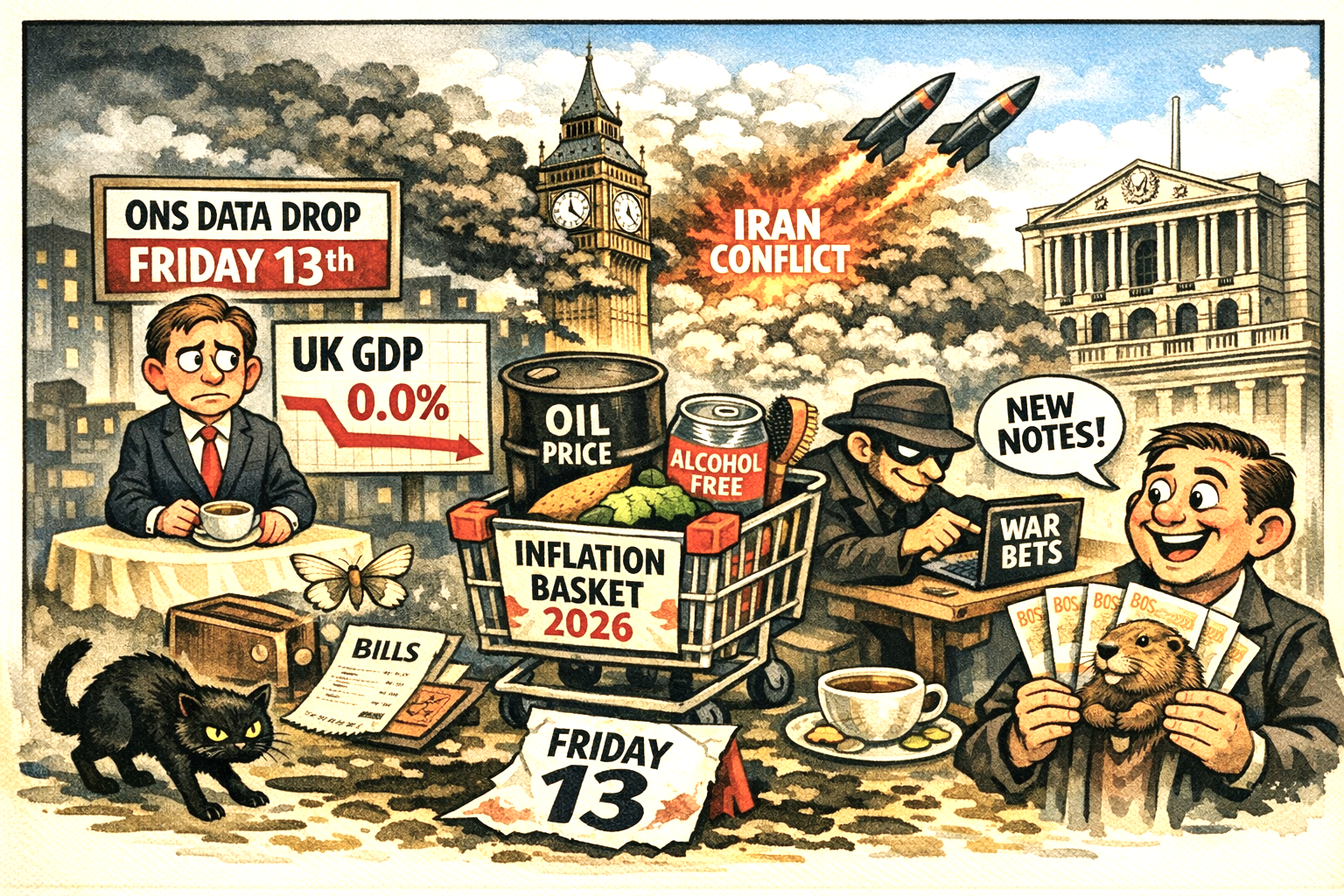

The latest batch of UK data landed on Friday 13th 2026 and painted a picture of an economy still struggling to regain momentum. January 2026 GDP came in flat, with the ONS reporting 0.0% growth for the month.

After slipping into a shallow recession at the end of last year, the economy has yet to show convincing signs of recovery.

The stagnation was driven in part by weaker discretionary spending, particularly on eating out, as households continued to rein in non‑essential purchases.

Oil price volatility

While not a formal data release, global energy volatility remains a defining backdrop. Oil markets swung sharply as tensions surrounding the Iran conflict intensified, feeding directly into UK inflation expectations.

Higher wholesale energy prices continue to complicate the Bank of England’s path toward easing, and markets remain sensitive to any sign that geopolitical risk may spill over into domestic costs.

The ONS also confirmed its annual update to the inflation basket, a technical change that nonetheless shapes how price pressures are measured.

New additions such as alcohol‑free beer and pet grooming services reflect shifting consumer behaviour, while other items have been removed or reweighted.

These adjustments won’t move the headline rate dramatically, but they do offer a useful snapshot of how UK households are spending in 2026.

Prediction markets challenged and new UK bank note design

Beyond the data, regulatory and policy stories added texture to the week. A debate over prediction market oversight intensified after reports of increasingly “gruesome” war‑related bets, raising questions about the boundaries of financial speculation.

Meanwhile, the ongoing redesign of UK banknotes continued to attract public interest, underscoring the symbolic weight of currency at a time of economic uncertainty.

Taken together, Friday 13th’s updates reinforce a familiar theme: the UK economy is edging forward, but with little momentum and plenty of external headwinds.