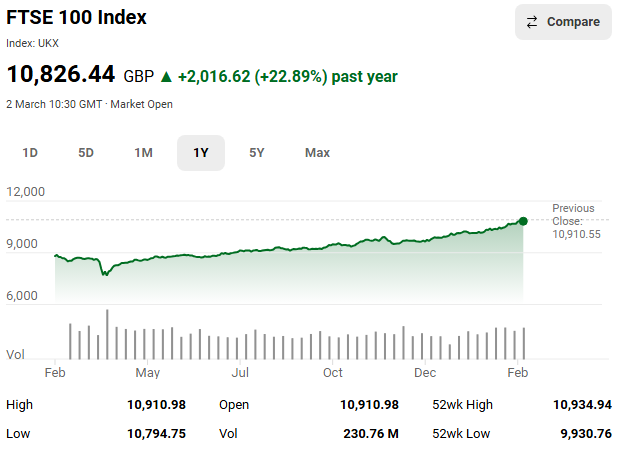

The FTSE 100 closed out last week by breaking through to a fresh all‑time high, underscoring a renewed wave of confidence in UK blue‑chip stocks.

The index ended Friday at 10,910.55, marking a record close after also touching an intra‑day peak of 10,934.94 earlier in the session.

This milestone capped a strong run in which the FTSE 100 repeatedly outperformed its U.S. and European counterparts, buoyed by resilient earnings, firmer commodity prices, and a rotation by investors seeking comparatively lower valuations in London’s market.

Several factors helped propel the index higher. Rising oil and precious‑metal prices supported heavyweight energy and mining constituents, while financials such as HSBC also contributed to the rally with upbeat results and improved outlooks.

Sector mix

Analysts noted that the FTSE’s sector mix—rich in defensives and less exposed to the more volatile AI‑driven tech trade—has offered investors a measure of stability during a period of global uncertainty.

The latest surge leaves the index within striking distance of the 11,000 mark, a level that would have seemed ambitious only months ago.

With the FTSE 100 already up nearly 10% for the year to date, attention now turns to whether this momentum can be sustained as markets digest geopolitical tensions, shifting tariff policies, and the next round of corporate earnings.