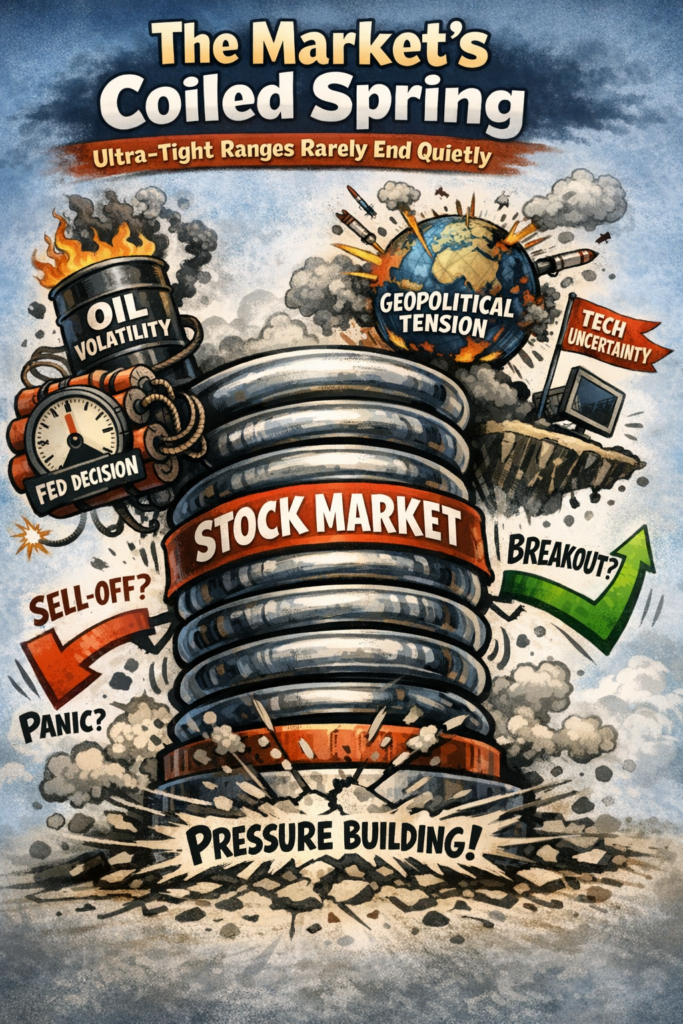

Markets rarely sit still without reason. When they do — as they have in recent sessions, grinding sideways in an ultra‑tight range — it signals not calm but compression.

Price action becomes like a coiled spring: energy building, tension rising, and traders waiting for the moment when restraint snaps into motion.

This week’s narrow trading bands reflect a market holding its breath. Geopolitical tension in the Middle East, oil volatility, and a Federal Reserve decision all loom over investors, yet equities have refused to break down.

Futures are edging higher, European indices are opening firmer, and even the tech wobble — with Nvidia’s muted reaction to its latest showcase — hasn’t derailed broader sentiment

Tight range – a waiting game.

Historically, such tight ranges rarely resolve with a whimper. When volatility is suppressed for too long, the eventual breakout tends to be sharp and directional. The question, of course, is which way.

Right now, the evidence suggests upward. Markets have absorbed war‑driven oil swings, shrugged off hedge‑fund losses, and continued to find buyers on dips.

Breadth is stabilising, and risk appetite — surprisingly resilient given the backdrop — is creeping back into European and Asian sessions.

That doesn’t guarantee a bullish surge, but it does suggest the path of least resistance is higher.

Fed tone

If the Fed avoids surprising investors and signals comfort with the current trajectory, the spring is more likely to uncoil to the upside.

A dovish‑leaning tone could ignite a breakout as sidelined capital rushes back into equities. Conversely, a hawkish shock would release the same stored energy — but violently downward.

The market is coiled. The catalyst is imminent. And when the range finally breaks, it won’t be subtle.

You know, it almost doesn’t matter what disasters are ongoing in the world – the stock market just wants to win and go up!

Just how bad does it have to be before the stock market corrects? And what will be the catalyst to make that happen?

Debt, credit concerns, geopolitical tension, political scandal, Epstein, a rogue nuclear attack, AI failure, war or just another Trump tariff scenario?

Who knows? And does anybody really care as long as ‘making money’ isn’t interrupted.

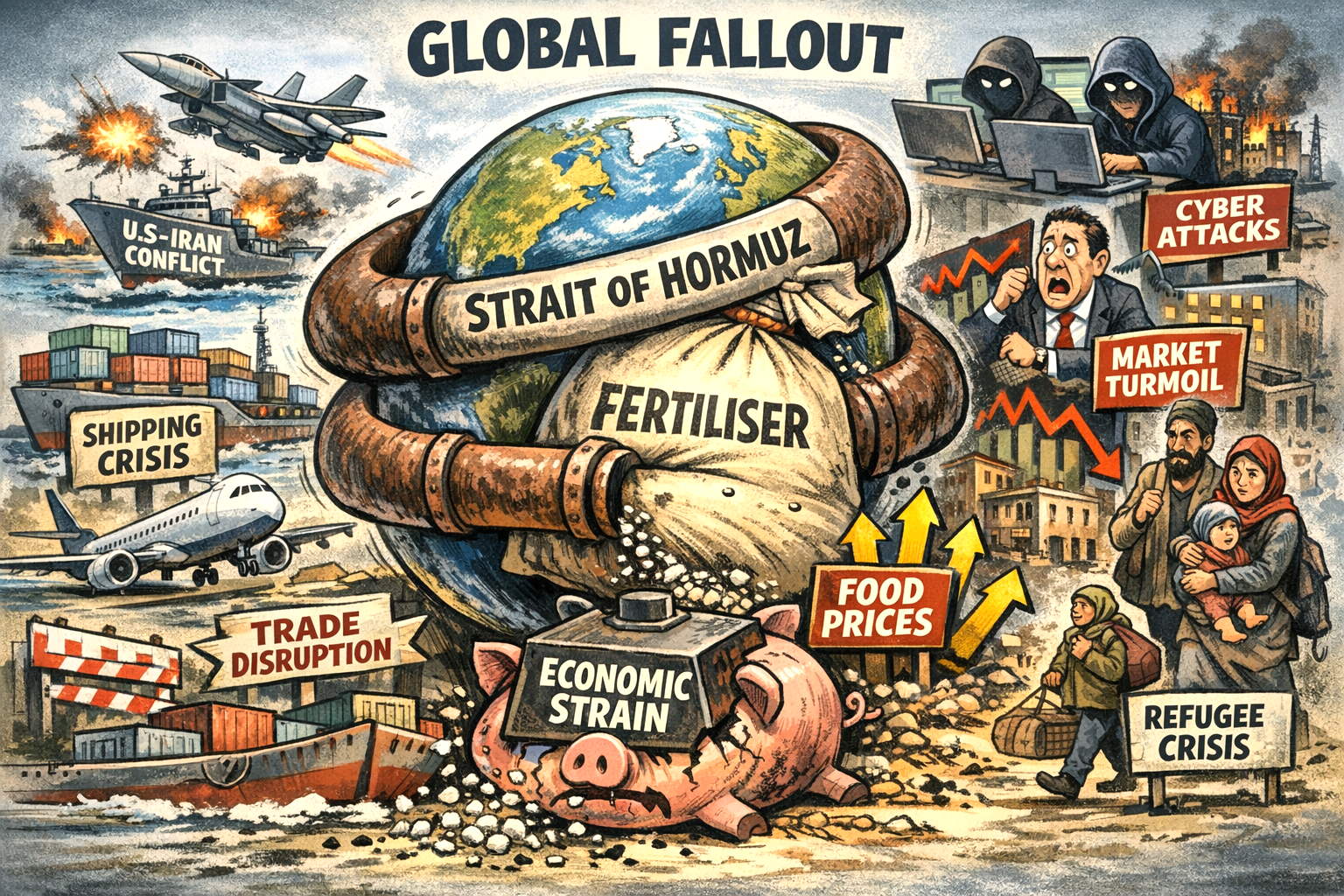

If the U.S.–Iran conflict drags on for weeks or months, the global impact will extend far beyond oil markets. Energy prices are only the first domino.

The deeper, more destabilising effects emerge through shipping disruption, fertiliser shortages, food‑price inflation, financial volatility, cyber escalation, and regional political instability.

For the UK — already wrestling with structural food‑system fragility — the conflict becomes a real‑world stress test.

This report outlines 15 potential major knock‑on effects that would shape the global economy if the conflict becomes protracted.

1. Global Shipping Disruption

The Strait of Hormuz is not just an oil artery; it is a global shipping chokepoint. As vessels reroute or halt operations:

Container shipping delays spread across Asia, Europe and the Gulf.

War‑risk insurance premiums spike for all vessels.

Freight costs rise, feeding into non‑energy inflation.

This is the mechanism by which a regional conflict becomes a global economic event.

2. Aviation and Travel Disruption

Iranian retaliation has already included strikes on Gulf airports and hotels. If this continues:

Airlines reroute or cancel flights across the Gulf, South Asia and East Africa.

Longer flight paths increase fuel burn and fares.

Tourism in the UAE, Oman, Bahrain and potentially Turkey contracts sharply.

Aviation is one of the fastest channels through which geopolitical instability hits consumers.

3. Financial Market Volatility

Markets dislike uncertainty, and this conflict delivers it in abundance.

Investors flee to gold, the dollar and U.S. Treasuries.

Emerging markets face capital outflows.

Equity volatility rises in shipping, aviation and manufacturing sectors.

The longer the conflict persists, the more entrenched this volatility becomes.

4. Fertiliser Disruption: The Hidden Trigger

Over one‑third of global fertiliser trade moves through the Strait of Hormuz. With shipments stranded:

Urea, ammonia, phosphates and sulphur prices surge.

Farmers worldwide face higher input costs.

Lower fertiliser availability leads to reduced crop yields.

This is the beginning of a food‑system shock that unfolds over months, not days.

5. Global Food‑Price Inflation

As fertiliser shortages ripple through agriculture:

Wheat, rice, maize and oilseed yields fall.

Livestock feed becomes more expensive, pushing up meat, dairy and egg prices.

Food‑importing regions face acute pressure.

Grain futures markets become more volatile.

This is how a conflict becomes a global cost‑of‑living crisis.

UK Exposure

The UK is particularly vulnerable because:

It imports a large share of its fertiliser and food.

Its agricultural sector is energy‑intensive.

Supermarket supply chains are sensitive to freight and insurance costs.

Bread, cereals, dairy and meat are the first categories to feel the squeeze.

6. Supply Chain Strain Beyond Food and Energy

A prolonged conflict disrupts:

Petrochemicals

Plastics

Fertilisers

Industrial metals

Gulf‑based manufacturing and logistics

This feeds into higher costs for everything from packaging to electronics.

7. Corporate Investment Freezes

Businesses hate uncertainty. Expect:

Delays or cancellations of Gulf megaprojects.

Slower investment in petrochemicals, logistics and tech hubs.

Reduced appetite for Gulf‑exposed assets.

This undermines diversification efforts like Saudi Vision 2030.

8. Cyber Escalation

Iran has a long history of cyber retaliation. Likely developments include:

Attacks on Western banks, utilities and government systems.

Disruptions to Gulf infrastructure, including airports and desalination plants.

Rising cybersecurity costs for businesses globally.

Cyber conflict is asymmetric, deniable and cheap — making it a likely pressure valve.

9. Regional Political Destabilisation

The killing of senior Iranian leadership has already shaken the region.

Possible outcomes include:

Internal instability within Iran.

Escalation involving Hezbollah, Iraqi militias, Syrian factions and the Houthis.

Pressure on Gulf monarchies if civilian infrastructure continues to be targeted.

This is where the conflict risks widening beyond its initial theatre.

10. Migration and Humanitarian Pressures

If the conflict intensifies:

Refugee flows from Iran, Iraq and Syria could rise.

Europe — especially Greece, Turkey and the Balkans — faces renewed border pressure.

Humanitarian budgets shrink as Western states divert funds to defence.

This adds a political dimension to the economic fallout.

11. Insurance Market Stress

War‑risk insurance is already spiking.

Expect:

Higher premiums for shipping, aviation and energy infrastructure.

Reduced insurer appetite for Gulf‑exposed assets.

Knock‑on effects on global trade costs and consumer prices.

Insurance is a silent amplifier of geopolitical risk.

12. Higher Global Borrowing Costs

Sustained conflict spending creates:

Budgetary strain for the U.S., UK, EU and Gulf states.

Reduced fiscal space for domestic programmes.

Higher global borrowing costs as markets price in sustained uncertainty.

This tightens financial conditions worldwide.

13. Pressure on Emerging Markets

Countries heavily reliant on imported energy or food face:

Worsening trade balances

Currency depreciation

Higher inflation

Greater risk of sovereign stress

This is especially acute in South Asia, North Africa and parts of Latin America.

14. Strain on Multilateral Institutions

A prolonged conflict diverts attention and resources from:

Climate finance

Development aid

Humanitarian relief

Global health programmes

Institutions already stretched by Ukraine, Gaza and climate disasters face further overload.

15. The Strategic Reordering of Alliances

A drawn‑out conflict may accelerate geopolitical realignment:

Gulf states hedge between Washington and Beijing.

India and Turkey pursue more independent foreign policies.

Europe faces renewed pressure to define its own security posture.

Russia benefits from higher energy prices and Western distraction.

This is the long‑term consequence: a shift in the global balance of power.

Conclusion: A Conflict That Radiates Far Beyond Oil

If the U.S.–Iran war limps on, the world will feel it in supermarket aisles, shipping lanes, financial markets and political systems.

The most consequential knock‑on effect is not oil — it is fertiliser. That is the hinge on which global food security turns.

For the UK, the conflict exposes the fragility of a food system dependent on imports, long supply chains and energy‑intensive agriculture.

This is not just a Middle Eastern conflict. It is a global economic event in slow motion.

Many economists stronly believe that India’s stellar economic trajectory alongside strong forecasts for some Southeast Asian countries will be important drivers for future global growth.

The next decade, could see Asia Pacific become the fastest growing region of the world economy. India, Indonesia, the Philippines and Vietnam will most likely be among the world’s fastest growing emerging markets over the next 10 years.

India’s economy grew 7.8% in the June quarter, marking the fastest pace of growth in a year.

The momentum in the Indian economy looks really strong at the moment, economists suggest. Some forecasts expect that India will surpass Japan to become the third largest economy by 2030, with the country’s GDP projected to rise from $3.5 trillion in 2022 to $7.3 trillion by 2030.

As a region, Asia-Pacific’s growth is expected to strengthen from 3.3% last year to 4.2% this year, according to economic projections.

Over the next decade, we expect that about 55% of the total increase in the world’s GDP will come from the Asia-Pacific region.

Where does this leave the U.S. and China?

Still, the U.S. will remain an important driver of the global economy, accounting for some 15% of the world’s growth over the next decade.

China will also still be pivotal in this growth story, contributing to about one-third of the total increase over the same period, analysts suggest. China’s recovery has been weaker than expected and the expected ‘growth momentum’ has wained.

China has been affected by a slew of economic data broadly missing expectations.

As a whole, analysts expect global growth to come in at 2.5% this year and next. But please bear in mind these are forecast and move regularly.

Ashoka Chakra – the Flag of India

The flag of India is a horizontal tricolour of saffron, white and green, with a navy blue wheel called the Ashoka Chakra in the centre. The flag was adopted on 22nd July 1947, after India gained independence from British rule.

It is based on the Swaraj flag, which was designed by Pingali Venkayya and modified by Mahatma Gandhi. The colours and symbols of the flag have different meanings and interpretations.

Saffron represents courage, sacrifice, Hinduism and Buddhism. White represents peace, truth, purity and other religions in India. Green represents faith, fertility, Islam and Sikhism.

The Ashoka Chakra represents the law of dharma, the cycle of life and death, and the ancient Indian emperor Ashoka who spread Buddhism across Asia.

India’s flag is also known as the Tiranga, which means ‘the tricolour’ in Hindi. The flag has a ratio of 2:3 and can only be made of khadi, a hand-spun cloth.

The flag code of India regulates the usage and display of the flag by the government and the public.

Ha Jiang, is a virtual online idol, and only exists online.

Ha Jiang signed a record deal with Whet Records, Warner Music Group’s pan-Asian dance label in China, in 2021. Ha Jiang is the first virtual idol to conduct a record deal with a major label. The virtual idol uses AI technology to create music and has become an online sensation in Asia.

Ha Jiang online music avatar. She is a virtual artist who uses artificial intelligence to create music

Virtual AI artist

Ha Jiang is a virtual artist who uses artificial intelligence to create music. She is the first virtual idol to sign a record deal with a major label, Whet Records, which is Warner Music Group’s pan-Asian dance label in China. My understanding is that the music was composed by humans, so not entirely AI generated then.

Would this also work in west – is it time to be concerned?

She already has more than 100,000 followers in China and is known for her sense of style and fashion. She is also a social influencer who has been hired by the city of Shanghai to promote safe driving. Ha Jiang is not a real person, but a computer-generated avatar who only exists online. She is part of a growing phenomenon of virtual idols in Asia, especially among Gen-Z fans.

Endel,is a sound startup company that uses artificial intelligence to create personalized audio tracks. Endel was the first to sign a record deal with Warner Music Group in 2019 to release 20 albums of ambient music.

Asia is promoting clear crypto rules at a time when large businesses are facing regulatory uncertainty in the U.S.

Some Asian countries that have taken the lead in crypto regulation include Singapore, Hong Kong, Japan, and South Korea. They have proposed or implemented frameworks that protect investors, prevent money laundering, and encourage innovation in the crypto industry.

Lack of clarity in U.S.

In contrast, the U.S. has been singled out for its lack of clarity and consistency in crypto regulation. The SEC for instance and other agencies have different views on how to classify and regulate crypto assets – take alook at the case with XRP and ripple of recent years.

Some industry leaders have threatened to leave the U.S. or sued the regulators over their actions. There is also a debate in Congress that could level crypto transactions with a tax.

Attractive

As a result, some analysts have suggested that Asia could become more attractive to investors and innovators in the crypto industry, as it offers more certainty and stability in the regulatory environment.

However, there are also challenges and risks involved in crypto regulation, such as balancing security and innovation, ensuring compliance and enforcement, and dealing with cross-border issue.