After months of gradual easing, the pause reflects a delicate moment for the UK economy, with price pressures beginning to shift beneath the surface.

Clothing was the biggest upward driver, with prices rising this year after falling during the same period in 2025.

This was offset by cheaper petrol, though those figures were captured before the recent surge in global oil prices triggered by the outbreak of war involving Iran.

While inflation is far below the peaks seen a few years ago, households are still contending with the reality that prices continue to rise—just more slowly.

ONS data

The ONS also introduced supermarket scanner data for the first time, offering a more accurate picture of food costs.

Economists warn that the conflict‑driven spike in oil and gas prices could push inflation higher again later in the year, with some forecasts suggesting a potential rise towards 4.6%.

Businesses already reliant on fuel, such as regional bus operators, report steep cost increases that may soon feed through to consumers.

The government insists it is working to ease cost‑of‑living pressures, though global events may limit its room for manoeuvre.

U.S. core wholesale prices rose 0.8% in January 2026, a sharper-than-expected acceleration that has renewed concerns about lingering inflationary pressures across the American economy.

The increase, reported by the Bureau of Labor Statistics, exceeded both December 2025’s 0.6% rise and the consensus expectation of 0.3%, marking one of the strongest monthly gains in recent months.

The core U.S. Producer Price Index (PPI), which strips out volatile food and energy components, is closely watched as an indicator of underlying cost pressures faced by businesses.

January’s jump suggests that inflationary forces remain embedded in key service sectors, even as goods prices continue to soften.

Indeed, services were the primary driver of the month’s overall wholesale inflation, with final demand services advancing 0.8%, while goods prices fell by 0.3% amid notable declines in gasoline and several food categories.

Divergence

This divergence between services and goods highlights a structural shift in inflation dynamics. Goods inflation has eased significantly as supply chains normalise and commodity prices stabilise.

By contrast, service-sector inflation—often tied to labour costs, logistics, and profit margins—has proven more persistent.

January 2026’s data underscores this trend, with strong increases in areas such as professional and commercial equipment wholesaling, telecommunications access services, and health and beauty retailing.

Complicates Inflation Outlook

For policymakers, the report complicates the inflation outlook. While headline PPI rose a more modest 0.5%, the strength of the core measure suggests that underlying pressures may not be cooling as quickly as hoped.

Markets had been anticipating a gradual easing that would give the Federal Reserve more confidence to consider rate cuts later in the year.

Instead, the January 2026 figures may reinforce a more cautious stance, particularly if upcoming consumer inflation data echoes the same pattern.

Businesses and consumers alike will be watching February 2026’s data closely to determine whether January represents a temporary spike or the beginning of a more stubborn inflation trend.

The United States economy lost momentum at the end of 2025, with fourth‑quarter GDP rising just 1.4%, a sharp deceleration from the 4.4% expansion recorded in the previous quarter.

The first estimate from the U.S. Bureau of Economic Analysis underscored a cooling backdrop that contrasts with the resilience seen through much of last year.

The slowdown was broad‑based. Government spending, which had previously provided a meaningful lift, swung lower.

Exports weakened

Exports also weakened, reflecting softer global demand and a less favourable trade environment.

Consumer spending — the backbone of the U.S. economy — continued to grow but at a more subdued pace, suggesting households are becoming more cautious as borrowing costs remain elevated. Although there has been some easing in U.S. mortgage rates.

Imports declined, which mechanically supports GDP, but the underlying signal points to softer domestic demand.

Analysts had expected a stronger finish to the year, with forecasts clustered closer to 2.5%.

The miss raises questions about the durability of U.S. growth heading into 2026, particularly as fiscal support fades and the effects of tighter monetary policy continue to filter through.

Q3 surge to Q4 slowdown

The contrast with the previous quarter is stark: Q3’s surge was driven by robust consumer activity, firmer government outlays, and a rebound in exports — dynamics that have since reversed.

Even so, the latest figures do not point to an imminent recession. Investment remains mixed rather than collapsing, and consumer spending is still contributing positively.

But the data does reportedly suggest the economy is entering a more fragile phase, where small shocks could have outsized effects.

For policymakers, the report complicates the Federal Reserve’s path. Inflation has eased but remains above target, and a softer growth profile may strengthen the case for rate cuts later in the year — though officials will want clearer evidence before shifting course.

Japan’s inflation rate has dipped below the Bank of Japan’s long‑standing 2% target for the first time in almost four years, marking a notable turning point in the country’s post‑pandemic price cycle.

Official figures show headline inflation easing to 1.5% in January, ending a 45‑month stretch above the central bank’s benchmark.

Slowdown

The slowdown reflects a broad cooling in cost pressures that had dominated the Japanese economy since 2022. Food inflation has eased to a 15‑month low, while transport, healthcare, and household goods have all seen slower price growth.

Energy costs remain negative, helped by government subsidies that continue to cushion households from global fuel volatility.

Core inflation — which strips out volatile fresh food prices — has also softened, slipping to 2.0%, its weakest pace in two years.

Analysts attribute much of the deceleration to base effects following last year’s sharp price increases, suggesting that underlying demand‑driven inflation remains relatively stable.

For the Bank of Japan, the latest figures present a delicate policy challenge. While inflation is finally within the target range, underlying price pressures have not disappeared entirely.

Rate increases?

Some economists argue the BOJ may still lean toward gradual rate increases, particularly as wage negotiations progress and the government pushes for sustained real income growth.

Others caution that tightening too soon could risk undermining Japan’s still‑fragile consumption recovery.

What is clear is that Japan has entered a new phase of its inflation story — one defined less by imported cost shocks and more by the question of whether domestic demand can carry the momentum forward.

The UK’s inflation rate has dropped to 3%, its lowest level since March last year, renewing expectations that the Bank of England (BoE) may soon begin cutting interest rates.

The fall, recorded in January, marks a clear reversal from December’s unexpected uptick to 3.4% and reinforces the broader downward trend seen in late 2025.

Economists note that easing petrol, food, and airfare prices have been key contributors to the decline, helping inflation move closer to the government’s 2% target.

Bank of England easier decision

The BoE has held Bank Rate at 3.75% in recent meetings, emphasising the need for confidence that inflation will not only reach 2% but remain there sustainably.

However, with inflation now falling faster than previously forecast, policymakers appear to have greater room to consider loosening monetary policy later this spring.

The Bank itself has acknowledged that inflation is likely to return to target ‘a bit quicker than previously forecast’, suggesting scope for cuts if economic conditions evolve as expected.

Rate reduction likely in March or April 2026

Market analysts increasingly anticipate a rate reduction as early as March or April, particularly as wage growth cools and unemployment edges higher—factors that reduce domestic inflationary pressure.

For households and businesses, a cut would offer welcome relief after two years of elevated borrowing costs, potentially lowering mortgage rates and improving credit conditions.

While the BoE remains cautious, the latest inflation figures strengthen the case for a shift towards easing—signalling that the long, difficult climb down from the inflation peak may finally be nearing its conclusion.

As expected

Most economists and market analysts expected UK inflation to fall back to around 3% in the January release, down from 3.4% in December 2025.

UK inflation falls to 3%

This means the actual figure—3%—came in exactly in line with forecasts, rather than surprising to the downside or upside.

That alignment matters for the Bank of England because it reinforces the sense that inflation is easing broadly as expected, rather than stalling or re‑accelerating.

Employment data

Alongside falling inflation, the Bank of England is closely watching UK labour market data, which remains a key factor in its interest rate decisions.

Recent figures show wage growth is easing, with average earnings excluding bonuses rising at a slower pace—now below 6%—while job vacancies continue to decline.

This softening suggests that domestic inflationary pressure from pay settlements may be waning, giving the Bank more confidence that inflation can return to target sustainably.

However, unemployment remains low, and services inflation is still sticky, meaning policymakers are likely to weigh jobs data carefully before committing to rate cuts.

If wage growth continues to moderate and employment weakens further, the case for easing monetary policy will strengthen.

This marks the second consecutive cut in 2025 amid economic uncertainty and a government data blackout.

In a move aimed at supporting growth, the Federal Reserve reduced its benchmark interest rate by 0.25% following its October policy meeting.

The decision, reportedly backed by a 10–2 vote from the Federal Open Market Committee, reflects growing concern over a weakening labour market and subdued consumer confidence.

Chair Jerome Powell acknowledged the challenges posed by the ongoing U.S. government shutdown, which has delayed key economic reports.

With official data frozen, the Fed relied on private indicators showing a slowdown in hiring and modest inflation. The Consumer Price Index rose just 3% year-on-year, below the Fed’s long-term target.

While the rate cut aims to ease borrowing costs and stimulate investment, Powell cautioned against assuming further reductions in December.

He emphasised that future decisions would depend on incoming data and evolving risks. It is not a done deal.

The Fed also announced plans to end quantitative tightening (QT) by 1st December 2025, signalling a broader shift towards monetary easing.

Markets responded cautiously, with investors weighing the implications for growth, inflation, and the Fed’s credibility.

Markets, after a short rally during the week, were subdued after the announcement.

The latest U.S. inflation figures show a modest increase in consumer prices. The annual rate rose to 3.0% in September 2025, up from 2.9% in August. 2025.

Core inflation—which excludes volatile food and energy prices—also rose by 0.2% in September. This brought the year-on-year rate to 3.0%, again undercutting forecasts of 3.1%.

A notable contributor to the headline figure was a 4.1% surge in petrol prices. This offset declines in other areas such as used vehicles and household furnishings.

Federal Reserve

The data arrives just ahead of the Federal Reserve’s next policy meeting, where a 0.5% rate cut is widely anticipated. Softer inflation readings have buoyed market sentiment, with futures posting gains on hopes of looser monetary policy.

Despite a partial government shutdown, the inflation report was released on schedule, underscoring its significance for financial markets and policymakers.

With inflation now hovering near the Fed’s target, attention turns to wage growth and consumer spending as key indicators of future price stability.

The next CPI update is due mid-November.

This CPI news added to the possibility of a Fed rate cut in conjunction to the possibility of a U.S. China ‘tariff trade’ deal and relaxation of Rare Earth material sales pushed markets to new all-time highs!

The Resilient Stock Market: A Double-Edged Shield Against Recession

In a year marked by political volatility, Trumps tariff war, soft labour data, and persistent inflation anxieties, one pillar of the economy has stood tall: the stock market.

Defying expectations, major indices like the Nasdaq, Dow Jones and S&P 500 have surged, buoyed by AI-driven optimism and industrial strength. This resilience has helped stave off a technical recession—but not without raising deeper concerns about economic fragility and inequality.

At the heart of this phenomenon lies the ‘wealth effect’. As equity portfolios swell, high-net-worth households feel richer and spend more freely.

This consumer activity props up GDP figures and masks underlying weaknesses in wage growth, job creation, and productivity.

August’s economic data showed surprising strength in consumer spending and housing, despite lacklustre employment figures and fading stimulus support.

But here’s the rub: this buoyancy is not broadly shared. According to the University of Michigan’s sentiment index, confidence has declined sharply since January, especially among those without significant stock holdings.

Balance

The U.S. economy, in effect, is being held aloft by a narrow slice of the population—those with the means to benefit from rising asset prices. For everyone else, the recovery feels distant, even illusory.

This divergence creates a dangerous illusion of stability. Policymakers may hesitate to intervene—whether through fiscal support or monetary easing—because headline indicators look healthy. Yet beneath the surface, vulnerabilities abound.

If the market were to correct sharply, the spending it fuels could evaporate overnight, exposing the economy’s dependence on asset inflation.

Moreover, the market’s resilience may be distorting capital allocation. Companies flush with investor cash are prioritising stock buybacks and speculative ventures over wage growth or long-term investment. This can exacerbate inequality and erode the foundations of sustainable growth.

In short, while the stock market’s strength has delayed a recession, it has also deepened the disconnect between Wall Street and Main Street.

The danger lies not in the market’s success, but in mistaking it for economic health. A resilient market may be a shield—but it’s not a cure. And if that shield cracks, the consequences could be swift and severe.

The challenge now is to look beyond the indices and ask harder questions: Who is benefitting? What are we neglecting?

And how do we build an economy that’s resilient not just in numbers, but in substance, regardless of nation.

In a candid assessment that sent ripples through global markets, Federal Reserve Chair Jerome Powell has acknowledged that U.S. stock prices appear ‘fairly highly valued’ by several measures.

Speaking at a recent event in Providence, Rhode Island, Powell reportedly responded to questions about the Fed’s tolerance for elevated asset prices, noting that financial conditions—including equity valuations—are closely monitored to ensure they align with the central bank’s policy goals.

Powell’s comments, however, injected a dose of caution, suggesting that the Fed is wary of froth building in the markets.

While Powell stopped short of calling current valuations unsustainable, his phrasing echoed past warnings from central bankers about speculative excess. ‘Markets listen to us and make estimations about where they think rates are going’, he reportedly said, adding that the Fed’s policies are designed to influence broader financial conditions—not just interest rates.

The timing of Powell’s remarks is notable. The Fed recently (September 2025) cut its benchmark rate by 0.25 percentage points, a move that had bolstered investor sentiment.

Yet Powell also highlighted the ‘two-sided risks’ facing the economy: inflation remains sticky, while the labour market shows signs of softening. This balancing act, he implied, leaves little room for complacency.

Markets reacted swiftly. Tech stocks, which have led the recent rally, saw sharp declines, with Nvidia and Amazon among the hardest hit.

Powell’s warning may not signal an imminent correction, but it does suggest the Fed is keeping a watchful eye on valuations—and won’t hesitate to act if financial stability is threatened

On 18th September, the Bank of England voted 7–2 to keep interest rates steady at 4%, resisting calls for further easing amid persistent inflationary pressures.

The decision follows August’s 25 basis point cut and reflects caution over elevated wage growth and stagnant UK GDP.

Inflation held at 3.8% in August, nearly double the Bank’s 2% target. Policymakers signalled a ‘gradual and careful’ approach to future cuts, citing upside risks to medium-term inflation.

With economic growth flat and the jobs market cooling, analysts now expect the next rate cut to come in early 2026.

On 17th September 2025, the U.S. Federal Reserve announced its first interest rate cut of 2025, lowering the benchmark federal funds rate by 0.25% to a range of 4.00%–4.25%.

The decision follows nine months of monetary policy stagnation and comes amid mounting evidence of a weakening labour market and persistent inflationary pressures.

Fed Chair Jerome Powell described the move as a ‘risk management cut’, citing slower job growth and a rise in unemployment as key drivers.

While inflation remains elevated—partly due to tariffs introduced by the Trump administration—the Fed opted to prioritise employment support, signalling the possibility of two further cuts before year-end.

The decision was not without controversy. New Fed Governor Stephen Miran, recently appointed by President Trump, reportedly dissented, advocating for a more aggressive half-point reduction. Political tensions have escalated, with Trump publicly urging Powell to ‘cut bigger’.

Markets responded with mixed signals: the Dow rose modestly, while the S&P 500 and Nasdaq slipped slightly. However, each improved in after-hours trading.

Analysts remain divided over the long-term impact, with some warning that easing too quickly could reignite inflation.

The Fed’s next move will be closely watched as it balances economic fragility with political crosswinds.

The next U.S. Federal Reserve meeting is scheduled for 29th–30th October 2025, with the interest rate decision expected on Wednesday, 30th October at 2:00 PM ET.

The latest figures from the Office for National Statistics (ONS) reveal that UK inflation remained unchanged at 3.8% in August 2025, matching July’s rate and defying expectations of a slight dip.

While this steadiness may offer a glimmer of stability, the underlying story is more complex—and more costly—for British households.

📈 Headline vs. Reality

The Consumer Prices Index (CPI) staying at 3.8% means inflation is still nearly double the Bank of England’s 2% target.

Core inflation, which strips out volatile items like energy and food, eased slightly to 3.6%, down from 3.8% in July.

However, food and drink inflation surged to 5.1%, marking the fifth consecutive monthly rise and the highest level since January 2023.

🥦 What’s Driving the Cost Surge?

The price hikes are most pronounced in everyday essentials

Vegetables, milk, eggs, cheese, and fish saw notable increases.

Rising employment costs, poor harvests, and new packaging taxes have added pressure on retailers, who are passing these costs onto consumers.

🏦 Monetary Policy in the Balance

The Bank of England, which recently cut interest rates from 4.25% to 4%, is treading carefully. With inflation expected to peak at 4% in September before easing in early 2026, policymakers are hesitant to introduce further rate cuts this year.

Economists suggest that unless inflation shows clearer signs of retreat, the central bank may hold off on additional monetary easing until February 2026.

💬 Political and Retail Response

Chancellor Rachel Reeves reportedly acknowledged the strain on families, pledging to ‘bring costs down and support people who are facing higher bills’.

Meanwhile, industry leaders are calling for relief in the upcoming Autumn Budget, urging the government to cut business rates and ease regulatory burdens.

Retailers like Tesco and Sainsbury’s are seeing mixed fortunes. Tesco gained market share and posted its strongest growth since December 2023, while Asda lagged behind with declining sales.

🧾 What It Means for You

For mortgage holders, renters, and shoppers, the unchanged headline rate offers little comfort. With food inflation outpacing wage growth, many households are feeling the pinch.

The Autumn Budget may bring targeted support, but for now, the weekly shop continues to swallow a larger chunk of UK income.

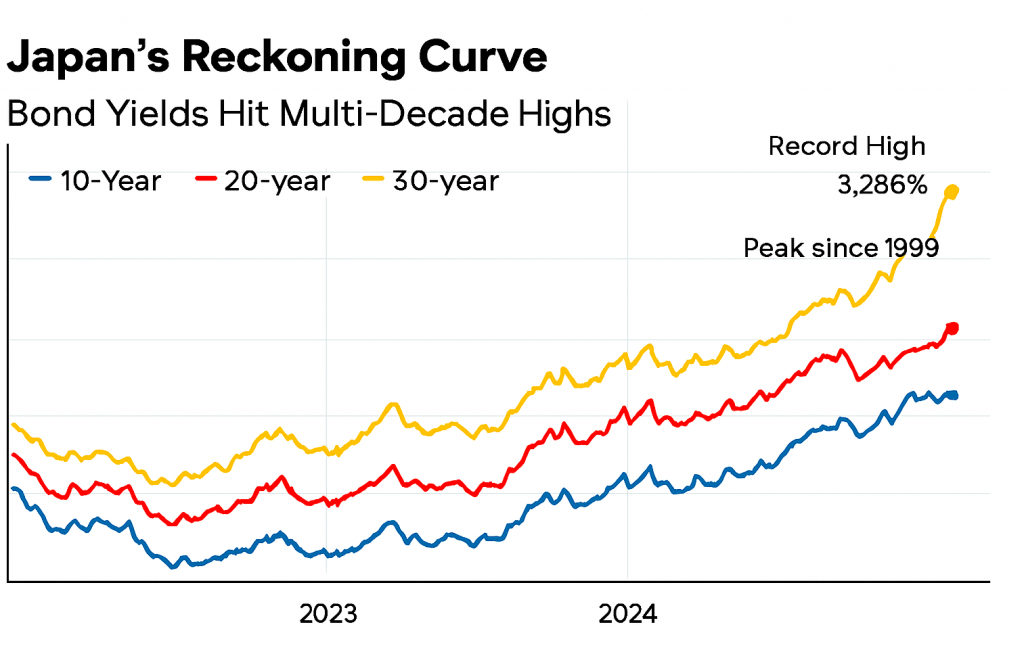

After decades of economic sedation, Japan’s long-term bond yields are rising with a vengeance.

The 30-year government bond has breached 3.286%—its highest level on record—while the 20-year yield has climbed to 2.695%, a peak not seen since 1999.

These aren’t just numbers; they’re seismic signals of a nation confronting its delayed past, now its deferred future.

Indicative Yield Curve for Japan

For years, Japan’s yield curve was a monument to inertia. Negative interest rates, yield curve control, and relentless bond-buying by the Bank of Japan created an artificial calm—a kind of economic Zen garden, raked smooth but eerily still.

That era is ending. Inflation has persisted above target for three years, and the BOJ’s retreat from monetary intervention has unleashed market forces long held at bay.

This steepening curve is more than financial recalibration—it’s a symbolic reckoning. Rising yields demand accountability: from policymakers who masked structural fragility, from investors who chased safety in stagnation, and from a society that postponed hard choices on demographics, debt, and productivity.

The bond market, once a passive witness, now acts as judge. Each basis point is a moral verdict on Japan’s economic past.

The shadows of the Lost Decades—deflation, aging populations, and overspending—are being dispelled not by command, but through the process of price discovery.

In this new era, Japan’s yield curve resembles a serpent uncoiling—no longer dormant but rising with intent.

The question isn’t whether the curve will flatten again, but whether Japan can meet the moment it has long delayed.

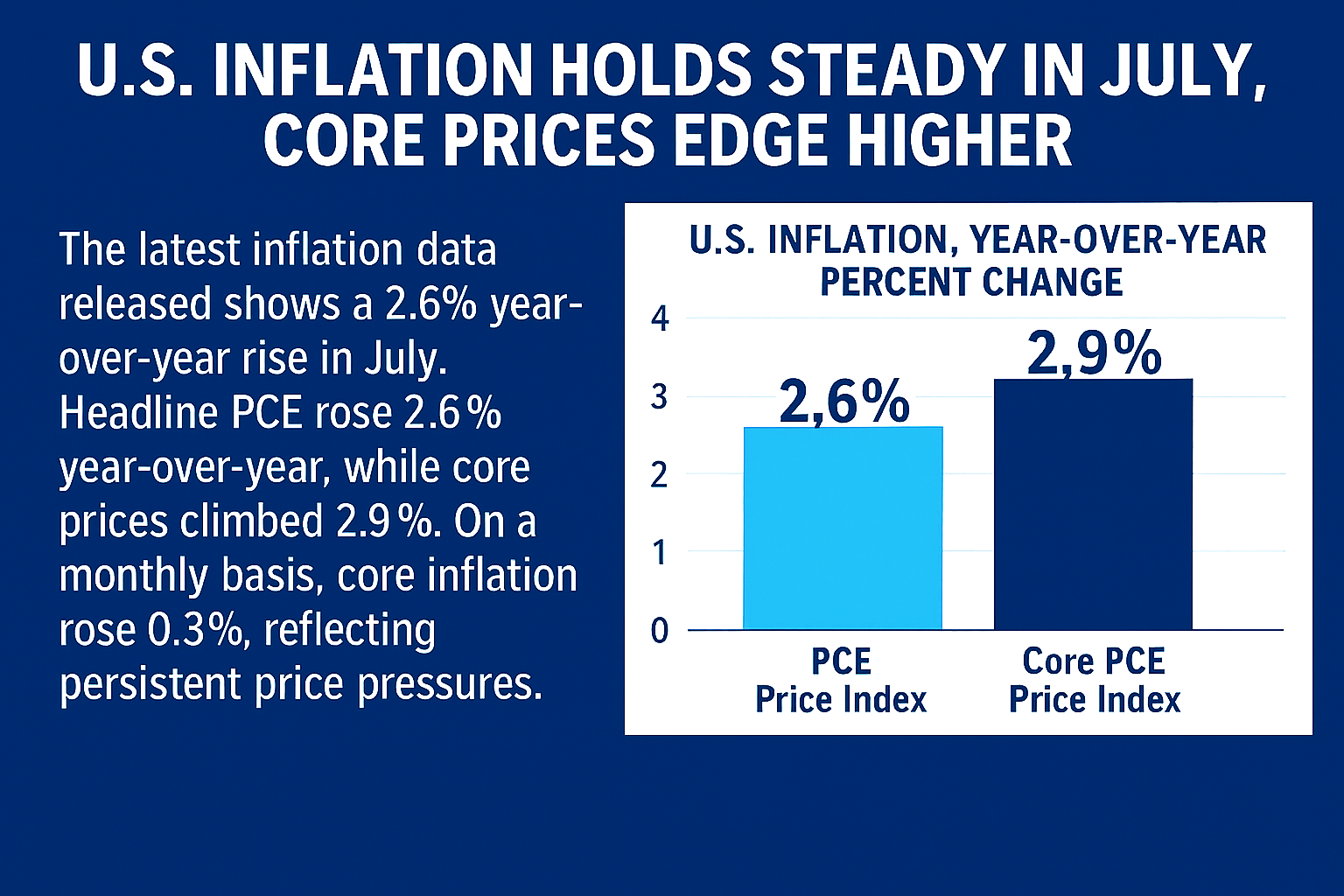

The latest inflation data for the month of July 2025 shows a mixed picture for the U.S. economy, as price pressures remain persistent despite signs of cooling in some sectors.

On a monthly basis, core prices increased 0.3%, in line with expectations, while consumer spending rose 0.5%, suggesting households are still resilient despite elevated costs. Personal income also climbed 0.4%, reinforcing the narrative of steady wage growth.

The Federal Reserve, which uses the PCE index as its preferred inflation gauge, faces a delicate balancing act.

With inflation still above its 2% target and labor market data showing signs of softening, markets are increasingly betting on a rate cut at the Fed’s September meeting.

Fed Chair Jerome Powell, speaking at Jackson Hole, reportedly acknowledged the risks to employment but maintained a cautious tone on policy shifts.

Investors and traders alike now see an 80% chance of a quarter-point cut, keeping all eyes on upcoming jobs data.

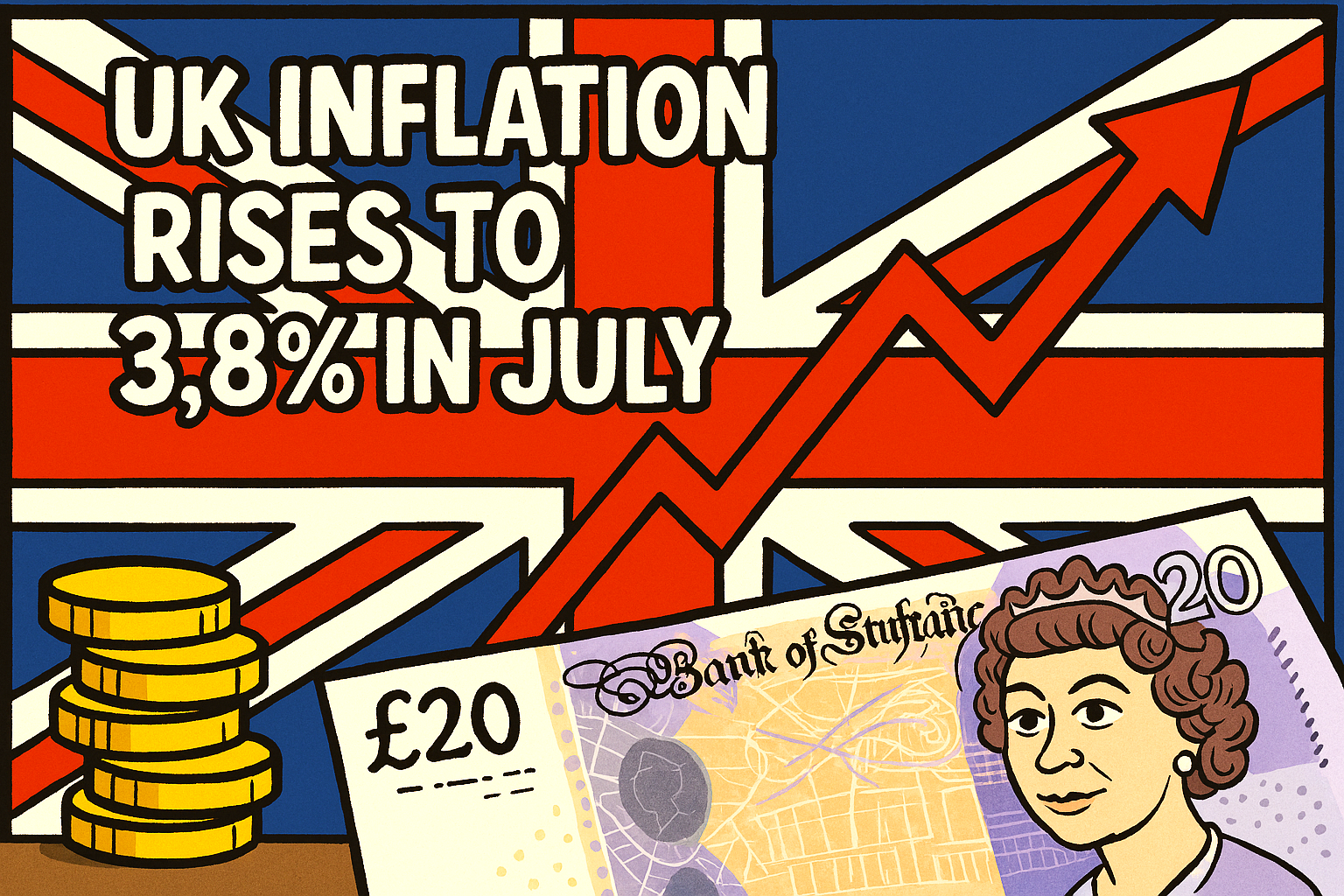

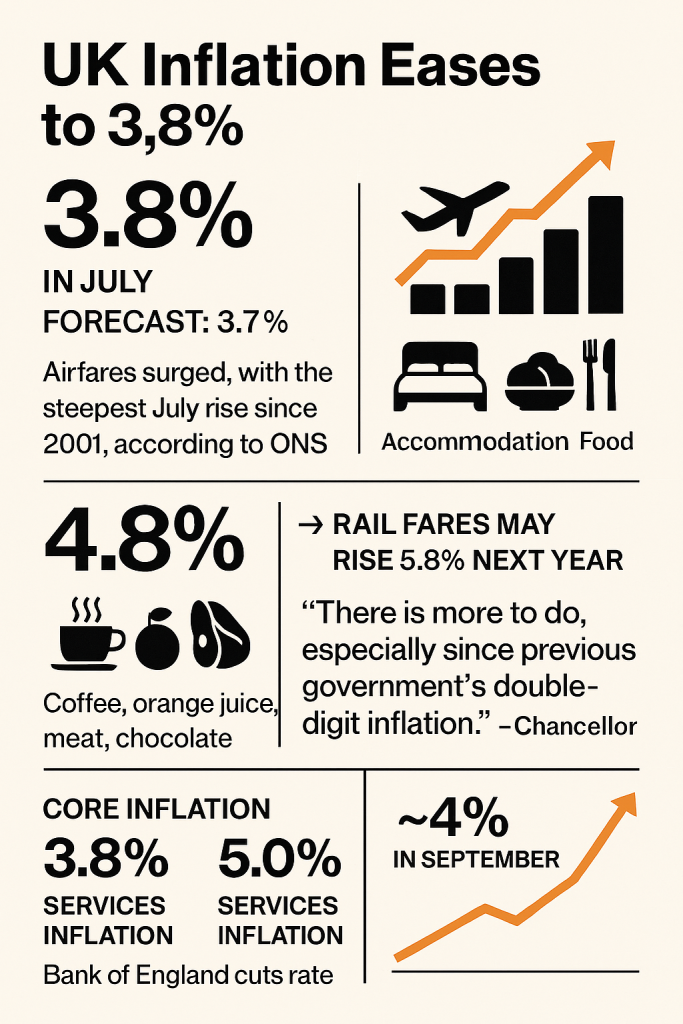

The UK’s annual inflation rate climbed to 3.8% in July, marking its highest level since January 2024 and outpacing economists’ forecasts of 3.7%.

The Office for National Statistics (ONS) attributed the unexpected rise to soaring airfares, elevated accommodation costs, and persistent food price pressures.

Transport costs were the primary driver, with airfares experiencing their steepest July increase since monthly tracking began in 2001.

Analysts suggest the timing of school holidays and a spike in demand—possibly amplified by high-profile events like the Oasis reunion tour—contributed to the surge.

Food inflation also continued its upward trend, with notable increases in coffee, fresh orange juice, meat, and chocolate.

The Retail Prices Index (RPI), which influences rail fare caps, rose to 4.8%, potentially signalling a 5.8% hike in regulated train fares next year.

Core inflation, which excludes volatile items such as energy and food, matched the headline rate at 3.8%, suggesting underlying price pressures remain stubborn.

Services inflation rose to 5%, reinforcing concerns that inflation may be embedding itself more deeply in the economy.

Despite the Bank of England’s recent rate cut to 4%, policymakers face a delicate balancing act. With inflation still nearly double the Bank’s 2% target, further monetary easing may be limited.

UK inflation July 2025 infographic

Chancellor Rachel Reeves acknowledged the challenge, stating that while progress has been made since the previous government’s double-digit inflation, ‘there’s more to do to ease the cost of living’.

Measures such as raising the minimum wage and expanding free school meals aim to cushion households from rising prices.

As inflation edges closer to a projected 4% peak in September 2025, the coming months will test both fiscal and monetary resilience.

In a sweeping rally that spanned continents and sectors, major global indices surged to fresh record highs yesterday, buoyed by cooling inflation data,renewed hopes of U.S. central bank rate cuts, and easing trade tensions.

U.S. inflation figures released 12th August 2025 for July came in at: 2.7% – helping to lift markets to new record highs!

U.S. Consumer Price Index — July 2025

Metric

Value

Monthly CPI (seasonally adjusted)

+0.2%

Annual CPI (headline)

+2.7%

Core CPI (excl. food & energy)

+0.3% monthly, +3.1% annual

Despite concerns over Trump’s sweeping tariffs, the U.S. July 2025 CPI came in slightly below expectations (forecast was 2.8% annual).

Economists noted that while tariffs are beginning to show up in certain categories, their broader inflationary impact remains modest — for now.

Global Indices Surged to Record Highs Amid Rate Cut Optimism and Tariff Relief

Tuesday, 12 August 2025 — Taking Stock

📈 S&P 500: Breaks Above 6,400 for First Time

Closing Level: 6,427.02

Gain: +1.1%

Catalyst: Softer-than-expected U.S. CPI data (+2.7% YoY) boosted bets on a September rate cut, with 94% of traders now expecting easing.

Sector Drivers: Large-cap tech stocks led the charge, with Microsoft, Meta, and Nvidia all contributing to the rally.

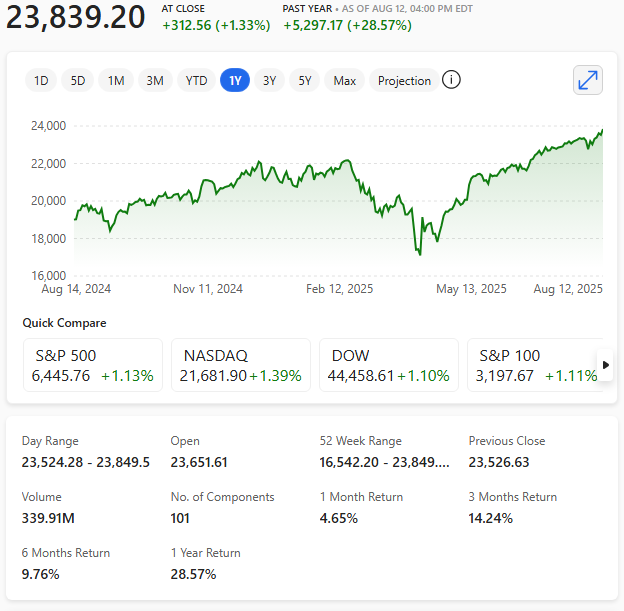

💻 Nasdaq Composite & Nasdaq 100: Tech Titans Lead the Way

Nasdaq Composite: Closed at a record 21,457.48 (+1.55%)

Nasdaq 100: Hit a new intraday high of 23,849.50, closing at 23,839.20 (+1.33%)

Highlights:

Apple surged 4.2% after announcing a $600 billion U.S. investment plan.

AI optimism continues to fuel gains across the Magnificent Seven stocks.

Nasdaq 100 chart 12th August 2025

Nasdaq 100 chart 12th August 2025

🧠 Tech 100 (US Tech Index): Momentum Builds

Latest High: 23,849.50

Weekly Gain: Nearly +3.7%

Outlook: Traders eye a breakout above 24,000, with institutional buying accelerating. Analysts note a 112% surge in net long positions since late June.

🇯🇵 Nikkei 225: Japan Joins the Record Club

Closing Level: 42,718.17 (+2.2%)

Intraday High: 43,309.62

Drivers:

Relief over U.S. tariff revisions and a 90-day pause on Chinese levies.

Strong earnings from chipmakers like Kioxia and Micron.

Speculation of expanded fiscal stimulus following Japan’s recent election results.

🧮 Market Sentiment Snapshot

Index

Record Level Reached

% Gain Yesterday

Key Driver

S&P 500

6,427.02

+1.1%

CPI data, rate cut bets

Nasdaq Comp.

21,457.48

+1.55%

AI optimism, Apple surge

Nasdaq 100

23,849.50

+1.33%

Tech earnings, institutional buying

Tech 100

23,849.50

+1.06%

Momentum, bullish sentiment

Nikkei 225

43,309.62

+2.2%

Tariff relief, chip rally

📊 Editorial Note: While the rally reflects strong investor confidence, analysts caution that several indices are approaching technical overbought levels.

The Nikkei’s RSI, for instance, has breached 75, often a precursor to short-term pullbacks.

On 7th August 2025, the Bank of England’s Monetary Policy Committee voted narrowly—5 to 4—in favour of reducing the base interest rate by 0.25% to 4%, marking its lowest level since March 2023.

This is the fifth rate cut in a year, aimed at stimulating growth amid sluggish GDP and persistent inflation, which currently stands at 3.6%.

Governor Andrew Bailey reportedly described the decision as part of a ‘gradual and careful’ easing strategy, balancing inflation risks with signs of a softening labour market.

While some committee members reportedly advocated for a larger cut, others urged caution, reflecting deep divisions over the UK’s economic trajectory.

The move is expected to ease borrowing costs for homeowners and businesses, with tracker mortgage rates falling immediately. However, savers will be losing out as rates continue to drop.

However, analysts warn that future cuts may hinge on upcoming fiscal decisions and inflation data, leaving the path forward uncertain.

There are increasingly credible signs that U.S. stocks may be heading into a deeper adjustment phase.

Here’s a breakdown of the key indicators and risks that suggest the current stumble could be more than a seasonal wobble. It’s just a hypothesis, but…

S&P 500 clinging to its 200-day moving average: While the long-term trend remains intact, short-term averages (5-day and 20-day) have turned negative.

Volatility Index (VIX) rising: A 7.61% surge in the 20-day average VIX suggests growing unease, even as prices remain elevated.

Diverging ADX readings: The S&P 500’s ADX (trend strength) is weak at 7.57, while the VIX’s ADX is strong at 45.37—classic signs of instability brewing.

🧠 Sentiment & Positioning: Optimism with Defensive Undercurrents

Investor sentiment is bullish (40.3%), but rising put/call ratios and a complacent Fear & Greed Index hint at hidden caution.

Historical parallels: Similar sentiment setups preceded corrections in 2021 and 2009. We’re not at extremes yet, but the complacency is notable.

🌍 Macroeconomic Risks: Tariffs, Fed Policy, and Structural Headwinds

Tariff escalation: Trump’s recent executive order raised effective tariffs to 15–20%, with new duties on rare earths and tech-critical imports.

Labour market weakening: July’s jobs report showed just 73,000 new jobs, with massive downward revisions to prior months. Unemployment ticked up to 4.2%.

Fed indecision: The central bank is split, with no clear path on rate cuts. This uncertainty is amplifying volatility.

Structural drag: Reduced immigration and R&D funding are eroding long-term growth potential.

🛡️ Strategic Implications: How Investors Are Hedging

Defensive sectors like utilities, healthcare, and gold are gaining traction.

VIX futures and Treasury bonds are being used to hedge against volatility.

Emerging markets with trade deals (e.g., Vietnam, Japan) may outperform amid global realignment.

🗓️ Seasonal Weakness: August and September Historically Slump

August is the worst month for the Dow since 1988, and the second worst for the S&P 500 and Nasdaq.

Wolfe Research reportedly notes average declines of 0.3% (August) and 0.7% (September) since 1990.

While the broader market still shows resilience—especially in mega-cap tech—the underlying signals point to fragility.

Elevated valuations, weakening macro data, and geopolitical uncertainty are converging. A deeper correction isn’t guaranteed, but the setup is increasingly asymmetric: limited upside, growing downside risk.

As of June 2025, the U.S. annual inflation rate rose to 2.7%, marking its highest level since February 2025.

This uptick was largely driven by new tariffs imposed by President Trump, which increased costs on goods like furniture, clothing, and appliances.

On a monthly basis, U.S. consumer prices climbed 0.3% from May to June, up from a modest 0.1% increase the previous month.

📊 Core inflation—which excludes food and energy—also edged up to 2.9% year-on-year, with a 0.2% monthly increase, suggesting underlying price pressures are building.

Summary

📈 Headline CPI: rose 2.7% year-over-year

🔍 Core inflation (excluding food and energy) climbed to 2.9% annually

📊 Monthly increases: 0.3% for headline CPI, 0.2% for core inflation

Eurozone inflation edged up to 2.0% in June, aligning precisely with the European Central Bank’s (ECB) target and marking a slight increase from 1.9% in May 2025.

The small rise was largely driven by persistent services inflation, which climbed to 3.3%, and steady increases in food, alcohol, and tobacco prices at 3.1%.

Core inflation, which excludes volatile items like energy and food, held firm at 2.3%, suggesting underlying price pressures remain stable. Energy prices, however, continued to decline, easing some of the broader inflationary strain.

The ECB, having already cut interest rates earlier this year, now faces a delicate balancing act. While inflation appears under control, economic growth remains sluggish, and ongoing trade tensions – particularly with the U.S. – could complicate the outlook.

With inflation now at target, attention shifts to whether the ECB will pause further rate cuts or act again to support the eurozone’s fragile recovery.

Japan has been jolted by a dramatic spike in rice prices, which surged by 101.7% year-on-year in May 2025 – the most significant increase in over fifty years.

This sharp rise in the cost of the country’s staple food has contributed heavily to Japan’s inflation, which jumped to 3.7%, marking its highest point since January 2023.

The Bank of Japan (BOJ) now faces mounting pressure, as this marks the 38th consecutive month inflation has surpassed the Bank’s 2% target.

Notably, the ‘core-core’ inflation rate, excluding fresh food and energy rose to 3.30%, an indication that broader cost pressures are sticking.

The government has begun releasing emergency rice stockpiles in an attempt to dampen prices, but analysts remain cautious.

With rice accounting for nearly half of Japan’s core inflation, its influence stretches well beyond supermarket aisles. A continued rise could affect everything from packaged goods to restaurant prices.

Despite calls for tightening policy, the BOJ has opted to keep interest rates at 0.5%, citing expectations of inflation easing in the coming months.

However, with geopolitical tensions and supply chain factors still looming, the outlook remains uncertain.

Switzerland has officially re-entered an era of zero interest rates, following a 0.25% cut by the Swiss National Bank (SNB) on 19th June 2025.

The move, though widely expected, marks a significant shift in monetary policy as the nation grapples not with inflation – but deflation.

Consumer prices in May dipped 0.1% year-on-year, driven largely by the enduring strength of the Swiss franc.

The SNB cited diminished inflationary pressure as the rationale behind the cut and indicated it remains focused on long-term price stability.

Chairman Martin Schlegel emphasised that short-term negative inflation readings weren’t the primary motivator. Instead, the Bank revised its inflation forecast down to 0.2% for 2025 and 0.5% for 2026.

Switzerland’s strong currency continues to weigh heavily on imported goods prices – an especially potent factor in a small, open economy.

Analysts suggest the SNB may go lower if inflation fails to rise, sparking speculation about a return to negative rates.

This development sets Switzerland apart from other major economies still battling inflation, underscoring the unique challenge of managing deflation in a world accustomed to rate hikes.

The next SNB policy decision is due in September 2025. Until then, all eyes remain on the franc – and the fallout.

U.S. Federal Reserve has kept its benchmark interest rate steady at 4.25% to 4.50% for the fourth consecutive meeting.

This decision reflects a cautious stance amid ongoing uncertainty surrounding President Trump’s tariff policies and their potential impact on inflation and economic growth.

The Fed still anticipates two rate cuts later in 2025, but officials are split – some expect none or just one cut.

Inflation projections have been revised upward to 3.0% for 2025, while economic growth expectations have been trimmed to 1.4%.

U.S. President Donald Trump has been sharply critical of Federal Reserve Chair Jerome Powell, especially following the Fed’s decision on June 18, 2025, to keep interest rates steady.

He’s called Powell ‘a stupid person’, ‘destructive’, and ‘Too Late Powell’. accusing him of being politically motivated and slow to act on rate cuts.

And the Federal Reserve is supposed to act independently of political influence.

In May 2025, U.S. inflation rose by 0.1% from the previous month, bringing the annual inflation rate to 2.4%, slightly below economists’ predictions of 2.5%.

Core U.S. inflation, which excludes food and energy, increased by 0.1% month-on-month, with a year-on-year rate of 2.8%.

The modest rise was largely offset by falling energy prices, particularly a 2.6% drop in petrol, which helped keep overall inflation in check.

Prices for new and used vehicles, as well as apparel, also declined. Meanwhile, food and housing (shelter) costs each rose by 0.3%, with housing (shelter) being the primary contributor to the monthly increase.

Despite President Trump’s sweeping tariffs introduced in April 2025, their inflationary impact has yet to fully materialise. Analysts suggest that many companies are still working through pre-tariff inventories, delaying price hikes for consumers.

However, economists caution that the effects may become more pronounced in the coming months.

The Federal Reserve is expected to hold interest rates steady for now, as U.S. policymakers monitor whether inflation remains contained or begins to accelerate due to trade-related pressures.

Markets responded positively to the data, with stock futures rising and Treasury yields falling.

So, while inflation remains above the Fed’s 2% target, May’s figures suggest a temporary reprieve.