Beginning in 2030, Mastercard will eliminate the need for Europeans to manually enter their card numbers during online checkout, regardless of the platform or device used.

The familiar 16-digit card number will be substituted with a randomly generated ‘token.’ This change will enable consumers to complete payments with a single click at the checkout page, authenticated by a thumbprint.

Mastercard reported that 100% tokenization across e-commerce sites will reduce fraud rates dramatically.

The way we pay for products and services online will feel very different in the coming years.

U.S. citizens have accumulated a record-breaking $1 trillion in credit card debt.

The Federal Reserve’s interest rate hikes through 2023 have caused average interest rates for credit cards to spike to more than 22%. Rates on retail credit cards are even higher, nearing 29% on average.

Despite rising costs and higher borrowing rates, a record number of consumers shopped over the Thanksgiving holiday weekend. The National Retail Federation found that more than 200 million consumers went shopping that weekend, more than the 196.7 million shoppers who turned out in 2022.

Retailers Macy’s and other larger retailers have issued warnings about a slowdown in repayments on their credit cards, highlighting a potential risk to retail revenue this holiday season.

The resilience of the American consumer will continue to be tested by the still-rising costs of groceries, fuel, energy and housing.

Interesting fact

The U.S. credit card debt is approximately equal to the size of Apple’s market cap of $1 trillion.

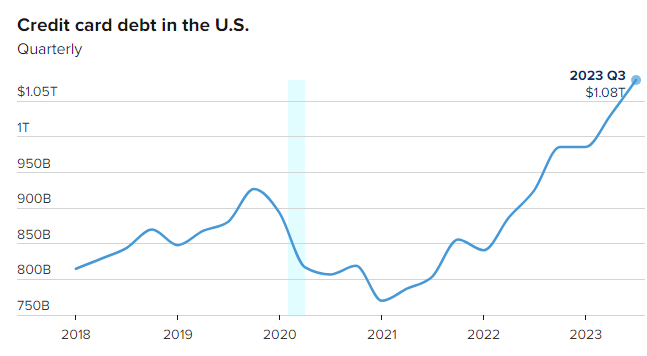

U.S. citizens now owe $1.08 trillion on their credit cards, according to a new report on household debtfrom the Federal Reserve Bank of New York.

U.S. Household Debt Rises to $17.29 Trillion Led by Mortgage, Credit Card, and Student Loan Balances

Total household debt rose by 1.3% to reach $17.29 trillion in the third quarter of 2023, according to the latest Quarterly Report on Household Debt and Credit.

Mortgage balances increased to $12.14 trillion, credit card balances to $1.08 trillion, and student loan balances to $1.6 trillion.

Auto loan balances increased to $1.6 trillion, continuing the upward trajectory seen since 2011. Other balances, which include retail credit cards and other consumer loans, were effectively flat at $0.53 trillion. Delinquency transition rates increased for most debt types, except for student loans.

Credit card losses in the U.S. are rising at the fastest pace since the Great Financial Crisis of 2008.

Goldman Sachs reportedly predicts that credit card losses will continue to climb through the end of 2024 or early 2025 for most issuers. This is unusual because the losses are accelerating outside of an economic downturn.

Unusual trend

The main factors behind this trend are higher interest rates from the Federal Reserve and a surge in spending since the pandemic.

U.S. citizens owe more than $1 trillion on credit cards, a record high, according to the Federal Reserve Bank of New York. Credit card defaults, which occur when a borrower fails to repay debt and the lender writes it off, are also projected to increase by 20% year-over-year in 2023.

This could have negative implications for the economy and consumers’ financial well-being.

Americans are using their credit cards more than ever, pushing the total balance to over $1 trillion for the first time in history, according to a report from the New York Federal Reserve.

The report, released August 2023, showed that credit card balances rose by $45 billion to $1.03 trillion in the second quarter of 2023, reflecting robust consumer spending as well as higher prices due to inflation. The increase was the largest quarterly gain since 2008 and surpassed the previous record of $1.02 trillion set in 2019.

The rise in credit card debt also coincided with a higher payment failure rate, which measures the share of borrowers who are at least 30 days behind on their payments. The failure measure climbed to 7.2% in the second quarter, up from 6.5% in the first quarter and the highest level since 2012.

The New York Fed reportedly said that the increase in failure rates may reflect a normalization to pre-pandemic levels, as many lenders offered relief programs and forbearance options to borrowers during the Covid-19 crisis. However, some analysts warned that the high level of credit card debt could pose a risk to the financial stability of households and the economy if interest rates rise or incomes fall.

Expensive debt

Credit card debt is one of the most expensive forms of debt, and it can quickly spiral out of control if not managed. ‘Consumers should aim to pay off their balances in full every month, or at least pay more than the minimum due, to avoid paying unnecessary interest and fees.

The burden of debt is all to consuming!

Interest rates and fees on credit cards are one of the highest payable and if you fall into the debt spiral it can be almost impossible to liberate yourself from that consuming debt.

Younger users

The New York Fed also noted that credit card usage has become more widespread among Americans, especially among younger and lower-income borrowers. The share of adults with at least one credit card increased from 76% in 2019 to 79% in 2021, while the share of those with four or more cards rose from 18% to 21% over the same period.

Tool

The report suggested that credit cards have become an essential tool for many consumers to access credit and smooth purchases over time, especially during periods of economic uncertainty and volatility. However, it also cautioned that credit cards can also lead to overborrowing and financial distress if not used responsibly.

It is one of the most expensive ways to borrow money and far too easy to access.